SEBI Consultation Paper on Online Bond Trading Platforms – Proposed Regulatory Framework

Jul 21, 2022 | Reports : Reports for Public Comments

1. Background:

1.1. Debt securities can be issued either through a public issuance or on private placement basis. A Public issue of debt securities is made through the on-line system of the Stock Exchanges and Depositories. For privately placed debt securities, the following issues of debt securities has to be mandatorily made through Electronic Book Provider Platform (EBP Platform):

- In case of issuers who are in existence for three years and more, where the issue size is of Rs.100 crore or more;

- If the issuers are in existence for less than three years, irrespective of the issue size.

Presently, the following participants are eligible to bid on the EBP platforms:

- Qualified Institutional Buyers (QIBs);

- Non-QIBs including arrangers who/which has been authorized by the issuer.

1.2. A snapshot of the issuances of listed debt securities, including the number of issues and amount raised, investor category and number of allottees invested in privately placed debt securities, etc. is presented below.

1.2.1. Table 11: The details of issues made through public issuances and on private placement basis (listed) for last three Financial Years (FY) are given below:

| Period | FY2021-2022 | FY2020-2021 | FY2019-2020 | ||||

| Category | No. of Issues | Amt. in INR crore | No. of Issues | Amt. in INR crore | No. of Issues | Amt. in INR crore | |

| Public issues# | (1) | 28 | 11,589.40 | 18 | 10,588.02 | 34 | 14,984.02 |

| Private Placement * | (2) | 1,405 | 5,88,036.94 | 1,995 | 7,71,840.00 | 1,787 | 6,74,702. 17 |

| Total | (1) +(2) | 1,433 | 5,99,626.34 | 2,013 | 7,82,428.02 | 1,821 | 6,89,686. 19 |

| EBP Issues | 784 | 5,22,337.00 | 1,146 | 7,07,679.50 | 713 | 5,94,101. 00 | |

# Data for debt public issues have been taken on the basis of final post issuance reports received. * Listed issues; EBP – Electronic Book Provider platform.

1.2.2. Table 22: Data pertaining to category and number of allottees invested in recent issues of listed debt securities issued on private placement basis through the EBP Platform is as follows:

1.2.2. Table 22: Data pertaining to category and number of allottees invested in recent issues of listed debt securities issued on private placement basis through the EBP Platform is as follows:

| Sr. No. |

Name of the Issuer | ISIN | Date of credit of securities in NSDL system | Value of securitries as per face value credited in NSDL system (Rs. in Crs.) | No. of allottees who are QIBs/ institutions | No. of allottees who are non-QIBs/ individulas |

| 1 | Issuer 1 | ISIN 1 | 08/07/2022 | 800.00 | 1 | 0 |

| 2 | Issuer 2 | ISIN 2 | 08/07/2022 | 1350.00 | 2 | 0 |

| 3 | Issuer 3 | ISIN 3 | 08/07/2022 | 200.00 | 9 | 0 |

| 4 | Issuer 4 | ISIN 4 | 07/07/2022 | 681.10 | 1 | 0 |

| 5 | Issuer 5 | ISIN 5 | 07/07/2022 | 65.00 | 1 | 0 |

| 6 | Issuer 6 | ISIN 6 | 07/07/2022 | 300.00 | 3 | 0 |

| 7 | Issuer 7 | ISIN 7 | 07/07/2022 | 330.00 | 4 | 0 |

| 8 | Issuer 8 | ISIN 8 | 07/07/2022 | 125.00 | 2 | 0 |

| 23 | 0 |

1.2.3. From the above two tables, the following is observed:

1.2.3.1. A substantial number of issuances of debt securities is through private placement mode.

1.2.3.2. While non-QIB investors authorized by the issuer are eligible for bidding/ participating on the EBP platform, there is no participation from non-institutional investors as hardly any market participant (including non-institutional investors) other than QIBs invests through the EBP platforms.

