The most awaited moment for all the chartered accountants is here. Finally, the CBDT has released all the Income Tax Return (ITR) forms for AY 2020-21 / FY 2019-20. Every year we are waiting for these forms to release so that we can start our workings and data collating work from client, according to the requirements of new forms. So, to help you all a little bit, I am coming here with this article which will bring every change in ITR from last year to this year. In this article I will try to cover each and every change in all the seven ITRs. So let’s begin..

Page Contents

Changes in Form ITR-1 Sahaj for AY 2020-21

Changes in Applicability Criteria

There is no change in applicability criteria for ITR 1

Changes in Form

1. A new check point is inserted in basic information of ITR 1, mainly to cross confirm the applicability of Seventh proviso to section 139(1) i.e. whether a person have deposited more than Rs 1 crore in current bank account or have incurred Rs 2 lakh on foreign travel or Rs 1 lakh on electricity.

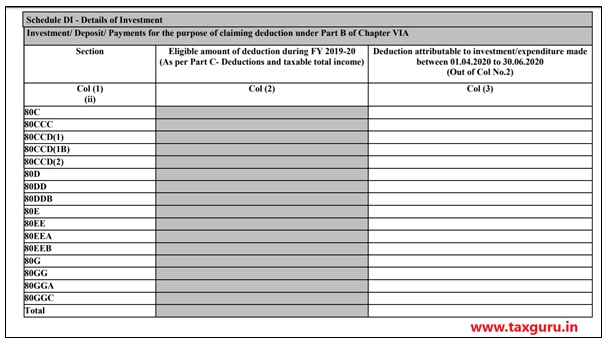

2. New Schedule DI i.e. Details of Investments is inserted at the end of the ITR 1. As we all aware that the income tax department has allowed taxpayers the laxity of making certain tax saving investments for FY 2019-20 till 30th June 2020 in view of the coronavirus lockdown. Deductions under Chapter-VIA-B of IT Act which includes Section 80C (LIC, PPF, NSC, etc), 80D (mediclaim) and 80G (donations) will now be allowed for spending till June 30th.

3. Earlier we have an option to choose any one bank account to claim refund. But now in New Forms, we have an option to choose more than one account to claim refund. But if we opt to choose more than one account, then refund will be credited to one of the accounts decided by CPC after processing the return.

Changes in Form ITR-2 for AY 2020-21

Changes in Form ITR-2 for AY 2020-21

Changes in Applicability Criteria

There is no change in applicability criteria for ITR 2

Changes in Form

1. A new check point is inserted in basic information of ITR 2, mainly to cross confirm the applicability of Seventh proviso to section 139(1) i.e. whether a person have deposited more than Rs 1 crore in current bank account or have incurred Rs 2 lakh on foreign travel or Rs 1 lakh on electricity.

