Reserve Bank of India

Date : Aug 06, 2021

Governor’s Statement : August 6, 2021

The Monetary Policy Committee (MPC) met on 4th, 5th and 6th August 2021. Based on an assessment of the evolving domestic and global macroeconomic and financial conditions and the outlook, the MPC voted unanimously to keep the policy repo rate unchanged at 4 per cent. The MPC also decided on a 5 to 1 majority to continue with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target, going forward. The marginal standing facility (MSF) rate and the bank rate remain unchanged at 4.25 per cent. The reverse repo rate also remains unchanged at 3.35 per cent.

2. Today, we are in a much better position than at the time of the MPC’s meeting in June 2021. As the second wave of the pandemic ebbs, containment eases and we slowly build back, vaccine manufacturing and administration are steadily rising. Yet the need of the hour is not to drop our guard and to remain vigilant against any possibility of a third wave, especially in the background of rising infections in certain parts of the country.

3. Our actions, together with those of the Government, are aimed at alleviating distress and prioritising growth, while keeping the financial system healthy and stable. Our approach can be best described by weaving together two quotes from Martin Luther King Jr1 “But I know, somehow, that only when it is dark enough can you see the stars. Keep moving. Let nothing slow you up. Move on …..”

4. Let me begin by setting out the rationale underlying the MPC’s decision. The MPC met in the shadow of the two recent inflation prints being above the upper tolerance band of the inflation target. It noted that economic activity has broadly evolved on the lines of the MPC’s expectations in June and the economy is recovering from the setback of the second wave. The monsoon has revived after a brief hiatus and kharif sowing is gaining momentum. Some high frequency indicators are also looking up again during June-July. Our expectation is that activity is likely to gather pace with progressive upscaling of vaccinations, continued large policy support, buoyant exports, better adaptations to COVID-related protocols, and benign monetary and financial conditions.

5. Consumer price inflation surprised on the upside in May, reflecting a combination of adverse supply shocks, elevated logistics costs, high global commodity prices and domestic fuel taxes. In June, headline inflation remained above the upper tolerance level, but price momentum moderated. Also, core inflation softened from its peak in May. International crude oil prices remain volatile; any moderation in prices as a consequence of the OPEC plus agreement could contribute towards alleviating inflation pressures.

6. On balance, the outlook for aggregate demand is improving, but the underlying conditions are still weak. Aggregate supply is also lagging below pre-pandemic levels. While several steps have been taken to ease supply constraints, more needs to be done to restore supply-demand balance in a number of sectors of the economy. The recent inflationary pressures are evoking concerns; but the current assessment is that these pressures are transitory and largely driven by adverse supply side factors. We are in the midst of an extraordinary situation arising from the pandemic. The conduct of monetary policy during the pandemic has been geared to maintain congenial financial conditions that nurture and rejuvenate growth. At this stage, therefore, continued policy support from all sides – fiscal, monetary and sectoral – is required to nurture the nascent and hesitant recovery. The MPC continues to be conscious of its mandate of anchoring inflation expectations as soon as the prospects for strong and sustainable growth are assured. Accordingly, the MPC decided to retain the prevailing repo rate at 4 per cent and continue with the accommodative stance with all its nuances.

Assessment of Growth and Inflation

Domestic Growth

7. Domestic economic activity has started normalising with the ebbing of the second wave of the virus and the phased reopening of the economy. High-frequency indicators suggest that (i) consumption (both private and Government), (ii) investment and (iii) external demand are all on the path of regaining traction. Let me elaborate on each of these three aspects. Further easing of restrictions and increasing coverage of vaccinations are likely to boost private spending on goods and services including travel, tourism and recreational activities, propelling a broad-based recovery in aggregate demand. The robust outlook for agriculture and rural demand would continue to support private consumption. Urban demand is likely to accelerate with recovery in manufacturing and non-contact intensive services, release of pent-up demand and the pace of vaccination. This is corroborated by encouraging movements in several high frequency indicators, viz., registration of automobiles, electricity consumption, non-oil non-gold imports, consumer durable sales and hiring of urban workers. The results of the July round of the Reserve Bank’s consumer confidence survey suggest that one year ahead sentiments returned to optimistic territory from historic lows. Early results from listed firms show that corporates have been able to maintain their healthy growth in sales, wage growth and profitability, led by information technology firms. This will also support aggregate disposable income of consumers.

