From the way in which the NFAC functions it is inferred that the purpose for which it was established is not served viz. litigation will be reduced to a very great extent as the assessment orders will be perfect in all respects because each unit is headed by Principal Chief Commissioner of Income Tax/Principal Director General of Income Tax and supported and guided by ‘Technical Unit’, Verification Unit’ and ‘Disputes Resolution Panel’. Since almost all the High Courts are flooded with writ petitions challenging the orders passed by the NFAC and most of the orders were struct down by the High Courts. The result is that the purpose for which the NFAC was established seems to be defeated. The Pr. CCIT, TN & P, Chennai has issued a Press Note dated 13.06.2022 stating that ‘Local Committee to deal with taxpayers Grievances from High Pitched Scrutiny Assessment’ has been constituted as per the guidance of CBDT to deal with the genuine grievances and these are to be disposed of within 60 days of filing the grievances. Whether the demand raised will be stayed and whether the time for filing appeal will also be extended once the grievance petition is filed is not known.

****

EXTRACT OF PRESS RELEASE

A “Local Committee to deal with taxpayers Grievances from High-Pitched Scrutiny Assessment” has been constituted by the Principal Chief Commissioner of Income Tax, Tamilnadu & Puducherry to expeditiously deal with Taxpayers’ grievances arising from High-Pitched Scrutiny Assessment under the Chairmanship of a Principal Commissioner of Income Tax, as per the guidelines of the CBDT.

The purpose of the constitution of the Committee is to effectively and efficiently deal with genuine grievances of tax-payers and help in supporting an environment where assessment orders are passed in a fair and reasonable manner.

Grievances arising from High Pitched Scrutiny Assessment(s) may be filed in the following email id.:chennai.hpsa.localcommitteeftincometax.g0v.in or by post to

The Local Committee for Grievances from

High Pitched Scrutiny Assessment,

0/o The Pr. Chief Commissioner of Income Tax (TN & Pdy),

No.121, Nungambakkam High Road,

Chennai – 600034.

(A. SASI KUMAR, IRS)

Addl. Commissioner of Income-Tax (HQ)(Admn. & TPS)(i/c)

0/0 the Pr. CCIT, TN & P, Chennai

******

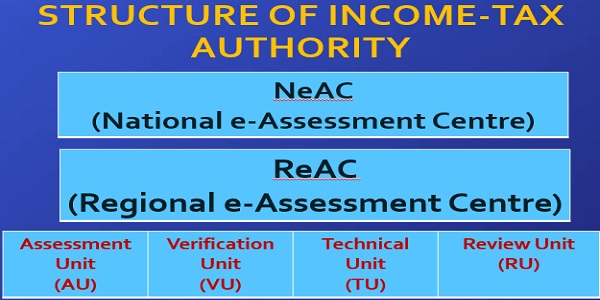

EXTRACT OF PPT ON STRUCTURE OF INCOME-TAX AUTHORITY

NeAC

> Virtually connect the Assessee

> Sends notice and receives response from the Assessee

> Transfer the documents to the required Units.

NeAC

> Communication among different Units via NeAC

> Principal Chief Commissioner or Principal Director General of Income Tax – in charge of NeAC

> NeAC shall assign case to specific AU in any one ReAC – automated allocation system

ReAC

Regional E-Assessment Center

> Each ReAc to be headed by CCIT

> 8 ReACs are set up in Delhi, Mumbai, Chennai, Kolkata, Ahmadabad, Pune,Banglore and Hyderabad.

Assessment units – AU

> For identifying points or issues, analyzing information, and other functions.

Verification Units- VU

> For enquiry, cross verification, examination of books of accounts, witness and recording of statements, and such other functions.

Verification Units- VU

- All communications to be in electronic mode except when done by verification unit for statements or personal hearing may be allowed in where SCN issued for modification but exclusively through video conferencing and/or through video telephony in any unit of this scheme.

Technical Units- TU

> For technical assistance including any assistance or advice on legal, accounting, forensic, information technology, valuation, audit, transfer pricing, data analytics, management or any other technical matter.

Review Units- RU

> For reviewing the draft assessment order to check whether the facts, relevant evidence and law and judicial decisions have been considered in the draft order.

