Financial statements:

♦ The presentation of financial statements is governed by both IAS 1 (International Accounting Standard 1) and Ind AS 1 (Indian Accounting Standard 1). The standards are comparable in many ways, however, there are some variances in the presentation criteria.

♦The objective of financial statements is to provide information about the financial position (Assets, Liabilities & Equity), financial performance (Income, Expenses including gains and Losses), and cash flows (Including cash equivalents) of an entity that is useful to a wide range of users in making economic decisions.

♦ Both standards require that financial statements should be prepared on the basis of the accrual principle, which means that transactions are recognized when they occur, rather than when cash is received or paid except for cash flow statements which need to be prepared based on cash principle.

Page Contents

- Components of Financial Statements:

- Key Principles:

- Structure and content:

- II. Balance sheet – Statement of financial position:

- III. Statement of profit or loss and other comprehensive income:

- 1. Statement of profit or loss:

- 2. Statement of other comprehensive income (OCI):

- IV. Statement of Cash Flows (IAS 7/INDAS 7):

- V. Statement of Changes in Equity:

- VI. Notes to the Financial Statements:

- VII. Third Balance sheet/Re-statement:

- Difference between IAS 1 and INDAS 1:

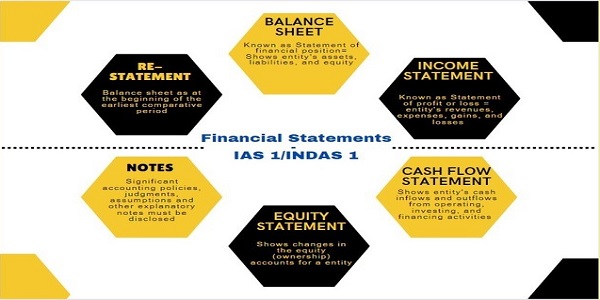

Components of Financial Statements:

A complete set of financial statements comprises:

1. A statement of financial position

2. A statement of profit or loss and other comprehensive income

3. A statement of changes in equity

4. A statement of cash flows

5. Notes: Significant accounting policies, judgments, assumptions, and other explanatory notes must be disclosed

6. Re-Statement/3rd Balance sheet: The balance sheet as at the beginning of the preceding period if there is a retrospective change in the accounting policy or reclassification or restatement.

Key Principles:

1. True and fair presentation and compliance with IND AS:

- Financial statements are required to be presented fairly as set out in the framework and in accordance with IND AS/IFRS and are required to comply with all the requirements of IND AS/IFRS.

- True and fair view = Compliance with applicable IND AS’s/IFRS + Additional disclosures when necessary.

2. Going concern:

- An entity neither has any intention nor has any necessity to curtail its business operations in foreseeable future. The firm will continue its operations for the next 12 months period.

- Financial statements are required to be prepared on a going concern basis (unless the entity is in liquidation or has ceased trading or there is an indication that the entity is not a going concern). Management shall make an assessment of an entity’s ability to continue as a going concern at the end of the accounting period. If material uncertainties exist on its ability to continue as a going concern, those uncertainties shall be disclosed.

3. Accrual basis of accounting:

- Recognize and record the items of revenue and expenditure as and when it is earned or incurred irrespective of the fact that when cash has been received or paid out respectively.

- Financial statements are prepared on an accrual basis (except cash flow information) to inform users not only about past transactions but also about future transactions.

4. Consistency:

- The same set of accounting principles, accounting policies, and accounting methods are followed from one accounting period to another accounting period.

- The standard requires the presentation and classification of items in financial statements to be consistent from one period to another unless:

♦ Change will result in a more appropriate presentation due to a change in entity operations or another presentation would be more appropriate having regard to criteria for selection and application of accounting policies in IND AS/IAS-8.

♦ Change required by an IND AS or IFRS standard/law.

5. Materiality:

- An entity shall present separately: Each material class of similar items shall be presented separately in the financial statements. Items of a dissimilar nature or function shall be presented separately unless they are immaterial.

- Financial statements should disclose all the items and facts which can influence the decisions taken by the users/readers of the financial statements.

6. Offsetting:

- Offsetting of assets and liabilities or income and expenses is not permitted unless required or permitted by other IND AS/IFRS.

- Offsetting is permitted when it reflects the substance of the transaction.

- Examples of offsetting:

a. Revenue recognized is after offsetting trade discounts and volume rebates. The same is allowed by IND AS/IFRS.

b. Gains/losses from the sale of non-current assets with a net of the selling expenses for the same.

c. Reporting a provisional loss net of third-party reimbursement.

7. Frequency of Reporting:

- As per IND AS 1, a complete set of financial statements should be presented at least annually. If not, then additional disclosures are required.

- When there is a change at the end of the reporting period and presents for a period longer or shorter than 1 year, an entity should disclose:

♦ Reason for using a longer or shorter period

♦ The fact that the amounts presented in the financials are not entirely comparable

8. Comparative Information:

- At least 1 year of comparative information.

- The information must be presented for the current and previous reporting period for all amounts reported in the financial statements.