8. Although investment demand is still anaemic, improving capacity utilisation, rising steel consumption, higher imports of capital goods, congenial monetary and financial conditions and the economic packages announced by the Central Government are expected to kick-start a long-awaited revival. Firms polled in the Reserve Bank’s surveys expect expansion in production volumes and new orders in Q2:2021-22 which would sustain through Q4:2021-22, boding well for investment. Innovation and working models adopted during the pandemic by businesses will continue to reap efficiency and productivity gains even after the pandemic recedes. This should help trigger a virtuous cycle of investment, employment and growth.

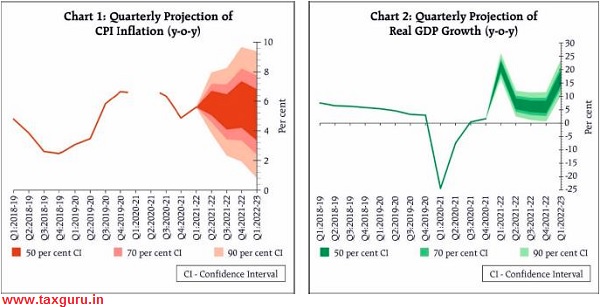

9. External demand remained buoyant during Q1:2021-22 and was reflected in increasing exports, lending critical support to aggregate demand. Strong external demand is an opportunity for India and further policy support should help in capitalising on this. Global commodity prices and episodes of financial market volatility, together with vulnerability to new waves of infections are, however, downside risks to economic activity. Taking all these factors into consideration, projection of real GDP growth is retained at 9.5 per cent in 2021-22 consisting of 21.4 per cent in Q1; 7.3 per cent in Q2; 6.3 per cent in Q3; and 6.1 per cent in Q4 of 2021-22. Real GDP growth for Q1:2022-23 is projected at 17.2 per cent.

Inflation

10. Headline CPI inflation edged up sharply to 6.3 per cent in May driven by a broad-based pick-up across all major groups on adverse supply shocks, sector-specific demand-supply mismatches and spillovers from rising global commodity prices. It remained at 6.3 per cent in June; however, core inflation registered an appreciable moderation.

11. The revival of the south-west monsoon and pick up in kharif sowing, buffered by adequate food stocks should help in containing cereal price pressures in the months ahead. High frequency food price indicators show some moderation in prices of edible oils and pulses in July on the back of supply side interventions by the government. Inflation in core services like house rentals remains below historical averages, reflecting subdued demand conditions. Crude oil prices are volatile with implications for imported cost pressures on inflation. The combination of elevated prices of industrial raw materials, high pump prices of petrol and diesel with their second-round effects, and logistics costs continue to impinge adversely on cost conditions for manufacturing and services, although weak demand conditions are tempering the pass-through to output prices and core inflation.

12. Before the onset of the pandemic, headline inflation and inflationary expectations were well anchored at 4 per cent, the gains from which need to be consolidated and preserved. Stability in inflation rate fosters credibility of the monetary policy framework and augurs well for anchoring inflation expectations. This, in turn, reduces uncertainty for investors, reduces term and risk premia, increases external competitiveness and, thus, is growth-promoting. Since the start of the pandemic, the MPC has prioritised revival of growth to mitigate the impact of the pandemic. The available data point to exogenous and largely temporary supply shocks driving the inflation process, validating the MPC’s decision to look through it. The supply-side drivers could be transitory while demand-pull pressures remain inert, given the slack in the economy. A pre-emptive monetary policy response at this stage may kill the nascent and hesitant recovery that is trying to secure a foothold in extremely difficult conditions.