NeAC shall

> Issue notice to the Assessee and Assessee has to respond within 15 Days

> Assign request to VU and TU

> After receipt of documents from Assessee and Reports from VU & TU transfer the same to AU

> If the Assessee fails to comply, serve notice u.s 144 for Best Judgment

> Assessee may respond to the notice u.s 144

> The AU will prepare the Draft Assessment order

> Examine the draft Assessment order – Risk Management Strategy, Automation Examination Tools etc.

> Finalise the Assessment Order and give an opportunity to Assessee for modification.

> Assign Draft Assessment order to RU

RU

> Shall conduct review of Draft Asst. Order.

> May decide to concur and intimate to NeAC.

> Or Suggest modification and send its suggestions to NeAC

NeAC

> Finalise the Draft Asst. Order.

> Upon receiving suggestions assign the case to another AU through automatic allocation system.

> AU sends the Final Draft Asst. Order to NeAC

> Shall serve Show Cause Notice and the Assessee shall furnish reply within the time frame.

> If no response – final A.O. is passed .

> If response is received the same is sent to AU, which sends back Draft A.O. to NeAC.

> If the Draft order is not prejudicial to the Assessee finalise the Order.

> If Prejudicial, another opportunity is given to the Assessee .

> NeAc shall deal with the response by following the same procedure of sending the same to AU for another Draft Order.

> At this stage the Assessee can file his objections with the Disputes Resolution Panel (DRP)

> The NeAC shall send the directions received from the DRP to the concerned AU

> The AU will prepare a draft Assessment Order in conformity with the directions issued by the DRP and send copy of the order to NeAC

> NeAC shall finalise Draft Assessment Order received from the AU and serve a copy and notice for initiating penalty proceedings, if any, to the Assessee.

> It shall issue Demand Notice specifying the amount payable by or refund due to the Assessee.

> After completion of Assessment, NeAC shall transfer all the electronic records to the Jurisdictional Assessing Officer for

> Collection and Recovery of Demand

> Imposition of Penalty.

> Rectification of Mistake

> Launch of Prosecution etc.,

APPEAL

Appeal against the Assessment Order passed by the NeAc can be filed with the CIT(Appeals) having jurisdiction over the jurisdictional A.O.

- All Income Tax appeals will be finalized in a faceless manner with the exception of appeals relating to serious frauds, major tax evasion, sensitive & search matters, International tax and Black Money Act.

EXCEPTIONS

> Assessment orders in cases assigned to Central Charges – Block Assessment cases u.s 153A/153C

> Assessment Orders incases assigned to International Tax Charges.

TECHNICAL ISSUES

> All attachments should be in PDF Format

> 1000 characters are only allowed for response – File name to be 100 characters only – file name should not be repeated.

> Maximum of 10 PDF documents can be attached for a single submission – for each attachment the size should not exceed 5 MB.

> If document exceeds 5 MB it can be split with different file names.

EXPECTATION

> Sweeping Changes have been brought in with very high technological procedures with the sole aim of bringing in perfection and eliminating corruption

> Let us hope that the assessment orders are passed with high perfection so that there are less appeals and the time spent on the assessment proceedings are brought down.

RESULT

> The time given for response is very short – less than 24 hours with intermittent holidays – notice received on Saturday 11.00a.m. directing to file the required documents before 11.00a.m. on Monday

> Cases completed u.s 143(3) are reopened u.s. 148 for the issues raised in original assessment and explained to the satisfaction of A.O. since the facts are not recorded by A.O. in the order sheet because the supporting documents given were not transferred to the NFAC, it seems

> In majority of the cases the draft assessment order is passed as the final assessment order without considering/discussing the objections given.

> If the final order is prejudicial, another opportunity is to be given to the Assessee; but it is not given

> As per the scheme the Draft Assessment order is to be assigned to the RU for examining the objections given by the assessee; but from the way in which assessments are completed it is not known whether any such RIVEW UNIT exists at all.

> In VC the language problem emerges – Hindi – English and accent – the way of speaking.

> If VC is requested for it is to given; formerly it was at the option of NFAC

> The List of case laws are given separately and all of them are writ petitions filed in various High Courts, wherein the orders passed by NFAC are cancelled.

> The case laws are listed under the following nine headings:

1. Personal hearing through Video Conferencing not given

2. Assessments are made hastily i.e. without examining the records submitted, without issuing SCN etc.,

> The case laws are listed under the following nine headings:

3. Objid reasons are given for making additions as ‘Unexplained Credits’ and taxing them under section 69 & 69A.

4. Adjournment not given

5. Disputes Resolution Panel (DRP)

6. Principles of Natural Justice – Time given for response is very less; such as 48 hours

7. Submission could not be filed due to non working of portal

8. Order passed before date of compliance as per SCN

CONCLUSION

> From the way in which the assessments were completed by NFAC it is not known, whether the procedure as laid down by the law are followed.

