The Securities and Exchange Board of India (SEBI), at its 214th Board Meeting held on 19 June 2026, approved several regulatory reforms across the securities market. The Board simplified the framework for transmission of securities by introducing Quick Transmission Processing (QTP), increasing limits for simplified documentation, and reducing procedural requirements for legal heirs. It reintroduced open market buy-backs through stock exchanges from 1 August 2026 with revised operational safeguards and approved amendments to the Buy-back Regulations. SEBI also permitted intraday borrowings by mutual funds for liquidity management, introduced the GARUDA mechanism to expedite Alternative Investment Fund (AIF) scheme launches, and approved the transfer of the Social Stock Exchange Capacity Building Fund to a Section 8 company. Further, amendments were approved for securitised debt instruments and municipal debt securities regulations, including measures to encourage retail participation and improve market efficiency. The Board also approved an evidence-based review of the SME capital raising framework and adopted a new Code of Conduct for SEBI Members.

Securities and Exchange Board of India

Press Release No. 33/2026 | Dated: June 19th 2026

Key decisions taken in the SEBI Board Meeting dated 19th June, 2026

The 214th meeting of the SEBI Board was held in Mumbai today.

The SEBI Board, inter-alia, approved the following:

1. Simplifying and standardising the framework for transmission of securities

1.1 In order to facilitate faster and easier transmission of securities to legal heirs/claimants of deceased investors, the Board approved comprehensive reforms to existing transmission framework.

1.2 A new category of Quick Transmission Processing (QTP) for small-value claims (i.e. up to Z10 thousand for physical holdings and up to Z30 thousand for dematerialised holdings) has been introduced to facilitate efficient processing of such claims with minimal documentation.

1.3 Further, limits for simplified documentation have been doubled from Z5 lakh to Z10 lakh for physical holdings per listed company and from Z15 lakh to Z30 lakh for dematerialised holdings per beneficial owner.

1.4 The revised framework also introduces several documentation and process related simplifications, reducing procedural burden for claimants while improving operational efficiency for intermediaries such as:

1.4.1 Existing requirement of submission of PAN has been removed considering that PAN is already available for opening demat accounts.

1.4.2 Mandatory requirement of Probate of Will has been done away with, in line with recent amendments to succession laws.

1.4.3 Combined affidavit-cum-NOC in place of separate affidavit and NOC has been permitted.

1.4.4 In addition to original/attested copy of death certificate, copy of death certificate with QR Code has been added as eligible document in view of ease of verification using the QR Code.

1.4.5 For death certificates issued in foreign jurisdictions, additional modes for verification from overseas branches of Indian banks or any foreign bank with whom Indian banks have correspondent banking relationship have been specified.

1.5 The approved measures are expected to facilitate easier and faster transmission of securities and reduce costs and procedural hardship for claimants.

1.6 The aforementioned proposals were deliberated with the Industry Standards Forum for Registrars to an Issue and Share Transfer Agents and the Association of Mutual Funds in India and have factored in the feedback received on the consultation paper issued on March 12, 2026.

2. Re-introduction of Open Market Buy-back through Stock Exchanges and Review of the SEBI (Buy-back of Securities) Regulations, 2018

2.1 The Board approved amendments to the SEBI (Buy-back of Securities) Regulations, 2018, to re-introduce open market buy-back through stock exchanges and review of buy-back processes, in light of the revision in taxation framework and the suggestions received from stakeholders with the objective of providing greater flexibility in undertaking buy-backs, reducing procedural complexity and strengthening investor protection.

2.2 The approved amendments, inter alia, provide for the following:

2.2.1 As per the existing regulatory framework, buy-backs can be undertaken through tender offer route and open market route through book-building. Considering the revised taxation framework applicable for buy-backs, open market buy-back through stock exchange is being reintroduced with effect from August 01, 2026 to provide additional route for the company to undertake buy-back.

2.2.2 There shall be dissemination of information about open market buy-backs to shareholders through electronic means in addition to the public announcement being already made through newspaper advertisements.

2.2.3 The reintroduced open market buy-back through stock exchanges shall be completed within 66 working days from the opening of buy-back with at least 40% of funds earmarked shall be utilized during first half of buy-back period.

2.2.4 Due to changes in the taxation framework applicable for buy-back and the fact that promoters are not allowed to take part in open market buy-back, now open market buy-back through stock exchanges will be treated as normal trading transaction. Therefore, requirement of a separate trading window and display of the company’s identity as purchaser on the trading screen is being dispensed with.

2.2.5 Shares or other specified securities of the company for which it is undertaking buy-back, held by promoter(s) or his/their associates shall remain frozen at ISIN level during the buy-back period.

