Introduction:

An assessee’s tax incidence is determined by his residential status. For example, an individual’s residential status in India determines whether income earned outside of India is taxable in India. Similarly, a foreign national’s residential status—rather than his citizenship—determines whether or not his income earned in India (or outside of India) is taxable in India. Therefore, determining a person’s residence status is crucial to determining his or her tax liability.

The Income Tax Act of 1961 governs the taxation system in India, outlining the rules for determining an individual’s residential status and its impact on tax incidence. Residential status plays a crucial role in assessing a person’s tax liability, as it determines the extent to which their income is taxed in India.

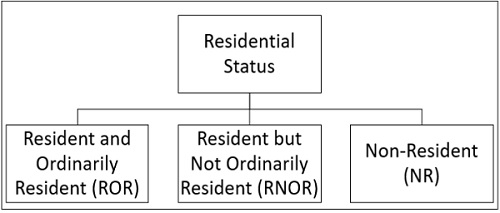

Under the Act, individuals are classified into three categories based on their stay in India during a financial year:

1. Resident and Ordinarily Resident (ROR)

2. Resident but Not Ordinarily Resident (RNOR)

3. Non-Resident (NR)

The scope of taxation varies based on these classifications. This classification affects not just individual taxpayers but also companies, Hindu Undivided Families (HUFs), and other entities. Understanding residential status and its effect on tax incidence is essential for tax planning, compliance, and avoiding legal issues under the Income Tax Act.

Key Norms for Determining Residential Status Under the Income Tax Act, 1961:

When determining the residential status of an assessee for tax purposes, the following key principles must be considered:

1. Classification of Taxable Entities:

For assessing residential status, taxable entities are broadly categorized into the following groups:

1. Individuals

2. Hindu Undivided Families (HUFs)

3. Firms and Associations of Persons (AOPs)

4. Joint Stock Companies

5. Other Legal Entities

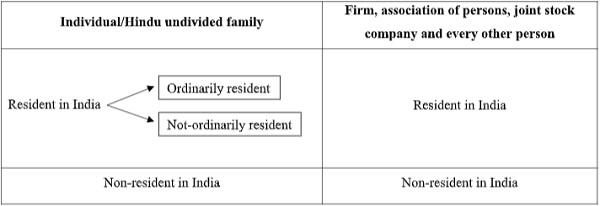

2. Categories of Residential Status:

An assessee can either be classified as:

1. Resident in India

2. Non-Resident in India

However, for individuals and Hindu Undivided Families (HUFs), further classification applies:

- Resident and Ordinarily Resident (ROR)

- Resident but Not Ordinarily Resident (RNOR)

- Non-Resident (NR)

For other entities like firms, AOPs, joint-stock companies, and other persons, the classification is simpler:

1. Resident in India

2. Non-Resident in India

3. Residential Status Is Assessed for Each Financial Year:

The residential status of an individual or entity must be evaluated for each financial year (previous year) separately. It may change depending on the person’s stay in India and other applicable conditions.

4. Consistency in Residential Status for the Same Assessment Year:

Once an individual is categorized as a resident in a financial year for any particular source of income, they will be considered a resident for all other sources of income in the same financial year [Section 6(5)]. It is not possible to have a different residential status for different sources of income within the same assessment year.

5. Variation in Residential Status Across Different Assessment Years:

An assessee’s residential status can change from one assessment year to another. For instance, an individual who has been classified as a Resident and Ordinarily Resident (ROR) in previous years may become a Non-Resident (NR) in a particular assessment year if they do not fulfil the conditions mentioned under Section 6(1) for that specific year.

6. Dual Residency: Resident in India and Another Country:

It is possible for a person to be classified as a resident in India while simultaneously holding residency status in another country. The Income Tax Act does not mandate that a person categorized as a resident in India must automatically be a non-resident in all other countries for the same assessment year. This situation is particularly relevant in cases where Double Taxation Avoidance Agreements (DTAA) apply, allowing individuals to manage their tax liabilities across multiple jurisdictions.

Determining the Residential Status of an Individual under Section 6 of the Income Tax Act, 1961:

Understanding an individual’s residential status is crucial for determining their tax liability in India. The Income Tax Act, 1961, lays down specific criteria under Section 6 to classify an individual as a Resident or Non-Resident for a given financial year. This classification directly impacts the scope of taxable income.