13. Inflation may remain close to the upper tolerance band up to Q2:2021-22, but these pressures should ebb in Q3:2021-22 on account of kharif harvest arrivals and as supply side measures take effect. Taking into consideration all these factors, CPI inflation is now projected at 5.7 per cent during 2021-22: 5.9 per cent in Q2; 5.3 per cent in Q3; and 5.8 per cent in Q4 of 2021-22, with risks broadly balanced. CPI inflation for Q1:2022-23 is projected at 5.1 per cent.

Liquidity and Financial Market Conditions

14. During June-July, global financial markets turned volatile in response to higher inflation numbers in several countries and the fear of early policy normalisation with skewed economic recovery in some advanced countries. These developments need to be factored into our policy matrix for framing an appropriate response, given that safeguarding the economy from the vicissitudes of global spillovers and ensuring financial stability remain a top priority for the Reserve Bank. Nonetheless, domestic macroeconomic situation and the evolving growth inflation dynamics will continue to be the principal pivot of our monetary policy actions.

15. The Reserve Bank through its market operations, both conventional and unconventional, has maintained ample surplus liquidity since the onset of the pandemic to ensure easing of financial conditions in support of domestic demand. Buoyed by the renewed vigour of capital inflows and the Reserve Bank’s purchase of government securities in the secondary market, total absorption through reverse repos surged from a daily average of ₹5.7 lakh crore in June to ₹6.8 lakh crore in July 2021 and further to ₹8.5 lakh crore in August 2021 so far (up to August 4).

16. Under the revised liquidity management framework announced on February 06, 2020, the Reserve Bank has been conducting 14-day variable rate reverse repo (VRRR) auctions as its main liquidity operation. With the commencement of normal liquidity operations, the VRRR, which was temporarily held in abeyance during the pandemic, has been re-introduced since January 15, 2021 and the initial absorption of ₹2 lakh crore has been rolled over in the subsequent fortnightly auctions. In parallel, access to the fixed rate overnight reverse repo has been kept open. Markets have adapted and even welcomed the VRRR in view of the higher remuneration it offers relative to the fixed rate overnight reverse repo. Fears that the recommencement of the VRRR tantamounts to liquidity tightening have been allayed. We have seen higher appetite for VRRR in terms of the bid-cover ratio in the auctions. Considering all these aspects, it has now been decided to conduct fortnightly VRRR auctions of ₹2.5 lakh crore on August 13, 2021; ₹3.0 lakh crore on August 27, 2021; ₹3.5 lakh crore on September 9, 2021; and ₹4.0 lakh crore on September 24, 2021. These enhanced VRRR auctions should not be misread as a reversal of the accommodative policy stance, as the amount absorbed under the fixed rate reverse repo is expected to remain more than ₹4.0 lakh crore at end-September 2021. Needless to add that the amount accepted under the VRRR window forms part of system liquidity.

17. The Reserve Bank’s secondary market G-sec acquisition programme (G-SAP) has been successful in anchoring yield expectations while eliciting keen response from market participants. We propose to conduct two more auctions of ₹25,000 crore each on August 12 and August 26, 2021 under G-SAP 2.0. We will continue to undertake these auctions and other operations like open market operations (OMOs) and operation twist (OT), among others, and calibrate them in line with the evolving macroeconomic and financial conditions.

18. It is necessary to have active trading in all segments of the yield curve for its orderly evolution. Our recent G-SAP auctions that have focussed on securities across the maturity spectrum are intended to ensure that all segments of the yield curve remain liquid. Furthermore, our options are always open to include both off the run and on the run securities in the G-SAP auctions and operation twist. It is expected that the secondary market volumes would pick up and market participants take positions that lead to two-way movements in yields.

