“Understand the tax implications of winnings from online games with the introduction of Sections 115BBJ and 194BA, mandating a 30% tax rate on net winnings and TDS deductions, effective from 01.07.2023, ensuring compliance with income tax laws.”

Nowadays entertainment and earning can go hand in hand with the increasing ways to earn online by playing online games or gambling. The ease of access to cheap mobile networks and smartphones has lured many people to play these online games. Due to the minimum capital requirement and the popularity of these gaming platforms, the number of online users has increased manifold.

These winnings are a source of income, which was earlier liable to tax under section 194B which generally covered all the winnings from any lottery or crossword puzzle, card game and other game of any sort for an amount exceeding Rs. 10,000. Therefore no tax was liable to be deducted if the earnings from online games/ gambling does not exceed Rs. 10,000. This provision gave a window of income escapement, as the limit of Rs. 10,000 was used by the online platforms to split the winning into chucks of amounts below Rs. 10,000 and thus avoid taxes. The latest budget 2023 has got a few new provisions to curb this escapement and bring these online winnings into the purview of Income Tax.

In the budget, it was proposed to insert 2 new sections in this regard, Section 115BBJ “Tax on winnings from Online games” and Section 194BA “TDS on winnings from Online games”. Section 115BBJ describes the taxability of the net amount received from the online winnings at a special rate of 30%. Basic exemption limit shall not be considered while computing the total income and the tax payable for winnings from online games. Similarly, no chapter VI – A deduction such as 80C, 80D etc., shall not be allowed and no expenses can be claimed against these incomes.

The following definitions are important to understand and determine the taxability of this section,

Definitions

A) Computer Resource means computer, computer system, computer network, data, computer database or software;

B) Internet means the combination of computer facilities and electromagnetic transmission media, and related equipment and software, comprising the interconnected worldwide network of computer networks that transmits information based on a protocol for controlling such transmission;

C) Online game means a game that is offered on the internet and is accessible by a user through a computer resource including any telecommunication device;

D) Online gaming intermediary means an intermediary that offers one or more online games;

E) User means any person who accesses or avails any computer resource of an online gaming intermediary;

F) User account means account of a user registered with an online gaming intermediary;

Section 194BA of Income Tax Act, 1961

1. The section is applicable with effect from 01.07.2023.

2. Winnings from online games are chargeable to tax under head income from other sources.

3. There is no limit upto which winnings from online game is not taxable, earlier there was a limit of Rs. 10,000/- winnings below which were not subject to TDS.

4. Where there is a winning from any online games during the financial year the person responsible for paying the winning to the person shall be responsible to deduct TDS @ 31.20% (30% of basic tax as per the Section 115BBJ plus 4% of education Cess and surcharge wherever applicable at the rates prescribed), on the net winnings lying in his user account at the end of that financial year.

5. Where the user withdraws amount from his user account during the financial year,

a. then TDS shall be deducted @ 31.20% on the net winnings in the user account, as per Section 115BBJ at the time of withdrawal.

b. For the unwithdrawn portion, TDS is deducted @ 31.20% on the net winnings remaining in the user account at the end of the financial year.

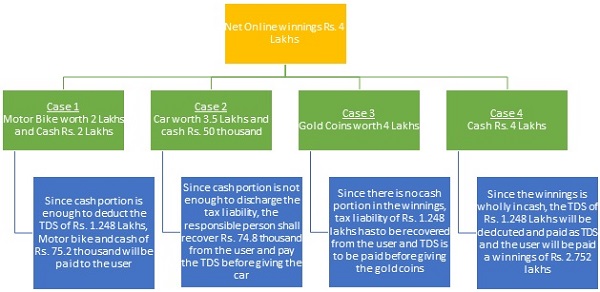

6. When the net winnings are wholly in kind or partly in cash, but the cash portion is not sufficient to deduct the TDS liability, the person responsible for paying shall ensure that the tax has been paid in respect of net winnings before releasing the winnings.

Example: Suppose the net winnings from online game amounts to Rs. 4,00,000/-and TDS liability is Rs. 1,24,800 (i.e., 31.20% of 4 Lakhs), consider the following individual cases illustrated below;

Due date for depositing the TDS under section 194BA

| Month in which winnings is credited | Due date for depositing TDS |

| April to February | 7th date of the subsequent month |

| March | On or before 30th April |

The payer on deducting and depositing the TDS shall file a quarterly return in form 26Q and issue Form 16A to the user for whom the tax deduction has been made.

Responsibilities of Gamers

1. The gamers are responsible for providing their PAN numbers to the online gaming intermediaries for deduction of TDS.

2. They must file their Income tax return within the due dates prescribed by disclosing their online winnings for which tax has been deducted U/s 194BA.

Author Bio