> The assessees were driven to High Court often to file writ petitions due to the defective functioning of the NFAC

> The very purpose of establishing the NFAC i.e assessment orders of high standard, reducing litigation etc., will be defeated if the same trend continues and unless corrective measures are taken at higher level immediately.

CONCLUSION LOCAL COMMITTEE

To relieve the assessees from the agony of High Pitched Assessments, CBDT has issued instruction No. F.No.225/101/2021 ITA-II dated 23.04.2022 directing all the offices to form ‘Local committee to deal with Taxpayers’ grievances from High Pitched Scrutiny Assessments’ with 3 members of Pr.CIT/CIT Rank to which the assessees can approach and such grievances are to be disposed of within 60 days from the date of receipt.

But it is not known whether the collection of tax will be stayed till the disposal and whether the time for filing appeal will also be automatically extended.

******

EXTRACT OF CASE LAWS

1. Personal hearing through Video Conferencing not given

| Case/Appeal No. | Case Name | Grounds of Appeal | Decisions/ Judgements |

| 1. Writ Petition (L) No. 13235 of 2021 | Shreeji Investment & Advisory Services Vs National Faceless Assessment Centre (Bombay High Court) | a) No draft assessment order was issued

b) Addition under Section 68 of the Act has been made without even giving an opportunity by issuing SCN and c) No personal hearing was granted despite petitioner requesting for the same. |

As per the judgement dated 25.10.2021, the Hon’ble Court be pleased to issue a Writ of Certiorari or any other writ, order or directionafter going through the impugned order and examining the question of legality thereof quash, cancel and set aside such impugned order and directing respondent no.1 not to take any action in furtherance to the impugned order. |

| 2. Writ Petition being WPO No. 969 of 2021 | Neeraja Rateria Vs National Faceless Appeal Centre Delhi (Calcutta High Court) | In spite of repeated request made by the petitioner, the Respondent Assessing Officer on each time has provided link for video conferencing but not provided the password. | The Hon’ble Court is of the view that the impugned assessment order has been passed in gross violation of principle of natural justice and is not tenable in the eye of law, accordingly the impugned assessment order is quashed and all actions subsequent to the impugned assessment order are not sustainable in law and the same are also quashed. |

| 3. W.P.(C) 4814/2021 | DJ Surfactants v. National E-Assessment Centre [2021] |

|

The Hon’ble High Court on 09.05.2021 passed order prima-facie in favour of the petitioner that although, a personal hearing was sought by the petitioner, the same was not granted by the assessing authority. |

| 4. Writ Petition no. 3195 of 2021 | Chander Arjandas Manwani v. NFAC (Bombay High Court) |

|

|

| 5. WP no. 6245/2021 and CM Appls. 19753-54/2021 | Naresh Kumar Goyal v. NFAC |

|

|

| 6. WP (C). 5741/2021 | Sanjay Aggarwal bearing v. NFAC (Delhi High Court) |

|

|

| 7. W.P.(C) 14528/2021 & CM APPL. 45702/2021 | Bharat Aluminium Company Ltd. V. Union Of India & Ors. |

|

|

| 8. W.P.(C) 5587/2021&CM APPL. 17382/2021 | Satia Industries Limited V. National Faceless Assessment Centre, Delhi |

|

|

2. Assessments are made hastily i.e. without examining the records submitted, without issuing SCN etc

| Case/Appeal No. |

Case Name |

Grounds of Appeal |

Decisions/Judgements |

| 1. Writ Tax No. – 465 of 2022 | Harish Chandra Bhati v. Principal Commissioner Of Income Tax Noida And 2 Others |

|

|

| 2. WP(C).No. 20314 of 2020(L) | IY TEE CEE Trading Company Vs ACIT (Kerala High Court) | The respondent proceeded to finalize the assessment in a hasty manner ignoring the objections and explanations given by the petitioner. | HC quash order and direct the respondent to redo the assessment in relation to the petitioner by considering the materials produced by the petitioner to justify his contentions on merit. |

