INTRODUCTION

In the budget speech, for FY 2015-16, the then Finance Minister Late Shri Arun Jaitely succinctly set the tone to have a more competitive tax regime in order to expand investments, jobs and the overall growth in the country. Subsequently, the CBDT in 2015 stipulated a road map to phase out from profit linked and investment linked tax deductions for corporate as well as non-corporate taxpayers. This intent was turned into action when the government reduced the tax rates from 30% to 25%, for corporate tax assessee, subject to a turnover cap.

A major change was brought in the year 2019, when our Hon’ble Finance Minister Smt. Nirmala Sitharaman promulgated the Taxation Laws (Amendment) Ordinance Act, 2019 in which a completely new corporate tax regime prescribing fixed rates, as opposed to the conventional trend of prescribing the rates under Finance Act was brought into effect.

It introduced Section 115BAA & 115BAB – concessional tax rate of 22%/15% respectively for domestic companies. In addition, a new Section 115BAC was introduced for Individuals/HUFs specifying different slab rates vide Finance Act, 2020.

By virtue of this paper, the authors have undertaken the task to find out how beneficial the new tax rates would be, if opted. The paper is divided into two parts, first, dealing with the corporates and second, the individuals/HUF u/s 115BAC.

A. IMPACT OF THE NEW CORPORATE TAX REGIME

It is necessary to note that as per the August Bulletin of the Ministry of Corporate Affairs, there are about 11.86 lakh companies are active in India as on 31.08.2019 and out of these companies around 99.3% companies are having a turnover of less than 400 crores. Thus, most likely majority of these domestic companies are paying tax at the rate of 25% (plus surcharge and cess) under 115BA or under the first schedule of the Finance Act.’

By choosing the provisions of 115BAA/115BAB, effective tax would amount to 25.17% and 17.16% respectively and the provisions of MAT will not be applicable, i.e. the entity will not be forced to pay tax under MAT and neither will the companies be allowed to claim the MAT credit standing in the hands of the corporate entity, if it opts for section 115BAA. However, the condition attached to availing the benefits is that the company opting either of the provisions will not be allowed to avail the following deductions.

| Section | Particulars/Nature of Business | Applicability Conditions | Amount of Deduction |

| 80-IA | Infrastructure facility | Indian Company commencing its business on or before 31.03.2017 | 100% for 10 consecutive years out of the applicable block period. |

| Industrial Park | – Undertaking notified by the Central Government

– Commencement of business on or before 31.03.2011 |

100% for 10 consecutive years out of the applicable block period. | |

| Power Generation, Transmission or Distribution | – Government Undertaking set up in India.

– Commencement of business on or before 31.03.2017 |

100% for 10 consecutive years out of the applicable block period. | |

| Reconstruction of a Power Unit | – India Company formed with a major equity participation on or before 30.11.2005.

– Commences operations on or before 31.03.2011 |

100% for 10 consecutive years out of the applicable block period. | |

| 80-IAB | Development of Special Economic Zones (SEZ) | – Commencement of operations on or before 31.03.2017.

– SEZ being notified on or after 01.04.2005 |

100% for 10 consecutive years out of the applicable block period. |

| 80-IAC | Eligible Business being a Start-Up | – Company incorporated b/w 01.04.2016-31.03.2021

– Turnover must not exceed 25 crores (100 crores w.e.f. 01.04.2021) – The company must hold a certificate of eligible business in the specified manner |

100% for 3 consecutive years out of the applicable block period. |

| 80-IB | Industrial Undertakings other than Infrastructure development undertakings | – Only for Undertaking in state of J&K.

– Commences its operations on or before 31.03.2012. |

100% for 5 consecutive years and 25%/30% (in case of a company)for the next 5 years |

| 80-IBA | Developing and Building Housing Project | – The project must be approved b/w 01.06.2016 – 31.03.2021

– The project must be completed within 5 years from the date of approval. |

100% deduction from profits generated out of the project |

| 80-IC | Undertaking in Special Category States | – Only for Undertaking in the state of Himachal Pradesh or Uttaranchal.

– Commences its operations on or before 31.03.2012. |

100% for 5 consecutive years and 25%/30% (in case of a company)for the next 5 years |

| 80-IE | Undertaking in North-Eastern State | – Commences its

operations on or before 01.04.2007-31.03.2017 |

100% for 10 consecutive years out of the applicable block period. |

| 80JJA | Biodegradable waste treatment | – Collecting and processing or treating biodegradable waste for generating power or producing bio-fertilizers, bio-pesticides or other biological agents or for producing biogas. | 100% for 5 consecutive years out of the applicable block period. |

| 80LA | Offshore banking unit or unit in IFSC | – scheduled bank, or, any bank incorporated by or under the laws of a country outside India;

– approved for setting up in such a Centre in a Special Economic Zone. |

– In case of Banking Unit: 100% for 5 consecutive years and 50% for the next 5 years;