2.2.6 Buy-backs proposed to be undertaken shall be in compliance with minimum public shareholding requirements.

2.2.7 Interval between two buy-backs has been aligned with Companies Act, 2013.

2.2.8 With a view to reduce cost to the company and ease of doing business, the appointment of Merchant Banker is made discretionary on part of the company for undertaking buy-back. If company decides not to appoint merchant banker the activities undertaken by Merchant Banker have been assigned to Company, Compliance officer, Statutory Auditor, Secretarial Auditor and Stock Exchanges.

2.3 These amendments aim to streamline the regulatory framework governing buybacks, enhance operational efficiency and facilitate ease of doing business. It shall also ensure that there are no inadvertent dealing of shares by the promoter or his/their associates during buy-back period and thereby strengthen investor protection.

2.4 The proposals were deliberated by the Primary Market Advisory Committee (PMAC) and public consultation papers in this regard were issued on April 02, 2026 and May 08, 2026. The approved amendments incorporate relevant feedback received from PMAC and through the public consultation process.

3. Utilization of intraday borrowing by Mutual Funds

3.1 The Board approved the amendment to SEBI (Mutual Funds) Regulations, 2026 to facilitate intraday borrowings availed by mutual funds for managing liquidity mismatches during the day.

3.2 The aforesaid amendment allows mutual funds to avail intraday borrowing for bridging difference arising out of pay-in/ pay-out settlement timings within asset classes, forex settlements, payments for MTM of derivative positions etc., subject to certain safeguards. This is in addition to the borrowing currently permitted upto 20% of net assets of scheme, for the purpose of meeting unitholder payouts such as redemptions.

3.3 The quantum of such intraday borrowings shall be upto receivables sighted during the day. Intraday borrowing over and above this threshold, may be availed solely for the purpose of meeting unitholder pay-outs, as specified under Regulation 42(1) of SEBI (Mutual Funds) Regulations, 2026.

3.4 It shall be the responsibility of the AMCs that intraday borrowings are repaid by end of the day and any intraday borrowing converted to overnight borrowing shall be within the regulatory limits and for the purposes allowed in SEBI (Mutual Funds) Regulations, 2026.

3.5 Intraday borrowings shall not be used as a source of leverage. Additional conditions include maintenance of adequate documentation for the intraday borrowing and having a policy, duly approved by AMC/Trustee Board, for utilization of the said facility.

3.6 The aforementioned proposals were considered pursuant to feedback received in public consultation in May 2026, and detailed deliberations with MFAC, concerned industry associations and stakeholders.

4. Green-Channel: AIF Rollout Upon Document Acknowledgement (GARUDA) Mechanism for Processing of Placement Memorandum of Alternative Investment Funds (AlFs) filed with SEBI- Ease of Doing Business measure

4.1 In continuation of recent initiative taken by SEBI to reduce the timelines for launch of schemes (vide SEBI circular dated April 30, 2026), to enable faster and more efficient deployment of capital by AIFs, the Board has approved GARUDA Mechanism through amendment in SEBI (Alternative Investment Funds) Regulations, 2012. As a result,

4.1.1 For Non- Accredited Investor Schemes which excludes LVF, Al only scheme and Angel Funds (“Regular schemes”), timeline for launch of new schemes by AIFs has been reduced to 10 working days compared with a longer period required earlier.

4.1.2 Considering the level of sophistication of Als, Al only schemes and Angel Funds (which comprises of only Als) have been exempted from filing Private Placement Memorandum (PPM) through Merchant Banker and permitted to launch immediately upon grant of SEBI registration or filing of PPM with SEBI.

4.2 The proposals were deliberated before the Alternative Investment Policy Advisory Committee (‘AIPAC’) on April 28, 2026, and a public consultation paper in this regard was issued on May 11, 2026. The approved framework incorporates relevant feedback received from AIPAC and through public consultation.

5. Transfer of funds, administration & management of Capacity Building Fund (CBF) to Section 8 Company in respect of Social Stock Exchange

5.1 In terms of the extant framework for the Social Stock Exchange (SSE), the Capacity Building Fund (CBF) is presently housed at the National Bank for Agriculture and Rural Development (NABARD) as the administrative fund for undertaking capacity-building initiatives for SSE stakeholders.

5.2 However, upon the incorporation of the Social Stock Exchange—Capacity Building Foundation (SSE-CBF), a Section 8 company, the roles and responsibilities relating to capacity building of the SSE ecosystem are being taken over by SSE-CBF from CBF.

5.3 Board has granted approval to transfer the balance amount, administration and management of CBF from NABARD to SSE-CBF.

