Case Law Details

Gujarat State Fertilizers & Chemicals Ltd. Vs DCIT (ITAT Ahmedabad)

It is evident from the same that the ITAT held that the claim of expenditure incurred by the assessee on the abandoned project, amounting to Rs.20.50 lakhs, was allowable to it subject to the assessee demonstrating the fact that it had incurred the expenditure itself, and not through Gujarat Acrylics Ltd., an Joint Venture entity of the assessee and This fact, we find, has been suitably demonstrated by the assessee, by pointing out that the Shareholders agreement between the JV partners entered on 06/01/1995 required the respective parties to the JV to bear costs up to 31-12-1994 and the assessee had till then incurred this cost of 20.51 lacs. As per the terms of agreement between the JV partners costs incurred upto 31-12 -1994 was to be borne by the partners themselves. There was no question therefore of the JV company, i.e Gujarat Acrylics Ltd, bearing any expenditure up to 31-12-1994 . The impugned expenses incurred by the assessee of 20.51 lacs have been suitably demonstrated as incurred up to 31-12-1994. The Revenue does not dispute this fact. Therefore ,there is no doubt in the fact that the said expenses of Rs.20.5 1 lacs have been incurred by the assessee itself, the Shareholders agreement ruling out in clear terms the JV company from bearing these expenses. Therefore, we find that the assessee had established clearly that this expenditure had been incurred by the assessee itself. In view of the same, we find that the assessee had sufficiently demonstrated compliance with the conditions stipulated by the ITAT for the allowance of the claim, and we hold that the assessee is entitled to the said claim of project expenses in terms of the direction of the ITAT in the first round.

Wage Settlement Expenditure Deductible in Year of Actual Payment

The ld. counsel for the assessee was unable to controvert the factual finding that to the extent of Rs.81 lacs the claim of wages was not settled in the impugned year. In view of the same, we see no reason to interfere in the order of the ld. CIT(A) disallowing the claim of wages to the extent of Rs. 81 lakhs. At the time same, we agree with the contentions of the assessee that the said claim be allowed in the year in which it is actually paid by the assessee.

FULL TEXT OF THE ORDER OF ITAT AHMEDABAD

Present appeal has been filed by the assessee against order passed by the ld. Commissioner of Income Tax (Appeals)-1, Vadodara [hereinafter referred to as “the ld. CIT(A)”] dated 13.8.2015 passed under section 250(6) of the Income Tax Act, 1961 [hereinafter referred to as “the Act” for short]for the Asst. Year 2000-01.

2. At the outset itself it was stated that this is second round of appeal before us and in the first round two claims of the assessee, disallowed by the AO, had been restored back by the ITAT to the AO for allowing the said claims after verifying compliance with specific conditions set out in the order for allowing them. It was pointed out that two issues which were restored back related to claim of expenses pertaining to abandoned project amounting to Rs.20,5 1,000/- and claim of expenses of wage settlement amounting to Rs.81,00,000/-. It was contended that in the second also both the claims of the assessee had been denied with the finding that the assessee had failed to demonstrate fulfillment of conditions which the ITAT had set out in its direction in the first round to be fulfilled by the assessee for the purpose of claiming of said deductions. The ld. counsel for the assessee contended that these finding of the authorities below was contrary to the facts, and therefore, the present appeal before us.

3. Taking first the issue relating to claim of expenses pertaining to abandoned project, the ld. counsel for the assessee pointed out that this issue was raised vide ground no.2 and 2.1 as under:

“2. The learned CIT(A) erred in law and on facts in upholding the disallowance of expenses written off incurred on abandoned project – Acrylon Nitric Project of Rs.20,51,000/- made by AO. It is submitted it be so held now.

2.1. The learned CIT(A) erred in law and on facts in exceeding his jurisdiction by adjudicating on the merits of the claim regarding allowability of expenditure on abandoned project written off despite the fact that the decision of the Hon,ble ITAT on merits was accepted by the AO by not challenging the same before the High Court. It is submitted that it be so held now and the finding of the Hon ,ble CIT(A) at Para 5.1.3 of the appellate order be struck down.”

4. The facts relating to the issue were pointed out from the order of the ITAT in the first round in ITA No.3490/Ahd/2003 dated 9.2010 placed before us at PB Page No.37 to 50. Our attention was drawn to para-5 of the said order at PB Page No.40 containing the facts relating to the issue as under:

5. Ground No.2 in assessee,s appeal relates to claim of expenses of Rs.20,51,000/- incurred on abandoned project -Acrylon Nitric project which was written off. The facts relating to this issue are that the assessee claimed an expenditure of Rs.20.51 lacs in respect of Acrylon Nitric project which; was initiated at Dahej as a joint venture with M/s Modi Rubber Ltd L For-this purpose assessee company floated another company named as Gujarat Acrylics Ltd. As per share holders agreement completed on 6.1.1995 cost and expenditure in the project incurred upto 31.12.1994 was to be borne by the respective parties except the fees payable to an Italian concern, The Italian concern was engaged for preparing feasibility report. The assessee company incurred upto 31.12.1994 an expenditure of Rs.20,50,939/-. The other partner in the joint venture required the project to be shifted to Haldia from Dahej to which assessee company did not agree and accordingly assessee decided to abandon the project and, claimed the expenditure as Revenue expenditure. The AO disallowed the claim on the ground that all the expenditure have been incurred for setting up of a new project which was abandoned mid-way. This business was not commenced and therefore, expenditure cannot be allowed unless there is some relatable income. Accordingly he proposed an addition of Rs.20.51 lacs. The Id. CIT(A) confirmed the addition by holding that the expenditure was incurred on an entirely new project for which separate facilities were to be created and it was not linked to any of the already existing units. Thus it is not an extension of the business. Since the business did not commence or abandoned in mid-way no claim is allowable under the head business income.”

5. Referring to the same, the ld. counsel for the assessee pointed out that the assessee had claimed expenses of Rs. 20.51 lakhs incurred on an abandoned project, Acrylon Nitric project entered into as a joint venture with M/s. Modi Rubber Ltd.; that for the said purpose another company had been floated by the name, Gujarat Acrylics Ltd. But since the project did not take off, all expenses incurred by the assessee in the said project amounting to Rs.20,50,939/- was claimed as expenses ,which was denied by the Revenue holding that since the business had not commenced, the expenditure could not be allowed. The ld. counsel for the assessee drew our attention to para-8 of the order wherein the ITAT had adjudicated the issue as under:

“8. We have considered the rival submissions and perused the material on record. In our considered view what is to be seen is whether assessee is able to start a new project. If assessee is not in the line of business and incurs expenditure on setting up of business which business is subsequently abandoned then such expenditure cannot be allowed as there is no business in existence. Where the assessee is already in the business then creating another unit will only be an extension of business. If assessee would have succeeded in creating an asset and established the project the expenditure so incurred would have to be capitalized with respect to that project but so long project does not see the light and no new asset is created then whatever expenditure is incurred by the assessee, it would be allowable expenditure of the existing business. Bifurcation of expenditure from the existing business to the new project would come only when new project comes into existence .If it does not, it remained the business expenditure of the existing business. However, certain facts are not clear in this case. Assessee has floated a company ‘Gujarat Acrylic Ltd. and with joint venture with Modi Rubber Ltd. The two companies would have floated their shares, created capital and would have incurred expenditure out of such capital. It has to be enquired into by the AO as to whether expenditure so claimed was actually incurred or in fact was incurred by the Gujarat Acrylic Ltd. If it was incurred by Gujarat Acrylic Ltd. then this cannot be allowed in the case of the assessee. The mode of payment and time of payment, the creation of company Gujarat Acrylic Ltd., who made the payment and to whom for which expenditure was claimed is required to be examined. If expenditure was incurred by the present assessee and was really attributed to it and not merely a transfer entry from Gujarat Acrylic Ltd. to the assessee then claim should be allowed but where it was originally incurred by the new entity and on abandoning the project, it was shifted to the assessee company then such expenditure cannot be allowed. For the limited purpose, we restore this issue to the file of AO. This ground of assessee is allowed but for statistical purposes.”

6. Referring to the same, he pointed out that the ITAT had held that the basis of disallowance by the Revenue that since no business had commenced, was not correct. On the contrary, it had held that since the assessee was already to an existing business, creating another unit was only an extension of the business, and since the project was abandoned and did not see light of the date, whatever expenditure incurred by the assessee was to be allowed. However, having held so, the ITAT pointed out that the facts relating to the claim of expenditure by the assessee, whether incurred by it or by the company that was floated i.e. Gujarat Acrylics Ltd. was not clear. The ITAT held that only if it was found that it was the assessee who had actually incurred the expenses, same could be allowed to the assessee, and in the process directed the AO to determine the time of payment, mode of payment; creation of the company, Gujarat Acrylics Ltd. and who made the payment and to whom. In effect to allow the claim only on finding the assessee to have incurred the expenses and not the new company floated.

7. The ld. counsel for the assessee thereafter pointed out that in the second round before the Revenue authorities, the assessee had demonstrated incurrence of these expenses by the assessee itself, and not by Gujarat Acrylics Ltd.. In this regard, he pointed out that it had been shown to the authorities below that as per the terms of agreement between the assessee and Modi Rubber Ltd. and Madalsa Mauritius, by virtue of which the entity Gujarat Acrylics Ltd. was set up as joint venture of the assessee and Modi Rubber Ltd., and Madalsa Mauritius, it was agreed that the respective parties were to bear cost incurred by them upto3 1.12.1994. Our attention was drawn to the said agreement dated 6.1.1995 placed before us at PB Page NO.58 to 75, more particularly, Page No.70 where relevant clause 32 of the agreement stated so as under:

“32. The respective parties agree to bear for the time being costs incurred by them up to 31st December, 1994 other than equally sharing the fees to be paid to Tecnimont S.p.A., Italy and Tecnimont India P.Ltd. for the detailed feasibility study; provided however the parties shall mutually agree on any of the costs and expenses to be reimbursed by the company or to be treated as advances towards the payment for equity shares of the company to be subscribed by the parties.”

