VALUATION OF SHARES FOR COMPANY REGISTERED UNDER STARTUP INDIA WITH MINISTRY OF COMMERCE & INDUSTRY: –

Valuation of equity shares is generally required for regulatory or financial reporting purposes for a business. In valuation of shares, the underlying asset is the business and per share value is calculated to arrive at the final valuation.

Page Contents

- Methods of Valuation to be followed by Registered Valuers for a Startup Valuation:

- Various Taxation Benefits for Companies/Entities registered under Start-up

- Valuation of Shares for fresh issue and transfer of shares as per Rule 11UA of Income Tax Rules 1962: –

- Valuation of Shares for fresh issue of shares

- Valuation of Shares for transfer of shares

Methods of Valuation to be followed by Registered Valuers for a Startup Valuation:

There are several commonly used and accepted methods for determining the fair value of the business of a company. They mainly fall under the following three categories and the application of any below mentioned methods of valuation depends on the nature of operations, level of maturity of the businesses, future business potential and purpose of valuation. For the purpose of arriving at the fair value of the Equity shares of the Company, it would be necessary to select an appropriate basis for valuation from among the various alternatives available.

A. Income based valuation approach (“Income Approach”): The Discounted Cash Flow (DCF) method under income approach is commonly used. It is accepted as an appropriate method by business appraisers. This approach constitutes estimation of the business value by calculating the present value of all the future cash flows which the company is expected to generate. As per Rule 11UA(2)(b) the fair market value of the unquoted equity shares shall be determined by a merchant banker or an accountant as per the Discounted Free Cash Flow method.

B. Net Asset Value based valuation approach (“Asset Approach”): The Asset Based Valuation Method is not an appropriate method of valuing a startup business, because it does not truly measure the earning capacity of an enterprise and its growth potential.

C. Market based valuation approach (“Market Approach”): The Market Based Valuation Method is also not an appropriate method since startups are not a listed company, they do not have a market price readily available for Valuing the Company. The Startups cannot be compared with listed comparable as well.

Various Taxation Benefits for Companies/Entities registered under Start-up

Section 56 of Income Tax Act, 1961: –

> As laid down under Section 56(2)(viib) provides for charging of the consideration received for issue of shares by certain companies, where such consideration exceeds the fair market value of such shares.

> These amendments will take effect from 1st April, 2020 and will, accordingly, apply in relation to the assessment year 2020-21 and subsequent assessment years.

> To apply for Income Tax Exemption on investments above fair market value received under Section 56 of Income Tax Act:

> A Startup shall be eligible for notification under clause (ii) of the proviso to clause (viib) of sub-section (2) of section 56 of the Act and consequent exemption from the provisions of that clause, if it fulfils the following conditions:

-

- it has been recognized by DPIIT under para 2(iii)(a) or as per any earlier notification on the subject

- aggregate amount of paid up share capital and share premium of the startup after issue or proposed issue of share, if any, does not exceed, twenty-five crore rupees.

Important Note: 1. While computing the aggregate amount of paid up share capital, it shall not be included:

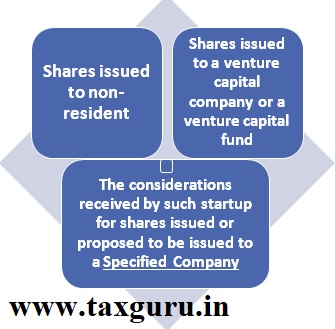

Meaning of specified Company: –

A Listed Company whose net worth on the last date of financial year in which shares are issued exceeds Rs. 100 crore or turnover for the financial year in which shares are issued exceeds Rs 250 Crores

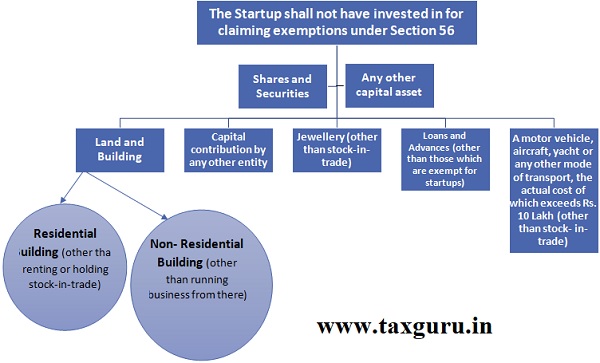

The startup has not invested in:

Section 80-IAC of Income Tax Act, 1961: –

A DIPP recognized Startup shall be eligible to apply to the Inter-Ministerial Board (IMB) for 100% deduction on the profits and gains from business for 3 years provided the following conditions are fulfilled:

> A private limited company or a limited liability partnership,

> Incorporated on or after 1st April 2016 but before 1st April 2021, and

> Start-up is engaged in innovation, development or improvement of products or processes or services or a scalable business model with a high potential of employment generation or wealth creation.

The startups holding a valid certificate from the Inter-Ministerial Board of Certificationare eligible for 100% tax deductions for 3 years provided the following conditions are fulfilled:

> Turnover shall not exceed Rs. 25 Crore in a year of deduction.

