Discover the crucial role of actuarial valuations in the realm of employee benefits. This article delves into the importance of actuarial assessments, discusses non-compliance concerns with Accounting Standards (AS) 15 and Ind AS 19, and presents opportunities for professionals in this field.

Background:

Employers play a key role in educating, encouraging or compelling their employees to plan benefit However, the most significant role played by the employers is financing employee benefits for their employees. Such financing may be a result of:

- Compulsion (Statutory like Gratuity, Negotiated benefits like compensated absence) or encouragement (NPS contribution) from the

- A paternalistic desire to look after employees and their dependents financially beyond the level provided by the

- Income Supplement in Retirement or Desire to attract and retain the services of key

The Accounting Standard dealing with the employee benefits is ‘Accounting Standard 15’ (namely Indian GAAP or AS 15) and new IFRS converged ‘Indian Accounting Standard 19’ (namely Ind AS or Ind AS 19).

Financial Statements are the paramount source in hands of the stakeholders to understand the financial well-being of an The users are highly reliant on the information depicted in the financial statements and therefore the preparers ought to ensure that the information presented in the financial statement is correct, complete, relevant and in adherence to the regulatory requirements.

This article deals with the Importance of Actuarial Valuations in Employee Benefits, non-compliances observed by the Financial Reporting Board of ICAI, with accounting and disclosure requirements prescribed under AS 15, Ind

Many a times it has been observed that professionals are not aware or miss the requirement of Actuarial Valuation provision, below summary explains requirement of AS 15 Employee Benefits, Actuarial Valuation provisions and certain relaxations given in the

This is to also note that in some instances company obtain Actuarial Valuation report from Insurance company like LIC or other Insurance company where they have done the funding of Group Gratuity, it is pertinent to note that such certificate is not for AS 15 accounting purpose, it is given only for the funding In many cases it has been found that Insurance company also give a disclaimer at the end that it is not for AS 15 certification.

Page Contents

- AS Deficiencies identified by Financial Reporting Review Board of ICAI

- Common Errors Found by FRRB (AS15, Ind AS19)

- Issues Found by Quality Review Board (QRB) [SA 620]

- Possible Solution to this:

- Applicability of AS 15 – Employee Benefits to Companies

- Screenshot from AS 15 Employee Benefits (as applicable to companies) Comment regarding – Small and Medium Company (SMC)

- Applicability of AS 15 – Employee Benefits to Non-company entities

- Benefits of Funding Employee Benefits:

- Related Opportunities for Professionals CA/CS)

- Related Opportunities for Actuaries

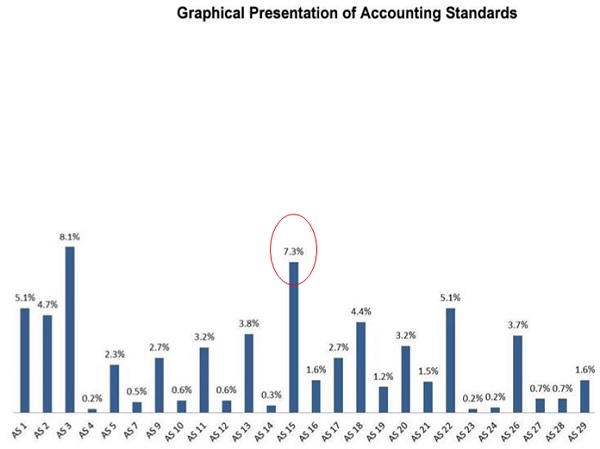

AS Deficiencies identified by Financial Reporting Review Board of ICAI

From the above it can be seen that amongst all Accounting Standards, AS 15 is the one where maximum non-compliance were found. Similarly in case of Ind AS non-compliances, ratio of Ind AS 19 – Employee Benefits noncompliance was higher.

