Before we jumping on to the topic of Startup funding,

Let’s understand First Startup then we move to the Funding

Recently, on the bourses of Stock Market, we all have seen number of Startups got listed. Some of them haves performed well or other ones are facing beta pressure, Selling pressure as HNIs are getting exit and valuation or funding issues. Because it becomes difficult for startups to raise money from the investor, the moment they listed.

In layman sense, startups are those which has disruptive technology, innovation, Patents, ability of execution, CRMs, Supply chain facility and Yes promoters vision plays a vital role.

Deeptech/ Cleantech/ Biotech/ Agritech/ HRtech/ Consumertech/ AI/ Edtech/ Adtech/ Fintech/ Healthtech/ Foodtech/ Gaming/

Basically, Startup founders are having the ideas but they requires huge amount of funding for,

- Research and Development,

- Setup Cost

- Marketing

- Hiring skill professionals

- To achieve minimal viable of Product

To support them Government is doing many programs for Skill building, providing them Grants, Incubations provides them a proper mentoring and networking with a prospective investor.

Startups are mainly categorized in,

1. Idea Stage – Early Stage – Seed Stage

2. Pre-Series Funding

3. Growth Stage

4. Development Stage

5. Later Stage – its also called as expansion stage where startups are driving for IPO where existing investors can get exit. Before IPO, they may also prefer route for exit of existing investor through the Buyback, Strategic sale, Third party sale.

Few of them Startups are,

- Nykaa – Beauty Tech

- Zomato – Food Tech

- Paytm – Fintech

- PB Fintech (Policy Bazaar) – Fintech

- Delhivery – Logistic Tech

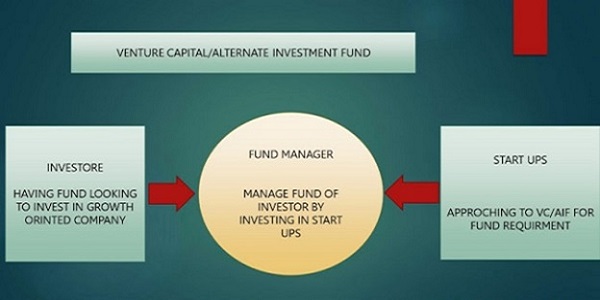

Alternate Investments Fund (AIFs): Way or Mediums for Startups to get potential funding for business.

These regulations shall be called the Securities and Exchange Board of India (Alternative Investment Funds) Regulations, 2012.

Definition: –

Alternative Investment Fund means any fund established or incorporated in India in the form of a trust or a company or a limited liability partnership or a body corporate which,-

(i) is a privately pooled investment vehicle which collects funds from investors, whether Indian or foreign, for investing it in accordance with a defined investment policy for the benefit of its investors; and

(ii) is not covered under the Securities and Exchange Board of India (Mutual Funds) Regulations, 1996, Securities and Exchange Board of India (Collective Investment Schemes) Regulations, 1999 or any other regulations of the Board to regulate fund management activities:

Provided that the following shall not be considered as Alternative Investment Fund for the purpose of these regulations,-

- Family Trusts

- ESOP Trusts set up under the Securities and Exchange Board of India

- Employee welfare trusts or gratuity trusts set up for the benefit of employees;

- Holding companies‘ within the meaning of Section 4 of the Companies Act, 1956;

- Other special purpose vehicles not established by fund managers, including securitization trusts, regulated under a specific regulatory framework;

- Funds managed by securitisation company or reconstruction company which is registered with the Reserve Bank of India under Section 3 of the Securitisation and Reconstruction of Financial Assets and Enforcement of Security Interest Act, 2002; and

- any such pool of funds which is directly regulated by any other regulator in India;

The AIF in India is regulated by the Securities Exchange Board of India (hereinafter referred to as “SEBI”), under the provisions of SEBI (Alternative Investment Funds) Regulations, 2012 (“AIF Regulations”) issued on May 21, 2012.

> Venture capital fund means an Alternative Investment Fund which invests primarily in unlisted securities of start-ups, emerging or early-stage venture capital undertakings mainly involved in new products, new services, technology or intellectual property right based activities or a new business model;

SEBI (Venture Capital Funds) Regulations, 1996.

> Angel Fund means a sub-category of Venture Capital Fund under Category I- Alternative Investment Fund that raises funds from angel investors and invests in accordance with

“Angel investor” means any person who proposes to invest in an angel fund and satisfies one of the following conditions,

> an individual investor who has net tangible assets of at least 2 crore rupees excluding value of his principal residence, and who:

-

- has early stage investment experience, or

- has experience as a serial entrepreneur, or

- is a senior management professional with at least ten years of experience;

Explanation: For the purpose of this clause, ‘early stage investment experience’ shall mean prior experience in investing in start-up or emerging or early-stage ventures and ‘serial entrepreneur’ shall mean a person who has promoted or copromoted more than one start-up venture.