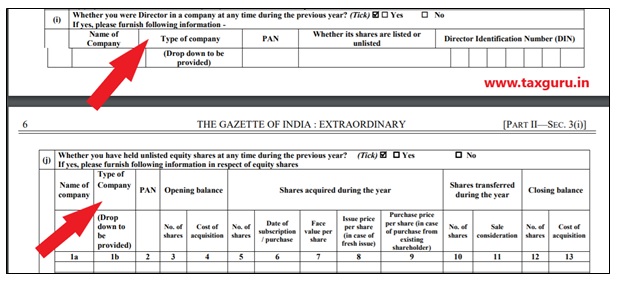

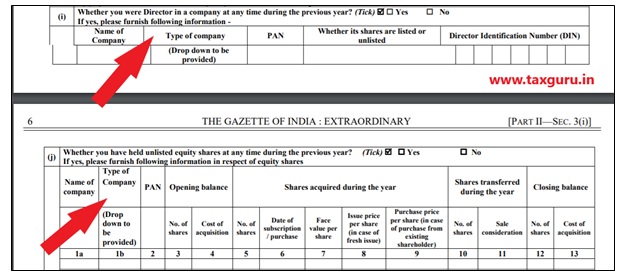

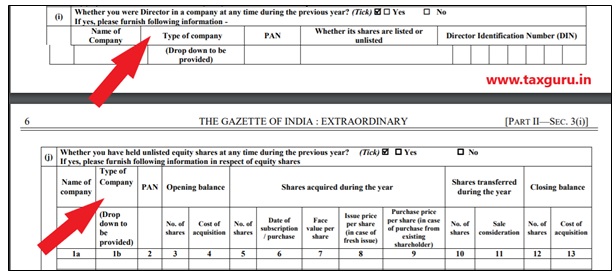

2. Under Basic information in ITR 2, where assessee needs to disclosed about his directorship in companies or holding of unlisted equity shares, one new disclosure column is added here which is “Type of Company”

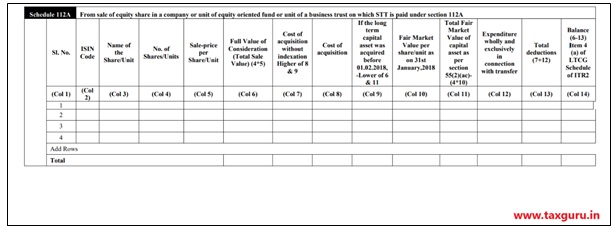

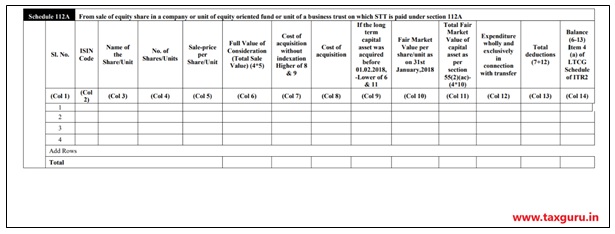

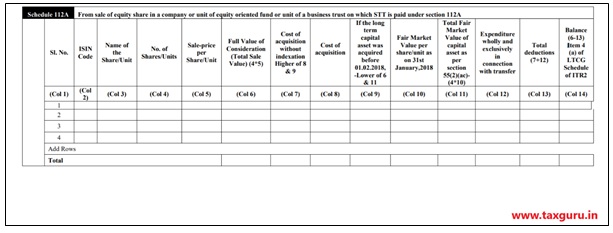

3. Introduced New Schedule 112A – From sale of equity share in a company or unit of equity-oriented fund or unit of a business trust on which STT is paid under section 112A

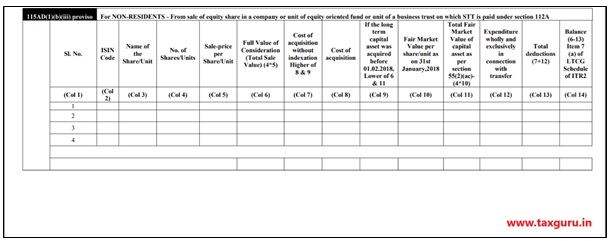

4. Introduced New Schedule 115AD(1)(b)(iii) proviso – For NON-RESIDENTS – From sale of equity share in a company or unit of equity-oriented fund or unit of a business trust on which STT is paid under section 112A

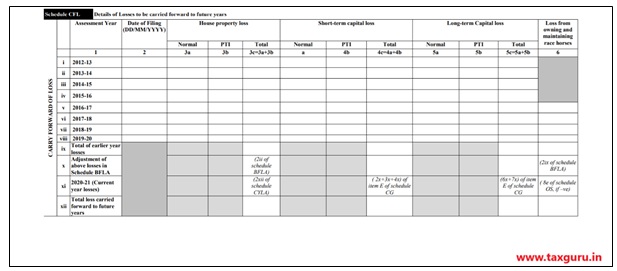

5. In schedule CFL i.e carry forward of losses, now there is a requirement of bifurcation of loss details in two columns mainly Normal loss and PTI. This specification is require for House Property, Short Term Capital Gains and Long Term Capital Gains.