19. Our endeavour as the debt manager of both Central and state Governments has been to ensure an orderly completion of their borrowing programmes at a reasonable cost while minimising rollover risk. In my earlier statements, I have emphasised orderly evolution of the yield curve as a public good in which both market participants and the Reserve Bank have a shared responsibility. As G-sec yields serve as a benchmark and have a high signalling value for other segments of the debt market, guidance on orderly path of yields was provided through auction cut-offs, devolvements, cancellations and exercise of green shoe options in primary market operations. The introduction of uniform price auctions announced recently for issuance of securities up to 14 years tenor is expected to mitigate risks that bidders may face in the primary segment. The decision of the Government to accommodate the GST compensation payment to states for the first half of the year within the existing cash balances should assuage market concerns on the size of Government’s borrowing programme this year.

20. The efficacy of RBI’s monetary policy measures and actions is reflected in the significant improvement in transmission during the current easing cycle. The reduction in repo rate by 250 basis points since February 2019 has resulted in a cumulative decline by 217 basis points in the weighted average lending rate (WALR) on fresh rupee loans. Domestic borrowing costs have eased, including interest rates on market instruments like corporates bonds, debentures, CPs, CDs and T-bills. In the credit market, transmission to lending rates has been stronger for MSMEs, housing and large industries. The low interest rate regime has also helped the household sector reduce the burden of loan servicing. The significant reduction in interest rates on personal housing loans and loans to commercial real estate sector augurs well for the economy, as these sectors have extensive backward and forward linkages and are employment intensive.

Additional Measures

21. After the onset of the pandemic, the Reserve Bank has announced more than 100 measures to mitigate its impact. Going forward, our endeavour would be to continue the monitoring of measures which are still in operation to ensure that the benefit of all our measures percolate down to targeted stakeholders. Against this backdrop and based on our continuing assessment of the macroeconomic situation and financial market conditions, certain additional measures are being announced today. The details of these measures are set out in the statement on developmental and regulatory policies (Part-B) of the Monetary Policy Statement. Let me outline these measures.

On-tap TLTRO Scheme: Extension of Deadline

22. The scope of the on-tap TLTRO scheme, initially announced on October 9, 2020 for five sectors, was further extended to stressed sectors identified by the Kamath Committee in December 2020 and bank lending to NBFCs in February 2021. The operating period of the scheme was also extended in phases till September 30, 2021. Given the nascent and fragile economic recovery, it has now been decided to extend the on-tap TLTRO scheme further by a period of three months, i.e. till December 31, 2021.

Marginal Standing Facility (MSF): Extension in Period of Relaxation

23. On March 27, 2020, banks were allowed to avail of funds under the marginal standing facility (MSF) by dipping into the Statutory Liquidity Ratio (SLR) up to an additional one per cent of net demand and time liabilities (NDTL), i.e., cumulatively up to 3 per cent of NDTL. To provide comfort to banks on their liquidity requirements, including meeting their Liquidity Coverage Ratio (LCR) requirement, this relaxation which is currently available till September 30, 2021 is being extended for a further period of three months, i.e., up to December 31, 2021. This dispensation provides increased access to funds to the extent of ₹1.62 lakh crore and qualifies as high-quality liquid assets (HQLA) for the LCR.

LIBOR Transition-Review of Guidelines – Export Credit in Foreign Currency and Restructuring of Derivative Contracts

24. The transition away from London Interbank Offered Rate (LIBOR) is a significant event that poses certain challenges for banks and the financial system. The Reserve Bank has been engaging with banks and market bodies to proactively take steps. The Reserve Bank has also issued advisories to ensure a smooth transition for regulated entities and financial markets. In this context, it has been decided to amend the guidelines related to (i) export credit in foreign currency and (ii) restructuring of derivative contracts. Banks will be permitted to extend export credit in foreign currency using any other widely accepted Alternative Reference Rate in the currency concerned. Since the change in reference rate from LIBOR is a “force majeure” event, banks are also being advised that change in reference rate from LIBOR/ LIBOR related benchmarks to an Alternative Reference Rate will not be treated as restructuring.

