Income Tax Department moving towards Digitalization (i.e from Traditional Assessment Model to Electronic Assessment Model)

E Assessment Scheme, 2019

Paradigm shift in E-Assessment:-

♦ Between 2016 and 2018, the Central Board of Direct Taxes (CBDT), which is the apex tax administrative body, progressively amended rules, notified various procedures and issued the required guidelines to increase the scope of E-proceedings.

♦ The CBDT also issued instructions that income-tax assessment proceedings to be framed in the year 2018-19 and 2019-20, shall be conducted through the E-proceeding facility.

♦ Exceptions: – Carved out for certain types of proceedings such as Search and Seizure cases, Re-assessments, Best-Judgment assessments, etc., where the assessment would be done through personal hearing process.

♦ CBDT also specified certain situations where taxpayer may be required to appear in person although the assessment is being carried out through e-proceedings.

♦ However, under this framework, the element of personal interaction with the tax department was always present as the entire tax assessment was carried out by the tax officer having jurisdiction over the taxpayer.

New E-Assessment Scheme, 2019:-

♦ Towards this objective, the Finance Act, 2019, amended the provisions of the Income Tax Act, 1961, (Act) to empower the government to notify a new tax assessment scheme, whereby the proceedings will be conducted entirely in an electronic mode.

♦ The finance minister while presenting the Union budget, 2019 also stated that the new scheme would be launched in a phased manner in the current financial year {F.Y 2019-20}.

♦ The new scheme was slated to bring in a paradigm shift in the way tax assessments were carried out in India by eliminating person-to-person contact to the extent it is technologically feasible, providing a fair and transparent framework of assessments, ensuring the tax assessments were technically sound and that consistent tax positions were taken.

The scheme lays down the procedure to carry out a faceless assessment through electronic mode:-

Contents:-

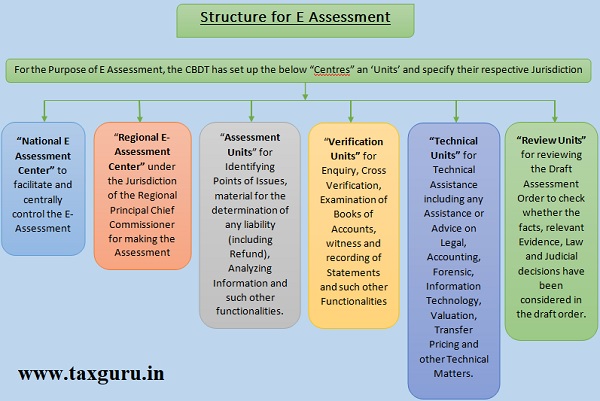

1. Structure for E Assessment

2. Procedure in E Assessment

3. Procedure for Penalty

4. Procedure for Appeal

5. Communication and Electronic Record

6. Appearance of Tax Payer between the Center and the Units

7. Power to Specify Process and Procedure

Structure:-

All the communications between all the units mentioned above, for the purpose of making an assessment under this scheme would be through the National e-Assessment Center.

Procedure for E Assessment:-

Procedure for E Assessment is as Follows:-

1. A notice under section 143(2) would be served by the National e-Assessment Center specifying the issues for selection of taxpayer’s case for assessment.

2. The taxpayer has a period of fifteen days for filing a response with the National e-Assessment Center.

3. The National E-Assessment Center will assign the case selected for the purposes of E-Assessment to a specific ‘assessment unit’ in any one ‘Regional e-Assessment Center’ through an automated allocation system.

4. Once a case is assigned to an assessment unit, it may make a request to the National E-Assessment Center for:

-

- Obtaining such further information, documents or evidence from the taxpayer or any other person, as it may specify.

- Conducting of certain enquiry or verification by verification unit; and

- Seeking technical assistance from the technical unit

5. Upon a request being made by the assessment unit for any documents or evidence, the National E-Assessment Center shall issue appropriate notice or requisition to the taxpayer or any other person for obtaining the information, documents or evidence requisitioned by the assessment unit.

