Institute of Company Secretaries of India

ICSI has issued Auditing Standard for audit by ‘Practicing Company Secretary” . These standards issued by ICSI.

- These standards were effective from 1st July, 2019. However, from 1st July,2019 it was recommendatory.

- These standards are mandatory w.e.f. 1st April, 2020.

Important Note:

** These standards are applicable on “Practicing Company Secretary”.

** PCS undertake audit assignment envisaged under the

√ Security and Exchange Board of India Act, 1992

√ Any other law prevailing in India.

Also Read-Guidance notes on ICSI auditing standards

Aims of Standard: To support the Company Secretaries

i. In developing auditing acumen, techniques and tools and

ii. Inculcate best auditing practices while conducting the audit and Promote standardization and uniformity in the professional arena.

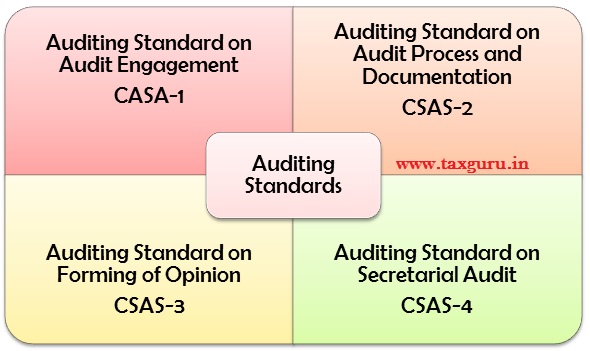

These standards are divided into four parts:

Following draft/ Specimen has been given by ICSI in Guidance Note:

- Eligibility Certificate for Practicing Company Secretary.

- Audit Engagement Letter

Auditing Standard on Audit Engagement- CASA-1

A. Audit Engagement Process: The Auditor shall undertake the following steps with respect to the Audit Engagement:

a) Pre-engagement Meeting with Auditee: – To discuss about the terms of engagement, prior year audit findings, auditee business operations, commercial terms of the audit and the timelines and milestones, if any.

b) Appointment: – The appointment of auditor shall be made in the manner prescribed in the applicable Law, Act, Rules and Regulations or manner determined by the appointing authority.

c) Eligibility Certificate: – The auditor shall submit a Certificate to the appointing authority confirming eligibility for appointment a auditor. Content and specimen of eligibility certificate given in Guidance Note.

d) Appointment Letter: – The auditor shall obtain an Audit engagement letter along with a copy of the resolution. The content of auditee engagement letter and specimen of same given in ICSI Guidance note.

e) *Important Pointes: The auditor is not permitted to pay a commission to obtain an audit nor shall he accept a commission for referral of an auditee to a third party.

f) *Communication to Previous Auditor: – The auditor in writing to the previous auditor, if any, before accepting the Audit Engagement. Auditor should maintain proper evidence of communication to previous auditor. Auditor shall wait for 7 days from the date of communication before accepting the audit. Example of assignments:

√ Signing of MGT-7

√ Certification in MGT-8

√ Secretarial Audit u/s 204 etc.

g) *Limit of Audit Engagement: – The auditor shall accept audit engagement within in limit prescribed by ICSI from time to time. Eg.

- Limit for Secretarial audit 10 per partner/ PCS

- Number of Annual Secretarial Compliance report issued by PCS are 5, etc.

h) Conflict of Interest: – The conflict of interest with the auditee explained below shall not be construed as a substantial of interest:

√ Auditor holding not more than 2% paid up share capital or share of nominal value of Rs. 50,000, which ever is lower;

√ Auditor indebted to the auditee for an amount not exceeding Rs. 500,000/-

√ Auditor was in employment of the auditee more than 2 year ago.

Note: ICSI in guidance note has given beautiful examples to understand above three situations.

BELOW CHART TAKEN FROM GUIDANCE NOTE OF ICSI

Audit Process and Documentation- CASA-2

The Audit process includes Planning, Execution and Documentation. Purpose of this standard to prescribe principle for an auditor:

√ To conduct audit as per the specified audit process

√ To maintain documentation that provide;

– Sufficient and appropriate record to form the basis for the auditors report;

– Evidence that the audit was planned and performed in accordance with the applicable auditing standards and statutory requirements.