- A body corporate with a net worth of at least 10 crore rupees; or

- An Alternative Investment Fund registered under these regulations or a Venture Capital Fund registered under the SEBI (Venture Capital Funds) Regulations, 1996

‘‘Foreign Venture Capital Investor’ means an investor incorporated and established outside India which proposes to make investment in Venture Capital Fund(s) or Venture Capital Undertaking(s) in India and is registered with SEBI under SEBI (Foreign Venture Capital Investors) Regulations, 2000;’

Venture capital undertaking means a domestic company which is not listed on a recognized stock exchange in India at the time of making investment; and which is engaged in the business for providing services, production or manufacture of article or things and does not include following activities or sectors:

- Non-banking financial companies;

- Gold financing;

Investible funds means the total amount of funds committed by investors to the Alternative Investment Fund by way of a written contract or any such document as on a particular date;

Private equity fund means an Alternative Investment Fund which invests primarily in equity or equity linked instruments or partnership interests of investee companies according to the stated objective of the fund;

Registration: –

Alternative Investment Funds shall seek registration categories mentioned hereunder:

- Category I Alternative Investment Fund which invests in start-up or early stage ventures or social ventures or SMEs or infrastructure or other sectors – Venture Capital Fund

- Category II Alternative Investment Fund which does not fall in Category I and III and which does not undertake leverage or borrowing other than to meet day-to-day operational requirements

- Category III Alternative Investment Fund which employs diverse or complex trading strategies and may employ leverage including through investment in listed or unlisted derivatives.

| Category I | Category II | Category II | |

| Venture Capital, Angel Fund, SME Fund, | Private Equity Fund, | Hedge Fund, PIPE Fund | |

| Instrument | start-up or early stage ventures or social ventures or SMEs or infrastructure | Equity and Debt Security | Listed/UnliCsted/Hedge Fund/ |

| Fees | 5 Lacs | 10 Lacs | 15 Lacs |

| Class | Closed ended | Close Ended | Open or Close |

| Tenure | 3 Years, Extension of 2 Years Sub to Approval 2/3 | 3 Years, Extension of 2 Years Sub to Approval 2/3 | No Minimum, Extension of 2 Years Sub to Approval 2/3 |

| Interest of Manager/ Sponsor | Lower of,

1. 2.5% of Corpus 0r 2. 5 Cr |

Lower of,

1. 2.5% of Corpus 0r 2. 5 Cr |

Lower of,

1. 5% of Corpus 0r 2.10 Cr |

| Limit | Invest upto 25% of fund in 1 Investee company directly or indirectly | Invest upto 25% of fund in 1 Investee company directly or indirectly | Listed up to 10% of NAV

Unlisted upto 10% of Investable fund |

Investment in AIFs:

- The Alternative Investment Fund may raise funds from any investor whether Indian, foreign or non-resident Indians by way of issue of units

- Each scheme of the Alternative Investment Fund shall have corpus of at 20 crore rupees

- The Alternative Investment Fund shall not accept from an investor, an investment of value less than one crore rupees:

- The Manager or Sponsor shall have a continuing interest in the Alternative Investment Fund of not less than two and half percent of the corpus or five crore rupees, whichever is lower

Provided that for Category III Alternative Investment Fund, the continuing interest shall be not less than five percent of the corpus or ten crore rupees, whichever is lower.

- No scheme of the Alternative Investment Fund shall have more than one thousand investors

- The fund shall not solicit or collect funds except by way of private placement

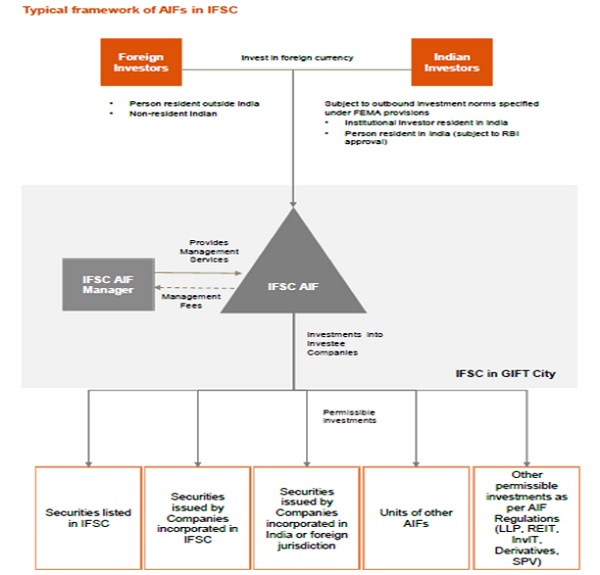

AIFs in Gift City: – IFSC – covers SEZ, Banking, SEBI, IRDAI, RBI as a single window compliance.

Source: Internet

The Government of India, launched first IFSC in “Gujarat International Finance Tec-City (GIFT)” with a object to make a global Financial and IT Service hub.

All three categories of Alternative Investment Funds (“AIFs”) (viz Category I, Category II and Category III) can be set up in an IFSC, including fund of funds.