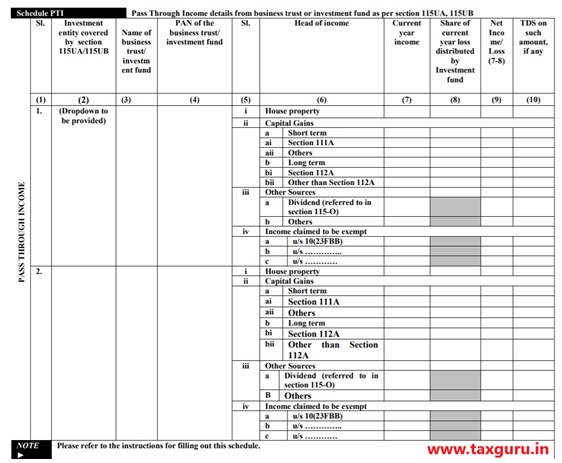

6. There are some additional disclosures made under schedule PTI, which are as under:

- Investment entity covered by section 115UA/115UB

- Bifurcation of Amount as per following 3 ways:

- Current year income

- Share of current year loss distributed by Investment fund

- Net Inco me/ Loss

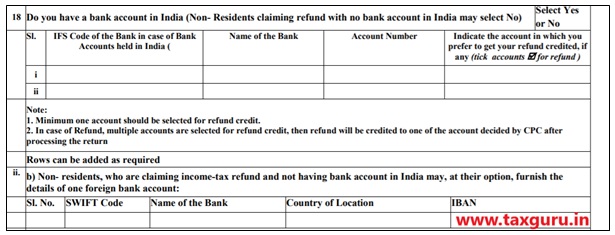

7. Now there is separate disclosure for Bank accounts in case of Non- Resident who are claiming income-tax refund and not having bank account in India. Following details will be required to disclose:

- SWIFT Code

- Name of the Bank

- Country of Location

- IBAN

Further, same option which is there in ITR 1 i.e. to choose more than one account to claim refund is as it there in ITR 2 as well.

8. New Schedule DI i.e. Details of Investments is inserted. As we all aware that the income tax department has allowed taxpayers the laxity of making certain tax saving investments for FY 2019-20 till 30th June 2020 in view of the coronavirus lockdown. Deductions under Chapter-VIA-B of IT Act which includes Section 80C (LIC, PPF, NSC, etc), 80D (mediclaim) and 80G (donations) will now be allowed for spending till June 30th.

The dates for making investment, construction or purchase for claiming roll over benefit in respect of capital gains under sections 54 to section 54GB has also been extended to June 30.

Changes in Form ITR-3 for AY 2020-21

Changes in Form ITR-3 for AY 2020-21

Changes in Applicability Criteria

There is no change in applicability criteria for ITR 3

Changes in Form

1. A new check point is inserted in basic information of ITR 3, mainly to cross confirm the applicability of Seventh proviso to section 139(1) i.e. whether a person have deposited more than Rs 1 crore in current bank account or have incurred Rs 2 lakh on foreign travel or Rs 1 lakh on electricity.

2. Under Basic information in ITR 3, where assessee needs to disclosed about his directorship in companies or holding of unlisted equity shares, one new disclosure column is added here which is “Type of Company”

3. Now there is new disclosure criteria regarding declaring income under presumptive income scheme such as section 44AE/44B/44BB/44AD/44ADA/44BBA/44BBB

4. There is additional disclosure in Other Information. Point No 11(da) and point No 17 is added.

- Point 11 – Any amount debited to profit and loss account of the previous year but disallowable under section 43B

- Sub Point (da) – Any sum payable by the assessee as interest on any loan or borrowing from a deposit taking non-banking financial company or systemically important non-deposit taking nonbanking financial company, in accordance with the terms and conditions of the agreement governing such loan or borrowing

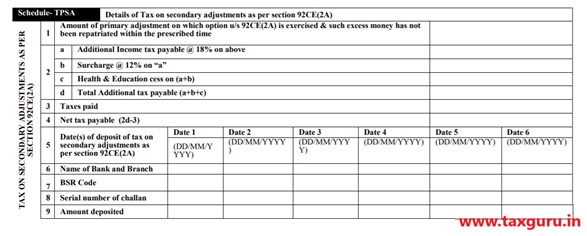

- Point 17 – Whether assessee is exercising option under subsection 2A of section 92CE (Tick – Yes/ No) [If yes , please fill schedule TPSA]

5. Under Depreciation on Plant and Machinery (Other than assets on which full capital expenditure is allowable as deduction under any other section) – New rate option of 45% is added.

