1. Amendment Due to Assent of Finance Act, 2020

a) Change In Tax Rates/ Slab Rates

Tax Rates for Individual, HUF, AOP, BOI and Artificial Judicial Person (other than opting for Sec 115BAC)

- Tax Rates for Co-operative Society

| Particulars | Rate of Tax |

| Upto Rs. 10000 | 10% |

| Rs.10000-20000 | 20% |

| >20000 | 30% |

- Tax Rates for Others

| Particulars | Rate of Tax |

| A.Y. 2020-21 | |

| Firms | 30% |

| Local Authority | 30% |

- Rate of Surcharge for

| Taxpayer |

Rate of Surcharge |

||||

|

A.Y. 2020-21 |

|||||

|

Range Of Income |

|||||

| Rs. 50 Lakhs to Rs.1 Crore | Rs.1 Crore to Rs. 2 Crore | Rs. 2 Crore to Rs. 5 Crore | Rs.5 Crore to Rs. 10 Crore | Exceeding Rs.10 Crore | |

| Individual/HUF | 10% | 15% | 25% | 37% | 37% |

| Firm/Local Authority | – | 12% | 12% | 12% | 12% |

| Domestic Company opting for Sec 115BAA or Sec 115BAB | 10% | 10% | 10% | 10% | 10% |

| Other Domestic Company | – | 7% | 7% | 7% | 12% |

| Foreign Company | – | 2% | 2% | 2% | 5% |

| Co-operative Societies Opting for Section 115BAD | 10% | 10% | 10% | 10% | 10% |

| Other Co-operative societies | – | 12% | 12% | 12% | 12% |

> Sections Introduced:

- Section 115BA: Applicable to any domestic Co. set up and registered on or after 01.03.2016 engaged in the business of manufacturing/ Production of an article or thing and research in relation to distribution of such article or thing manufactured or produced

- Section 115BAA: All Domestic Company (Form – 10IC)

- Section 115BAB: Set up or registered on or after 01.10.2019 engaged in business of manufacturing/Production of an article or thing (Form – 10ID)

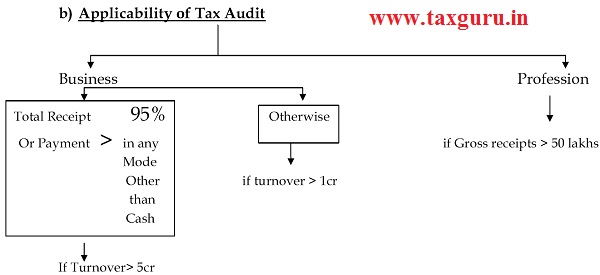

d) Due date for filling of Tax audit report:

Audit report shall be furnished at least one month prior to due date of filing of ROI (i.e. 31st October, 2020)

Thus, every assessee require to furnish Tax audit report upto 30th September

e) Trading in commodity derivatives:

- Prior to 2015, commodity derivatives was covered by FMC

- In 2015 FMC was merged with SEBI

- By specified notification, definition of commodity derivatives extended to cereals, pulses, oil seeds etc.

- Now, to encourage , commodity derivatives, Commodity transaction Tax is regulated to charge as follow:

f) No withholding of Tax at the time of exercising ESOP by an employee of eligible startup

- ESOP or Sweat equity shares are treated as perquisites in hands of employees and thus employer is liable to deduct TDS over the same at the time of exercise. As a result employees were unable to get immediate benefit from such ESOP/SES

- Therefore, to reduce the burden of taxes, it is amended that, the deduction of tax & payment of same shall be made within 14days from the day earlier of the following:

> Expiry of 48 months from end of A.Y. in which ESOPs are exercised

> At the date assessee ceases to be employee

> At the date of sale of ESOP share

g) Withdrawal of exemption for UPSC chairman & Chief election Commission

- As per section 10(45), any allowance & perquisites paid to serving or retired chairman or member of UPSC shall be exempt.

- Exemption against rent free residence, conveyance, medical, sumptuary etc.