Deferral of Deadline for Achievement of Financial Parameters under Resolution Framework 1.0

25. The resolution plans implemented under the Resolution Framework for COVID-19 related stress announced on August 6, 2020 require sector specific thresholds to be met in respect of certain financial parameters. Of these parameters, the thresholds in respect of four parameters relate to operational performance of the borrowing entities, viz. Total Debt to EBIDTA ratio, Current Ratio, Debt Service Coverage Ratio and Average Debt Service Coverage Ratio. These ratios are required to be met by March 31, 2022. Recognizing the adverse impact of the second wave of COVID-19 and the resultant difficulties on revival of businesses and in meeting the operational parameters, it has been decided to defer the target date for meeting the specified thresholds in respect of the above four parameters to October 1, 2022.

Concluding Remarks

26. As the COVID-19 second wave ebbs, there is optimism that with adequate pandemic protocols and ramp-up in the vaccination rate, we should be able to tide over a third wave, if it occurs. As a nation, we should continue to be vigilant and ready to proactively deal with any resurgence of the pandemic with more rapidly transmissible mutants of the virus, should it happen.

27. The recovery remains uneven across sectors and needs to be supported by all policy makers. The Reserve Bank remains in “whatever it takes” mode, with a readiness to deploy all its policy levers – monetary, prudential or regulatory. In parallel, our focus on preservation of financial stability continues. At this juncture, our overarching priority is that growth impulses are nurtured to ensure a durable recovery along a sustainable growth path with stability. In this endeavour, we have consciously chosen optimism over gloom, inspired by Mahatma Gandhi: “I am an irrepressible optimist, but I always base my optimism on solid facts”2.

Thank you. Stay safe. Stay well. Namaskar.

(Yogesh Dayal)

Chief General Manager

Press Release: 2021-2022/643

Notes:-

1 Source: Speeches delivered at Bishop Charles Mason Temple in Memphis, Tennessee (3 April 1968) and at Prayer Pilgrimage for Freedom (Call to Conscience, 1957) in Washington, D.C USA.

2 Source: Book “Mahatma” by D.G. Tendulkar, Volume 2.

Reserve Bank of India

Date : Aug 06, 2021

Monetary Policy Statement, 2021-22 Resolution of the Monetary Policy Committee (MPC) August 4-6, 2021

On the basis of an assessment of the current and evolving macroeconomic situation, the Monetary Policy Committee (MPC) at its meeting today (August 6, 2021) decided to:

- keep the policy repo rate under the liquidity adjustment facility (LAF) unchanged at 4.0 per cent.

Consequently, the reverse repo rate under the LAF remains unchanged at 3.35 per cent and the marginal standing facility (MSF) rate and the Bank Rate at 4.25 per cent.

- The MPC also decided to continue with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

These decisions are in consonance with the objective of achieving the medium-term target for consumer price index (CPI) inflation of 4 per cent within a band of +/- 2 per cent, while supporting growth.

The main considerations underlying the decision are set out in the statement below.

Assessment

Global Economy

2. Since the MPC’s meeting during June 2-4, 2021 the pace of global recovery appears to be moderating with the resurgence of infections in several parts of the world, especially from the delta variant of the virus. In June and July, global purchasing managers’ indices (PMIs) slipped from the highs scaled in May. The growing consensus is that the recovery is occurring on a diverging two-track mode. Countries that are ahead in vaccination and have been able to provide or maintain policy stimulus are rebounding strongly. Growth in other economies remains subdued and vulnerable to new waves of infections. There has been a slowing of momentum in global trade volumes in Q2:2021, with elevated shipping charges and logistics costs posing headwinds.

