OBJECTS OF COMPANIES AMENDMENT ACT, 2017

√ Simplification of Compliances and doing away with unnecessary procedures.

√ Lesser regulatory interference and greater self-regulation

√ Clarity in the provisions of the Act.

√ Encouragement for Startups

√ Strengthen Corporate Governance Standard

√ Strict Action against defaulting Companies

√ Transparency

JOURNEY SO FAR

NOTIFIED SECTIONS

IMPACT ON THE SECTIONS

MAJOR IMPACTS

1. “ASSOCIATE COMPANY” [Section 2(6)]{Notified w.e.f. 07th May, 2018} in relation to another company, means a company in which that other company has a significant influence, but which is not a subsidiary company of the company having such influence and includes a joint venture

Explanation. — For the purposes of this clause, “significant influence” means control of at least twenty per cent of total share capital, or of business decisions under an agreement;

| Issue in Definition | Total share capital comprises the aggregate of paid up equity share capital and convertible preference share capital.

Hence a company may be treated as associate company merely bases on ownership of Optionally convertible redeemable preference shares. |

| Amended Provision

|

Significant Influence’ under the definition of Associate Company:

Significant influence to mean control of at least 20% of voting power or control or participation in business decision under an agreement. |

| Implication | After Amendment – To check whether a Company is associate Company or not Only Equity share Capital with Voting Right shall be considered.

This Amendment comes in force to remove the ambiguity of considering Convertible Preference share capital to check status as Associate. |

| Still an Issue | The definition should provide for participation in business decision rather than control thereof. If an investor exercise control over the business decisions, then the company on which the control is exercised is a subsidiary company and not an associate Company. |

Food for Thought::

| As this Section has been notified whether this will impact preparation of financial statement for the F. Y. ended 31.03.2018 |

2. SUBSIDIARY COMPANY….[Section 2(87)]{ Notified w.e.f. 07th May, 2018}

“Subsidiary company” or “subsidiary”, in relation to any other company (that is to say the holding company), means a company in which the holding company

(ii) Exercises or controls more than one-half of the total share capital either at its own or together with one or more of its subsidiary companies

| Issue in Definition | This definition also results in issues/challenges similar to those for the definition of the term ‘Subsidiary Company’. |

| Amended Provision | Exercise or control more than one half of the Total Voting Power |

| Implication | To Check relationship of Holding Subsidiary only Equity Share Capital with Voting Right shall be consider. Preference Share Capital shall not consider. |

| Alignment | This will align ‘subsidiary’ definition under the 2013 Act with AS 21 Consolidated Financial Statement. However, it will continue to be different from definition under Ind As. |

| Definition in Ind AS | Under Ind AS an option to convert to equity shares would be considered for deciding if a company is a subsidiary, provided the option is substantive and exercisable when the relevant decisions are to be taken. |

Food for Thought::

| Company A and B together incorporate a Company ‘C” whether such ‘C’ shall be consider as joint venture Company. If yes Why? If Not Why? |

3. HOLDING COMPANY: [Section 2(46)]{ Notified w.e.f. 09th Feb, 2018}

Holding Company”, in relation to one or more other companies, means a Company of which such companies are subsidiary companies;

| Ambiguity | Unlike the definition of the term ‘subsidiary company’, this definition does not contain any reference to a body corporate. |

| Amended Provision

|

The definition of the term ‘Holding Company’, the expression “Company” includes any “Body Corporate”. |

Quick Question:

| Whether Foreign Parent Shall be considered as Holding Company or Not ? |

—

| Whether LLP Shall be Considered as Holding Company or Not ? |

—

| Implication | LLP/ Foreign Co. etc to be considered as ‘Holding Company” if holds more than 50% of voting right in any Company. |

| We believe it is a minor amendment aimed at correcting an anomaly. It should not have significant financial reporting implication. | |

4. DEBENTURE[Section 2(30)]{ Notified w.e.f. 09th Feb, 2018}debenture’ includes debenture stock, bonds or any other instrument of a company evidencing a debt, whether constituting a charge on the assets of the company or not.

| Ambiguity | the phrase ‘any other instrument of a company evidencing a debt’ has made the definition very broad and included instruments such as commercial papers and other money market instruments, which are often used as an important short-term fund raising source by eligible companies and are well regulated under the RBI regulations |

| Amended Provision | the term debenture will not include the following:

I. Instruments referred to in Chapter III-D of the Reserve Bank of India Act, 1934. Chapter III-D of the RBI Act regulates transaction in derivatives, money market instrument, securities etc. Money market instruments include call or notice money, term money, repo, reverse repo, certificate of deposit, commercial usance bill, commercial paper and such other debt instrument of original or initial maturity up to one year as the RBI may specify from time to time. II. Such other instrument, as may be prescribed by the Central Government in consultation with the RBI. |

| Implication | The term ‘debenture’ will not include money market instruments, which are used for short- term fund raising by eligible Companies and are regulated under the RBI regulations. |

5. FINANCIAL YEAR [Section 2(41)]{ Notified w.e.f. 09th Feb, 2018}

Uniform Financial Year

Section 2 (41) of the 2013 Act required companies, except specified International Financial Services Centre (IFSC) companies, to adopt a uniform accounting year ending 31 March.

However, a proviso to the definition states that a company may apply to the National Company Law Tribunal (Tribunal/NCLT) for adoption of a different financial year if it satisfies the following two criteria:

- It is a holding or subsidiary of a company incorporated outside India.

- It is required to follow a different financial year for consolidation of its financial statement outside India.

| Ambiguity | Companies which are associates or joint ventures of a company incorporated outside India did not have right to approach the NCLT for adopting a different financial year-end, though their financial statements were also taken into consideration in the preparation of CFS outside India |

| Amended Provision | Associate company of a company incorporated outside India can also apply to the NCLT for a different financial year. Hence, the relief will apply to joint ventures also. |

—

| Companies which are associates or joint ventures of a company incorporated outside India can now approach the NCLT for adoption of a different financial year. |

6. KEY MANAGERIAL PERSONNEL….[Section 2(51)]{ Notified w.e.f. 09th Feb, 2018}

“Key Managerial Personnel”, in relation to a company, means—

(i) The Chief Executive Officer or the managing director or the manager;

(ii) The Company Secretary;

(iii) The whole-time director;

(iv) The Chief Financial Officer; and

| Amended Provision

|

To include (v) “such other officer not more than one level below the directors who is in whole time employment and designated as KMP by the Board |

| Implication | Board of Directors can appoint a person one level below Director also as KMP. |

Which person shall be considered as one level below the Directors?