6. Introduced New Schedule 112A – From sale of equity share in a company or unit of equity-oriented fund or unit of a business trust on which STT is paid under section 112A

7. Introduced New Schedule 115AD(1)(b)(iii) proviso – For NON-RESIDENTS – From sale of equity share in a company or unit of equity-oriented fund or unit of a business trust on which STT is paid under section 112A

8. In schedule CFL i.e carry forward of losses, now there is a requirement of bifurcation of loss details in two columns mainly Normal loss and PTI. This specification is require for House Property, Short Term Capital Gains and Long Term Capital Gains.

9. There are some additional disclosures made under schedule PTI, which are as under:

- Investment entity covered by section 115UA/115UB

- Bifurcation of Amount as per following 3 ways:

- Current year income

- Share of current year loss distributed by Investment fund

- Net Income/ Loss

10. New Schedule – TPSA introduced – Details of Tax on secondary adjustments as per section 92CE(2A)

11. New Schedule DI i.e. Details of Investments is inserted. As we all aware that the income tax department has allowed taxpayers the laxity of making certain tax saving investments for FY 2019-20 till 30th June 2020 in view of the coronavirus lockdown. Deductions under Chapter-VIA-B of IT Act which includes Section 80C (LIC, PPF, NSC, etc), 80D (mediclaim) and 80G (donations) will now be allowed for spending till June 30th.

The dates for making investment, construction or purchase for claiming roll over benefit in respect of capital gains under sections 54 to section 54GB has also been extended to June 30.

9. Now there is separate disclosure for Bank accounts in case of Non- Resident who are claiming income-tax refund and not having bank account in India. Following details will be required to disclose:

- SWIFT Code

- Name of the Bank

- Country of Location

- IBAN

Further, same option which is there in ITR 1 i.e. to choose more than one account to claim refund is as it there in ITR 3 as well.

Changes in Form ITR-4 for AY 2020-21

Changes in Form ITR-4 for AY 2020-21

Changes in Applicability Criteria

There is no change in applicability criteria for ITR 4

Changes in Form

1. A new check point is inserted in basic information of ITR 4S, mainly to cross confirm the applicability of Seventh proviso to section 139(1) i.e. whether a person have deposited more than Rs 1 crore in current bank account or have incurred Rs 2 lakh on foreign travel or Rs 1 lakh on electricity.

2. New Schedule DI i.e. Details of Investments is inserted. As we all aware that the income tax department has allowed taxpayers the laxity of making certain tax saving investments for FY 2019-20 till 30th June 2020 in view of the coronavirus lockdown. Deductions under Chapter-VIA-B of IT Act which includes Section 80C (LIC, PPF, NSC, etc), 80D (mediclaim) and 80G (donations) will now be allowed for spending till June 30th.

3. Earlier we have an option to choose any one bank account to claim refund. But now in New Forms, we have an option to choose more than one account to claim refund. But if we opt to choose more than one account, then refund will be credited to one of the accounts decided by CPC after processing the return.

Changes in Form ITR-5 for AY 2020-21

Changes in Applicability Criteria

There is no change in applicability criteria for ITR 5

Changes in Form

1. Under Basic information in ITR 5, where assessee needs to disclosed about his directorship in companies or holding of unlisted equity shares, one new disclosure column is added here which is “Type of Company”

2. Now there is new disclosure criteria regarding declaring income under presumptive income scheme such as section 44AE / 44B / 44BB / 44AD / 44ADA / 44BBA / 44BBB

3. There is additional disclosure in Other Information. Point No 11(da) and point No 17 is added.

- Point 11 – Any amount debited to profit and loss account of the previous year but disallowable under section 43B