3. There has been a considerable hardening of commodity prices, particularly of crude oil. The latest agreement within the Organisation of Petroleum Countries (OPEC) plus to raise oil production for a likely restoration of output to the pre-pandemic levels by September 2022 imparted transient softening to spot and future crude prices from the recent peak in early July. Headline inflation has ratcheted up in several advanced economies (AEs) as well as most emerging market economies (EMEs), prompting a few central banks in EMEs to tighten monetary policy. In contrast, sovereign bond yields have softened across AEs as markets seem to have acquiesced to the views of central banks that inflation is largely transitory. In EMEs, bond yields remain relatively high on inflation concerns and country-specific factors. In the foreign exchange market, EME currencies have depreciated in the wake of portfolio outflows since mid-June as risk appetite ebbed, while the US dollar has strengthened.

Domestic Economy

4. On the domestic front, economic activity picked up pace in June-July as some states eased pandemic containment measures. As regards agriculture, the south-west monsoon regained intensity in mid-July after a lull; the cumulative rainfall up to August 1, 2021 was one per cent below the long-period average. The pace of sowing of kharif crops picked up in July along with some high frequency indicators of rural demand, notably tractor and fertiliser sales.

5. Reflecting large base effects, industrial production expanded in double digits year-on-year (y-o-y) in May 2021 on top of the massive jump in April, but it was still 13.9 per cent below its May 2019 level. The manufacturing purchasing managers’ index (PMI) that had dropped into contraction to 48.1 in June for the first time in 11 months, rebounded well into expansion zone with a reading of 55.3 in July. High-frequency indicators – e-way bills; toll collections; electricity generation; air traffic; railway freight traffic; port cargo; steel consumption, cement production; import of capital goods; passenger vehicle sales; two wheeler sales –posted strong growth in June/July, reflecting adaptations to COVID related protocols and easing of containment. Services PMI remained in contractionary zone due to COVID-19 related restrictions, though the pace eased to 45.4 in July from 41.2 in June 2021. Initial quarterly results of non-financial corporates for Q1:2021-22 show healthy growth in sales, wage growth and profitability led by information technology firms.

6. Headline CPI inflation plateaued at 6.3 per cent in June after having risen by 207 basis points in May 2021. Food inflation increased in June primarily due to an uptick in inflation in edible oils, pulses, eggs, milk and prepared meals and a pick-up in vegetable prices. Fuel inflation moved into double digits during May-June 2021 as inflation in LPG, kerosene, and firewood and chips surged. After rising sharply to 6.6 per cent in May, core inflation moderated to 6.1 per cent in June, driven by softening of inflation in housing, health, transport and communication, recreation and amusement, footwear, pan, tobacco and other intoxicants (as the effects of the one-off post-lockdown taxes imposed a year ago waned), and personal care and effects (due to sharp reduction in inflation in gold).

7. System liquidity remained ample, with average daily absorption under the LAF increasing from ₹5.7 lakh crore in June to ₹6.8 lakh crore in July and further to ₹8.5 lakh crore in August so far (up to August 4, 2021). Auctions for a cumulative amount of ₹40,000 crore in Q2:2021-22 so far under the secondary market government securities acquisition programme (G-SAP) evened liquidity across illiquid segments of the yield curve. Reserve money (adjusted for the first-round impact of the changes in the cash reserve ratio) expanded by 11.0 per cent y-o-y on July 30, 2021 driven by currency demand. As on July 16, 2021, money supply (M3) and bank credit by commercial banks grew by 10.8 per cent and 6.5 per cent, respectively. India’s foreign exchange reserves increased by US$ 43.1 billion in 2021-22 (up to end-July) to US$ 620.1 billion.

Outlook

8. Going forward, the revival of south-west monsoon and the pick-up in kharif sowing, buffered by adequate food stocks should help to control cereal price pressures. High frequency indicators suggest some softening of price pressures in edible oils and pulses in July in response to supply side interventions by the Government. Input prices are rising across manufacturing and services sectors, but weak demand and efforts towards cost cutting are tempering the pass-through to output prices. With crude oil prices at elevated levels, a calibrated reduction of the indirect tax component of pump prices by the Centre and states can help to substantially lessen cost pressures. Taking into consideration all these factors, CPI inflation is now projected at 5.7 per cent during 2021-22: 5.9 per cent in Q2; 5.3 per cent in Q3; and 5.8 per cent in Q4 of 2021-22, with risks broadly balanced. CPI inflation for Q1:2022-23 is projected at 5.1 per cent (Chart 1).