7. NET WORTH….[Section 2(57)]{ Notified w.e.f. 09th Feb, 2018}

“net worth” means the aggregate value of the paid -up share capital and all reserves created out of the profits and securities premium account, after deducting the aggregate value of the accumulated losses, deferred expenditure and miscellaneous expenditure not written off, as per the audited balance sheet, but does not include reserves created out of revaluation of assets, write-back of depreciation and amalgamation

| Amended Provision | To include “AND the Debit or Credit balance of Profit and Loss account in the calculation of Net Worth”. |

| Implication | Credit balance of P&L will increase the net worth and

Debit balance of P&L with decrease the net worth |

| Net worth of Company reflects the ‘intrinsic value’. Hence this is a clarificatory change, one that was important to make. | |

8. TURNOVER….[Section 2(91)]{ Notified w.e.f. 09th Feb, 2018}

“Turnover” means the aggregate value of the realization of amount made from the sale, supply or distribution of goods or on account of services rendered, or both, by the company during a financial year.

| Ambiguity | From the definition, it was not clear whether indirect taxes such as excise duty/Goods and Services Tax (GST) will be included in or excluded from turnover |

| Example: . From a financial reporting perspective, a company collects GST on behalf of the Government and therefore it is excluded from revenue. Consequently, it was not clear whether the determination of turnover under the 2013 Act will be in line with the financial statements or it will be the gross amount received from customer. | |

| Amended Provision

|

Turnover to mean the gross amount of revenue recognized in the profit and loss account from the sale, supply, or distribution of goods or on account of services rendered, or both, by a company during a financial year |

| Implication | Net of Taxes to be Considered. (revenue included GST) Hence, going forward, revenue recognized in the financial statements will be turnover under the statute as well |

“Turnover” means the aggregate value of the realization of amount made from the sale, supply or distribution of goods or on account of services rendered, or both, by the company during a financial year.

9. OTHER DEFINITIONS…

| Small Company

[Section 2(85)] Notified 09.02.2018 |

To Check the status of Company as Small or not “Turnover should be as per profit and loss account for the immediately preceding financial year” and not as per its last financial year. |

| Cost Accountant

[Section 2(28)] Notified 09.02.2018 |

Cost Accountant means a person who is a member of the Institute of Cost Accountants of India and who hold a Valid Certificate of Practice. |

Amendment in Sections

A.

New Section 3A- Members Severally Liable certain Cases:

{Notified w.e.f. 9th February, 2018}

In case Number of Members reduced from Statutory Minimum i.e. 2 in case of Private Limited Company or 7 in case of Public Limited Company, Company carry business for more than 6 month.

Then the member shall be liable for the payment of the whole debts of the Company contracted during that time.

This Section was there in the Companies Act, 1956 Section 45 but was missing from the Companies Act, 2013.

B. PACT ON INCORPORATION OF COMPANY:

I. Alteration in Period of reservation of Name –Section 4(5)(i) – Memorandum:: {Notified}

As per CAA-2017, the name shall be preserved for the following period:

- In case of Incorporation of New Company:Name shall be reserved for the 20 days from the date of approval. (earlier it was available for 60 days)

- In case of Change of Name:Name shall be reserved for the 60 days from the date of approval.

II. Affidavit by Subscriber – Section 7:: {Notified w.e.f. 27thJuly, 2018}

At the time of incorporation of the company, declaration by each subscriber will be required to be attached instead of an affidavit, as currently provided.

III. Registered Office – Section 12::{Notified w.e.f. 27th July, 2018}

The company shall within 30 days of its incorporation have registered office instead of current requirement to have registered office on and from the 15 day of its incorporation

Notice of Every Change of the situation of the registered office shall be given to the Registrar within 30 days instead of 15 days.

IV. Authentication of Documents [Section 21]:: {Notified w.e.f. 9thFeb, 2018}

The change permits Board to authorise any officer or employee of the company for authentication of documents, proceedings and contracts of the Company.

Earlier, any Key Managerial Personnel duly authorized by Board only can authenticate the documents, proceedings and contracts of the Company.

C. IMPACT ON CHARGES:

a. Exemption List of Charges [Section 77]::{Notified w.e.f. 07th May, 2018}

This section shall not apply to certain charges, as may be prescribed by the Central Government in consultation with the Reserve Bank of India.

(Like: Hypothecations, Pledge etc.)

Food for Thought::

- Whether Company need to create Charge on Hypothecation of Agreement i.e. purchase of Vehicle?

- Whether director of Company has given his property as security for the loan to Company. Whether charge will create on such security or not?

b. Time Period for Satisfaction of Charges [Section 82]::{Notified w.e.f. 05th July, 2018

Timeline for filing of satisfaction of charge is to be increased to 300 days on payment of additional fee. (Same as creation of charge)

1. Maximum No. of persons to whom offer can be made:

- An offer can be made under a Private Placement Offer Letter to not more than 2000 people in a financial year.

- The 20 people limit excludes Qualified Institutional Buyers and Employeesof the Company being offered securities under a scheme of employee stock option in terms of provision of clause (b) of sub section 62(1)

Question:

A. Whether Limit of 200 persons shall be calculated individually/ jointly for each type of securities?

The restriction of 200 persons would be reckoned ‘Individually’ for each kind of security that is ‘Equity Shares, Preference Shares or Debentures’.

2. Right of Renunciation:

The Private Placement offer shall not carry any renunciation right. Only the person in whose name offer letter issued can apply for the subscription.

3. Modes for Payment of Subscription Money:

Subscription money shall be paid either by cheque or demand draft or other banking channel or not by cash. Shares under Private Placement can’t be subscribed by payment in cash.

