Introduction

The implementation of the Finance Act 2021 brought significant changes to the procedures governing income tax assessments in India. One of the crucial aspects of these changes was the introduction of Section 144B, Section 151A, and Section 130, with the primary goal of facilitating faceless assessments for greater efficiency, transparency, and accountability.

This article delves into the question of whether the proceedings conducted under Section 148A(b) and Section 148A(d) after the Finance Act 2021 by local jurisdictional Assessing Officers are legally valid. We will examine the relevant legal provisions, government schemes, and recent court judgments to provide a comprehensive analysis.

Legal Framework Post-Finance Act 2021

Sec-144B, as inserted by Finance Act, 2021, wef 01.04.2021-Starts with non-obstante clause; read as under:

“Notwithstanding anything to the contrary contained in any other provision of this Act, the assessment, reassessment or recomputation under sub-section (3) of section 143 of under section 144 or under section 147 as the case may be with respect to the cases referred to in sub-section (2), shall be made in a faceless manner as per the following procedure, namely:-

(i) the National Faceless Assessment Centre shall assign the case selected for the purposes of faceless assessment under this section to a specific assessment unit through an automated allocation system;

(ii) the National Faceless Assessment Centre shall intimate the assessee that assessment in his case shall be completed in accordance with the procedure laid down under this section;

(iii) a notice shall be served on the assessee, through the National Faceless Assessment Centre, under sub-section (2) of section 143 or under sub-section (1) of section 142 and the assessee may file his response to such notice within the date specified therein, to the National Faceless Assessment Centre which shall forward the same to the assessment unit”;

Faceless Assessment Procedures

Another Relevant Sec 151A(1), which refers to faceless assessment of income escaping assessment; read as

”The Central Government may make a scheme, by notification in the Official Gazette, for the purposes of assessment, reassessment or re-computation under section 147 or issuance of notice under section 148 for conducting of enquiries or issuance of show-cause notice or passing of order under section 148A1 or sanction for issue of such notice under section 151, so as to import greater efficiency, transparency and accountability by

(a) eliminating the interface between the income-tax authority and the assessee or any other person to the extent technologically feasible;

(b) optimising utilisation of the resources through economies of scale and functional specialisation;

(c) introducing a team-based assessment, reassessment, re-computation or issuance or sanction of notice with dynamic jurisdiction’s.

SIMILARLY, Sec 130(1) conferring jurisdiction of Income Tax Authorities, in the light of Faceless Assessment procedures being adopted, read as:

The Central Government may make a scheme, by notification in the Official Gazette, for the purpose of

(a) exercise of all or any of the powers and performance of all or any of the functions conferred on, or, as the case may be, assigned to income-tax authorities by or under this Act as referred to in section 120; or

(b) vesting the jurisdiction with the Assessing Officer as referred to in section 124; or

(c) exercise of power to transfer cases under section 127; or

(d) exercise of jurisdiction in case of change of incumbency as referred to in section 129,

so as to impart greater efficiency, transparency and accountability by

(i) eliminating the interface between the income-tax authority and the assessee or any other person, to the extent technologically feasible;

(ii) optimising utilisation of the resources through economies of scale and functional specialisation;

(iii) introducing a team-based exercise of powers and performance of functions by two or more income-tax authorities, concurrently, in respect of any area or persons or classes or cases, with dynamic jurisdiction.”

In furtherance to the powers conferred u/s 130(1) & Sec 130(2), CBDT framed a Scheme called as “Faceless jurisdiction of Income Tax Authorities Scheme, 2022.” Which defines automated allocation, as defined u/s 2(1)9b), read as

“In this Scheme, unless the context otherwise requires, —

(a) ‘Acts means the Income-tax Act, 1961 (43 of 1961);

(b) ‘automated allocation” means an algorithm for randomised allocation of cases, by using suitable technological tools, including artificial intelligence and machine learning, with a view to optimise the use of resources;

Further Sec 3 of the said scheme deals with vesting of the jurisdiction with the Assessing Officer; read as

”vesting the jurisdiction with the Assessing Officer as referred to in section 124 of the Act, shall be in a faceless manner, through automated allocation, in accordance with and to the extent provided in-

(i) Section 144B of the Act with reference to making faceless assessment of total income or loss of assessee;

CBDT Schemes

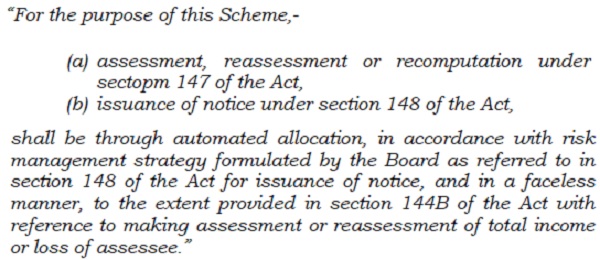

ADDITIONALLY & FURTHER, CBDT, in exercise of its powers conferred u/s 151A(1) and Sec 151A(2), framed another scheme called as the e-assessment of Income Escaping Assessment Scheme 2022, which defines automated allocation as under:

And the scope of the scheme again has been envisaged in Section 3 of the said scheme; read as under

NOW, to Analyse & read in above seriatim, as follows:

1) CBDT vide above TWO notifications dt 28-03-2022 & 29-03-2022 was very clear in its mind when it framed the aforesaid two schemes with respect to the proceedings to be drawn under Sec 148A, that is to have it in a faceless manner.

2) There were two mandatory conditions which were required to be adhered to by the Department,

(i) firstly, the allocation being made through the automated allocation system in accordance with the risk management strategy formulated by the Board under Section 148 of the Act.