- Sub Point (da) – Any sum payable by the assessee as interest on any loan or borrowing from a deposit taking non-banking financial company or systemically important non-deposit taking nonbanking financial company, in accordance with the terms and conditions of the agreement governing such loan or borrowing

- Point 17 – Whether assessee is exercising option under subsection 2A of section 92CE (Tick – Yes/ No) [If yes , please fill schedule TPSA]

4. Introduced New Schedule 112A – From sale of equity share in a company or unit of equity-oriented fund or unit of a business trust on which STT is paid under section 112A

5. Introduced New Schedule 115AD(1)(b)(iii) proviso – For NON-RESIDENTS – From sale of equity share in a company or unit of equity-oriented fund or unit of a business trust on which STT is paid under section 112A

6. Under Computation of income from business or profession, New section “E” is added i.e. Computation of income from life insurance business referred to in section 115B

7. In schedule CFL i.e carry forward of losses, now there is a requirement of bifurcation of loss details in two columns mainly Normal loss and PTI. This specification is require for House Property, Short Term Capital Gains and Long Term Capital Gains.

8. There are some additional disclosures made under schedule PTI, which are as under:

- Investment entity covered by section 115UA/115UB

- Bifurcation of Amount as per following 3 ways:

- Current year income

- Share of current year loss distributed by Investment fund

- Net Income/ Loss

9. New Schedule – TPSA introduced – Details of Tax on secondary adjustments as per section 92CE(2A)

10. New Schedule DI i.e. Details of Investments is inserted. As we all aware that the income tax department has allowed taxpayers the laxity of making certain tax saving investments for FY 2019-20 till 30th June 2020 in view of the coronavirus lockdown. Deductions under Chapter-VIA-B of IT Act which includes Section 80C (LIC, PPF, NSC, etc), 80D (mediclaim) and 80G (donations) will now be allowed for spending till June 30th.

The dates for making investment, construction or purchase for claiming roll over benefit in respect of capital gains under sections 54 to section 54GB has also been extended to June 30.

Changes in Form ITR-6 for AY 2020-21

Changes in Applicability Criteria

There is no change in applicability criteria for ITR 6

Changes in Form

1. Now there is new disclosure criteria regarding declaring income under presumptive income scheme such as section 44AE / 44B / 44BB / 44AD / 44ADA / 44BBA / 44BBB

2. There is additional disclosure in Other Information. Point No 11(da) and point No 17 is added.

- Point 11 – Any amount debited to profit and loss account of the previous year but disallowable under section 43B

- Sub Point (da) – Any sum payable by the assessee as interest on any loan or borrowing from a deposit taking non-banking financial company or systemically important non-deposit taking nonbanking financial company, in accordance with the terms and conditions of the agreement governing such loan or borrowing

- Point 17 – Whether assessee is exercising option under subsection 2A of section 92CE (Tick – Yes/ No) [If yes , please fill schedule TPSA]

3. Introduced New Schedule 112A – From sale of equity share in a company or unit of equity-oriented fund or unit of a business trust on which STT is paid under section 112A

4. Introduced New Schedule 115AD(1)(b)(iii) proviso – For NON-RESIDENTS – From sale of equity share in a company or unit of equity-oriented fund or unit of a business trust on which STT is paid under section 112A

5. Under Computation of income from business or profession, New section “E” is added i.e. Computation of income from life insurance business referred to in section 115B

6. In schedule CFL i.e carry forward of losses, now there is a requirement of bifurcation of loss details in two columns mainly Normal loss and PTI. This specification is require for House Property, Short Term Capital Gains and Long Term Capital Gains.