Common Errors Found by FRRB (AS15, Ind AS19)

Non-provisioning of Gratuity (Matching

No disclosure or inadequate disclosures post-employment plans Defined Benefit Plan wrongly treated as Defined Contribution Plan Non-Disclosure of expense for Defined Contribution Plan

Inadequate disclosure pertaining to Use of PUCM Method, Assumptions

Actuarial Gain/ loss recognized inappropriately, In case of Ind AS 19 it requires Actuarial Gain/ loss to be recognized in Other Comprehensive Income for Post employment benefit obligations and Profit or Loss account for Other long term benefit

Provision for Long service awards, Leave without Actuarial Method

Issues Found by Quality Review Board (QRB) [SA 620]

Not evaluating whether:

the actuary has the necessary competence, capabilities and objectivity for the auditor’s purposes and the relevance and reasonableness of the assumptions and methods used by him (Para 9, 12).

(Ref: QRB Report on Audit Quality Review – 2021-22 – (02-11-2022) ICAI Website)

Possible Solution to this:

Auditor can check/ ask for the qualification/ CoP of member providing actuarial valuation As per the Institute of Actuaries of India, Fellow Actuary having valid Certificate of Practice can practice in this field as proprietor or partnership firm, company is not allowed to practice as per Actuaries Act.

The reasonableness of Assumption should be checked, for example company having Actual Attrition rate of 15% – 20% a. consistently but 2% p.a. Attrition assumption is used. This can be checked by performing assumption analysis at overall level and may require thorough analysis at regular intervals from Company/ Actuary.

Applicability of AS 15 – Employee Benefits to Companies

The scheme for applicability of Accounting Standards to Company shall come into effect in respect of accounting periods commencing on or after April 1, 2021. They need to follow Accounting Standards as per Companies (Accounting Standards) Rules, 2021, as issued by MCA.

| Particulars | Non-SMC# | SMC |

| Securities Listed in India or Outside India | √ | |

| Bank, Financial Institution, Insurance company | √ | |

| Turnover in Previous Year | > 250 cr | < 250 cr |

| or | and | |

| Borrowing at any time in Previous Year | > 50 cr | < 50 cr |

| Holding/ Subsidiary of above | √ | √ |

Earlier for accounting period till 31 March, 2021, limit of turnover was 50 cr and for borrowing 10 cr, which is now increased to

250 cr and 50 cr respectively.

| Particulars | Non-SMC | SMC |

| Applicability of AS 15 – Employee Benefits | Full Applicable | With Exemptions |

| Gratuity/ Leave/ Long Service Award | ||

| A. Whether Provision is Required? | Yes | Yes |

| B. Provision as per Actuarial Valuation PUCM Method? | ||

| Employees 50 or more: | Yes | Yes |

| Employees Less than 50 : | Yes | Yes |

| C. Detailed Disclosure for Gratuity? | Yes | Exempted |

The Payment of Gratuity Act, 1972 is applicable to all entities employing 10 or more employees, so they should make provision as per AS 15 as post-employment benefit

Leave Provisions are governed by the respective state’s Shop & Establishment Act, most of them allow for carrying forward of leave and encashment on separation. They should make provision of Leave as per AS 15 as other long-term benefit