(ii) Secondly, the re-assessment has to be done in a faceless manner to the extent provided under Section 144B of the Act.

After the introduction of the above two schemes:

a) IT becomes mandatory for the Revenue to conduct/initiate proceedings pertaining to reassessment u/s 147, 148 & 148A of the Act in a faceless manner.

b) Proceedings under Section 147 and Section 148 of the Act would now have to be taken as per the procedure legislated by the Parliament in respect of reopening/ re-assessment i.e., proceedings under Section 148A of the Act.

c) The amendment was brought with an intention to make the law more transparent and effective.

In the present case(after introduction of above schemes), the impugned Proceedings u/s 148A, as well as consequential notices u/s 148 of the Act,

(i) were issued by the local jurisdictional officer; and

(ii) not in the prescribed faceless manner.

It is well settled principle of law that where the power is given to do certain things in certain way, the thing has to be done in that way alone and no any other manner which is otherwise not provided under the law.

References

Chandra Kishore Jha Vs. Mahaveer & others [1999 8 SCC 266] (SC) Para-17

“it is well settled solitary principle that if statute provides for a thing to be done in a particular manner, then it has to be done in that manner and in no other manner”

Cherrukurimani Vs. Chief Secretary Government of Andhra Pradesh & Others [2015 13 SCC 722] (SC) – Para-14

“where law prescribe a thing to be done in a particular manner following a particular procedure, it shall have to be done in the same manner following the provisions of law without deviating from the prescribed procedure”

The said principle has again recently been reiterated & followed in:

(1) Municipal Corporation Greater Mumbai Vs. Abhilash Lal and others [2020 13 SCC 234]

(2) Opto Circuit India Limited Vs. Axis Bank and others [2021 6 SCC 707]

(3) UOI Vs. Mahesh Singh [No.4807 of 2022]

(4) Tata Chemicals Limited Vs. CoC (preventive) Jam Nager [2015 11 SCC 628 ]

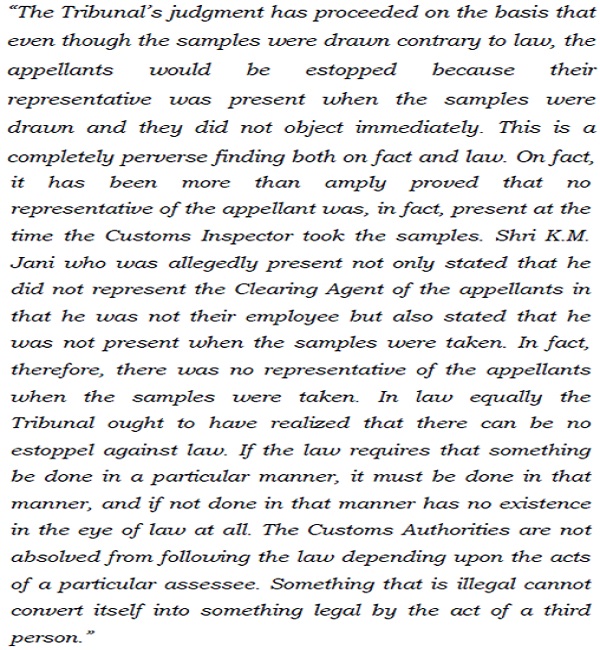

wherein it has been held that there can be no Estoppel against the law. If the law requires something to be done in a particular manner, then it must be done in that manner, if it is not done in that manner then it would have no existence in the eye of law. In paragraph 18 of the said judgment:

Thus the Notices so issued u/s 148A(b), there after orders u/s 148A(d), & Notice u/s 148 are per se illegal, and accordingly all other proceedings based on above said notices / orders are Null & Void, and don’t have any legal existence

Complied from = Writ Petition Nos.25903, 28214, 28271, 32075, 32090, 32688, 33050, 33402, 33478, 34100, 34101, 34340, 34598, 34604, 34661, 34698, 34746, 34836, 35774, 36598, 36828, 36945, 37414, 37491, 37536, 43427, 45047 of 2022, Writ Petition Nos.15383, 47, 3719, 3721, 3729, 3738, 9695, 11599, 14485, 14492, 15421, 15736, 15745, 15768, 15779, 16164, 16223, 16224, 16761, 16783, 19966, 20914, 20929, 20959 and 23556 of 2023 by Order dt 14-09-2023 of Telangana High Court

Thus on the basis of above, its suggested:

(1) Raise objections on the basis of above, in all pending proceedings u/s 148A(b)/148A(d) and 148 wherein above referred has not been followed

(2) AND to take Additional Ground of Appeal, in all pending appellate proceedings (against orders passed u/s 148A(b), 148A(d) and 148) before Hon’ble CIT(A),

“…. The present impugned assessment order is null and void as passed by not following Mandatory & Statutorily procedure ie in faceless manner as in contravention to Sec 144B / Sec 151A / Sec 130 & in contravention to CBDT Notifications dt 28-03-2022 & 29-03-2022”

Conclusion

The question of whether proceedings conducted under Sections 148A(b) and 148A(d) after the Finance Act 2021 by local jurisdictional Assessing Officers are valid is a matter of legal significance. The introduction of faceless assessment procedures and the strict adherence to statutory requirements have transformed the landscape of income tax assessments in India.

This article has provided a comprehensive analysis of the legal provisions, government schemes, and legal principles that govern the issue. It underscores the importance of compliance with statutory procedures and the consequences of failing to do so.

Taxpayers and their legal representatives are encouraged to consider the arguments presented and take appropriate actions to safeguard their rights and interests in cases where faceless procedures have not been followed.

Author Bio