Employee Pension Scheme, shortly and popularly known as EPS, is a social security scheme. Notably, EPS was launched in the year 1995. It provides retirement benefits to the employees who are covered under Employees’ Provident Fund Scheme (EPF).

The present article highlights eligibility criteria for availing benefits under EPS; manner of allocation of employer’s and employee’s contribution towards EPF and EPS; formula to calculate EPS pension and different types of pension in EPS.

Page Contents

Eligibility criteria for availing benefits under EPS –

Employee needs to satisfy the following eligibility criteria for availing benefits under EPS –

- Must be a member of EPFO;

- Must have completed 10 years of service;

- Must have attained age of 58 years in case of regular pension and age of 50 years in case of early pension;

Notably, in case the pension is deferred for two years (i.e. up to the age of 60 years), pensioner will get eligible for an additional pension @ 4% each year.

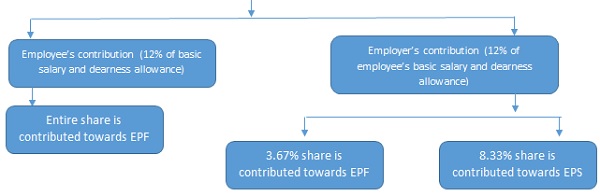

Manner of allocation of employer’s and employee’s contribution towards EPF and EPS –

Employer’s and employee’s contribution and its allocation towards EPF and EPS is simplified hereunder with the help of a flowchart –

Formula to calculate EPS pension –

Formula to calculate EPS pension is –

EPS amount = [Service Period X Pensionable Salary] / 70

Service Period –

Number of years worked in an organisation. Notably, service period under different employers are to be added together. However, employee need to get EPS certificate from earlier employer and submit the same to new employer at the time of switching over of the job.

Importantly, maximum service period considered under EPS scheme is 35 years.

Pensionable Salary –

Average monthly salary (i.e. basic salary + dearness allowance) earned by the employee during the period of last 5 years (60 months) of services.

Let us understand EPS formula with the help of an example –

Suppose, employee has served for 20 years and has pensionable salary of INR 14,000. Then, EPS amount will be –

EPS amount = [20 years * INR 14,000] / 70

EPS amount = INR 4,000 per month.

Different types of pensions in EPS –

Types of pensions in EPS is highlighted hereunder –

- Regular pension –

This is regular pension paid up on retirement at the age of 58 years with completion of at least 10 years of service.

- Early pension –

This is early pension eligible at the age of 50 years with completion of at least 10 years of service. However, in such case, pensioner will get reduced amount.

- Widow pension –

Widow pension is payable to the spouse up on death of the employee. This pension continues till the death of the spouse or remarriage.

- Child pension –

Child pension is payable to the surviving children up to death of the employee. This pension is paid in addition to the widow pension. Pension will be paid till the child attains the age of 25 years and it is paid to a maximum of two children.

- Orphan pension –

Orphan pension is payable when both the employee and his spouse has passed away. It is paid at 75% of the value of widow’s pension.

Also Read:

ITAT direct AO to find Every Month’ Definition in Clause 38 of EPF Scheme from PF/ESI Authority

Supreme Court upholds amended employees’ pension scheme with modifications

Taxation of EPF, Superannuation, Leave Encashment, Gratuity, NPS

ITAT Pune: Re-adjudication on Relief u/s 89 for Employee under ERS Scheme

Employee Pension Scheme for International Workers

Exemption towards commuted value of pension Section 10(10A)

All you want to know about Pension & Its Taxability

All about Employee Pension Scheme in a brief

Author Bio