| 3. W.P.(C) 4774/2021 & CM APPL. No.14723/2021 | K L Trading Corporation Vs National E-Assessment Centre Delhi (Delhi High Court) |

|

As per the decision dated 16.04.2021, the operation of the assessment order dated 31.03.2021 shall remain stayed till the next date of hearing (21 May 2021). |

| 4. W.P.(C) 5272/2021 | Clh Gaseous Fuel Applications Pvt. Ltd. Versus National E-Assessment Centre, Delhi(Delhi High Court) |

|

|

| 5. W.P.(C) 5087/2021 and CM APPL. No.15585/2021 | M/S SasFininvest LLP Versus National E-Assessment Centre Income Tax Department New Delhi(Delhi High Court) |

|

As per the decisions dated 04.05.2021, the Assessee should be given fair opportunity to explain his position on the proposed variations, accordingly issue notice and the impugned order shall stay. |

| 6. W.P. (C) No. 11052 of 2021 | Parag Kishor chandra Shah v. National Faceless Assessment Centre in W.P. | The assessment order has been passed without giving a proper opportunity of being heard to the assessee and as such the order is not in adherence to the principles of natural justice. |

|

| 7. W.P.(C) 6482/2021 | RMSI Private Ltd. v. National E-Assessment Centre(Delhi HC) |

Assessment proceeding done by NFAC without issuing SCN to the assessee. | The Delhi High Court on 14.07.2021, held that it is mandatory for the NFAC to give an opportunity of being hearing to the assessee by serving SCN. |

| 8. W.P.(C) 9651/2021 & CM APPLs. 29810-11/2021 | Pooja Singla Builders and Engineers Private Limited v. National Faceless Assessment Centre & Ors | The impugned assessment order passed – no mandatory valid show cause notice as well as draft assessment order had been issued to the Petitioner and created a tax demand of Rs. 3,11,37,680/-. | Having heard learned counsel for the parties, this Court is of the view that the Act mandatorily provides for issuance of a prior show cause notice and draft assessment order before issuing the final assessment order. So the order set aside and the matter is remanded back to the Assessing Officer, who shall issue a show cause notice and draft assessment order. |

| 9. Writ Petition No. 10949 of 2021 | Shelf Drilling Offshore Services (India) Private Limited v Deputy Commissioner of Income Tax, Mumbai and Others (Bombay High Court) | The petitioner’s submissions were not heard at all in respect of the new additions made in the assessment order. |

|

3. Objection given by the assessee is neither considered nor rejected for the proposed additions

| Case/Appeal No. | Case Name | Grounds of Appeal | Decisions/Judgements |

| 1. W.P. No. 1732 of 2020 & W.M.P. Nos. 2006 & 2007 of 2020 | Salem Sree Ramavilas Chit Company v. Dy. CIT | The petitioner has explained the deposit of cash amounting Rs. 67,37,500 collected during the demonetization with necessary breakups but the respondent without considering it passed order that it is to be treated as unexplained income but the collection made from regular chit fund business of the petitioner. | Since the assessment proceedings no longer involve human interaction and is based on records alone, the assessment proceeding should have commenced much earlier so that before passing assessment order, the respondent assessing officer could have come to a definite conclusion on facts after fully understanding the nature of business of the petitioner.

|

| 2. W.P.(C) 7406/2022 | Divya Capital One Private Limited v. Assistant Commissioner Of Income Tax Circle 7(1) Delh&Anr.(Delhi High Court) |

|

|

| 3. Writ Petition No.1625 of 2021 | Mantra Industries Limited Vs National Faceless Assessment Centre (NFAC or NeAC) &Ors. (Bombay High Court) |

|

The Hon’ble Court is of the view that respondents have passed the assessment order without application of mind, without considering replies. Therefore the order and consequential notices are set aside. |

| 4. W.P.(C) 5234 OF 2021 AND CM NOS. 16065-16067 OF 2021 | KBB Nuts (P.) Ltd. v. National Faceless Assessment Centre Delhi(Delhi High Court) |

|

As per the decision dated 10.05.2021, the impugned assessment order was be to set aside and NFAC was to pass a fresh assessment order after taking into account objections filed qua show cause notice on behalf of petitioner. |