4. Use of Allotment Money:

A company shall not utilize monies raised through private placement unless allotment is made and the return of allotment (i.e. e-form PAS-3) is filed with the Registrar in accordance with sub-section (8).

This is major change by Amendment Act, 2017. After amendment without filing of e-form PAS-3 for allotment of Shares Company can’t use the funds received from subscription.

Food for Thought::

What shall be the implication if Company use money, before filing of e-form PAS-3?

5. No further offer till completion of earlier offer:

No offer or invitation of security shall be made unless allotments with respect to offer or invitation made earlier in respect of any other kind of security in completed.

6. Separate Bank Account:

The money so received shall be kept in a separate bank account of the company and utilized only for allotment (or repayment).

7. No need of filing of PAS-4 and PAS-5:

There is no need to file GNL form with ROC for Offer Letter in PAS-4 and PAS-5.

8. If not allotted within 60 days:

If allotment is not made within 60 days then till 75th day the monies have to be repaid. Failure to repay has a liability of interest at 12% pa.

b) Allotment of Share at Discount- Section 53::{Notified w.e.f. 9th February, 2018}

Issuance of shares at discount allowed, subject to the same is issued to creditors when debt is converted into shares in pursuance of any statutory resolution plan or debt restructuring scheme in accordance with any guidelines or directions or regulations specified by Reserve Bank of India under the Banking Regulation Act, 1949 or the Reserve Bank of India Act 1934.

c) Issue of Sweat Equity Shares- Section 54::{Notified w.e.f. 07th May, 2018}

It is allowed issue of sweat equity shares at any time after registration of the Company.

Food for Thought::

To whom Company can issue Sweat Equity Shares?

d) Right Issue of Shares- Section 62::{Notified w.e.f. 07th May, 2018}

The change in the provision relates to the mode of sending the notice for rights offer. Section 62(2) has been relaxed to include courier or other modes of delivery capable of providing proof of delivery.

Right issue of offer letter can be sent through courier also.

E. ANNUAL RETURN

i. The requirement of extract of annual returnto the board‘s report in Form MGT-9 has been omitted.

ii. Sufficient that the web-link of the annual returnbe disclosed in the board‘s report.

iii. Requirement related to disclosing indebtednessomit from the Annual Return.

iv. Changed in theparticular of Annual Return

v. The Central Government may prescribe abridged form ofannual return for One Person Company (‘OPC’), Small Company and such other class or classes of companies as may be prescribe.

- Whether shares are listed on stock exchange

- Particular of Holding Or Subsidiary Companies

- Remuneration to Directors or Key managerial Personnel

- Net worth

- Turnover

Food for Thought::

As this Section has been notified whether this will impact Annual Filing for the F. Y. ended 31.03.2018

vi. Removal of reference of Section 403:{Notified w.e.f. 07th May, 2018}

Due to this amendment Companies shall be required to file the Annual Return within 60 day of AGM from 61st day it shall be considered as default. Now the additional time period of 270 days removed from this sub section.

Impact of this Amendment:

In case of company fails to file Annual return within 60 days of AGM

i. Company and the officer shall be liable to fine from the 61stday itself.

ii. Additional fees shall be Rs. 100/- per day from 61stDay in case of one time default.

iii. Additional fees shall be double from 61stDay in case of continue default more than once.

Food for Thought:

What shall be impact on Private Limited Companies if they fail to file Annual Return within 60 days of AGM?

F. General Meeting:

Annual General Meeting- Section 96:: {Notified w.e.f. 13th June, 2018}

Annual General Meeting (‘AGM’) of unlisted company may be held at any place in India if consent is given in writing or by electronic mode by all the members in advance.

Extra- Ordinary General Meeting- Section 100:: {Notified w.e.f. 07th May, 2018}

Extraordinary General Meeting (‘EGM’) of wholly owned subsidiary of a company incorporated outside India can be held outside India.

Convening of general meetings at a shorter notice i.e. – Section 101:: {Notified w.e.f. 07th May, 2018}

- In case of an annual general meeting with the consent of at least 95% of the members entitled to vote thereat and

Food for Thought::

As this Section has been notified whether this will impact Annual Filing for the F. Y. ended 31.03.2018

- In case any other general meeting with the consent of at least majority in number (i.e. more than 50%) and 95% (ninety five percent) of such part of the paid up share capital of the company giving a right to vote at such a meeting.

G. Statutory Auditor:

{Notified w.e.f. 7th May, 2018}

The auditor of a company is appointed by the shareholders at the AGM, for a consecutive period of five years. However, the appointment needs to be ratified each year at the AGM. The 2013 Act was silent on the implications of non-ratification of the auditor appointment at the AGM. In the absence of clarity, the following two views were possible:

- If shareholders do not ratify the appointment of the auditor at the AGM, it would tantamount to removal of the auditor from the office.

- Section 140(1) of the 2013 Act requires that the auditor appointed under section 139 can be removed from its office before the expiry of term only by passing a special resolution of the company at the AGM and after obtaining previous approval from the Central Government

However, The Committee was of the view that a company should not be allowed to remove the auditor merely by non-ratification at the AGM. Rather, it should be required to follow procedures for removal of the auditor before the completion of the five-year term, viz., special resolution at the general meeting and approval from the Central Government

- Ratification of Auditor- Section 139:: {Notified w.e.f. 07thMay, 2018}

The requirement related to annual ratification of appointment of auditor by members is omitted. This change will avoid potential conflict between two requirements and is supportive of auditor independence

Food for Thought::

What shall be impact of this Amendment on resolution of Annual General Meeting?

This provision is supportive to auditor independence.

- Access of Accounts of Associate Company::

Earlier Holding Company could have the right to access records of associate companies. Auditors of holding company can have access records of associate companies also along with subsidiaries Companies

- Qualification & Disqualification of Auditor- Section 141:: {Notified w.e.f. 09thFebruary, 2018}

A person who, directly or indirectly, renders any service referred to in section 144 to the company or its holding company or its subsidiary company will not be eligible for appointment as Auditor.