– In case of IFSC: 100% for 10 consecutive years out of the applicable block period. |

| 10AA | Unit in SEZ | – Commences the manufacturing industry between after 01.04.2006 and 31.03.2021 | 100% for 5 consecutive years and 50% for the next 5 years;

– additional 5 years against the amount deposited in the SEZ Reinvestment Reserves account. |

| 32 | Depreciation | – Additional depreciation for the year in which the capital expenditure is made | 20% of the amount expensed, or

35% in case of special states |

| 32AD | Investment in P&M in Backward Areas | – Bihar, Andhra Pradesh, Telangana, West Bengal | 15% in case of backward areas |

| 33AB | Tea, Coffee or Rubber Business | – Special reserve account is opened in accordance with the approval of Tea/Coffee/Rubber Board | 40% of the amount of profits, max. to amount deposited in special account |

| 33ABA | Site Restoration fund | – Assessee in the business of prospecting, extracting or production of petroleum or gas and has entered into an agreement with the government for the same.

– has deposited any amount in a special account or Site Restoration Account |

20% of the amount of profits, max. to amount deposited in special account |

| 35 | Expenditure on Scientific Research | – Applicable to any association, university, college or other institution having scientific research as its main object and is approved or notified in the Official Gazette by the Central Government | 100% deduction for the amount donated or expensed for the purpose of scientific research |

| 35AD | Capital Expenditure in Specified Business | – Applicable to businesses mentioned in Section 35AD(2).

– Capex prior to the date of commencement can also be claimed as deduction in the year in which business commences. |

100% deduction for the amount of capital expenditure |

| 35CCC | Expenditure on Agriculture Extension Project | Expenditure on Agricultural Extension Project notified by the Board | 100% deduction of the amount expensed |

| 35CCD | Skill Development Project | Expenditure on Skill Development Project notified by the Board | 100% deduction of the amount expensed |

{*The highlighted sections are applicable to section 115BAA as well as 115BAB, whereas the non-highlighted sections are not applicable for section 115BAB.}

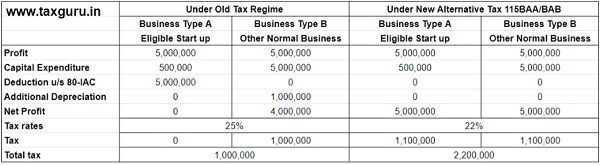

In a case, wherein the assessee company is eligible to claim any of the aforesaid deductions, it would clearly be better to utilize the existing tax rates, unless major changes are brought into force, alienating these deduction provisions. It is also pertinent to note, that the companies will have the choice of choosing between the tax rates on or before the due date of filing of return. Thus, such a decision should be taken after taking into consideration the applicable deductions and the taxation rates as prevailing.

A general scenario has been taken to evaluate the existing tax rate and the new tax rate, henceforth.

Scenario:

X Pvt. Ltd. is a company established on 01.06.2016. It has two types of businesses, one of which is eligible for a deduction u/s 80-IAC (hereinafter referred to as “Business Type A”). The company also has the option to claim an additional depreciation u/s 32.

Question:

Whether utilizing the existing rate of tax would be beneficial or the new tax rate?

Solution:

It is a clear cut case that in case of assessees having a single business to which deductions under the chapter VI are allowable (Business Type A only), the existing tax rates would prove to be more beneficial.But, in case assesses having a single business to which no such deductions are available (Business Type B only) as specified in the table above the new alternative tax rates are more beneficial but not by much.

In conclusion, the relief granted in the form of the new tax rates will not be benefiting the assessee’s in a significant way.

B. IMPACT OF THE NEW TAX REGIME ON THE INDIVIDUALS/HUF (115BAC)

INTRODUCTION:

Section 115BAC of the Income Tax Act has been introduced vide Finance Act, 2020 which deals with the new income tax slab rates, which are applicable only for individuals and Hindu Undivided Families (HUFs). This new regime comes with significantly reduced slab rates, but takes away a major part of income tax deductions and exemptions that were available under the old regime for these types of assessees. The same has been discussed as under:

APPLICABILITY:

The Assessee has the option to exercise the said option at the time of filing of his return of Income u/s 139(1). An Assessee having income from business or profession can avail this option for any AY commencing on or after 1st April 2021 and the option once exercised shall apply to subsequent assessment years. Such assessee, after opting for the new scheme and decides to opt-out of the said scheme, he can never avail the said option unless he ceases to have income from business or profession.