6. Upon a request being made for certain enquiry or verification as above, the request shall be assigned by the National E-Assessment Center to a verification unit through an automated allocation system.

7. Upon a request being made seeking technical assistance as above, the request shall be assigned by the National E-Assessment Center to a technical unit in any one Regional E-Assessment Center’s through an automated allocation system.

8. The ‘assessment unit’ shall, after taking into account all the relevant material gathered as above, pass a draft assessment order either accepting the returned income of the taxpayer or modifying the returned income of the taxpayer, as the case may be, and send a copy of such order to the National E-Assessment Center.

9. The ‘assessment unit’ shall, while making draft assessment order, provide details of the penalty proceedings to be initiated therein, if any.

10. The National E-Assessment Center shall examine the draft assessment order in accordance with the risk management strategy specified by the CBDT, including by way of an automated examination tool, whereupon it may decide to:

-

- Finalize the assessment as per the draft assessment order and serve a copy of such order and notice for initiating penalty proceedings, if any, on the taxpayer, along with the demand notice, specifying the sum payable by, or refund of any amount due to the taxpayer on the basis of such assessment; or

- Provide an opportunity to the taxpayer, in case a modification is proposed, by serving a notice calling upon him to show cause as to why the assessment should not be completed as per the draft assessment order; or

- Assign the draft assessment order to a review unit in any one Regional e-Assessment Center, through an automated allocation system, for conducting review of such order.

11. The review unit shall conduct review of the draft assessment order, referred to it by the National E-Assessment Center, whereupon it may decide to:

-

- Concur with the draft assessment order and intimate the National e-Assessment Center about such concurrence; or

- Suggest such modification, as it may deem fit, to the draft assessment order and send its suggestions to the National e-Assessment Center.

12. The National E-Assessment Center shall, upon receiving concurrence of the review unit finalize the draft assessment order or provide an opportunity to the taxpayer in case a modification is proposed.

13. The National E-Assessment Center shall, upon receiving suggestions for modifications from the review unit, communicate the same to the assessment unit.

14. The assessment unit shall, after considering the modifications suggested by the review unit, send the final draft assessment order to the National E-Assessment Center.

15. The National E-assessment Center shall, upon receiving final draft assessment order, finalize the draft assessment order, or provide an opportunity to the taxpayer in case a modification is proposed, as the case may be.

16. The taxpayer may, in a case where notice is issued for making submissions against the draft assessment order, furnish his response to the National E-Assessment Center on or before the date and time specified in the notice.

17. The National E-Assessment Center shall:

-

- In a case where no response to the show-cause notice is received, finalize the assessment as per the draft assessment order; or

- In any other case, send the response received from the taxpayer to the assessment unit.

18. The assessment unit shall, after taking into account the response furnished by the taxpayer, make a revised draft assessment order and send it to the National E-Assessment Center.

19. The National E-Assessment Center shall, upon receiving the revised draft assessment order:

-

- In case no modification against the interest of the taxpayer is proposed with reference to the draft assessment order, finalize the draft assessment; or

- In case a modification against the interest of the assesse is proposed with reference to the draft assessment order, provide an opportunity to the taxpayer for hearing and making submissions.

20. The response furnished by the taxpayer shall be dealt with by the National E-Assessment center and the draft assessment order finalized.

21. The National E-Assessment Center shall, after completion of assessment, transfer all the electronic records of the case to the Assessing Officer having jurisdiction over such case for:

-

- Imposition of penalty;

- Collection and recovery of demand;

- Rectification of mistake;

- Giving effect to appellate orders;

- Submission of remand report, or any other report to be furnished, or any representation to be made, or any record to be produced before the Commissioner (Appeals), Appellate Tribunal or Courts, as the case may be;

- Proposal seeking sanction for launch of prosecution and filing of complaint before the Court.

22. The National E-Assessment Center may at any stage of the assessment, if it considers necessary, transfer the case to the Assessing Officer having jurisdiction over such case.