1.3. This perhaps explains why a number of online bond platforms have mushroomed over the past two to three years, which sell debt securities to investors, particularly non-institutional investors. Some of these platforms seemingly operate in a manner similar to organized avenues for trading a’la market infrastructure institutions, especially stock exchanges, bringing together buyers and sellers (most often only the platform providers) for executing trades in debt securities. While these bond platforms do tap a group of investors, particularly non-institutional investors to invest in bonds, they do not come under any regulatory purview i.e. the platform providers are not registered with any regulator. This has given rise to a need to guide and regulate these platforms in order to bring about, inter-alia, regulatory oversight, common standard practices, investor redress mechanism etc. Towards this end, this paper attempts to bring forth the salient features of such bond platforms and proposes framework for regulating them.

2. Indian bond platforms :

2.1. In India, most of such bond platforms are fintech companies or are backed by brokers. The following table3 provides a snapshot of some of the platforms currently offering debt securities to investors in India:

| Platform | Backed by | No. of users registered* |

| GoldenPi | GoldenPi Technologies Private Limited | 1,18,350 |

| BondsIndia | Launchpad Fintech Private Limited | 437 |

| Harmoney | Wealthsigns Fintech Private Limited | 632 |

| Altifi | Northern Arc Capital Limited | 867 |

| Wintwealth | Fourdegreenwater Capital Private Limited | 9766 |

| BondsKart | JM Financial Products Ltd | 6133 |

| Indiabonds | India Bond Private Limited | 5192 |

*As on January 31, 2022

2.2. Among the platforms mentioned in the table, GoldenPi was launched in 2018, whereas all other platforms were launched during 2020 and thereafter. It is observed that other platforms like AxisYield (backed by Axis Securities, a broker), Plutus (backed by CredAvenue, a fintech company) have been launched recently.

2.3. The majority of the investors registered on these platforms are non-institutional investors.

2.4. The data regarding the transactions undertaken on the bond platforms were sought from two bond platforms. The summary of the data is given in the table below:

Financial

|

No. of issues offered for sale |

No. of

|

No. of

|

For institutional investors |

For non-institutional investors |

||||

No. of Users/ investors who have transacted on bond platform |

Volume

|

Volumeof trades (Amt in crore) |

No. of Users/ investors who have transacted on bond platform |

Volume

|

Volumeof trades (Amt in crore) |

||||

2019-20 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

0 |

2020-21 |

1 |

1 |

9862 |

0 |

0 |

0 |

2037 |

189350 |

19.935 |

2021-22 |

25 |

20 |

244671 |

1 |

2 |

36.12 |

5632 |

443158 |

120.54 |

2.5. Based on the analysis of the data above, the following is inferred:

2.5.1. There has been a significant increase in the number of users registered on the bond platforms.

2.5.2. There has been a noticeable increase in the volume of trades undertaken on the bond platform as well as in the number of users who have transacted on the bond platform.

2.5.3. Majority of the investors transacting on the bond platforms are non-institutional investors.

3. International experience:

Globally, bond platforms have been in existence for almost a decade. There are several platforms across the globe that facilitate trading in debt securities. Some of them are as follows4:

| Name of platform | Country | Funding | Year |

| TruMid | USA | 788 Mn USD | 2014 |

| Origin | UK | 10 Mn USD | 2015 |

| CoPower | Canada | 2 Mn USD | 2013 |

| Market Axess | USA | – | 2000 |

| WorthyBonds | USA | 213 k USD | 2017 |

| ElectronFile | USA | 12 Mn USD | 2013 |

| EM Bonds | USA | 7 Mn USD | 2013 |

| Tongbanje | China | 60 Mn USD | 2012 |

| DelphX | USA | – | 2011 |

4. Reasons for rise in the number of bond platforms:

Persistently low interest rates in the recent years have reduced the interest of the investors in fixed deposits. Additionally, with the rise of digitalization and increasing penetration of the internet, there has been a consequential growth in the technological temper of investors, making them more tech-savvy. Further, offering of debt securities by online bond platforms provides an attractive and alternative investment option to non-institutional investors. The following are significant to note:

4.1. Enhanced visibility of investment options for non-institutional investors as a variety of bonds are available for purchase on such platforms;

4.2. During the course of the lockdown due to the Covid-19 pandemic, there has been a substantial increase in the number of demat accounts and investors in securities market.