7. Under Computation of income from business or profession, in section “F – Intra head set off of business loss of current year” following point has been added:

- Income from Life Insurance business u/s. 115B

8. There are some additional disclosures made under schedule PTI, which are as under:

- Investment entity covered by section 115UA/115UB

- Bifurcation of Amount as per following 3 ways:

- Current year income

- Share of current year loss distributed by Investment fund

- Net Income/ Loss

9. New Schedule – TPSA introduced – Details of Tax on secondary adjustments as per section 92CE(2A)

10. New Schedule DI i.e. Details of Investments is inserted. As we all aware that the income tax department has allowed taxpayers the laxity of making certain tax saving investments for FY 2019-20 till 30th June 2020 in view of the coronavirus lockdown. Deductions under Chapter-VIA-B of IT Act which includes Section 80C (LIC, PPF, NSC, etc), 80D (mediclaim) and 80G (donations) will now be allowed for spending till June 30th.

The dates for making investment, construction or purchase for claiming roll over benefit in respect of capital gains under sections 54 to section 54GB has also been extended to June 30.

11. Now there is separate disclosure for Bank accounts in case of Non- Resident who are claiming income-tax refund and not having bank account in India. Following details will be required to disclose:

- SWIFT Code

- Name of the Bank

- Country of Location

- IBAN

Further, same option which is there in ITR 1 i.e. to choose more than one account to claim refund is as it there in ITR 7 as well.

Changes in Form ITR-7 for AY 2020-21

Changes in Form ITR-7 for AY 2020-21

Changes in Applicability Criteria

There is no change in applicability criteria for ITR 7

Changes in Form

1. Under basic personal information, four more declarations are added under tab “Details of registration or approval under the Income-tax Act (Mandatory, if required to be registered)”

- Whether Application for registration is made as per new provisions

- Section under which the registration is applied

- Date on which the application for registration/approval as per new provisions is made

- Section of exemption opted for under the new provisions

2. There are some additional disclosures made under schedule PTI, which are as under:

- Investment entity covered by section 115UA/115UB

- Bifurcation of Amount as per following 3 ways:

- Current year income

- Share of current year loss distributed by Investment fund

- Net Income/ Loss

3. Removed following two points from Part B (Total Income):

- Corpus donation to other trust or institution chargeable as per Explanation 2 to section 11(1)

- Deduction u/s 10AA

4. Added new point under Part B – Computation of tax liability on total income:

- Net tax payable on 115TD income including interest u/s 115TE (Sr.no. 12 of Schedule 115TD)

5. Now there is separate disclosure for Bank accounts in case of Non- Resident who are claiming income-tax refund and not having bank account in India. Following details will be required to disclose:

- SWIFT Code

- Name of the Bank

- Country of Location

- IBAN

Further, same option which is there in ITR 1 i.e. to choose more than one account to claim refund is as it there in ITR 7 as well.

I hope after reading this article all doubts regarding changes in ITR has been cleared and now you can fully geared up your self for handling this year Income Tax Returns.

LTCG from equity details are to be filled in Schedule 112A. However, this has 2 issues.

1. Loss in any row is not considered. It is shown computing to 0. Only the profits are added up for the total.

2. The final total is taken into B4 of the CG sheet without deducting Rs 1 lakh and appears in its entirety in the total income.

Have I done something wrong? Is nobody seeing the same thing?

its a good compilation all forms where the changes done. I wish to know that which business man file ITR 3.becouse there is option of 44AD. 44ADA, AND 44 AE also.

where do you report the cumulative losses passed on by Alternate funds (cat 1 and 2) ,as on 31-03-2019 as PASS THROUGH LOSS , by fund in PTI schedule where the column is for only current year losses

ITR 2 Schedule 112A Column 10. If units of equity mutual fund are purchased after 31 Jan 2018 and sold after an year then where is relevance to enter NAV on 31 Jan 2018. But software demands entering a numeric value in Col 10. Advice what can be done.

the hard work put in making comparison of ITRs and that too with relevant pics of that part of ITRs with detailed write up is really appreciable. It is of immense use to all tax practitioners

A very good compilation of main changes in ITRs notified for AR 2020-21 and to do more disclosure in relation to your personal expenditure of electricity and foreign traveling, cash deposit in current account, unit vise disclosure of investment sale under capital gains etc and so more.

Could you please arrange a Webinar on

1) GST

2) Different Taxes

3) ITR Return