9. Domestic economic activity is starting to recover with the ebbing of the second wave. Looking ahead, agricultural production and rural demand are expected to remain resilient. Urban demand is likely to mend with a lag as manufacturing and non-contact intensive services resume on a stronger pace, and the release of pent-up demand acquires a durable character with an accelerated pace of vaccination. Buoyant exports, the expected pick-up in government expenditure, including capital expenditure, and the recent economic package announced by the Government will provide further impetus to aggregate demand. Although investment demand is still anaemic, improving capacity utilisation and congenial monetary and financial conditions are preparing the ground for a long-awaited revival. Firms polled in the Reserve Bank surveys expect expansion in production volumes and new orders in Q2:2021-22, which is likely to sustain through Q4. Elevated levels of global commodity prices and financial market volatility are, however, the main downside risks. Taking all these factors into consideration, projection for real GDP growth is retained at 9.5 per cent in 2021-22 consisting of 21.4 per cent in Q1; 7.3 per cent in Q2; 6.3 per cent in Q3; and 6.1 per cent in Q4 of 2021-22. Real GDP growth for Q1:2022-23 is projected at 17.2 per cent (Chart 2).

10. Inflationary pressures are being closely and continuously monitored. The MPC is conscious of its objective of anchoring inflation expectations. The outlook for aggregate demand is improving, but still weak and overcast by the pandemic. There is a large amount of slack in the economy, with output below its pre-pandemic level. The current assessment is that the inflationary pressures during Q1:2021-22 are largely driven by adverse supply shocks which are expected to be transitory. While the Government has taken certain steps to ease supply constraints, concerted efforts in this direction are necessary to restore supply-demand balance. The nascent and hesitant recovery needs to be nurtured through fiscal, monetary and sectoral policy levers. Accordingly, the MPC decided to keep the policy repo rate unchanged at 4 per cent and continue with an accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward.

11. All members of the MPC – Dr. Shashanka Bhide, Dr. Ashima Goyal, Prof. Jayanth R. Varma, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das – unanimously voted to keep the policy repo rate unchanged at 4.0 per cent.

12. All members, namely, Dr. Shashanka Bhide, Dr. Ashima Goyal, Dr. Mridul K. Saggar, Dr. Michael Debabrata Patra and Shri Shaktikanta Das, except Prof. Jayanth R. Varma, voted to continue with the accommodative stance as long as necessary to revive and sustain growth on a durable basis and continue to mitigate the impact of COVID-19 on the economy, while ensuring that inflation remains within the target going forward. Prof. Jayanth R. Varma expressed reservations on this part of the resolution.

13. The minutes of the MPC’s meeting will be published on August 20, 2021.

14. The next meeting of the MPC is scheduled during October 6 to 8, 2021.

(Yogesh Dayal)

Chief General Manager

Press Release: 2021-2022/644

Reserve Bank of India

Date : Aug 06, 2021

Statement on Developmental and Regulatory Policies

This Statement sets out various developmental measures including liquidity and regulatory measures.

I. Liquidity Measures

1. On Tap TLTRO Scheme – Extension of Deadline

With a view to increasing the focus of liquidity measures on revival of activity in specific sectors that have both backward and forward linkages and having multiplier effects on growth, the RBI had announced the On Tap TLTRO scheme on October 9, 2020 for five sectors which was available up to March 31, 2021. Stressed sectors identified by the Kamath Committee were also brought within the ambit of the scheme on December 4, 2020 and subsequently bank lending to NBFCs on February 5, 2021. On April 7, the scheme was extended by a period of six months, i.e., till September 30, 2021. Given the nascent and fragile economic recovery, it has now been decided to extend the On Tap TLTRO scheme further by a period of three months, i.e., till December 31, 2021.