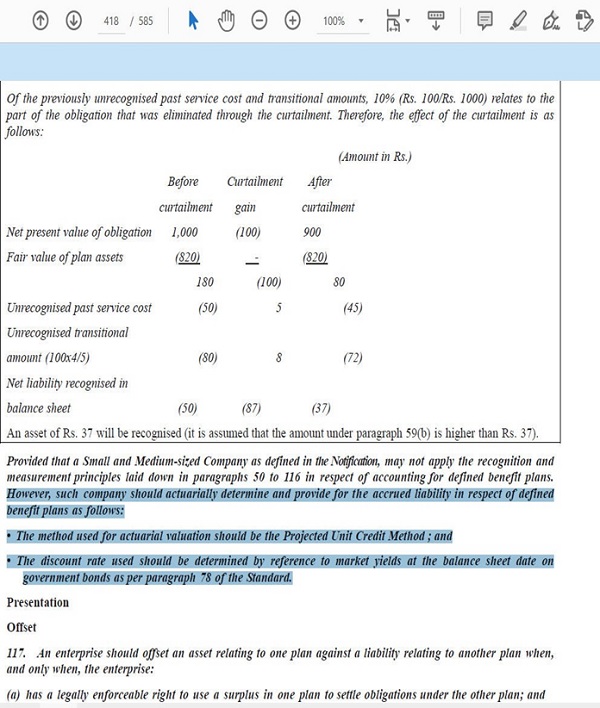

In case Detailed disclosures are exempted for SMC, such company should actuarially determine and provide for the accrued liability in respect of defined benefit plans as follows:

- The method used for actuarial valuation should be the Projected Unit Credit Method; and

- The discount rate used should be determined by reference to market yields at the balance sheet date on government bonds as per paragraph 78 of the

An SMC which avails the exemptions or relaxations given to it shall disclose (by way of a note to its financial statements) the fact that it is an SMC and that it has complied with the Accounting Standards insofar as they are applicable to SMC on following lines: “The Company is a Small and Medium Sized Company (SMC) as defined in the Companies (Accounting Standards) Rules, 2021 notified under the Companies Act, Accordingly, the Company has complied with the Accounting Standards as applicable to a Small and Medium Sized Company.”

An existing company, which was previously not a SMC and subsequently becomes SMC, shall not be qualified for exemptions or relaxation in respect of Accounting Standards available to a SMC until the company remains a SMC for two consecutive accounting

Screenshot from AS 15 Employee Benefits (as applicable to companies) Comment regarding – Small and Medium Company (SMC)

Applicability of Accounting Standard to Companies — (Issued by MCA): Accounting period till 03.2021:

http://www.mca.gov.in/Ministry/notification/pdf/Notification_GSR_739.pdf

Accounting period on or after 01.04.2021: (Page 329)

https://egazette.nic.in/WriteReadData/2021/227890.pdf

Applicability of AS 15 – Employee Benefits to Non-company entities

The scheme for applicability of Accounting Standards to Non-company entities shall come into effect in respect of accounting periods commencing on or after April 1, 2020. They need to follow Accounting Standards as issued by ICAI.

| Particulars | Level I | Level II | Level III | Level IV |

| Securities Listed in India or Outside India√ | √ | × | × | × |

| Bank, Financial Institution, Insurance | √ | × | × | × |

| Turnover in Previous Year | > 250 cr | 50 cr – 250 cr | 10 cr – 50 cr | < 10 cr |

| Borrowing at anytime in Previous Year | > 50 cr | 10 cr – 50 cr | 2 cr – 10 cr | < 2 cr |

| Holding/ Subsidiary of above | √ | √ | √ | √ |

–

| Particulars | Level I | Level II | Level III | Level IV |

| Applicability of AS 15 – Employee Benefits | Full Applicable | With Exemptions | With Exemptions | With Exemptions |

| Gratuity/ Leave/ Long Service Award | ||||

| A. Provision in accounts Required? | Yes | Yes | Yes | Yes |

| B. Provision as per Actuarial Valuation PUCM

Method? |

||||

| Employees 50 or more: | Yes | Yes | Yes | Exempted |

| Employees Less than 50 : | Yes | Exempted | Exempted | Exempted |

| C. Detailed Disclosure for Gratuity? | Yes | Exempted | Exempted | Exempted |

The Payment of Gratuity Act, 1972 is applicable to all entities employing 10 or more employees, so they should make provision as per AS 15 as post-employment benefit

Leave Provisions are governed by the respective state’s Shop & Establishment Act, most of them allow for carrying forward of leave and encashment on separation. They should make provision of Leave as per AS 15 as other long-term benefit

In case Actuarial Valuation is exempted for specific class of entities, such entities may calculate and account for the accrued liability under the defined benefit plans by reference to some other rational method, g., a method based on the assumption that such benefits are payable to all employees at the end of the accounting year.

