Case Law Details

ACIT 7(1)(1) Vs Horizon Packs Pvt. Ltd. (ITAT Mumbai)

ITAT Upholds Goodwill Depreciation Because Opening Written Down Value Cannot Be Reopened; ITAT Allows Section 80G Deduction for CSR Expenditure Because It Operates Independently of Section 37; ITAT Upholds Goodwill Depreciation and Section 80G CSR Deduction Because Earlier Assessment Was Not Disturbed.

The Income Tax Appellate Tribunal (ITAT), Mumbai dismissed the Revenue’s appeals for Assessment Years 2018-19 and 2020-21, upholding the orders of the CIT(A) on depreciation on goodwill arising from amalgamation and, for AY 2020-21, the allowability of CSR expenditure as a deduction under Section 80G. The Revenue contended that the goodwill was created through the merger of group companies and that depreciation should not have been allowed. The Tribunal noted that three companies were merged with the assessee under a scheme approved by the National Company Law Tribunal (NCLT), with the difference between the purchase consideration and the net asset value being accounted for as goodwill. The Tribunal observed that depreciation on such goodwill had first been claimed and allowed in AY 2017-18 after scrutiny, and the Assessing Officer had accepted the claim without any adverse inference. Relying on the jurisdictional Bombay High Court’s decision, the Tribunal held that once depreciation on the opening written down value of the block of assets had been accepted in an earlier assessment and had not been disturbed through proceedings under the Act, the Assessing Officer could not dispute the opening written down value in subsequent years. Accordingly, the Tribunal found no infirmity in the CIT(A)’s order deleting the disallowance of depreciation on goodwill.

With respect to AY 2020-21, the Tribunal also considered the Revenue’s challenge to the allowability of CSR expenditure claimed as a deduction under Section 80G. The Assessing Officer had disallowed the claim on the ground that CSR expenditure is mandatory and therefore not deductible under Section 80G. The CIT(A) held that Section 80G falls under Chapter VIA and operates after computation of gross total income, whereas Section 37 applies only to the computation of business income, and therefore there was no conflict between the two provisions. The Tribunal noted that Coordinate Benches had consistently held that CSR expenditure could be claimed as a deduction under Section 80G, and, following those decisions, found no reason to interfere with the findings of the CIT(A). Consequently, the Tribunal dismissed all the Revenue’s grounds of appeal and upheld the relief granted to the assessee.

FULL TEXT OF THE ORDER OF ITAT MUMBAI

I.T.A. No. 5950 & 6096/Mum/2024 are two separate appeals by the revenue against two separate orders dated 21/09/2024 pertaining to AY 2018-19 and 2020-21 by NFAC, Delhi [hereinafter ‘the ld. CIT(A)’].

2. Since common grievance is involved in both the appeals, they were heard together and are disposed off by this common order for the sake of convenience and brevity.

3. The sum and substance of the grievance of the revenue is that the ld. CIT(A) erred in deleting the addition made by the AO on account of disallowance of claim of depreciation on good-will u/s 32 of the Act and in doing so, without appreciating the facts that such good-will was created by way of merger/amalgamation transactions between the group company and when such creation of good-will itself was not justified.

4. Briefly stated the facts of the case are that during the year under consideration, three companies, namely, Pyramid Packaging Private Limited, Monad Technologies Pvt. Ltd and Sigma Corru Box Private Limited, were merged with the assessee e.f. 01/04/2016. The scheme was approved by the NCLT, Mumbai Bench vide its order dated 22/03/2017, with the appointed date of the said merger as 01/04/2016 effective from 01/05/2017. The assessee had paid total purchase consideration of Rs. 3,38,95,66,300/- for acquiring the above referred three companies whose net asset value as on appointed date was Rs. 1,75,00,70,889/-. The difference of Rs. 1,63,94,95,411/- has been accounted as Goodwill in the books of accounts of the assessee on which the depreciation was claimed which is under dispute.

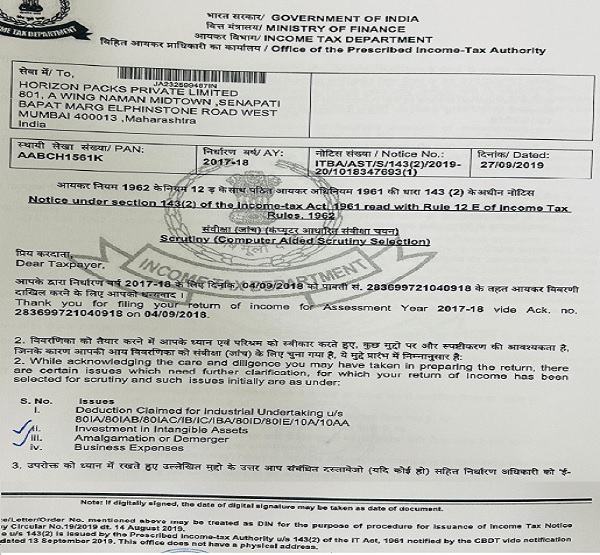

5. It would be pertinent to refer to the assessment history for AY 2017-18 which year, the depreciation was first claimed by the assessee. The return for AY 2017-18 was selected for scrutiny assessment for the following reasons as per the notice u/s 143(2) of the Act, which reads as under:-