The International Financial Services Centre Authority (IFSCA) has notified the IFSCA (Fund Management) Regulations. The IFSCA Fund Regulations have been introduced to regulate the framework for investment funds in India’s International Financial Services Centre (IFSC), in particular Gujarat International Finance Tec-City (GIFT City). The IFSCA Fund Regulations will come into force on the 30th (thirtieth) day from the date of its publication in the Official Gazette i.e. April 19, 2022.

As an immediate result of the introduction of the IFSCA Fund Regulations, various regulatory provisions and circulars issued by Securities and Exchange Board of India (SEBI) with respect to the funds in IFSC will cease to operate. Amongst others, the IFSCA Fund Regulations, in particular, repeal the applicability of SEBI (Alternative Investment Funds) Regulations, 2012; SEBI (Mutual Funds) Regulations, 1996; Chapter VI on Funds of SEBI (International Financial Services Centres) Guidelines, 2015, in IFSC. Further, all existing Fund Managers of Alternative Investment Fund (AIFs) registered by IFSCA will need to seek fresh registration from IFSCA under the IFSCA Fund Regulations within six (6) months from the effective date.

The IFSCA Fund Regulations in essence will govern, inter alia, an establishment of fund management entities (FMEs); schemes for fund management – venture capital schemes, restricted schemes (non-retail), retail schemes, special situation funds focusing on special situation assets, exchange traded funds; other fund management activities such as portfolio management, investment trust being Infrastructure Investment Trust (InvIT), Real Estate Investment Trust (REIT), family investment fund; environmental, social and governance (ESG) norms to be followed by FMEs; listing by the funds; general obligations and responsibilities; and advertisement by funds.

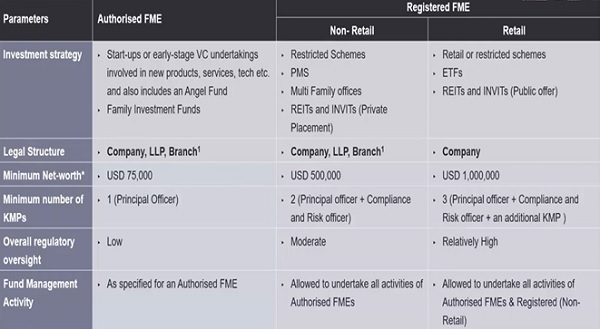

Classification of FMEs:

1. Authorized FMEs

2. Registered FMEs (Non-retail)

3. Registered FMEs (Reatils)

Authorised FME:

The FMEs that pool money from accredited investors or investors investing above the specified threshold by way of private placement and invest in start-ups or early-stage ventures through Venture Capital Scheme. Family Investment Fund investing in securities, financial products and such other permitted asset classes shall also seek registration as an Authorised FME.

Registered FME (Non-Retail):

The FMEs that pool money from accredited investors or investors investing above a specified threshold by way of private placement for investing in securities, financial products and such other permitted asset classes through one or more restricted schemes. Such FMEs shall also be able undertake Portfolio Management Services (including for multi-family office) and act as investment manager for private placement of Investment Trust (REITs and InvITs). Such FMEs shall also be able to undertake all activities as permitted to Authorised FMEs.

Registered FME (Retail):

The FMEs that pool money from all investors or a section of the investors under one or more schemes for investing in securities, financial products and such other permitted asset classes through retail or restricted schemes. Registered FME (Retail) may act as investment manager for public offer of Investment Trusts (REITs and InvITs). Such FMEs shall also be able to launch Exchange Traded Funds (ETFs). Further, such FMEs shall also be able to undertake all activities as permitted to Authorised FMEs and Registered FMEs (Non-retail).

Condition:

Scheme of Fund Management divide in:

> Restricted Schemes (Non-retail Scheme)

> Venture Capital Scheme |Green Channel

> Retail Scheme

> Family Investment Funds

> Special Situation Funds

> Exchange Traded Funds

> Environmental Social Governance

The detailed requirement under schemes is published by IFSCA regulation and can be reach at https://ifsca.gov.in/Regulation

Taxation of AIF and AIF in GIFT:

Fund Level:

> Category I and II shall have Pass through status

Nature of Income –

Venture Capital Income – Interest |Dividend |Gain or Loss from undertaking

> Non-VCU Income or Business Income shall have taxed at fund level, In case of AIF in GIFT 100% Tax holiday can claimed sub. To (10/15 years)

> AIF registered funds shall have to provide Form 64D or 64C to the Investor

Investors Level:

> Income shall be taxed at the hand of investor as if they had made investment based on Pass through income.

> Non-resident investors making investments in units of an IFSC AIF are not required to obtain a Permanent Account Number (PAN), or file income tax returns in India, provided they do not have any other taxable income from their activities or investments in India.

> Income accruing to or received by non-resident investors from offshore investments made by a GIFT City AIF should not be taxable in India.

Manger of Fund:

| Nature | AIF | AIF in GIFT |

| GST | Applicable | Not Applicable |

| Income Tax | Taxed | Tax holiday (10/15 Years) |

| TDS | Under 194LBB | Resident -10% and Non-resident – as applicable rate |

Author Bio