Level IV, Level III, and Level II entities are referred to as Micro, Small and Medium size entities (MSMEs). An MSME which avails the exemptions or relaxations given to it shall disclose (by way of a note to its financial statements) the fact that it is an MSME, the Level of MSME and that it has complied with the Accounting Standards insofar as they are applicable to entities falling in Level II or Level III or Level IV, as the case may

Applicability Level I/II/III/IV – Non-Corporate — (Issued by ICAI): Accounting period on or after 01.04.2020: https://resource.cdn.icai.org/64269asb51535.pdf

Benefits of Funding Employee Benefits:

Provide Security to employees that benefit will be paid as they are insured and managed by professionals and regulated by competent

Provide Flexibility to employer to contribute towards accumulation of fund.

Company may not face liquidity problem when they have to pay huge amount to outgoing employees for benefits to be

As per Income Tax Act, superannuation benefits, gratuity, and other benefits are deductible from income when benefits are paid or Contribution made in trust fund to the limits prescribed in Income tax rules 87-88 & 101-104.

Provides Tax benefits on investment income of trust fund, so company should consider tax effective return for considering funding decision.

Beneficial in case of employee transfers: When employee transfers form one organization to another may be as part of mergers & acquisition or transfer within group Company, accrued benefit liability as on date of transfer should also be transferred to another In case scheme is funded, equitable transfer of assets also needs to be made to another fund. In case if an employee transferred from one group company to another company, then the company should transfer their Gratuity, PF (in case of recognized provident fund) from one trust fund to another, since continuation of service is pre requisite for getting tax free benefit and for that transfer of fund is required.

Related Opportunities for Professionals CA/CS)

As per Income Tax regulations in India, as per Section 36 (1) (v) company can claim deduction for Gratuity contribution to Approved Gratuity Part C of Schedule IV laid down various requirements and rules for such approved Gratuity trust and they need to follow certain investment pattern. As a Tax Auditor of the company or Consultant to company you can advise them for appropriate Gratuity funding and assist in following activities:

- Gratuity Trust Set up

- Gratuity Trust Income Tax Approval

- Gratuity Trust Yearly Audit of Gratuity trust financials.

- Funding from Insurance company from network

Demand Supply Gap of Actuaries – At present in India we have approx. 550+ Actuaries, given nature of work and requirement there are ample opportunities in this field. CA cum Actuary would be a good combination to serve in the Actuarial work, given that members already have accounting and auditing skills so Actuarial skill on top of that will help them to advice client in an appropriate manner. In addition to Employee Benefit actuarial work, one actuary can also work in field of Insurance for Actuarial consultancy.

Related Opportunities for Actuaries

ESOP Scheme Design, ESOP Valuation as Valuer

ESOP Regulation Compliance Certificate every year

Approved Gratuity Fund (Section 36(1)(v) read with Part C of Schedule IV):

- Gratuity Trust Set up,

- Gratuity Trust Income Tax Approval,

- Gratuity Trust Yearly Audit

Funding from Insurance company

Labor Law Consulting & Leave Policy Design

Demand Supply Gap of Actuaries.

Conclusion: In an era where employee benefits hold significant importance for both employers and employees, actuarial valuations emerge as a critical tool for accurate financial reporting. The insights provided through these valuations assist companies in making informed decisions, ensuring compliance, and maintaining financial transparency. Professionals in the field, particularly actuaries and auditors, have the opportunity to play a vital role in shaping the financial well-being of organizations and safeguarding the interests of employees.

*****

Author: Kartikey Kandoi, FIAI, FIA, FCA Consulting Actuary, ESOP Advisor | Council Member of the Institute of Actuaries of India | ICAI – ASB Special Invitee Member | Faculty for Ind AS Certificate & Deep Dive course on Ind AS 102 by ICAI

Author Bio