1. Categories of Residential Status: An individual can be classified into three categories:

A. Resident and Ordinarily Resident (ROR)

B. Resident but Not Ordinarily Resident (RNOR)

C. Non-Resident (NR)

Each category has distinct tax implications, making it essential to determine the correct status annually.

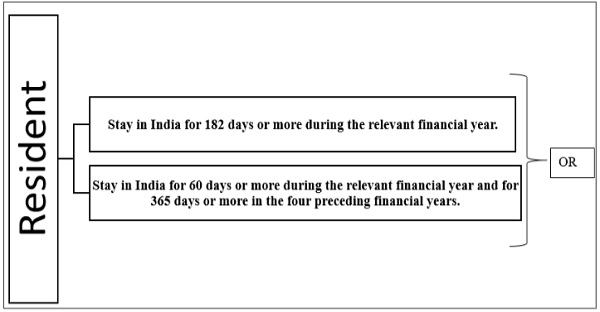

2. Determining Resident Status (Basic Conditions under Section 6(1)):

An individual is considered a Resident in India for a financial year if they satisfy any one of the following conditions:

Stay in India for 182 days or more during the relevant financial year.

OR

Stay in India for 60 days or more during the relevant financial year and for 365 days or more in the four preceding financial years.

Exceptions to the 60-day Rule:

- For Indian citizens leaving India for employment abroad or as a crew member of an Indian ship: The 182-day condition applies (the 60-day condition is ignored).

- For Indian citizens or Persons of Indian Origin (PIOs) visiting India:

A. If total Indian income exceeds ₹15 lakhs, the 60-day rule is extended to 120 days.

B. If Indian income is ₹15 lakh or less, the 182-day condition applies exclusively.

If neither of the above conditions is met, the individual is classified as a Non-Resident (NR).

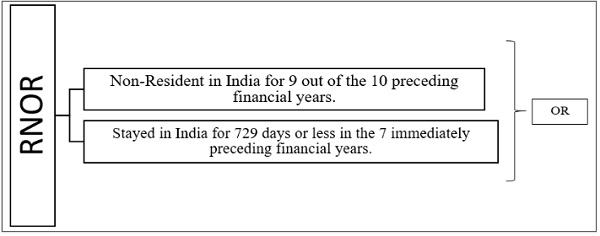

3. Classification as RNOR or ROR (Additional Conditions under Section 6(6)):

If an individual qualifies as a Resident, they must be further categorized as either:

A. Resident and Ordinarily Resident (ROR)

B. Resident but Not Ordinarily Resident (RNOR)

A Resident individual is classified as RNOR if they satisfy any one of the following conditions:

Non-Resident in India for 9 out of the 10 preceding financial years.

OR

Stayed in India for 729 days or less in the 7 immediately preceding financial years.

If neither of these conditions is met, the individual is classified as a Resident and Ordinarily Resident (ROR).

4. Key Amendments Introduced by the Finance Act, 2020:

Recent changes have impacted deemed residency rules:

- Indian citizens with total Indian income exceeding ₹15 lakhs who are not liable to tax in any other country will be deemed residents of India.

This amendment ensures that high-net-worth individuals cannot claim non-resident status solely for tax avoidance purposes.

5.Practical Examples for Better Understanding:

Example 1: Indian Employee Working Abroad

- Ajay, an Indian citizen, moves to the US for employment on July 1, 2023, and does not return to India until March 2025.

- In FY 2023-24, his stay in India is less than 182 days.

- Ajay is classified as a Non-Resident (NR) for FY 2023-24.

Example 2: Indian Citizen Visiting India

Priya, a US citizen of Indian origin, visits India for 150 days in FY 2023-24 and had stayed 400 days in the past four years.

- Her Indian income is ₹20 lakh.

- Since her Indian income exceeds ₹15 lakh, the 120-day rule applies..

- Since she stayed more than 120 days and 365 days in the past 4 years, she is a Resident.

- However, since she was a Non-Resident for 9 out of 10 previous years, she qualifies as an RNOR.

Example 3: Business Owner Frequently Traveling

- Ramesh, an Indian businessman, spends 250 days in India every year but was living abroad for 10 years before returning in FY 2023-24.

