What is section 192?

Section 192 provides that any person responsible for paying any income chargeable under the head salaries is required to deduct tax on the amount payable.

Download Format of Form 16 in Word Format

Who deduct TDS?

A payment can be categorised as ‘salary’ only if it arises out of ‘employer-employee’ relationship. It must be ‘contract of service’ nor ‘contract for service’.

- It may be noted that pension is also ‘salary’ & though it is received from the employer pensioners are also covered u/s 192.

- Family pensioners are not covered under this section.

- Hospital apart from the regular employees, engaged in consultation of doctors and paid salary will be fall under ‘fees for professional services’.

When tax is to be deducted?

- Tax is to be deducted at the time of payment of salary i.e. Tax is to be deducted at the time of actual payment of the salary.

Conditions to be satisfied for application of section 192

- Any payment is made by an employer to his employee.

- Such payment must be chargeable under the head ‘Salaries’.

- If such payments exceeds the threshold limit in that financial year.

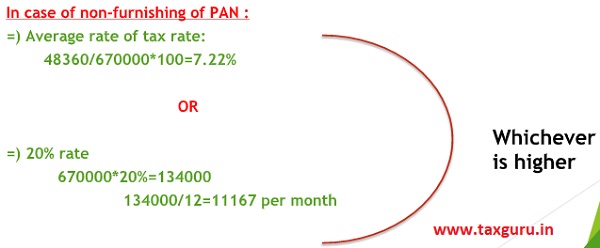

Effects of non-furnishing of PAN on rate of tax

- Every person whose receipts are subject to deduction of tax at source shall furnish the PAN to the deductor. If the person does not furnish the deductor will deduct tax at higher rates in the following rates:-

1. At the rate prescribed in the Act

2. At the rate in force or

3. At the rate of 20%

- No tax or lower tax is to be deducted when the assessing officer has issued the lower deduction certificate.

| Se ction | Nature of payment | Rate | Additional points |

| 192 | Salary | Slab rate |

|

- Section 192 does not specify a TDS rate. TDS will deducted as per the income tax slab and rates thereof applicable to the relevant financial year for which the salary is paid.

- TDS is to be deducted from the starting of the F.Y.(Eg. 1).

Salary from more than one employer

- If the employee is engaged with two or more employers simultaneously, employee can provide details about your salary and TDS in Form 12B to anyone of the employers. Once, the employer receives all kinds of information from employee he will be responsible in computing your gross salary to deduct TDS.

- Subsequently, if employee resign and join a different employer, employee can provide details of the previous employment in Form 12B to the new employer & will deduct TDS accordingly on gross salary for the remaining month.

Standard Deduction

- Every employee is eligible to get the standard deduction of Rs. 50000/-.

Allowances

- The standard deduction is replaced by transport allowance & medical reimbursement.

- A salaried individual having a rented accommodation can get the benefit of HRA. This could be totally or partially exempted from income tax. However, if you aren’t living in any rented accommodation and still continue to receive HRA, it will be taxable.

Example 1

| Estimated Gross salary | 750000 |

| Less:standard deduction | 50000 |

| Net salary income | 700000 |

| Loss of house property | 30000 |

| Gross total income | 670000 |

| Less:Deductions (if any) | – |

| Net income | 670000 |

| Tax on above | 48360 |

TDS deducted per month 48360/12=4030.

Read Below post for –

Tax Rate Option exercise by Employee for TDS on Salary & by Business