4.3. Returns offered on bond platforms are generally more attractive as compared to fixed deposits.

4.4. Bond platforms enable easy access to non-institutional investors for investment in debt securities as they provide an interface similar to that of online shopping websites such as Amazon, Flipkart etc.

5. Issues concerning bond platforms:

As mentioned earlier in this paper, bond platforms largely tap into the non-institutional segment, hitherto unexplored as far as bond market investment is concerned. While it is a welcome sign that more investors are investing in the bond market, these platforms also give rise to certain concerns. The following are the possible regulatory concerns as regards to the functioning of bond platforms:

5.1. Lack of regulatory oversight:

At present, these platforms are not governed by any regulatory framework. The sanctity of transactions executed on these platforms especially by non-institutional investors may be a cause of concern as there is no statutory obligation on these platforms to ensure completion of the entire leg of transaction including settlement. Moreover, in case of any infirmity in any transaction on the platforms, investors may not have any recourse.

5.2. Listed and unlisted securities:

Presently, it is observed that both listed and unlisted debt securities are being offered on the same webpage/ under the same tab on the websites of these platforms. While the

listing status of the debt securities is being mentioned by the bond platforms, an investor needs to be discerning in order to distinguish between the two. Hence there is a need to separate the two, on the basis of the listing status of the security.

5.3. Absence of standards for Know Your Client (KYC) norms:

Each of these platforms has its own KYC norms. Prima facie, it was observed that many of these platforms do not align and/ or comply with the Prevention of Money Laundering Act, 2002 (PMLA) guidelines or SEBI KYC requirements.

5.4. Ambiguity in redressing Investor Grievances:

It is not certain as to how investor grievances is handled by these platforms and each of the platform may have their own method/ process for the same. For trades done through regulated platforms, presently, the Investor Services Cell (ISC) of the Stock Exchange caters to the needs of investors by addressing the queries of investors, resolving investor complaints and providing Arbitration Mechanism for quasi-judicial settlement of disputes. Bringing a regulatory framework for these bond platforms will ensure extension of the services of the ISC to investors on these bond platforms.

5.5. Possibility of mis-representation:

A major concern also arises from the possibility of investors having a false sense that reporting of the transactions by the platforms to Stock Exchanges would mean that the stock exchange investor protection framework is applicable and that the Exchange will address any investor grievances arising from these transactions.

5.6. Conflict of interest, product offerings, information availability and possible mis-selling:

To attract non-institutional investors, these platforms may offer high yield securities to whet the investor appetite. While certainly it is the decision of an investor to invest in a low rated/ high yielding security, there is a concern that such high yield securities may be relatively lower rated securities and investors may fall prey to mis-selling of such offerings, due to lack of appropriate product disclosures, which may not be commensurate with the investor’s risk appetite. There is also the possibility of the bond platforms’ involvement with the issuers by way of cross holdings/ management linkages etc. in which case, the cause for regulation is only more.

5.7. Concerns regarding Deemed Public Issue:

5.7.1. There is a concern that down selling of the debt securities issued on private placement basis by the bond platforms to a large number of investors may possess the characteristics of a deemed public issue (DPI).

5.7.2. To understand this concern better, data of listed debt securities issued on private placement basis during FY 2021-22 subscribed by and further offered for sale by few bond platforms was analysed, wherein it was observed that in couple of instances, the entire issue was down sold to more than 200 investors within 15 days from the date of allotment.