–

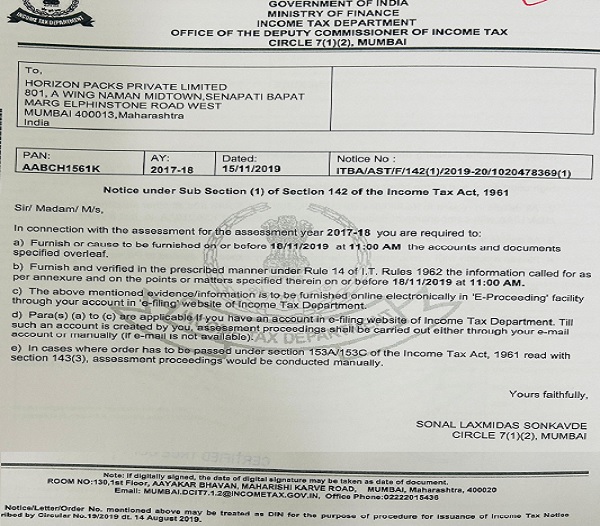

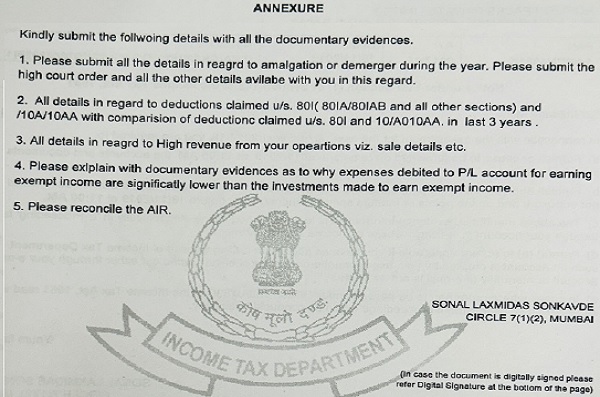

6. The notice u/s 142(1) of the Act, raised the following queries:-

–

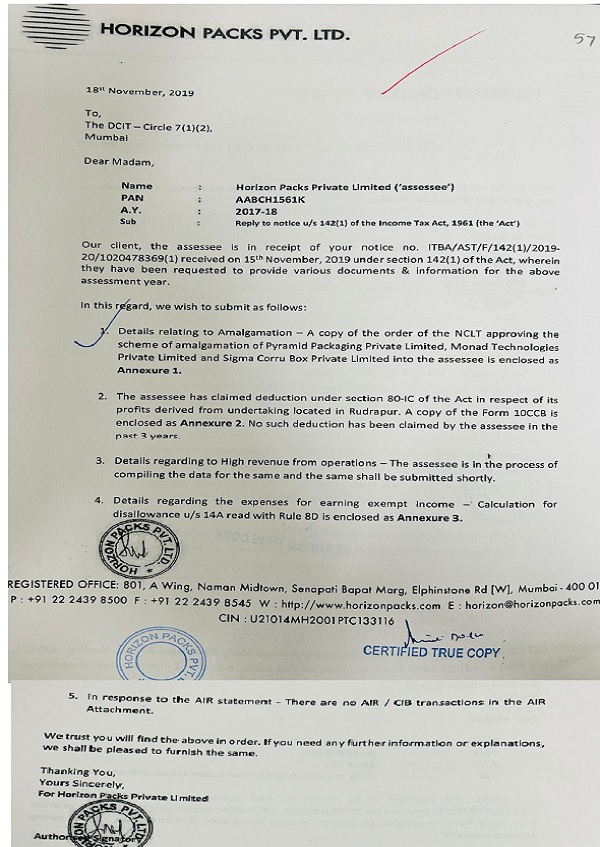

7. The assessee filed a detailed reply which reads as under:-

8. Complete scheme of amalgamation and further on Note on Amalgamation & Investment in Intangible Assets, explained as under:-

“During AY 2017-18, Pyramid Packaging Private Limited (“Pyramid”), Monad Technologies Private Limited (“Monad”) and Sigma Corru Box Private Limited (“Sigma”) (hereinafter collectively known as “the Transferor Companies”) were merged with the assessee with effect from 1 April 2016. The scheme was heard and approved by the National Company Law Tribunal (Mumbai Bench) vide its order dated March 22, 2017. A copy of the scheme is enclosed as Annexure 3. The appointed date for the said merger is 1 April 2016 and the effective date is 1 May 2017.

