This is premium content. Please become a Premium member. If you are already a member, login here to access the full content.

TDS can be recovered only if dept shows that recipient of income has not paid due taxes thereof

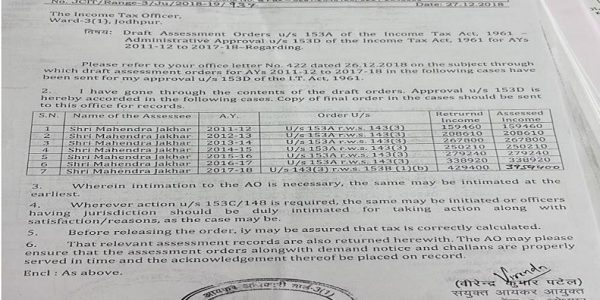

Case Law Details

- Case Name

- Allahabad Bank Vs Income Tax Officer (ITAT Agra)

- Appeal Number

- Only available for paid members

- Date of Judgement/Order

- Only available for paid members

- Related Assessment Year

- 2001- 02

Upgrade to Basic or Premium to download.

Already Upgraded? Log in.

Lapse on account of non-deduction of tax at source is to be visited with three different consequences – penal provisions, interest provisions and recovery provisions. The penal provisions in respect of such a lapse are set out in Section 271 C. So far as penal provisions are concerned, the penalty is for lapse on the part of the assessee and it has nothing to do with whether or not the taxes were ultimately recovered through other means. The provisions regarding interest in delay in depositing the taxes are set out in Section 201(1A). These provisions provide that for any delay in recovery o...

The article is very relavent as the banks or the authority to deduct TDS may fail to deduct TDS and credit to IT dept.,. Blindly penalising them is un-scientific. It may so happen the assessee having come to know his income is indeed taxable may pay it to the IT dept as advance tax or SAtax. This serves the purpose of collecting the tax. It is a historic juegement and clips the wings of the IT Dept if they prefer to blindly penalise the TDS deductor for the default.