5.7.3. While at present, the number of transactions and number of investors involved in such bond platforms are limited, it may receive more traction and as the volumes grow, the number of investors to whom such debt securities would be down sold may increase. Thus, concerns regarding DPIs are only well founded.

5.7.4. Further, Section 25 (2) (a) of the Companies Act, 2013 inter-alia provides that:

“For the purposes of this Act, it shall, unless the contrary is proved, be evidence that an allotment of, or an agreement to allot, securities was made with a view to the securities being offered for sale to the public if it is shown—

(a) that an offer of the securities or of any of them for sale to the public was made within six months after the allotment or agreement to allot;

Thus, if debt securities issued on private placement basis are offered for sale by the bond platforms to more than 200 investors, it would violate the above mentioned provision of Companies Act. 2013.

5.8. Reporting of trades:

5.8.1. As per the norms for trading in debt securities mentioned in the SEBI Operational Circular dated August 10, 2021 (amended till date), all persons dealing in such securities are required to report transactions to the trade reporting platform of the Exchanges and settle such transactions through Clearing Corporations of the Exchanges.

5.8.2. As per the current regulatory mandate, only mutual funds, insurance companies and portfolio managers are required to execute specified portions of their overall corporate bond transactions through Request for Quote (RFQ) Platform.

5.8.3. While all persons dealing in such securities are required to report transactions to the trade reporting platform of the Exchanges and settle such transactions through Clearing Corporations of the Exchanges, bringing the bond platforms under the regulatory purview will ensure compliance with the aforesaid provisions.

5.9. Clearing and settlement:

On a cursory look at the details of the processes followed by the bond platforms, inconsistencies in certain procedural norms were observed. The role of Stock Exchanges/ Clearing Corporations also appeared to be bypassed in many instances. The role of Clearing Corporations was played by these bond platforms in certain instances by directly accepting funds from the client and processing the security settlement through off-market mode. These instances were also observed in cases where the bonds are unlisted and/or the value of the transaction is below Rs. 2 lakhs in view of RTGS restrictions.

6. Discussions and evaluation of alternatives:

Issues regarding bond platforms were discussed in SEBI’s Corporate Bonds & Securitization Advisory Committee (CoBoSAC). Pursuant to the discussions, it was observed that there is an imperative need to govern the operations of these online bond platforms, keeping in mind the core objective of facilitation of efficient trading and robust investor protection norms for investors particularly non-institutional investors. The key points of the proposed regulatory framework emanating from such discussions are given below:

6.1. Mandatory SEBI Stock-Broker registration:

Bond platforms play the role of facilitators, thereby facilitating transactions by investors registered on their websites. Therefore, it is proposed that these bond platforms should register as stock-brokers (debt segment) with SEBI or be run by SEBI registered brokers. This will also enhance the confidence among investors, particularly non-institutional investors, as the platforms would be provided by SEBI regulated intermediaries. Additionally, the stock-broker regulations will be applicable to these entities, which would govern their code of conduct and other aspects related to their operations and risk management.

6.2. Eligible securities:

The debt securities offered for buy/ sale by the online bond platforms shall be only listed debt securities.

6.3. Proposed Lock-in period for the eligible securities:

To address the issue of DPI mentioned in para 5.7 above, it is proposed that listed debt securities issued on private placement basis, offered for sale on bond platforms shall be locked-in for a period of six months from the date of allotment of such debt securities by the issuer.

6.4. Channelizing transactions through either of the following two options:

6.4.1. Exchange Platform – Debt segment: The transactions executed on the online bond platforms are to be routed through the trading platform of the debt segment of Exchanges. Routing their trades through the trading platform of Exchanges, will help in mitigating settlement risk associated with these online bond platforms as the settlement is guaranteed on T+2 basis.

6.4.2. Request for Quote Platform (RFQ): Alternatively, the transactions executed on the online bond platforms can be routed through RFQ platform of the Stock Exchanges where the transactions will be cleared and settled on a Delivery Versus Payment (DVP-1) basis.