Services u/s 144(1)

(a) accounting and book keeping services;

(b) internal audit;

(c) design and implementation of any financial information system;

(d) actuarial services;

(e) investment advisory services;

(f) investment banking services;

(g) rendering of outsourced financial services;

(h) management services; and

(i) any other kind of services as may be prescribed

Food for Thought::

Before notification of this provision, if any person was providing these services to Holding/ Subsidiary Companied then what should be the course of Action for the Auditor and Company?

There will be no restrictions in rendering these services to another companies.

- Fine in case of failure to file resignation by Auditor in ADT-3 reduced to 50,000/- or the remuneration of auditor whichever is less.

H. Director:

- For the purpose of Resident Director 182 days to be computed with reference to Financial Year. However, 182 days stay in India in the current financial year and not the previous financial year.{Notified w.e.f. 07th May, 2018}

Food for Thought::

If a person appointed as Director in Month of October then how to calculate the resident status of Director.

- In case of New Companies requirement of 182 days shall apply proportionately at the end of the financial year. {Notified w.e.f. 07th May, 2018}

Suggestion: Companies will need to plan in advance so that they are compliant with this requirement at the end of the financial year. In some cases, they may even need to enter into an arrangement with one or more directors so that they stay in India for a minimum 182 days in the financial year.

The requirement of deposit of rupees one lakh with respect to nomination of directors shall not be applicable in case of appointment of independent directors or directors nominated by nomination and remuneration committee or a director recommended by the Board of Directors of the Company, in the case of a company not required to constitute Nomination and Remuneration Committee. (Section 160){Notified w.e.f. 09th Feb, 2018}

Food for Thought::

Whether Private Companies required to deposit Rs. 100,000/- for appointment of new director?

- Directorship in the Dormant Company shall not be including in the limit of 20 Companies.

- Filing of e-form DIR-11 by retiring Director is Optional. (Section 168) {Notified w.e.f. 07th May, 2018}

- A person holding directorship in the Company can’t appoint as alternate Director. (Section 161) {Notified w.e.f. 07th May, 2018}

- Companies may fill casual vacancy by the Board and casual vacancy filed by the Board shall be subsequently approved in the immediate next general meeting. (Section 161) {Notified w.e.f. 09th Feb, 2018}

- Disqualification for appointment of Director Section 164:{Notified w.e.f. 07th May, 2018}

When a Director is appointed in Company which is in default of filling of Financial statement or annual return or repayment of deposits or pay interest or redemption or debentures or payment of interest or redemption of debentures payment of interest thereon or payment of dividend such director shall not incur the disqualification for a period of 6 month from the date of his appointment.

- Vacancy of Office of Director Section 167.{Notified w.e.f. 07th May, 2018}

If the Director incurs disqualification mentioned in section 164(2), then he shall vacant office in all the Companies other than the Company which is in default.

I. Board Meeting:

a) Presence through video Conferencing: (Section 173){Notified w.e.f. 07th May, 2018}

Where there is quorum in a meeting through physical presence of directors, any other director may participate through video conferencing or other audio visual means in such meeting on any matter specified under the first proviso (i.e. restricted matters).

Restricted Matters:

(i) the approval of the annual financial statements;

(ii) the approval of the Board’s report;

(iii) the approval of the prospectus;

(iv) the Audit Committee Meetings for consideration of financial statement

(v) the approval of the matter relating to amalgamation, merger, demerger, acquisition and takeover

b) Audit Committee: (Section 177){Notified w.e.f. 07th May, 2018}

Only Every Listed Public Company shall constitute Audit Committee. Companies listed due to debenture listing not required Audit Committee.

c) Nomination & Remuneration Committee:(Section 178) {Notified w.e.f. 07th May, 2018} Only Every Listed Public Company shall constitute Nomination & Remuneration Committee. Companies listed due to debenture listing not required Nomination & Remuneration Committee.

J. Director Report

{Notified w.e.f. 31stJuly, 2018}

- The requirement of the extract of the annual return in Form MGT-9 to be included in the board‘s report has been omitted, instead web address or link of the annual return to be provided in Board Report.

Food for Thought::

Whether Companies required preparing MGT-9 in relation to Annual Filing for the F.Y. ended 31.03.2018?

- Disclosures which have been provided in the financial statement shall not be required to be reproduced in the report again (like: Section 186, 188)

- Instead of exact text of the policies, key feature of policies along with its web link shall be disclosed in Board report.

- Abridge Board Report for Small Companies and OPC

Disclosures to be mentioned in Directors’ Report:

a) The web address, if any, where annual return referred to in sub-section (3) of section 92 has been placed;

b) Number of Meeting of Board of Directors

c) Directors responsibility statement as referred in sub-section 5 of section 134

d) Details in respect of frauds reported by auditors under sub-section (12) of section 143 other than those which are reportable to the Central Government.

e) Explanations or comments by the Board on every qualification, reservation or adverse remark or disclaimer made by the auditor in his report.

f) The state of the Company’s affairs;

g) The financial summary and highlights;

h) Material changes from the date of closure of the financial year in the nature of business and their effect on the financial position of Company.

i) The details of directors who were appointed or have resigned during the year;

j) The details or significant and material orders passed by the regulators or courts or tribunals impacting the going concern status and company’s operation in future.

K. Financial Statement:

- Sign of Financial Statement: {Notified w.e.f. 07thMay, 2018}

CEO whether appointed as director or not will sign the financial statement. Therefore, now onwards CS, CFO and CEO all three are required to sign the financial statement mandatory.

Food for Thought::

Whether it is mandatory for the Directors of the Company to sign financial statement in case Company having CEO/CFO or CS?

As this Section has been notified whether this will impact Annual Filing for the F. Y. ended 31.03.2018

- Unaudited Foreign Subsidiary financials:

Allowed the filing of unaudited financial statements of foreign subsidiary which is not required to get its accounts audited along with a declaration to that effect.

- Placement of Financial of Subsidiary on website:

Only listed Companies having a subsidiary or subsidiaries will be required to place separate audited accounts in respect of each of subsidiary on their website, if any. This requirement will not apply to non-listed Companies.

- Inspection of Subsidiary Financials:

Both listed and non-listed companies will be required to provide subsidiary financial statements to a member of the Company who asks for it.