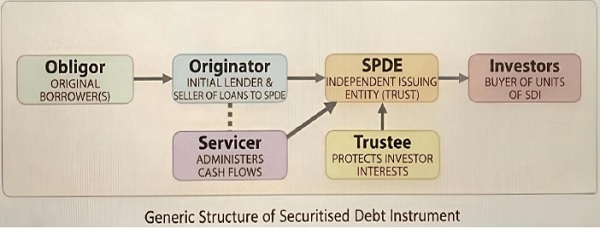

6. Amendments to SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008 (‘SDI Regulations’)

6.1 The Board approved the proposal for amendments to the SEBI (Issue and Listing of Securitised Debt Instruments and Security Receipts) Regulations, 2008, with the objective of aligning the regulatory framework governing listed securitisation transactions with the RBI’s framework on securitisation.

6.2 The amendments will enable development of listed SDI market and propose the following changes:

a) Permitting single-asset securitisation transactions by RBI-regulated entities.

| Existing position | Proposed position | Rationale |

| No obligor shall constitute more than 25% of the asset pool at the time of issuance of Securitised Debt Instruments (SDIs).

|

Exempting RBI- regulated entities (e.g. Banks, NBFCs) from the 25% obligorn concentration limit when undertaking securitisation.

Additional disclosure of the concentration risk arising from single- asset securitisation as a prominent risk factor in the offer document. |

This proposal aligns SDI regulations with the existing RBI framework, which permits single- asset securitisation for RBI-regulated entities. This will help in development of the listed securitisation market.

Additional disclosure will ensure that investors are fully aware of the potential concentration risk. |

b) Stipulating certain disclosure and reporting obligations in respect of servicers.

| Existing position | Proposed position | Rationale |

| Periodic disclosure obligations (such as monthly reports, performance data) are placed solely on the Originator of the securitized assets. | Shifting responsibility to Servicer for periodic disclosures and other related disclosures as mentioned in regulation. | This proposal aligns with the current practice, recognizing that the Servicer is the entity responsible for data collection and reporting. |

c) Aligning governance requirements relating to Constitution of Board of Trustee of SPDE for RBI regulated Originators.

| Existing position | Proposed position | Rationale |

| Trustees associated with the sponsor or originator cannot constitute more than one-half of the Board of Trustees of the SPDE.

|

For SPDEs where the originator is an RBI- regulated entity, it has been proposed to limit the originator’s representation on the Board to a maximum of one representative. | This proposal aligns SDI Regulations with the existing, more specific requirement within the RBI’s securitisation framework for RBI-regulated entities. |

d) Clarification regarding the originator and Special Purpose Distinct Entity (SPDE) belonging to the same group to enter into a securitization transaction.

| Existing position | Proposed position | Rationale |

| The plain reading of the existing provision gives an impression that SPDE shall not acquire any debt or receivables from any originator if they belong to the same group. | The revised wording clarifies that SPDE shall not acquire any debt or receivables from any originator if the originator is part of the same group as that of the trustee or the originator is under the same control as that of the trustee. | To remove any ambiguity while interpreting the existing regulation. |

e) Empowering SEBI to appoint a new trustee while suspending/ cancelling the registration of an old trustee

| Existing position | Proposed position | Rationale |

| While passing an order of suspension or cancellation of registration of a trustee, the Board may also direct winding up of schemes of the special purpose distinct entity (SPDE). | To appoint a new trustee in place of the old trustee whose registration is suspended or cancelled.

Additionally, retaining SEBI’s discretionary power to wind up schemes in exceptional circumstances (such as systemic risk, fraud) to protect investor interests. |

This will facilitate continuity of securitisation structure, in the event of suspension or cancellation of registration of trustee. |

6.3 These proposals are intended to promote regulatory alignment, increase operational efficiency and support the development of the listed securitisation market while maintaining appropriate investor protection safeguards.

6.4 The proposal to the Board was made after public consultation undertaken vide consultation paper issued on May 04, 2026, and based on the recommendations of the Corporate Bonds and Securitization Advisory Committee of SEBI.

6.5 For ease of reference, certain terminology used herein are explained as under:

a) ORIGINATOR: The entity that initially extends credit (loans, receivables, etc.) to the Obligor. This could be a bank, NBFC (Non-Banking Financial Company), housing finance company, or other lending institution.

b) OBLIGOR: The borrower(s) of the original loans/assets. These are the entities or individuals making payments on the underlying debt.

c) SPDE (Special Purpose Distinct Entity): A legally independent entity (trust) created specifically for the purpose of the securitization transaction.

d) TRUSTEE: SEBI registered Debenture Trustee to protect the interests of the investors.

e) SERVICER: The entity responsible for the day-to-day administration, including cash flow management of the underlying assets.

f) INVESTORS: Entities that purchase units of the SDIs issued by the SPDE.