6.4.3. The APIs of the Exchange platforms can be utilised by the bond platforms for ease of integration with the Exchange systems mentioned above. This will be similar to the trading model followed for equity transactions, where stock brokers build their own front-end for facilitating placing of orders by their clients and the transactions are executed on the Exchange trading platforms. The platforms will, thus, continue to maintain the current web interface (front end), where they will show the list of available debt securities, ratings, risk associated and other information of the debt securities on their website.

7. Benefits of the proposed Regulatory framework:

7.1. Registration of the bond platforms as stock brokers under SEBI Regulations, will be beneficial to the market and market participants as:

7.1.1. The standard KYC requirements will be applicable while registering clients on bond platforms.

7.1.2. The Net worth and deposit requirements prescribed for stock brokers will ensure that the bond platform has a sound and stable financial health.

7.1.3. The applicability of code of conduct mandated for stock brokers will ensure fairness in their dealings with clients.

7.1.4. They will be subjected to regulatory inspection and oversight, providing more confidence to investors and hence, will have the potential to attract more investors.

7.2. Routing of transactions through trading platform of Exchanges will provide the following benefits:

7.2.1. Robust Risk Management framework and Surveillance mechanism;

7.2.2. Fair and transparent pricing;

7.2.3. Guaranteed settlement;

7.2.4. Exit opportunity to the investors;

7.2.5. Augment market making; and

7.2.6. Well defined framework for redress of Investor grievances

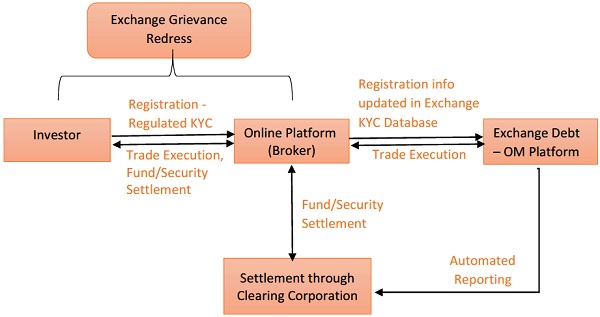

8. Proposed transaction structure

8.1. The proposed structure of the transactions to be executed on bond platforms highlighting the role of the stakeholders is as under:

8.2. The proposed framework would attempt to ensure:

8.2.1. Retention of the business potential and opportunities for the bond platforms;

8.2.2. Efficient offering of services to the non-institutional investors.

9. Public Comments

Public comments are invited for the proposed regulatory framework for the online bond platforms that are selling listed debt securities. The comments/ suggestions may be provided as per the format given below:

| Name of the person/ entity proposing comments: | |||

| Name of the organization (if applicable): | |||

| Contact details: | |||

| Category: whether market intermediary/ participant (mention type/ category) or public (investor, academician etc.) | |||

| Sr. No. | Issues | Proposals/ Suggestions | Rationale |

Kindly mention the subject of the communication as, “Comments on Consultation paper on Online Bond Trading Platforms – Proposed Regulatory Framework”.

Comments as per aforesaid format may be sent to the following, latest by August 12, 2022 (within 21 days from date of publication of this consultation paper on SEBI website) through the following modes:

a. By email to: pradeepr@sebi.gov.in; nikhilc@sebi.gov.in; and kirand@sebi.gov.in or

b. By post to the following address:

Pradeep Ramakrishnan,

General Manager,

Department of Debt & Hybrid Securities

Securities and Exchange Board of India,

SEBI Bhavan, C4-A, G-Block,

Bandra Kurla Complex, Bandra (East),

Mumbai – 400051

Issued on: July 21, 2022

Notes:

1 Source: NSE, BSE, CDSL and NSDL

2Source: NSDL; Issues on July 07 and 08, 2022

3 Source: data collected from bond platforms

4 https://tracxn.com/d/trending-themes/Startups-in-Fixed-Income-Trading-Platforms