- He qualifies as a Resident but, since he was a Non-Resident for 9 out of 10 previous years, he will be RNOR.

- Once he spends more than 729 days in India over 7 years, he will become ROR.

Residential Status of Different Entities under Section 6 of the Income Tax Act, 1961:

Determining the residential status of taxable entities such as Hindu Undivided Families (HUFs), Firms, Associations of Persons (AOPs), Joint Stock Companies, and other entities is essential for taxation under the Income Tax Act, 1961. Section 6 of the Act provides clear rules for determining whether an entity is a resident or non-resident for taxation purposes.

1. Residential Status of Hindu Undivided Family (HUF):

The residential status of an HUF depends on the control and management of its affairs:

A. Resident HUF: If the control and management of the HUF is wholly or partly in India during the financial year, it is considered resident.

B. Non-Resident HUF: If the control and management is wholly outside India, it is considered non-resident.

Further Classification of Resident HUF:

A resident HUF is further classified as either:

A. Resident and Ordinarily Resident (ROR): If the Karta (head of the family) meets the conditions applicable to individuals for ROR status.

B. Resident but Not Ordinarily Resident (RNOR): If the Karta meets the RNOR conditions for individuals.

Example:

If an HUF has business activities in India but its decisions are made outside India, it will be considered a non-resident.

2. Residential Status of Firms and Associations of Persons (AOPs):

For Firms and AOPs, the residential status is determined by the location of their control and management:

A. Resident: If the control and management of affairs is wholly or partly in India, the entity is resident.

B. Non-Resident: If the control and management is wholly outside India, it is non-resident.

Example:

If an Indian firm has its key business decisions made entirely outside India, it will be non-resident. However, if some decisions are made in India, it will be a resident firm.

3. Residential Status of Joint Stock Companies:

A company’s residential status depends on the Place of Effective Management (POEM), introduced under the Finance Act, 2016.

A. Resident Company:

- An Indian company (incorporated in India) is always a resident.

- A foreign company is treated as a resident if its Place of Effective Management (POEM) is in India during the relevant financial year.

B. Non-Resident Company: If the POEM is outside India, it is non-resident.

Understanding POEM:

POEM refers to the location where key managerial and commercial decisions necessary for the conduct of business are made in substance.

Example:

A company registered in India but making major decisions in the USA is still a resident company.

A foreign company with effective control in India will be deemed resident in India for tax purposes.

4. Residential Status of Every Other Person (Other Entities):

Entities not covered in the above categories (e.g., trusts, societies, LLPs) follow similar principles:

A. If control and management is wholly or partly in India, it is

B. If control and management is entirely outside India, it is non-resident.

Example:

A trust registered in India but managed by a board outside India will be a non-resident.

5. Recent Amendments and Key Takeaways:

a. Introduction of POEM for Companies (Finance Act, 2016)

Foreign companies with effective control in India are now taxed as residents.

Designed to prevent tax avoidance by shell companies.

b. Stricter Rules for HUF and AOPs

If decision-making happens mostly in India, the entity may still be considered resident, even if some members are abroad.

c. Increased Scrutiny on NRIs with Business Interests in India

Double Taxation Avoidance Agreements (DTAA) help in avoiding double taxation for non-resident entities.

Tax Incidence Under the Income Tax Act, 1961:

The concept of tax incidence refers to the entity or individual on whom the final burden of tax falls. Under the Income Tax Act, 1961, tax incidence depends on the residential status of the taxpayer and the source of income. Understanding tax incidence is crucial for determining whether an individual or entity is liable to pay tax in India on their global income or only on income earned within India.

1. Factors Determining Tax Incidence: The tax liability of a person depends on the following factors:

- The residential status of the taxpayer (Resident, Non-Resident, or Resident but Not Ordinarily Resident).

- The location of income generation (whether the income is earned in India or abroad).

- The nature of income (salary, capital gains, business profits, etc.).

2. Tax Incidence Based on Residential Status: The scope of taxable income is classified as follows:

| Residential Status | Income Earned in India | Income Received in India | Foreign Income |

| Resident and Ordinarily Resident (ROR) | Taxable | Taxable | Taxable |

| Resident but Not Ordinarily Resident (RNOR) | Taxable | Taxable | Not Taxable (Except if derived from India) |

| Non-Resident (NR) | Taxable | Taxable | Not Taxable |

Thus, residents are taxed on their global income, while non-residents are only taxed on Indian income.