4. No valid reasons are given for making additions as ‘Unexplained Credits’ and taxing them under section 69 & 69A

| Case/Appeal No. |

Case Name |

Grounds of Appeal |

Decisions/Judgements |

| 1. W.P.(MD)No.3999 of 2020 And W.M.P.(MD).Nos. 3394 And 3395 of 2020 | Nadimuthupathar Sundarapandian Elavarman Vs. Acit (Madras High Court) | Cash deposited treated as unexplained money under Section 69 (A) without considering the fact that cash amount deposited under the Pradhan Mantri Garib Kalyan Yojana Scheme, 2016, which cannot be treated as unexplained money. | As per the decision dated 09.12.2020, the impugned assessment order is hereby quashed and the matter is remanded back to the respondent for fresh consideration. |

5. Adjournment not given

| Case/Appeal No. | Case Name | Grounds of Appeal | Decisions/Judgements |

| 1. W.P.(C) 8012/2021 | SG Corporation Joint Venture Vs ITO & Ors. (Delhi High Court) | The impugned notices are invalid in the eyes of law and void from inception as they were issued without following the process of issuance of prior notice under section 148A of the Act- amendments are applicable to all the notices issued under Section 148 of the Act post 01 April, 2021. | Judgement dated 11.08.2021- Court is of the prima facie view that the impugned notification is contrary to settled principle of statutory interpretation, namely, that any action taken post the amendment of a procedural section would have to abide by the new procedures stipulated in the amended Act and the date for implementation of statutory provision, as stipulated in the Act, cannot be varied or changed.

|

| 2. CM APPL. No.16785/2021 | Blue Square Infrastructure LLP Vs NFAC (Delhi High Court) |

|

|

| 3. | Magick Woods Exports Private Limited v National e-Assessment Centre, Delhi |

|

The court directed the tax authorities to enable the online portal to receive the objections, hear the petitioner and complete the assessment in accordance with law.

|

| 4. CM No. 16066/2021 | KBB Nuts Private Limited Vs National Faceless Assessment Centre Delhi (Delhi High Court) |

|

Judgement of the High Court:

|

6. Disputes Resolution Panel (DRP)

| Case/Appeal No. | Case Name | Grounds of Appeal | Decisions/Judgements |

| 1. WPA No.13778 of 2021 | Lexmark International (India) Private Limited Vs Union of India & Ors. (Calcutta High Court) | The Respondent A.O passed impugned order without waiting for the directions of DRP and without considering the circular of CBDT dt. 25.06.2021 that last date of filing such objections under that section was extended till 31 August, 2021- in which the order seeks the petitioner to file response within 30 days. |

|

| 2. WP Nos.38884 of 2015 and 1143 of 2016 and MP Nos.1 of 2015 and 875 of 2016

|

M/S.Sesa Sterlite Limited vs DRP-2, Deputy commissioner and assistant commissioner of Income Tax (Madras High Court) |

|

As per the judgment dated 29.07.2021, the proceeding before the DRP is quashed, the consequential assessment order passed by the Assessing Authority is also quashed. The proceedings before the DRP stands restored.

|

7. Principles of Natural Justice – Time given for response is very less; such as 48 hours

| Case/Appeal No. | Case Name | Grounds of Appeal | Decisions/Judgements |

| 1. W.P.(C) 5234 OF 2021 AND CM NOS. 16065-16067 OF 2021 | KBB Nuts (P) Ltd v. National Faceless Assessment Centre in [2021] (Delhi) |

|

The Hon’ble High has held that, “without getting into the tenability of the objections on merits, in our view, the best course forward would be to set aside the impugned assessment order dated 22.04.2021, and have respondent no.1 pass a fresh assessment order after taking into account the objections filed qua the show cause notice dated 19.04.2021 on behalf of the petitioner.” |

| 2. Writ Petition no. 2848 of 2021 | Suresh Kumar Lakhotiya v. NFAC (Mumbai High Court) | The assessee had filed a grievance petition on the portal for the unreasonable manner in which the assessment was being carried out. | As per the decision on 08.09.2021, The Mumbai High Court quashed the assessment order which gave only 30 hours to the assessee to respond to the Show Cause Notice. |

Author Bio

Unless the high-pitched artificial demands are put to end, the Government may think of winding up of NFAC because the assesseess are put to lot of trouble; either they have to file a writ or pay 20% and go for appeal. Incidentally the Allahabad High Court in the case of Harish Chandra Bhati (Writ Tax No. -465 of 2022)has observed that NFAC has passed conflicting orders as to treating the same of piece of land as agri. Land in one case and non-agri. Land in another case by subjecting the sale to Capital Gains Tax.