Procedure for Penalty:-

1. Any unit may, in the course of assessment proceedings, for non-compliance of any notice, direction or order issued under this scheme on the part of the taxpayer or any other person, send recommendation for initiation of any penalty proceedings under the income tax law, against such taxpayer or any other person, as the case may be, to the National E-Assessment Center, if it considers necessary or expedient to do so.

2. The National E-Assessment Center shall, on receipt of such recommendation, serve a notice on the taxpayer or any other person, as the case may be, calling upon him to show cause as to why penalty should not be imposed on him under the income tax law.

3. The response to show cause notice furnished by the taxpayer or any other person, if any, shall be sent by the National E-Assessment Center to the concerned unit which has made the recommendation for penalty.

4. The said unit shall, after taking into consideration the response furnished by the taxpayer or any other person, as the case may be:

-

- Make a draft order of penalty and send a copy of such draft to National E-Assessment Center; or

- Drop the penalty after recording reasons, under intimation to the National E-Assessment Center

5. The National E-Assessment Center shall levy the penalty as per the said draft order of penalty and serve a copy of the same on the taxpayer or any other person, as the case may be.

Procedure for Appeal:-

An appeal against an assessment order made by the National E-Assessment Center under this scheme can be filed before the Commissioner (Appeals) having jurisdiction over the jurisdictional Assessing Officer.

Communication and electronic record:-

1. All communications between the National E-Assessment Center and the taxpayer, or his authorized representative, shall be exchanged exclusively by electronic mode; and

2. All internal communications between the National E-Assessment Center, Regional E-Assessment Center’s and various units shall be exchanged exclusively by electronic mode.

All the electronic records issued under the scheme shall be authenticated by the originator by affixing his digital signature.

Every notice or order or any other electronic communication under this scheme shall be delivered to the taxpayer, by way of:

- Placing an Authenticated copy of the communication in the Tax Payer’s registered account.

- Sending an Authenticated copy thereof to the registered Email.

- Uploading an Authenticated copy on the Assesses Mobile app and followed by a real time alert to the Tax Payer.

The taxpayer shall file his response to any notice or order or any other electronic communication, under this scheme, through his registered account and once an acknowledgement is sent by the National E-Assessment Center containing the hash result generated upon successful submission of response, the response shall be deemed to be authenticated.

Appearance of taxpayer before the Center and Units:-

1. A person is not required to appear either personally or through authorized representative in connection with any proceedings under this scheme before the income tax authority at the National E-Assessment Center or Regional E-Assessment Center or any unit set up under this scheme.

2. In a case where a modification is proposed in the draft assessment order, the taxpayer will be given an opportunity to make submissions against such modifications. The taxpayer or his authorized representative is also entitled to a personal hearing before income tax authority in any unit under this scheme. Such hearing would be conducted exclusively through video conferencing, including through video telephony, in accordance with the procedure laid down by the CBDT.

3. An income tax authority has the power to examine a taxpayer or record the statement of any taxpayer under this scheme.

Power to specify Process and Procedure:-

1. The Principal Chief Commissioner or the Principal Director General, in charge of the National E-Assessment Center shall lay down the standards, procedures and processes for effective functioning of the National E-Assessment Center, Regional e-Assessment Center’s and the Units set-up under this scheme.

2. The systems shall function in an automated and mechanized environment, including format, mode, procedure and processes in respect of the following, namely:-

-

- Service of the notice, order or any other communication;

- Receipt of any information or documents from the person in response to the notice, order or any other communication;

- Issue of acknowledgement of the response furnished by the person;

- Provision of ‘E-Proceeding’ facility including login account facility, tracking status of assessment, display of relevant details, and facility of download;

- Accessing, verification and authentication of information and response including documents submitted during the assessment proceedings;

- Receipt, storage and retrieval of information or documents in a centralized manner;

- General administration and grievance redressal mechanism in the respective Center’s and units.

Author Bio