7. Amendments to SEBI (Issue and Listing of Municipal Debt Securities) Regulations, 2015 (‘ILMDS Regulations’) The Board approved the amendments to the SEBI (Issue and Listing of Municipal Debt Securities) Regulations, 2015 (“ILMDS Regulations”) with the objective of development of municipal bond market. The key amendments are as under:

7.1 Re-financing as an objective for raising of funds: The amendments are aimed at enabling municipalities to raise funds for re-financing of existing debt of specific project(s). Municipalities shall be required to make disclosures in respect of the existing lenders and loan(s) that are being refinanced in the offer document/ placement memorandum to enable investors to assess the issuers financial health and liquidity risk.

7.2 Raising of funds by two or more municipalities through a Pooled finance vehicle: The current framework has an enabling provision for raising of funds by two or more municipalities through a pooled finance vehicle. The specific disclosures required to be made in the offer document, while raising funds through a pooled finance vehicle, shall be specified through this amendment. Further, operational aspects, viz. agreement between the pooled vehicle SPV (“issuer”) and the constituent municipalities and the escrow account mechanism, shall also be specified for clarity regarding the pooled finance arrangement and the repayment mechanism.

7.3 Encourage retail participation in municipal debt securities: Following measures shall be introduced to encourage retail participation and to provide greater clarity for municipal debt securities issued under the ILMDS Regulations:

7.3.1 In line with the provision under SEBI (Issue and Listing of Non-Convertible Securities) Regulations, 2021, issuers shall be permitted to offer incentives in the form of additional interest or a discount to the issue price to certain category of investors, namely senior citizens, women, serving and retired defence personnel, widows and widowers of defence personnel, retail individual investors or any other category of investors as may be specified by the Board from time to time.

7.3.2 The face value/ trading lot for municipal debt securities issued on private placement basis shall be specified as Rs. One Lakh or Rs. Ten Thousand. Municipal debt security issued at a face value of Rs. Ten Thousand shall have a fixed maturity and be without any structured obligations.

7.3.3 Electronic modes have been permitted for making advertisements for public issues.

7.4 Extension in timelines for post-issue event based compliances: Given the complexity and diversity of operations of municipalities, compiling accurate and comprehensive financial and operational data within the prescribed timelines is a significant challenge. Accordingly, the timelines for financial results shall be relaxed as under:

7.4.1 Submitting unaudited half-yearly financial results: From the current 45 days to 60 days from the end of half year, and

7.4.2 Submitting audited annual financial results: From the current 60 days to 90 days from the end of financial year.

7.5 These proposals are intended to support the development of the municipal debt market in India while maintaining appropriate investor protection safeguards.

7.6 The proposal to the Board was made after public consultation undertaken vide consultation paper issued on May 13, 2026, and based on the recommendations of the Corporate Bonds and Securitization Advisory Committee of SEBI.

8. Themes for Assessment proposed by External Experts Advisory Committee (EEAC)

The Union Budget 2025-26 had announced the establishment of a mechanism to assess the impact of existing regulations and subsidiary instructions, with the objective of enhancing regulatory responsiveness and supporting the continued development of the financial sector. In line with that vision and as guided by the Financial Stability and Development Council (FSDC) and FSDC-Sub Committee (FSDC-SC), SEBI had constituted an External Experts Advisory Committee (EEAC) in December 2025 as an independent advisory body to identify subjects for thematic, evidence-based reviews of regulatory frameworks. The Committee had deliberated on various themes which could be taken up for an independent review of regulations for FY 2026-27 and recommended the same for consideration of the SEBI Board.

The SEBI Board considered the recommendations of the Committee and approved the theme “Assessment of the framework for SME Capital Raising in Securities Markets” for an evidence-based review of the regulatory framework.

9. Code of Conduct for Members of the Securities and Exchange Board of India and amendments to the SEBI ESR Regulations to implement the recommendations of HLC

9.1 SEBI had set up a High-Level Committee on conflict of interest, disclosures and related matters in respect of Members and Officials of SEBI (“HLC” or “Committee”) to undertake a comprehensive review of the existing framework governing conflict of interest, disclosures and related matters in respect of Board Members and employees of SEBI.

9.2 The recommendations of HLC were approved by the Board in the previous meeting held on March 23, 2026 with suitable modifications. As a next step, the Board has now approved a new Code of Conduct for Members of SEBI, 2026 (“2026 Code”) and amendments to the SEBI (Employees’ Service) Regulations, 2001 (“ESR”).

9.3 The final Code and the amendments to the ESR shall be made available on SEBI website, after following due process including publication of ESR amendments in the Official Gazette.

Mumbai

June 19, 2026