Note: 100% Deduction of income for three years out of ten years from the year of its incorporation is allowed.

| Particulars | Fresh Issue of Shares | Transfer of Shares |

| Method of Valuation | Either DCF or Intrinsic Value or any other method at the option of the Assessee | Intrinsic Value as defined in rules. |

| Relevant Section | Section 56(2)(viib) read with Rule 11UA(2) of Income Tax rules | Section 56(2)(x) read with Rule 11UA(1)(c) of Income Tax rules |

| Valuation report | Merchant Banker | Merchant Banker or Chartered Accountant |

As per Explanation to section 56(2)(viib), for issue of shares the Fair Market Value of shares shall be the value –

(i) as may be determined in accordance with such method as may be prescribed; or

(ii) as may be substantiated by the company to the satisfaction of the Assessing Officer, based on the value, on the date of issue of shares, of its assets, including intangible assets being goodwill, know-how, patents, copyrights, trademarks, licenses, franchises or any other business or commercial rights of similar nature,whichever is higher

As per sub-rule 2 of rule 11UA of Income Tax Rules 1962,Fair market value of unquoted equity shares for the purposes of sub-clause (i) of clause (a) of Explanation to clause (viib) of sub-section (2) of section 56 shall be the value, on the valuation date, of such unquoted equity shares as determined in the following manner under clause (a) or clause (b), at the option of the assessee, namely: —

(a) the fair market value of unquoted equity shares = (A–L) × (PV),

(PE)

where,

A= book value of the assets in the balance-sheet as reduced by any amount of tax paid as deduction or collection at source or as advance tax payment as reduced by the amount of tax claimed as refund under the Income-tax Act and any amount shown in the balance-sheet as asset including the unamortized amount of deferred expenditure which does not represent the value of any asset;

L=book value of liabilities shown in the balance-sheet, but not including the following amounts, namely:

(i) the paid-up capital in respect of equity shares;

(ii) the amount set apart for payment of dividends on preference shares and equity shares where such dividends have not been declared before the date of transfer at a general body meeting of the company;

(iii) reserves and surplus, by whatever name called, even if the resulting figure is negative, other than those set apart towards depreciation;

(iv) any amount representing provision for taxation, other than amount of tax paid as deduction or collection at source or as advance tax payment as reduced by the amount of tax claimed as refund under the Income-tax Act, to the extent of the excess over the tax payable with reference to the book profits in accordance with the law applicable thereto;

(v) any amount representing provisions made for meeting liabilities, other than ascertained liabilities;

(vi) any amount representing contingent liabilities other than arrears of dividends payable in respect of cumulative preference shares;

PE= total amount of paid up equity share capital as shown in the balance sheet;

PV= the paid up value of such equity shares; or

(b) the fair market value of the unquoted equity shares determined by a merchant banker as per the Discounted Free Cash Flow method.

As can be seen, at the option of the assesse, the assesse can opt for fair market value as per the Discounted Free Cash Flow method in case the company is willing to raise funding at higher value vis-à-vis book value of company.

As per Explanation to Section 56(2)(x), Fair Market Value shall have the same meaning as assigned in Explanation to clause (vii). Further, as per Explanation to clause (vii), “fair market value” of a property, other than an immovable property, means the value determined in accordance with the method as may be prescribed.

As per sub-rule 1 (c) of rule 11UA of Income Tax Rules 1962, the fair market value of unquoted equity shares shall be the value, on the valuation date, of such unquoted equity shares as determined in the following manner, namely: —

the fair market value of unquoted equity shares =(A+B+C+D – L)× (PV)/(PE), where,

A= book value of all the assets (other than jewellery, artistic work, shares, securities and immovable property) in the balance-sheet as reduced by, —

(i) any amount of income-tax paid, if any, less the amount of income-tax refund claimed, if any; and

(ii) any amount shown as asset including the unamortized amount of deferred expenditure which does not represent the value of any asset;

B = the price which the jewellery and artistic work would fetch if sold in the open market on the basis of the valuation report obtained from a registered valuer;

C = fair market value of shares and securities as determined in the manner provided in this rule;

D = the value adopted or assessed or assessable by any authority of the Government for the purpose of payment of stamp duty in respect of the immovable property;

L= book value of liabilities shown in the balance sheet, but not including the following amounts, namely:

(i) the paid-up capital in respect of equity shares;

(ii) the amount set apart for payment of dividends on preference shares and equity shares where such dividends have not been declared before the date of transfer at a general body meeting of the company;

(iii) reserves and surplus, by whatever name called, even if the resulting figure is negative, other than those set apart towards depreciation;

(iv) any amount representing provision for taxation, other than amount of income-tax paid, if any, less the amount of income-tax claimed as refund, if any, to the extent of the excess over the tax payable with reference to the book profits in accordance with the law applicable thereto;

(v) any amount representing provisions made for meeting liabilities, other than ascertained liabilities;

(vi) any amount representing contingent liabilities other than arrears of dividends payable in respect of cumulative preference shares;

PV= the paid up value of such equity shares;

PE = total amount of paid up equity share capital as shown in the balance sheet

As can be seen, the fair market value of shares for transfer of shares will be as per intrinsic value of shares.

To conclude, a company can use Discounted Free Cash Flow method for the purpose of Valuation of Fair market value of shares in case of fresh issue of shares and in case of transfer of shares a company can use intrinsic value for the purpose of Valuation of Fair market value of shares.

About the Author :

Author is Gourav Goyal, working as Director – Assurance with Neeraj Bhagat & Co. Chartered Accountants, a Chartered Accountancy firm helping foreign companies in setting up business in India and complying with various tax laws applicable to foreign companies while establishing their business in India. He is a member of the Institute of Chartered Accountants of India (ICAI) since 2012. He has been conducting Statutory & Tax audit, Internal audit of large & medium scale Limited Companies, carrying out Bank Audits and providing services in the field of accounts, Income Tax & Company Law matters.