- Both of the exemptions are now withdrawn

h) Exemption to wholly owned subsidiary of Abu-Dhabi Investment Authority (ADIA) and sovereign Wealth fund

As per section 10(23FE), income of wholly owned subsidiary of ADIA in the nature of dividend, interest or LTCG earned through Investment by way of debt or equity (on or before 31.03.2021 and held at least for 3 years) in Indian company engaged in business of developing or operating and maintaining or developing , operating and maintaining any infrastructure facility u/s 80IA (4)(i) shall be exempt.

i) Exemption to Indian Strategic Petroleum Reserve Ltd (ISPRL) :

- Any Income (as a result of arrangement for replenishment of crude oil in its storage facility) accrue/arise to ISPRL is exempt u/s 10(48C)

- Exemption shall be allowed only if:

Crude oil replenished within 3 years from the end of F.Y in which oil was removed from storage facility for the first time

j) Rationalization of provision in respect of segregated portfolios of Mutual Funds (MFs) :

Due to fraud in case of ILFS and DHFL, MF impacted severely. Therefore, SEBI has permitted MF to segregate its one scheme unit into another (two or more)

k) More persons are authorized to verify the Income Tax Return of a Co. and LLP:

In current provision of section 140, Return is verified by the following

- In case of company: It should be verified by Managing Director. But if MD is not able to sign and verify the return due to unavoidable reasons it should be verified by director of the company

- In case of LLP: it should be verified by designated partner, But if designated partner is not able to sign and verify the return due to unavoidable reasons it should be verified by any partner of the LLP

Now, as per amended provision, any other person, as may be prescribed by the board, to verify the return of income in case of company and an LLP. But such person shall hold power of attorney to verify the return.

l) Due date of filing of return:

| Particulars | Due date for filing of return for A.Y. 2020-21 |

| If assessee is required to furnish a report of transfer pricing (TP) audit in Form no.3CEB | 30th November,2020 |

| Company assessee not required to furnish transfer pricing audit report in Form No.3CEB | 31st October, 2020 |

| If assessee is required to get its accounts audited under Income Tax Act or under any other law | 31st October, 2020 |

| If individual is a partner (whether working or non-working) in a firm whose accounts are required to be audited | 31st October, 2020 |

| In any other case | 31st July, 2020 |

m) Attribution of Profit to PE within the scope of Safe Harbour Rule and Advance Pricing Agreement:

If books of account have been prepared by the foreign enterprise, a PE in India, the profits to be attributed to such PE shall be calculated in accordance with the financial statements so prepared. However, if books of accounts not been maintained, the profit attributed to the PE shall be calculated by the Assessing officer (Rule 10 of Income Tax Rules) which is disputed by the assessee.

To provide certainity in such cases, it has been provided that such attribution shall be made as per Safe Harbour Rule and the Advance Pricing Agreement.

n) No stay to be granted by the ITAT unless 20% of the disputed tax is deposited:

As per section 254(2A), ITAT may pass an order granting stay on the basis of following:

a) First Proviso: ITAT to grant stay of 180 days on the basis of merits of application made by assessee

b) Second Proviso: ITAT to grant a further stay, if, delay is not attributable to assessee. However, the aggregate of stay under first and second proviso should not exceed 365 days

c) Third Proviso: After lapse of above time frame, the order of stay shall stand vacated even if the delay is not attributable to assessee.

It is now amended in the first proviso that ITAT can grant stay under first proviso only if the assessee has deposited or furnished security to the extent of 20% of his tax liabilities. Consequential amendments have also been made to second proviso to section 254(2A).

o) Faceless Appeal is proposed up to CIT(A):

E-filing of appeals before CIT(Appeals) has already been enabled through e-filing portal. However, the process that follows after filing of neither electronic nor faceless. To achieve the motto of faceless assessment as CIT(A) level, an appellate system , with dynamic jurisdiction in which appeal shall be disposed of by one or more commissioner (appeals), has been proposed to be introduced.

p) Approval of CIT/director is required to conduct survey u/s 133A:

As per section 133A, survey can be conducted by an assistant director or deputy director or an A.O or a Tax Recovery officer or an inspector of Income Tax only after obtaining the approval of the Joint Director or the Joint Commissioner.

In order to prevent the misuse of the aforesaid provision, power of survey has been proposed to be rationalized as under:

a. Where some information has been received from the prescribed authority Survey can be conducted by an Assistant Director or a Deputy Director or an Assessing Officer or a Tax Recovery Officer or an Inspector of Income Tax only after obtaining the approval of the Joint Director or the Joint Commissioner

b. In any other case:

Survey can be conducted by Joint Director or the Joint Commissioner or an Assistant Director or a Deputy Director or an Assessing Officer or a Tax Recovery Officer or an Inspector of Income Tax only after obtaining the approval of the Director or the Commissioner

q) Reference to DRP

As per section 144C, A.O. mandated to forward the draft assessment order to the eligible assessee (Foreign company and any person to which provisions of Transfer Pricing applies) if he purposes to make any variation in the returned income or loss which is prejudicial to the interest of such assessee.