- Removal of reference of Section 403:Due to this amendment Companies shall be required to file the Financial Statement within 30 day of AGM from 31st day it shall be considered as default. Now the additional time period of 270 days removed from this sub section.

In case of company fails to file Financial Statement within 30 days of AGM Company and the officer shall be liable to fine from the 31st day itself.

L. DEPOSIT (Section 73-76)

{To be notified w.e.f. 15th August, 2018}

- A Company accepting deposit will be required to deposit and keep in a schedule bank the amount which is not less than 20% of the amount of deposits maturing during the current financial year.

There will be no need to deposit any amount in respect of deposits maturing in the next financial year.

- Deposit Insurance:Requirement of providing Deposit Insurance Omit.

- The Companies Law Committee observed that this requirement was too harsh on companies which may have defaulted due to reasons beyond their control, such as industry conditions at some point of time in the past but have repaid such deposits with earnest efforts thereafter. Imposing a lifelong ban for a default anytime in the past would be inappropriate.

- Company which had defaulted in repayment of deposits can also accept deposit after a period of 5 years from the date of making good the default.

M. Loan to Director:

Notified w.e.f. 07thMay, 2018}

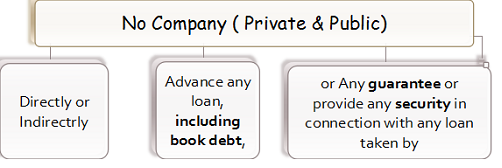

Section 185 has been completely re-written under the Companies Amendment Act, 2017. This Section limits the prohibition on loans, advances, guarantee, Security etc., to any person in which any of the directors are interested.

New amended Section 185 (1)

- Any director of Company, or of a Company which is its Holding Company or

- any partner or relative of any such director; or

- Any firm in which any such director or relative is partner.

However, following loan can be given by company to any person in whom directors are interested after fulfilling the conditions mentioned below:

- Advance any loan, including loan represented by a book debt

- Give any guarantee

- Provide any security in connection with any loan taken

Conditions:

a) Special Resolution passed by the Company in General Meeting

b) The loans are utilized by the borrowing company for its principal business activities.

Sub-section 3: Nothing contained in sub-section (1) and (2) shall apply to–

Clause (a): Loan to Managing Director & Whole Time Director:

There are two ways to give Loan to Managing and Whole Time Director. The exception is extended to a particular class of directors, i.e. to the managing or whole-time directors only.

i. Loan can be given to a Managing or Whole-Time Director as a part of the condition of their service.

Condition: Conditions should be available for all the employees of the Company.

ii. Loan can be given to a Managing or Whole-Time Director pursuant to any Scheme.

Condition: Scheme should be approved by Shareholders by passing of Special Resolution.

Example: The Companies pass a resolution for appointment of Managing Director and it approves the terms and conditions of its appointment and if as a part of its terms, there is a loan which can be given to that director, then it falls under the exception given in section 185 of the Act.

Clause (b): Loan in Ordinary Course of Business:

A company which in the Ordinary Course of its business provides:

– Loans or

– Gives guarantees or

– Securities for the due repayment of any loan and

– In respect of such loans an interest is charged at a rate not less than the rate of prevailing yield of one year, three year, five year or ten year government security closest to the tenor of the loan; or.

Clause (c): Loan by holding Company to its wholly own subsidiary Company:

Any loan made by a Holding Company to its Wholly own Subsidiary Company or any guarantee given or security provided by a Holding Company in respect of any loan made to its wholly own subsidiary Company.

Clause (d): Guarantee and Security by holding Company to its subsidiary Company:

Any guarantee given or security provided by a Holding Company in respect of Loan made by any Bank or financial institution to its subsidiary Company.

Condition: loan made under this clause utilized by the subsidiary company for its principal business activity only.

Section 186: {Notified w.e.f. 07th May, 2018}

For the purpose of this section excludes employees so that loan given to them part of condition of service are not covered under this section.

Wholly own Subsidiary:

No need to pass Special Resolution in case of Loan/ Guarantee/ Security provides by a Company to its Wholly Own Subsidiary Company.

A. List of Restricted Person:

A Company can’t give Loan/ Guarantee/ Security to following below mentioned person:

I. Not Allowed

i. Any director of Company, or

ii. Any director of a Company which is its Holding Company, or

iii. Any partner of Director of lender company, or

iv. Any relative of Directors of Lender Company, or

v. Any firm in which any of Director of Lending Company is Director, or

vi. Any firm in which any relative of Director of lending Company is Director

II. Not Allowed if fails to pass special resolution:

i. Any Private Company of which any such Director is a Director or member;

ii. Body Corporate in which 25% or more voting power rests with one or more directors;

iii. Body Corporate whose Board accustomed to act on directions of BOD or Directors of lending company

B. List of Permissible Person:

III. Allowed if, Special Resolution Passed:

i. Any Private Company of which any such Director is a Director or member;

ii. Body Corporate in which 25% or more voting power rests with one or more directors;

iii. Body Corporate whose Board accustomed to act on directions of BOD or Directors of lending company

Note:

Loan to above mentioned entities are allowed after fulfilling below mentioned both conditions:

i. Special Resolution passed by the Company in General Meeting.

ii. The loans are utilized by the borrowing company for its principal business activities.

IV. Allowed without falling u/s 185(1) and (2):

i. Loan to Managing Director or Whole Time Director.

ii. L/G/S under ordinary course of business.

iii. L/G/ S to wholly owned subsidiary Company

iv. Loan to Subsidiary Company.

V. Allowed without falling u/s 185:

i. Loan to any Public Company (having common Director/ Shareholder or not).

ii. Private Company fulfilling all 3 conditions mentioned in Exemption Notification dated: 05thJune, 2015.

iii. Guarantee / Security provided for the purpose other than loan taken by other entity.

iv. Loan to Holding Company (subject to condition that holding Company doesn’t have common directors)

v. Loan to Subsidiary Companies (subject to condition that subsidiary Company doesn’t have common directors)

Note:

Above mentioned entities are not fall u/s 185, therefore Company can give Loan/ Guarantee/ Securities to above mentioned entities freely without any restriction / compliance of Section 185.