2. Marginal Standing Facility (MSF) – Extension of Relaxation

On March 27, 2020 banks were allowed to avail of funds under the marginal standing facility (MSF) by dipping into the Statutory Liquidity Ratio (SLR) up to an additional one per cent of net demand and time liabilities (NDTL), i.e., cumulatively up to 3 per cent of NDTL. This facility, which was initially available up to June 30, 2020 was later extended in phases up to March 31, 2021 and again for a further period of six months till September 30, 2021, providing comfort to banks on their liquidity requirements and also to enable them to meet their Liquidity Coverage Ratio (LCR) requirements. This dispensation provides increased access to funds to the extent of ₹1.62 lakh crore and qualifies as high-quality liquid assets (HQLA) for the LCR. It has now been decided to continue with the MSF relaxation for a further period of three months, i.e., up to December 31, 2021.

II. Regulatory Measures

3. LIBOR Transition – Review of Guidelines

The London Interbank Offered Rate (LIBOR) transition is a significant event that poses challenges for banks and the financial system. RBI has issued an advisory on June 8, 2021 encouraging banks and other RBI regulated entities to cease entering into new contracts that use LIBOR as a reference rate and instead adopt any Alternative Reference Rate (ARR) as soon as practicable and in any event by December 31, 2021. The Reserve Bank has been engaging with banks and market bodies to proactively take steps, as necessary, to ensure a smooth transition for regulated entities and financial markets. In this context, it has been decided to amend the guidelines related to export credit in foreign currency and restructuring of derivative contracts as detailed below.

(i) Export Credit in Foreign Currency – Benchmark Rate

Authorized dealers are currently permitted to extend Pre-shipment Credit in Foreign Currency (PCFC) to exporters for financing the purchase, processing, manufacturing or packing of goods prior to shipment at LIBOR / EURO-LIBOR / EURIBOR related rates of interest. In view of the impending discontinuance of LIBOR as a benchmark rate, it has been decided to permit banks to extend export credit using any other widely accepted Alternative Reference Rate in the currency concerned.

(ii) Prudential Norms for Off-balance Sheet Exposures of Banks – Restructuring of Derivative Contracts

For derivative contracts, as per extant instructions, change in any of the parameters of the original contract is treated as a restructuring and the resultant change in the mark-to-market value of the contract on the date of restructuring is required to be cash settled. Since the impending change in reference rate from LIBOR is a “force majeure” event, banks are being advised that change in reference rate from LIBOR / LIBOR-related benchmarks to an Alternative Reference Rate will not be treated as restructuring.

4. Deferral of Deadline for Achievement of Financial Parameters under Resolution Framework 1.0

The resolution plans implemented under the Resolution Framework for COVID-19 related stress announced on August 6, 2020 are required to meet the sector specific thresholds notified in respect of five financial parameters, four of which are related to the operational performance of the borrowing entity, viz. Total Debt to EBIDTA ratio (Total Debt/EBIDTA), Current Ratio, Debt Service Coverage Ratio and Average Debt Service Coverage Ratio, by March 31, 2022. Recognising the adverse impact of second wave of COVID-19 on revival of businesses, and the difficulty it may pose in meeting the operational parameters, it has been decided to defer the target date for meeting the specified thresholds in respect of the above parameters to October 1, 2022.

As regards the parameter Total Outside Liabilities/Adjusted Total Net Worth (TOL/ATNW), this ratio reflects the revised capital structure (i.e., debt-equity mix) as required under the implementation conditions for the resolution framework and was expected to be crystallised upfront as part of the resolution plan. Accordingly, the date for achieving the same remains unchanged, i.e. March 31, 2022.

A circular to this effect, modifying the previous instructions dated September 7, 2020, will be issued shortly.

(Yogesh Dayal)

Chief General Manager

Press Release: 2021-2022/645