3. Types of Income and Their Tax Treatment:

A. Income Accruing or Arising in India-

Any income generated within India is taxable for all taxpayers, including non-residents.

Examples: Salary for work performed in India, rent from property in India, business income from operations in India.

B. Income Received in India-

If income is received in India, it is taxable, irrespective of where it was earned.

Example: A non-resident receiving dividends from an Indian company.

C. Income Deemed to Accrue or Arise in India-

Under Section 9, certain incomes are deemed to accrue or arise in India even if earned outside the country:

Income from a business connection in India

Salaries paid by the Government of India to Indian citizens abroad

Capital gains from the transfer of assets situated in India

D. Foreign Income-

Residents (ROR): Taxable on their global income.

RNOR and NR: Foreign income is not taxable unless linked to India.

4. Tax Incidence on Different Entities

| Taxpayer | Resident | Non-Resident |

| Individuals | Taxed on global income | Taxed only on Indian income |

| HUFs, Firms, AOPs | Taxed on global income | Taxed only on Indian income |

| Companies | Indian companies taxed on global income; foreign companies taxed on Indian income | Foreign companies taxed only on income from India |

| Trusts, LLPs | Taxed on income earned in or received in India | Taxed only on Indian income |

5. Special Provisions Affecting Tax Incidence:

A/. Place of Effective Management (POEM) for Companies

If a foreign company’s effective management is in India, it will be taxed as a resident company.

Introduced to prevent tax evasion by companies claiming non-resident status.

B. Double Taxation Avoidance Agreements (DTAA)

Non-residents can avoid being taxed twice on the same income by availing benefits under DTAA agreements between India and other countries.

C. Deemed Residency (Finance Act, 2020)

Indian citizens earning more than ₹15 lakhs in India but not paying taxes in any country are deemed residents of India. Prevents individuals from claiming non-resident status solely to avoid taxation.

Conclusion:

The residential status of an individual or entity under the Income Tax Act, 1961, plays a crucial role in determining the extent of tax liability in India. It defines whether a taxpayer is required to pay tax only on income earned in India or on their global income.

Residents and Ordinarily Residents (ROR) are taxed on their worldwide income, making it essential for them to plan their finances carefully.

Resident but Not Ordinarily Residents (RNOR) enjoy a partial exemption, with only Indian income and foreign income linked to India being taxable.

Non-Residents (NR) are liable to pay tax only on income earned or received in India, reducing their tax burden significantly.

For businesses and other entities, factors such as the Place of Effective Management (POEM) and control and management location impact their residential status and, consequently, their tax obligations.

With recent amendments tightening tax laws—such as deemed residency for high-income NRIs and POEM rules for foreign companies—it has become more important than ever for individuals and businesses to assess their residential status accurately. Strategic tax planning, compliance with DTAA provisions, and understanding the scope of taxable income can help optimize tax liabilities and prevent any legal complications.

In conclusion, residential status is the foundation of tax incidence and must be carefully evaluated to ensure compliance while maximizing tax efficiency.

REFERANCES:

- ClearTax, https://cleartax.in/s/residential-status#h11, last viewed on 22nd February,2025.

- Taxxman,https://cdn.taxmann.com/BookshopFiles/bookfiles/9789357788649_sampleNewa0956cf78e4b.pdf, last viewed on 22nd February,2025

- Testbook, https://testbook.com/ugc-net-commerce/residential-status-and-incidence-of-tax, last viewed on 22nd February,2025.

- Groww, https://groww.in/p/tax/residential-status-under-income-tax-act, last viewed on 22nd February,2025.

- EGyankosh, https://egyankosh.ac.in/bitstream/123456789/66970/3/Unit-3.pdf,last viewed on 22nd February,2025.

- DR JYOTSNA I PATEL P, “Residential Status and Tax Incidence Under The Income Tax Act, FEMA and Companies Act”, 4 INTERNATIONAL JOURNAL OF SCIENTIFIC RESEARCH 3(2015)

*****

Author: Krithika Mittal is 4th year student of BBA. LLB (Hons.), Lovely Professional University, Punjab.