N. Change in Filing Fees:

{Notified w.e.f. 07thMay, 2018}

A. Additional Late Filing Fees:in sub-section (1), for the first and second provisos, the following provisos shall be substituted:

Effect of new proviso:

If Company fails to file Annual Return u/s 92 and Financial statement u/s 137 within time prescribed under their specific sections “without prejudice to any other legal action or liability under this act,” it may be submitted by payment of additional fees “which shall not be less than INR 100/- (Rupees Hundred) per day” and different amount may be prescribed for different classes of Companies.

- If company fails to file any other documents, facts, information etc other than section 92 and 137 “without prejudice to any other legal action or liability under this act,” it may be submitted by payment of additional fees as may be prescribed.

HIGHER ADDITIONAL FEES: New concept of higher additional fees has been introduced. As per this proviso

– Where there is default on Two or More occasions in submitting, filling, registering, recorded of documents,

– without prejudice to any other legal action or liability under this act,

– may be file with “Higher Addition Fees”

– as may be prescribed and

– which shall not be lesser than “twice the additional fee provided under first and second proviso”

Due to above mention proviso if company fails to file any form with in time prescribed under its specific section and company made the default TWO or “MORE OCCASION” then additional fees for filing of from shall be “TWICE of ADDITIONAL FEES

In case Companies fails to file Annual forms for Any Previous Financial years whether under Companies Act, 1956/ 2013 till 30th June, 2018. In such case Company have to pay additional fees as per these rules.

Following below mentioned annual filing forms:

| S. No. | Forms | Purpose of Filing | Section Involved | |

| 1. | AOC-4

(including AOC-4 XBRL, AOC-4 CFS 23AC,ACA) |

Filing of Financial Statements | Section 137 | Within 30 days of AGM |

| 2. | MGT-7

(Including 20B) |

Filling of Annual Return | Section 92 | Within 60 days of AGM |

What shall be additional Fees in above mentioned Situation?

A. Filing of Annual Form for f.y. ended on or before 31stMarch, 2018

B. Company having capital of Rs. 100,000/- and date of AGM 30.09.2018.

Additional Fees shall be as follow:

| Actual Filing Date | Actual Fees | Total

Till 29th October |

From 1st October, 2018 Rs. 100/- per day | Total Fees |

| 29th October, 18 | Rs. 300 | 300 | 0 | 300 |

| 30th October, 18 | Rs. 300 | 300 | 100 | 400 |

| 28th November, 18 | Rs. 300 | 300 | 3,000 | 3300 |

| 28th December, 18 | Rs. 300 | 300 | 6000 | 6300 |

O. Remuneration to Managerial Personnel:Section 197)

Food for Thought::

Whether there is any restriction for Remuneration to Directors of Private Limited Companies?

Section 197(1):

The total managerial remuneration payable by a Public Company, to its:

i. Directors, and

ii. Managing Director and

iii. Whole-Time Director, and

iv. Manager

in respect of any financial year shall not exceed eleven per cent. of the net profits of that company for that financial year computed in the manner laid down in section 198 except that the remuneration of the directors shall not be deducted from the gross profits.

However, such limits may be exceeded with the approval of the shareholders and the Central Government.

Currently, the laws in countries such as the US, the UK and Switzerland do not require a company to approach government authorities for approving remuneration payable to their managerial personnel, even in a scenario where the company has losses or inadequate profits.

Companies Amendment Act, 2017 The word “with the approval of Central Government” removed from every place under this section.

- No need approval of CGfor payment of remuneration more than 11% of net profit,

- No need of CG approvalof recovery of any sum refundable from director.

Inadequate Profit: No need of CG approval for remuneration in situation of no profit or inadequate profit. In such case remuneration shall be paid according to Schedule V.

| PART II | SECTION II | SCHEDULE V |

| Remuneration payable by companies having no profit or inadequate profit | ||

Above mentioned section of part II States about remuneration to Directors including MD/WTD / Manager.

No Profit: This is situation when Company is in loss, it doesn’t have any profit in its financials.

Inadequate Profit: This is situation when Company is having sufficient profit in its financials for payment of remuneration. However, profit is not sufficient to cover in limit of 11% of net profit. Exp.

| S. No. | Profit Amount | 11% of Profit | Remuneration want to pay | Remark |

| i. | 1,00,00,000 | 11,00,000 | 50,00,000 | Inadequate Profit |

| ii. | 1,50,00,000 | 16,50,000 | 17,00,000 | Inadequate Profit |

| iii. | 50,00,000 | 550,000 | 500,000 | Sufficient |

| iv. | 0 | 0 | 50,00,000 | No Profit |

As per Schedule V, Part II, Section II company can pay remuneration more than 11% by following the below mentioned:

Company by passing of Ordinary Resolution in General Meeting can pay remuneration upto below mentioned limit:

| Where the effective capital is | Limit of yearly remuneration payable shall not exceed (Rupees) |

| (i) Negative or less than 5 crores | 60 Lakhs |

| (ii) 5 crores and above but less than 100 crores | 84 Lakhs |

| (iii) 100 crores and above but less than 250 crores | 120 Lakhs |

| (iv) 250 crores and above | 120 lakhs plus 0.01% of the effective capital in excess of Rs. 250 crores: |

Company by passing of Special Resolution in General Meeting can pay remuneration ANY AMOUNT without any limit:

For payment of remuneration as per above mention Limit of Section II Company have to comply with following conditions:

i. Board Resolution:payment of remuneration is approved by a resolution passed by the Board and, in the case of a company covered under sub-section (1) of suction 178 also by the Nomination and Remuneration Committee

ii. No Default:the company has not committed any default in payment of dues to any bank or public financial institution or non-convertible debenture holders or any other secured creditor, and in case of default, the prior approval of the bank or public financial institution concerned or the non-convertible debenture holders or other secured creditor, as the case may be, shall be obtained by the company before obtaining the approval in the general meeting.

iii. General Meeting:an ordinary resolution or a special resolution, as the case may be, has been passed for payment of remuneration as per item (A) or (B), at the general meeting of the company for a period not exceeding three years.

iv. Notice of General Meeting:a statement along with a notice calling the general meeting referred to in clause (iii) is given to the shareholders containing the following information as mention in schedule:-

v. Company Secretary Certificate:

The auditor or the Secretary of the company or where the company is not required to appointed a Secretary, a Secretary in whole-time practice shall certify that the requirement of this Schedule have been complied with and such certificate shall be incorporated in the return filed with the Registrar under sub-section (4) of section 196.