Now the amended act provides that the draft assessment order shall be forwarded to the assessee if it is prejudicial to the interest of assessee and even if it is not resulting in variation in the returned income or loss. Also, meaning of eligible assesee has been extended to include Non-Resident as well.

r) e-Assessment scheme to cover best judgment assessment:

The Finance bill, 2020 proposes to expand the scope of e-assessment to cover the best judgment assessment under section 144.

s) Insolvency professionals can act as ‘authorized representative’

Section 288 provides the person who can appear before any Income tax authority on behalf of assessee as his ‘authorized representative’.

IBC, 2016 empowers the insolvency professionals or the administrator to exercise the board of directors or corporate debtors to act as an ‘authorized representative’

t) Scope of Form 26AS widened:

The govt. is planning to enlarge the scope of form 26AS to cover the information of various transactions such as securities market.

These information will be useful for the A.O. to cross check the details furnished in ROI by taxpayers. On the other hand, taxpayer would be able to easily compute his tax liability and file ROI on the basis of Form 26AS.

For the above said purpose, a new section 285BB is purposed to be inserted to make available financial statement to the asessee containing informations of the various financial transactions made by him

Further, section 203AA (for the issuance of Form 26AS) is purposed to be deleted as section 285BB would extend the scope beyond the information about tax deducted.

u) New e-penalty scheme is purposed to be notified

Section 274 has been proposed to be amended to authorize the central government to notify an e-scheme for the purpose of imposing penalty. The directions in this regard may be made by the central government by 31.03.2022, specifying provisions relating to jurisdiction and procedure of imposing penalty shall not apply or shall apply with such exceptions, modifications, and adaptations.

v) Penalty for False entry in the books of account

To deal with fraudulent arrangements, new section 271AAD introduced, to levy penalty on a person, if it is found that in books of accounts maintained by him there is:

a) False entry;

False entry Include the following:

> Forged or falsified documents (False invoice, false piece of documentary evidence)

> Invoice in respect of supply or receipt of goods or services or both issued by the person or any other person without actual supply or receipt of such goods or services or both;

> Invoice in respect of supply or receipt of goods or services or both to ot from a person who do not exist.

b) Even, any person who cause in any manner a person to make or cause to make a false entry or cause to omit any entry shall also be liable for the same penalty

c) Any entry relevant for computation of total Income of such person has been omitted to evade tax liability.

Penalty = aggregate amount of false entries or omitted entry

w) Modifications in conditions for offshore funds:

The amendment is purposed to Section 9A (Offshore Funds) to relax following two conditions:

a) Aggregate participation of resident person in the offshore funds shall not exceeds 5% of the corpus fund. It has been amended that to calculate the aggregate participation or investment in the fund, directly or indirectly, by an Indian resident, the contribution of eligible fund manager during first 3 years up to Rs.25 crores shall not be accounted for,

b) Section prescribes that the average corpus of the fund shall not be less than 100 crores however, if the fund has been established or incorporated during the previous year, the condition of a monthly average of the corpus of the fund of Rs.100 crores should be fulfilled within 6 months from the last day of its establishment or incorporation. The period of 6 months is purposed to be increased to 12 months

x) Scope of allowing carry forward of losses or depreciation in certain amalgamation has been widened

Scope of Section 72AA has been extended to include amalgamation of one or more corresponding new banks under a scheme brought into force by the CG under section 9 of the Banking Companies and amalgamation of govt. Companies under scheme sanctioned and brought into force by the CG under section 16 of the General Insurance Business

2. Amendment Due to COVID-19

a) Tax Saving Investment for FY 2019-20 under section 80C, 80D, 80G etc can be made till 06.2020

b) Revised and Belated ITR for FY 2018-19 can be filed till 30.06.2020 (Late fees of Rs.1000, for Income up to Rs.5 Lakhs and late fees of Rs.10000 for other ITR will be applicable as earlier)

c) Advance Tax, TDS/TCS which will be due to be paid between 20.03.2020 to 29.06.2020 can be paid till 30.06.2020 with a reduced rate of Interest @ 0.75% per month or part thereof

d) Due date of linking of PAN and Aadhar has been extended till 30.06.2020

e) Deduction of amount contributed to PM – CARES fund will be allowed @ 100% deduction without any limit under section 80G

Author Bio