Terms to be use in standard:

I. Mode of Documents: The audit documents may be in Physical and/or electronic mode.

II. Working Paper: Include the audit plan, letter of representation and/or confirmation, abstracts of auditees documents etc.

i. Audit Plan: – Audit plan is very crucial and should be designed with due care. Audit plan should give answers of what, where, who, when and how: eg

√ What are the audit objective?

√ Where will the audit be done? Etc.

The audit shall be planned in a manner which ensures that qualitative audit is carried out in an efficient, effective and timely manner. However, audit plan should not be followed rigidly and it should be changed according to the circumstances to effective conduct the audit.

ii. Risk Assessment: – Risk assessment shall be done considering industrial & business environment, organizational structure and compliance requirements. The industrial & business environment includes the regulatory changes & judicial orders, compliance and disclosure requirements etc.

iii. Information about Auditee: – The auditor shall obtain sufficient information about auditee that is relevant to conduct audit eg.

√ Nature of Business

√ Law applicable to business of auditee etc.

iv. Audit Checklist: – Auditor shall use systematic and comprehensive audit checklist for carrying out the audit and to verify the compliance requirements. It should provide assistance to the audit process and should be reviewed and updated from time to time to mee the scope of audit and its effectiveness.

v. Documentation: – The auditor shall adequately document the Audit Evidence in working papers, including the basis and extent of planning, work performed and the findings of audit. Audit documents shall take place throughout the audit process.

*Audit Documents shall be properly indexed, referenced with and supplemented by the set of working papers.

Note:

√ The audit Documents shall be collated for records within a period of 45 days from the date of signing of Auditors Report.

√ The Audit Documents shall be maintained in physical or electronic form and retained for a period of 8 years from the date of signing of Auditors Report.

Forming of Opinion- CASA-3

Objective of this standard to lay down the basis and manner for evaluation of the conclusions drawn from the Audit Evidence obtained and express the opinion through written report.

This standard defined many terms like:

a) Misstatement: – means any information or statement which is false, incorrect, incomplete, misleading or misrepresents, omits or suppresses a material fact.

b) Records: – includes;

√ MOA & AOA

√ Minutes, returns, forms, index and registers; etc.

*Generally, the records mean the records for the audit period.

i. Process for forming of opinion: –Forming of opinion on the audit observation is an important part of any audit. The auditor shall consider materiality while forming the opinion and adhere to;

√ The principle of Completeness.

√ The principle of Objectivity.

√ The principle of timeliness

√ The principle of a contradictory process

ii. Judgement: –The auditor may consider various judgments, clarifications and opinion, conflicting interpretations while framing the opinion to the best of his professional acumen.

Type of Opinions:

Note:

√ Whenever the auditor express a modified opinion or disclaims an opinion, the text of the opinion shall be either italics or bold letter.

iii. Auditors Responsibility: –The auditors report shall include a section with the heading “Auditor’s responsibility”. The audit report shall also state that the audit was conducted in accordance with applicable standard.

Auditors responsibility heading will state followings:

√ Whether the audit has been conducted as per the application Auditing Standards.

√ Whether the auditor has obtained reasonable assurance about whether the statement prepared , records maintained by the auditee are free from miss statement etc.

iv. Format of Report: – The reports shall be addressed to the appointing authority unless otherwise specified in audit engagement letter or provided in the applicable law. The report shall be detailed enough to serve the intended purpose.

v. Signature of Report: Signature shall mention the

√ names of audit firm along with registration number, if any

√ the name of the auditor

√ certificate of practice number

√ the membership number of the auditor

√ specified associate or fellow member

The auditor clearly mention the Date and Place of signing the report, in case report is signed by two different persons on different dates or different places; same shall be mentioned in the report.

Note:

√ Audit report is the result of the audit performed in as per its scoep and objectives.

√ The audit Report must be prepared in detail so that the purpose of preparing the report and showcasing the true state of affairs of the auditee can be attained.

Author Bio