Food for Thought::

If a Person is holding position as director of Private Limited Company and having position as employee of Company. Whether such person shall be considered as Director or Whole Time Director.

P. OTHERS

A. Conversion of Partnership firm or LLP into Company: (Section 366)

{To be notified w.e.f. 15th August, 2018}

Now it is allow converting the partnership firm, LLP etc with 2 or more partners into private company.

B. “Section 446A – Factor for determining level of punishment”{ Notified w.e.f. 09th Feb, 2018}

According the this Section the Court or Special Court while deciding the amount of fine or imprisonment under this Act, shall have due regard to the following factors, namely

(a) Size of the company;

(b) Nature of business carried on by the company;

(c) Injury to public interest;

(d) Nature of the default; and

(e) Repetition of the default

Note: After the amendments court shall consider the factors for penalize the Company. It is a good move to consider the different-2 factors for penalty in case of non –compliance.

C. “Section 446B – Lesser penalties for One Person Companies or Small Companies” { Notified w.e.f. 09th Feb, 2018}

In this section relief to OPC and Small Companies i.e. in case of failure to comply with provisions of

- Section 117(2)(c) – Resolution and Agreement to be filed

- Section 137(3) – Copy of Financial statement to be filed

- Section 92(5) – Annual Return

In case of default, such company and officer in default of such company shall be punishable with fine or imprisonment or fine and imprisonment, as the case may be, which shall not be more than one-half of the fine or imprisonment or fine and imprisonment, as the case may be, of the minimum or maximum fine or imprisonment or fine and imprisonment, as the case may be, specified in such sections.

D. Postal Ballot: {Notified w.e.f. 07thMay, 2018}

Companies which are mandatorily required to provide electronic voting facility, to transact item in general meeting, can transact business of postal ballot also through electronic voting.

LIST A

MCA has notified below mentioned 5 sections of Companies Amendment Act, 2017 w.e.f. 12th September, 2018.

| S. No. | Section No. of Amendment Act, 2017 | Section No. of Companies Act, 2013 | Particular of Section |

| 1. | Section 66 | Section 196 | Appointment of Managing Director, Whole-time Director or Manager |

| 2. | Section 67 | Section 197 | Overall Maximum Managerial Remuneration and Managerial Remuneration in Case of Absence or Inadequacy of Profits |

| 3. | Section 68 | Section 198 | Calculation of Profits |

| 4. | Section 69 | Section 200 | Central Government or Company to Fix Limit with Regard to Remuneration |

| 5. | Section 70 | Section 201 | Forms of, and Procedure in Relation to, Certain Applications |

LIST B

MCA has notified below mentioned 4 sections of Companies Amendment Act, 2017 as follow

| S. No. | Section No. of Amendment Act, 2017 | Section No. of Companies Act, 2013 | Notification Date | Particular of Section |

| 6. | Section 37 | Section 135 | 19th September, 2018 | Corporate Social Responsibility |

| 7. | Section 10 | Section 42 | 07th August, 2018 | Issue of shares on Private Placement Basis |

| 8. | Section 36 | Section 134 | 31st July, 2018 | Financial Statement and Board Report |

| 9. | Section 5 | Section 7 | 27th July, 2018 | Incorporation of Company |

| 10. | Section 6 | Section 12 | 27th July, 2018 | Registered office of Company |

LIST C

MCA has notified below mentioned 4 sections of Companies Amendment Act, 2017 w.e.f. 15th August, 2018.

| S. No. | Section No. of Amendment Act, 2017 | Section No. of Companies Act, 2013 | Section No. of Companies Act, 2013 |

| 11. | Section 15 | Section 73 | Prohibition on Acceptance of Deposits from Public |

| 12. | Section 16 | Section 74 | Repayment of Deposits, etc., Accepted Before Commencement of this Act |

| 13. | Section 75 | Section 366 | Companies Capable of Being Registered |

| 14. | Section 76 | Section 374 | Obligations of Companies Registering Under this Part |

LIST D

MCA has notified below mentioned 1 sections of Companies Amendment Act, 2017 w.e.f. 5thJuly, 2018.

| S. No. | Section No. of Amendment Act, 2017 | Section No. of Companies Act, 2013 | Particular of Section |

| 15. | Section 20 | Section 82 | Company to Report Satisfaction of Charge. |

LIST E

MCA has already notified below mentioned 5 sections of Companies Amendment Act, 2017 w.e.f. 13th June, 2018.

| S. No. | Section No. of Amendment Act, 2017 | Section No. of Companies Act, 2013 | Particular of Section |

| 16. | Section 22 | Section 90 | Register of Significant beneficial owners in a Company |

| 17. | Section 24 | Section 93 | Return to be filed with Registrar in case promoters’ stake change |

| 18. | Section 25 | Section 94 | Place of Keeping and inspection of registers, returns etc. |

| 19. | Section 26 | Section 96 | Annual General Meeting |

| 20. | Section 71 | Section 216 | Investigation of ownership of Company |

LIST F

MCA has already notified below mentioned 28 sections of Companies Amendment Act, 2017 w.e.f. 7th May, 2018.

