Section 44AA, talks about the various provisions related to maintenance of books of accounts, which books are required to maintain and the period for which such books to maintained.

So we will analyse the provisions of section 44AA, in details –

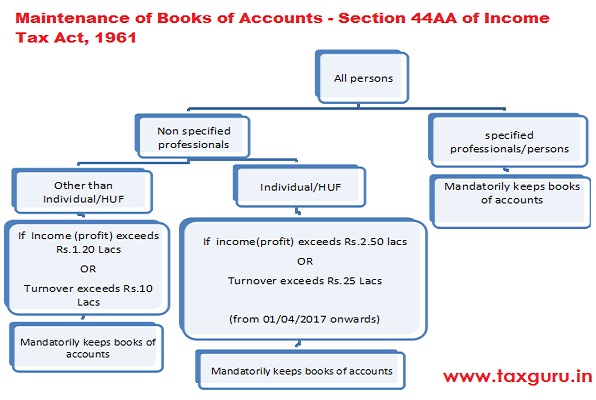

Sub-section (1) of section 44AA, says, all persons, which are carrying on specified profession or specified business, which are listed as below, are mandatorily required to keep and maintain books of accounts and other documents.

– This section 44AA(1) is applicable to all persons, whether it is a individual, HUF, firm, company, BOI/AOP etc.

– If the above persons, opts for section 44ADA, then they are not required to keep and maintain books of accounts.

– Every person covered under sub section (4) of section 44ADA, i.e.who have shown his profits below 50% of gross receipts and whose income does not exceeds the maximum amount, which is not chargeable to tax, then he is not required to maintain books of accounts.

– The specified profession/business are as follows-

1) Legal,

2) Medical,

3) Engineering or architectural profession or

4) Accountancy or technical consultancy or interior decoration or

5) Any other profession as is notified by the Board in the Official Gazette

Sub-Section (2) of section 44AA, covers all persons, who are not carrying specified professions/business. Those persons requires to maintain and keep books of accounts when-

(i) if his income from business or profession exceeds one lakh twenty thousand rupees or his total sales, turnover or gross receipts, as the case may be, in business or profession exceed or exceeds ten lakh rupees in any one of the three years immediately preceding the previous year; or

(ii) where the business or profession is newly set up in any previous year, if his income from business or profession is likely to exceed one lakh twenty thousand rupees or his total sales, turnover or gross receipts, as the case may be, in business or profession are or is likely to exceed ten lakh rupees, during such previous year; or

(iii) where the profits and gains from the business are deemed to be the profits and gains of the assessee under section 44AE or section 44BB or section 44BBB, as the case may be, and the assessee has claimed his income to be lower than the profits or gains so deemed to be the profits and gains of his business, as the case may be, during such previous year; or

(iv) where the provisions of sub-section (4) of section 44AD are applicable in his case and his income exceeds the maximum amount which is not chargeable to income-tax in any previous year,

[Provided that in the case of a person being an individual or a Hindu undivided family, the provisions of clause (i) and clause (ii) shall have effect, as if for the words “one lakh twenty thousand rupees”, the words “two lakh fifty thousand rupees” had been substituted :

Provided further that in the case of a person being an individual or a Hindu undivided family, the provisions of clause (i) and clause (ii) shall have effect, as if for the words “ten lakh rupees”, the words “twenty-five lakh rupees” had been substituted.]

For understanding purpose, the above provisions are summarized in a given diagram, in simple words –

In all above cases, all assesses, whether specified professionals or any other persons, who opts the provisions of presumptive taxation under section 44ADA, Section 44AD, Section 44 AE, are not required to keep and maintain any books of accounts.

However, in case of all assesses, who covers under the provisions of sub -section (4) of section 44ADA, i.e. who have shown there profits below 8% or 6% or 50% etc and whose income exceeds the maximum amount, which is not chargeable to tax.

It means, if the income is below, the maximum amount, which is not chargeable to tax, then they are not required to maintain books of accounts

Which books of accounts needs to maintain –

Under sub- section (3) of section 44AA, the board has prescribed, the following books of accounts to be maintained by persons, in Rule-6F, which are as follows-

1) Cash Book

2) Journal

3) Ledger

4) Carbon copies of sale bills, exceeding Rs.25/-, which should be serially numbered.

5) Bills of expenditure incurred, exceeding Rs.50/-, along with signed payment vouchers.

[Provided that the requirements as to the preparation and signing of payment vouchers shall not apply in a case where the cash book maintained by the person contains adequate particulars in respect of the expenditure incurred by him.]

6) A person carrying on medical profession shall, in addition to the books of account and other documents specified in sub-rule (2), keep and maintain the following, namely :—

(i) a daily case register in Form No. 3C;

(ii) an inventory [under broad heads, ] as on the first and the last day of the previous year, of the stock of drugs, medicines and other consumable accessories used for the purpose of his profession

At which Place such books of accounts, to be kept –

As per sub section (3) of section 44AA, under Rule 6F, the books of accounts should be maintained by the person at the place where he is carrying on the profession or, where the profession is carried on in more places than one, at the principal place of his profession.

Where the person keeps and maintains separate books of account in respect of each place where the profession is carried on, such books of account and other documents may be kept and maintained at the respective places at which the profession is carried on.

Period for which Such books to be kept –

As per sub section (3) of section 44AA, under Rule 6F, the books of accounts should be kept and maintained for a period of six years from the end of the relevant assessment year.

Author Bio

how many years should a doctor maintain records as per current income tax rules

An Individual having more then one business which are different in nature. And he exceeds the prescribed limit u/s 44AA.

Should he require to maintain seprate books of accounts for for both businesses or he can maintain consolidated books.

in SEZ different LOA units / Developers can maintain the same books of Accounts?

How about when we sell a property??