TAX RATES:

The following table shows the new slab rates as per Section 115BAC.

| Annual Income | New Income Tax Slab Rate |

| Nil to Rs. 2.5 lakh | Exempt |

| Above Rs. 2.5 lakh to Rs. 5 lakh | 5% |

| Above Rs. 5 lakh to Rs. 7.5 lakh | 10% |

| Above Rs. 7.5 lakh to Rs. 10 lakh | 15% |

| Above Rs. 10 lakh to Rs. 12.5 lakh | 20% |

| Above Rs. 12.5 lakh to Rs. 15 lakh | 25% |

| Above Rs. 15 lakh | 30% |

Those with income under ₹5 lakh can continue to claim rebate of up to ₹12,500 under Section 87A

DEDUCTIONS DISALLOWED:

The option to pay tax at lower rates shall be available only if the total income of assessee is computed without claiming following exemptions or deductions:

| Section | Particular of Deduction | Type of Assessee/Income holder |

| 10(5) | Leave Travel concession | Salaried Employee |

| 10(13A) | House Rent Allowance | Salaried Employee |

| 10(14) | Official and personal allowances | Salaried Employee |

| 10(17) | Allowances to MPs/MLAs | Government Employee |

| 10(32) | Allowances for income of minor | Any Individual |

| 10AA | Deduction for units established in Special Economic Zones | Business Income |

| 16(ia) | Standard Deduction | Salaried Employee |

| 16(ii) | Entertainment Allowance | Salaried Employee |

| 16(iii) | Professional Tax | Salaried Employee |

| 24(b) | Interest on housing loan | Any Individual |

| 32(1)(iia) | Additional depreciation in respect of new plant and machinery | Business Income |

| 32AD | Deduction for investment in new plant and machinery in notified backward areas | Business Income |

| 33AB | Deduction in respect of tea, coffee or rubber business | Business Income |

| 33ABA | Deduction in respect of business consisting of prospecting or extraction or production of petroleum or natural gas in India | Business Income |

| 35(1)(ii) | Deduction for donation made to approved scientific research association, university college or other institutes for doing scientific research which may or may not be related to business | Business Income |

| 35(1)(iia) | Deduction for payment made to an Indian company for doing scientific research which may or may not be related to business | Business Income |

| 35(1)(iii) | Deduction for donation made to university, college, or other institution for doing research in social science or statistical research | Business Income |

| 35(2AA) | Deduction for donation made for or expenditure on scientific research | Business Income |

| 35AD | Deduction in respect of capital expenditure incurred in respect of certain specified businesses, i.e., cold chain facility, warehousing facility, etc. | Business Income |

| 35CCC | Deduction for expenditure on agriculture extension project | Business Income |

| 57(iia) | Deduction for family Pension | Any Individual |

| Chapter VIA – Part ‘C’ | Deduction in respect of certain incomes other than specified under Section 80JJAA, 80CCD(2) and deduction under section 80LA for Unit located in IFSC | Any Individual |

SOME ADDITIONAL POINTS TO BE NOTED:

– The c/f loss or depreciation from any earlier AY shall lapse, if such loss or depreciation is attributable to any of the deductions referred in the table above

– The c/f loss under the head “Income from house property” with profit under any other heads of income.

DEDUCTIONS ALLOWED u/s 115BAC:

| Deduction u/s 80CCD(2) (employer’s contribution to the pension account) | Deduction u/s 80JJAA (additional employee cost for newly enrolled employees) | Transport Allowance for Differently Abled Employees |

| Conveyance Allowance for Official tours and conveyance | Allowance for the Cost of Travel and Conveyance | Daily Allowance given to Employees under Certain/special Conditions |

MAIN QUESTION

How beneficial is the new regime to the individual?

SOLUTION:

The same is explained with an illustration as under.

ILLUSTRATION:

| Net Income

(Rs.) |

Taxable Income | Tax Out-go | Difference Between the Total Tax Outgo

(Old Regime – New Regime) |

||

| Under Old Regime (Deduction of Rs. 2.25 lakh) | Under New Regime (No deduction) | Under Old Regime | Under New Regime | ||

| 7 lakh | 4.75 lakh | 7 lakh | 0* | 37,500 | -37,500 |

| 10 lakh | 7.75 lakh | 10 lakh | 70,200 | 78,000 | -7,800 |

| 15 lakh | 12.75 lakh | 15 lakh | 2,02,800 | 1,95,000 | +7,800 |

| 30 lakh | 27.75 lakh | 30 lakh | 670,800 | 6,63,000 | +7,800 |

CLARIFICATION:

On various representations received expressing the said concern, CBDT has issued a circular vide F.No.370142/13/2020-TPL dated April 13, 2020. The said circular has provided the following clarification:

“In case of an employee having income other than income from Business or Profession, who intends to avail concessional rate of tax u/s 115BAC shall intimate the deductor (the employer) for each previous year. Upon such intimation, the deductor shall make TDS as per the concessional rate. If such intimation is not made by the employee, the employer shall make TDS without considering the provisions of Sec 115BAC.

The intimation so made to the deductor shall be only for the purposes of TDS during the previous year and cannot be modified during that year. But, this doesn’t mean exercising the option u/s 115BAC. The option to choose the scheme is always at the time of filing of return of income u/s 139(1). Thus, the option at the time of filing of return of income and intimation made to the employer could be different.”

CONCLUSION:

The question whether an individual should opt for the new scheme or the old scheme will depend on the nature of Income, specified Savings that he makes and thus. and must be calculated on the total tax outgo as per New and old scheme.

Authors- Advocate Sankalp Malik and CA Arjun Jain

Author Bio