- Narrative and descriptive comparative information is also required, to understand the current period’s financial statements.

- 3rd Balance sheet as at the beginning of the preceding period if there is a retrospective change in accounting policy or reclassification or restatement.

Structure and content:

I. IDENTIFICATION OF THE FINANCIAL STATEMENTS: Financial statements must be clearly identified and distinguished from other information in the same published document. The following information shall be displayed to facilitate understanding:

- Name of the reporting entity

- Whether financial statements relate to an individual entity or a group of entities

- Reporting date and reporting period

- Presentation Currency

- Level of rounding used

II. Balance sheet – Statement of financial position:

a. IND AS 1/IFRS 1 specifies that the following items, as a minimum, are presented on the face of the balance sheet. There is no prescribed order or format in which items are to be presented.

- Assets: Property, plant and equipment; investment property; intangible assets; financial assets; investments accounted for using the equity method; biological assets; deferred tax assets; current tax assets; inventories; trade and other receivables; and cash and cash equivalents

- Equity: Issued capital and reserves attributable to the parent’s owners; and non-controlling interest

- Liabilities: Deferred tax liabilities; current tax liabilities; financial liabilities; provisions; and trade and other payables

- Assets and liabilities held for sale: The total of assets classified as held for sale and assets included in disposal groups classified as held for sale; and liabilities included in disposal groups classified as held for sale in accordance with Ind AS/IFRS 105, ‘non-current assets held for sale and discontinued operations.

b. Present additional line items, headings, and subtotals when such presentation is relevant on the face of the balance sheet.

c. Present Current and Non-Current items separately

d. Deferred tax asset/liability shall be classified as Non-Current

e. Presentation

♦ Current / Noncurrent

♦ Liquidity

♦ Both

f. Distinction of Current / Non-Current:

Classification of asset

Classification of liability

III. Statement of profit or loss and other comprehensive income:

1. Statement of profit or loss:

- Report = Expenses incurred & Revenue earned

- The expenses are classified in the statement of profit and loss based on the nature of the expense.

2. Statement of other comprehensive income (OCI):

- Line items within other comprehensive income are required to be categorized into two categories:

♦ Those that could subsequently be reclassified to profit or loss

♦ Those that cannot be re-classified to profit or loss.

- The statement of other comprehensive income represents a company’s change in equity during a specific period from transactions and events that are typically Unrealized (non-cash) gains and losses. When the gains and losses crystallize into cash (Realized), they are usually reflected on the income statement and removed from other comprehensive income.

- Other comprehensive income provides additional detail to the balance sheet’s equity section, which identifies the change in stockholder’s equity beyond the net income listed on an income statement. The statement provides details of entries in the OCI account.

- Some of the transactions included in other comprehensive income are revenue, expenses, losses and gains not realized in the income statement. The reason a company has not realized those transactions is that they have not yet been completed, such as a sale of an investment (preventing a company from paying dividends to its shareholders with the gains), but its value has changed since the acquisition.

IV. Statement of Cash Flows (IAS 7/INDAS 7):

This statement provides information about an entity’s cash inflows and outflows during the period, categorized into operating, investing, and financing activities. Please refer to my article dated 23rd March 2023.

V. Statement of Changes in Equity:

- Total comprehensive income for the period, showing separately amounts attributable to owners of the parent and to non-controlling interests.

- For each component of equity, the effects of retrospective application/restatement are recognized in accordance with INDAS/IAS 8.

- For each component in equity, a reconciliation between the carrying amount at the beginning and end of the period, separately disclosing each change.

- Amount of dividends recognized as distributions to owners during the period in this statement or disclosed in the notes.

- Analysis of each item of OCI (alternatively to be disclosed in the notes).

VI. Notes to the Financial Statements:

Notes should contain

- A statement of compliance with IFRS/IND AS.

- A summary of significant accounting policies, estimates, assumptions, and judgments must be disclosed.

- Supporting information for the numbers presented in the financial statements, and other disclosures/additional information useful to users understanding / decision-making to be presented.

VII. Third Balance sheet/Re-statement:

An entity shall present a third balance sheet as at the beginning of the preceding period in addition to the minimum comparative financial statements required if:

♦ It applies an accounting policy retrospectively makes a retrospective restatement of items in its financial statements, or reclassifies items in its financial statements; and

♦ The retrospective application, retrospective restatement, or reclassification has a material effect on the information in the balance sheet at the beginning of the preceding period.

Difference between IAS 1 and INDAS 1:

- Ind AS 1 requires entities to present a statement of profit or loss and other comprehensive income, while IAS 1 allows entities to present comprehensive income in either a single statement or two separate statements.

- IAS 1 requires an entity to present an analysis of expenses recognized in profit or loss using a classification based on either their nature or their function within the equity. Ind AS 1 requires only nature-wise classification of expenses.

- IAS 1 permits the periodicity, for example, of 52 weeks for the preparation of financial statements. However, Ind AS 1 does not permit it.

- For materiality and disaggregation requirements, Ind AS 1 includes the words ‘except where required by law’.

Author Bio