By way of merger, in consideration of the assets acquired by the assessee on merger, shares of the assessee have been allotted in the following manner:

– 587 fully paid up equity shares of IN 10 each of the assessee Company for every 10 fully paid up equity shares of IN 100 each held in Pyramid

– 810 fully paid up equity shares of IN 10 each of the assessee Company for every 10 fully paid up equity shares of IN 10 each held in Monad 86 fully paid up equity shares of IN 10 each of the assessee Company for every 10 fully paid up equity shares of IN 10 each held in Sigma

The said merger has been accounted for under the “Purchase” method as prescribed by Accounting Standard 14 (AS 14) “Accounting for Amalgamations” notified under section 133 of the Companies Act, 2013 read together with paragraph 7 of the Companies (Accounts) Rules 2014. Accordingly, the assets, liabilities and other reserves of the Transferor Companies as at April 1, 2016 have been taken over at their fair values. Further, the difference between the assets and liabilities taken over and the additional share capital issued in accordance with this scheme is accounted as Goodwill in the books of the assessee.

Various courts, including the Supreme Court in the case of CIT v. Smifs Securities Ltd. (2012) 348 ITR 302, have held that Goodwill, being the difference between the purchase price and the value of the assets received, is a depreciable asset under Explanation 3(b) to section 32(1) of the Act. Accordingly, the assessee has considered Goodwill arising on account of the merger as an intangible depreciable asset.”

9. With this factual background, the AO framed the assessment order dated 19/12/2019 and allowed the claim of depreciation on goodwill.

9.1. This means that during the year under consideration, the assessee has claimed depreciation on good-will on the written down value brought forward from earlier year. The Hon’ble Bombay High Court in the case of DIT (IT) vs. HSBC Asset Management (I)(P) Ltd. [2014] 47 taxmann.com 286 (Bombay), had the occasion to consider a similar situation where the depreciation was allowed in earlier assessment years and denied in subsequent assessment year. The Hon’ble High Court held as under:-

“9. Having perused this Appeal Memo including the impugned orders, we are of the opinion that the Delhi High Court judgment has been delivered on 5th November 2012 and the impugned order was passed on 15th June 2011. The Tribunal has essentially based its conclusion on the consistent stand of the Assessee and that of the Assessing Officer. In dealing with the shift in stand for the subject assessment year, the Tribunal found that this claim of depreciation was raised in the assessment year 2003-2004. The Assessee claimed that it is allowable as per the provisions of Income Tax Act on block of assets under the head “intangible assets”. The Assessing Officer allowed the claim for that assessment year by an order under Section 143(3) dated 28.03.2006. The Tribunal then, proceeds to hold that when the Assessing Officer had to allow depreciation on the written down value of the block of assets, then, it cannot in the present assessment year dispute the opening written down value of the block of assets nor can he examine the correctness or otherwise of the opening written down value brought forward from the earlier year. The order under Section 143(3) for the assessment year 2003-2004 continues to operate and no proceedings under the Act were initiated to disturb the same.”

10. We find that the ld. CIT(A) at para 5.5.8 of his order categorically mentioned that depreciation was first claimed in AY 2017-18 and the same was accepted without any adverse inference. Respectfully following the decision of the Hon’ble Jurisdictional High Court (supra), we do not find any error or infirmity in the findings of the ld. CIT(A). This common ground in both the appeals are dismissed.

11. In ITA No. 6096/Mum/2024; AY 2020-21, the revenue has raised one more ground which relates to the allowability of CSR expenses as donation u/s 80G of the Act.

12. While scrutinizing the return of income, the AO noticed that certain payments were made towards CSR expenses which were subsequently claimed as donation deductible u/s 80G of the Act. The AO disallowed the same holding that the CSR expenditure are not voluntary but mandatory in nature hence not allowable u/s 80G of the Act. When the disallowance was agitated before the ld. CIT(A), the ld. CIT(A) was of the opinion that Section 80G of the Act falls in Chapter VIA which comes into action only after the gross total income has been computed by applying the computation provisions under various heads of income and there is no co-relation between Section 37 r.w. Explanation 2 and Section 80G. The ld. CIT(A) further observed that deduction u/s 80G of the Act is available for all heads of income in contrast to Section 37, which is applicable for computing income under the head ‘business income’ only. Accordingly, the ld. CIT(A) held that the scope of Section 37(1) of the Act is limited so far as the applicability of Section 80G is concerned.

13. We find that the Co-ordinate Benches have taken a consistent view that CSR expenditure can be claimed as a deduction u/s 80G of the Act in the following cases:- Motilal Oswal Securities Ltd. (ITA No. 1795/Mum/2023, order dated 18.08.2023), Allegis Services India Pvt. Ltd. (ITA No. 1693/Bang/2019), IMS Mining Put. Ltd. [130 taxmann.com 118 (Kolkata Trib.)] and Elan Pharma (India) Pot. Ltd. vs. PCIT in ITA No. 2419/Mum/2025.

14. Respectfully following the same, we do not find any reason to interfere with the findings of the ld. CIT(A). This Ground is accordingly dismissed.

In the result, appeals by the revenue are dismissed.

Order pronounced in the Court on 6th October, 2025 at Mumbai.

Author Bio