| S. No. | Section No. of Amendment Act, 2017 | Section No. of Companies Act, 2013 | Particular of Section |

| 21. | Section 2 Clause (i) and (xiii) | Section 2 | Definitions |

| 22. | Section 8 | Section 26 | Matter to be stated in Prospectus |

| 23. | Section 13 | Section 54 | Issue of Sweat Equity Shares |

| 24. | Section 18 | Section 77 | Duty to Register charge |

| 25. | Section 19 | Section 78 | Application for registration of charge |

| 26. | Section 21 Clause (i) (ii) | Section 89 | Declaration in respect of beneficial interest in any share |

| 27. | Section 23 clause (iii) & (iv) | Section 92 | Annual Return |

| 28. | Section 30 | Section 117 | Resolution and agreements to be filed |

| 29. | Section 31 | Section 121 | Report on Annual General Meeting |

| 30 | Section 33 | Section 129 | Financial Statement |

| 31. | Section 39 | Section 137 | Copy of financial statement to be filed with Registrar |

| 32. | Section 40 | Section 139 | Appointment of Auditors |

| 33. | Section 46 | Section 149 | Company to have Board of Directors |

| 34. | Section 49 | Section 157 | Company to inform Director identification Number to Registrar |

| 35. | Section 52 | Section 164 | Disqualifications for appointment of Director |

| 36. | Section 54 | Section 167 | Vacation of office of Director |

| 37. | Section 55 | Section 168 | Resignation of Director |

| 38. | Section 56 | Section 173 | Meeting of Board |

| 39. | Section 57 | Section 177 | Audit Committee |

| 40. | Section 58 | Section 178 | Nomination and Remuneration Committee and Stakeholders Relationship Committee |

| 41. | Section 61 | Section 185 | Loan to Directors |

| 42. | Section 62 | Section 186 | Loan and investment by Company |

| 43. | Section 80 Clause (i) (ii) | Section 403 | Fee for Filing etc |

| 44. | Section 83 | Section 410 | Constitution of Appellate Tribunal |

| 45. | Section 86 | Section 435 | Establishment of Special Courts |

| 46. | Section 87 | Section 438 | Application of code of proceedings before special court |

| 47. | Section 88 | Section 439 | Offences to be non-cognizable |

| 48. | Section 89 | Section 440 | Transitional provisions |

LIST G

MCA has already notified below mentioned 43 sections of Companies Amendment Act, 2017 w.e.f. 9th February, 2018.

| S. No. | Section No. of Amendment Act, 2017 | Section No. of Companies Act, 2013 | Particular of Section |

| Section 2 | Section 2 | Definations (except definition of Associate & Subsidiary) | |

| 49. | Section 3 | New Section 3A | Member severally liable in certain cases |

| 50. | Section 7 | Section 21 | Authentication of Documents, Proceeding & Contracts |

| 51. | Section 9 | Section 35 | Civil Liability for mis-statement in prospectus |

| 52. | Section 11 | Section 47 | Voting Right |

| 53. | Section 12 | Section 53 | Prohibition on issue of shares at discount |

| 54. | Section 14 | Section 62 | Further issue of share capital |

| 55. | Section 17 | Section 76A | Penalty on Deposit |

| 56. | Section 27 | Section 100 | Calling of extra ordinary general meeting |

| 57. | Section 28 | Section 101 | Notice of Meeting |

| 58. | Section 29 | Section 110 | Postal Ballot |

| 59. | Section 32 | Section 123 | Declaration of Dividend |

| 60. | Section 34 | Section 130 | Re opening of accoiunts of courts or tribunals order |

| 61. | Section 35 | Section 132 | Constitution of National financial reporting authority |

| 62. | Section 38 | Section 136 | Right of members to copies of audited financial statement |

| 63. | Section 41 | Section 140 | Removal, resignation of auditor |

| 64. | Section 42 | Section 141 | Eligibility, qualifications and disqualification of auditors |

| 65. | Section 43 | Section 143 | Power and duties of auditors and autiding standards |

| 66. | Section 44 | Section 147 | Punishment for contravention |

| 67. | Section 45 | Section 148 | Central govt. to specify audit of items of cost in respect of certain companies |

| 68. | Section 47 | Section 152 | Appointment of Directors |

| 69. | Section 48 | Section 153 | Application of allotemnt of DIN |

| 70. | Section 50 | Section 160 | Right of persons other than retiring directors to stand for directorship |

| 71. | Section 51 | Section 161 | appointment of additional director, alternate director and nominee director |

| 72. | Section 53 | Section 165 | Number of directorship |

| 73. | Section 59 | Section 180 | Restrictions of power of board |

| 74. | Section 60 | Section 184 | Disclosure of interest by Director |

| 75. | Section 63 | Section 188 | Related party transaction |

| 76. | Section 65 | Section 195 | Prohibition on insider trading of securities |

| 77. | Section 64 | Section 194 | Prohibition on forward dealings in securities of company by director or key managerial personnel |

| 78. | Section 72 | Section 223 | Inspector’s Report |

| 79. | Section 73 | Section 236 | Purchase of minority shareholding |

| 80. | Section 74 | Section 247 | valuation by registered valuer |

| 81. | Section 77 | Section 379 | Application of act to foreign companies |

| 82. | Section 78 | Section 384 | Debentures, annual return, registered of charge, books of account |

| 83. | Section 79 | Section 391 | Application of section 34 to 36 and chapter XX |

| 84. | Section 82 | Section 409 | Qualification of president and member of tribunal |

| 85. | Section 84 | Section 411 | Qualification of chair person and member of appellate tribunal |

| 86. | Section 85 | Section 412 | Selection of members of Tribunal and appellate tribunal |

| 87. | Section 90 | Section 441 | Compounding of certain offences |

| 88. | Section 91 | Section 446 | Insertion of new section 446A and 446B |

| 89. | Section 92 | Section 447 | Punishment for fraud |

| 90. | Section 93 | Section 458 | Delegation by central government of its powers and functions |

(Author – CS Divesh Goyal, GOYAL DIVESH & ASSOCIATES Company Secretary in Practice from Delhi and can be contacted at csdiveshgoyal@gmail.com).

Author Bio

VERY INFORMATIVE. THANK YOU

Above article is not covering amendments in Section 186 of Companies Act and what is covered is essentially relates to Section 185 of the Act.

Particularly it does not cover amendments in Section 186 (11) of the Act relating to exemptions from the Act.

I draw attention to clause b of the said section.language of which seems to be confusing imply that lending by NBFC is not covered by exemption and only Investments are exempted.

This is particularly relevant as clause a dealing with lending on does not include NBFC.

Please clarify your views on applicability of the exemption to pure lending by NBFC registered under Chapter IIi B of RBI Act.

Thanks