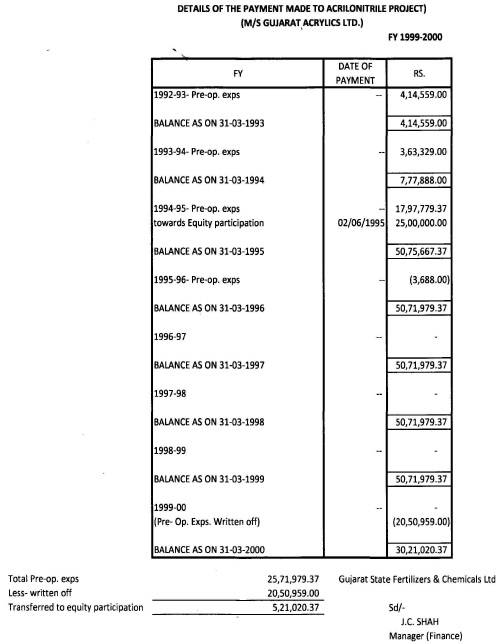

That in accordance with this agreement, the assessee had incurred expenditure up to 31.12.1994 amounting to Rs.20,50,959/- on the project ,excluding the amount spent towards equity participation of Rs.25 lakhs, and had accordingly claimed the said expenditure as revenue expenses on the abandonment of the project. The ld. counsel for the assessee contended that details of the payment mode on this new project by the assessee up to 31st December, 1994 amounting to Rs.20,50,959/- was filed to the authorities below, which was placed before us at PB Page No.55 as under:

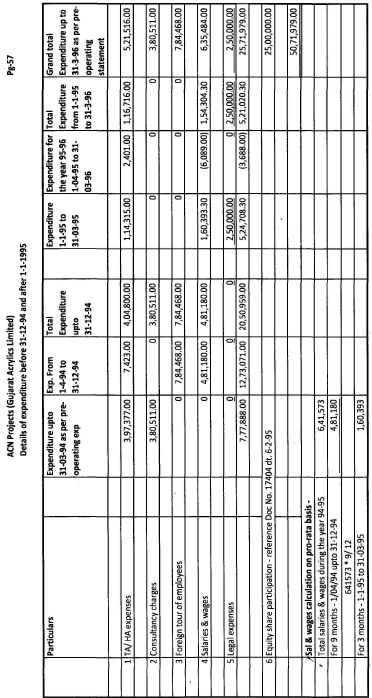

Referring to the above, he pointed out that up to the financial year 1994-95, the assessee had incurred preoperative expenses of Rs.20,50,959/- and the remaining amount of Rs.25.00 lakhs had been incurred on equity participation on 6.2.1995. He thereafter pointed out that even the details of expenses incurred by the assessee as so claimed was filed and placed before us at PB Page No.55B as under:

9. Referring to the same, he pointed out that the details reflected that the amount primarily being incurred upto3 1.12.1994 were on travelling expenses, consultancy charges, foreign tour of the employees and salaries & wages. Then, he pointed out that the Note on the discussion with Auditors on the amounts spent on the abandoned project Gujarat Acrylics Ltd. was also filed to the AO, and placed before us in PB at page no.76. The ld.counsel for the assessee therefore contended that in terms of direction of the ITAT it had been clearly demonstrated that the entire expenditure of Rs.20.51 lakhs had been incurred by the assessee up to 31.12.1994 as per the terms of shareholders’ agreement.

10. He thereafter pointed out that Gujarat Acrylics Ltd. was established only on 24.11.1994, and therefore also there is no question of Gujarat Acrylics Ltd. having incurred the expenditure. The ld. counsel for the assessee contended that the assessee had clearly demonstrated fulfillment of the above conditions stated by the ITAT in its directions for claiming the impugned expenses, and therefore, the same was allowable.

He thereafter drew our attention to the finding of the ld. CIT(A) while upholding the order of the AO at para 5.1.2 of the order. Referring to the same, he stated that claim of expenditure had been denied holding that the assessee had not complied with the directions of the ITAT on the ground that mode of payment; and to whom the payment was made and nature of expenditure claimed had not been furnished by the assessee.

The ld. counsel for the assessee contended that the crux of the directions of the ITAT was to allow the claim if it was the assessee who had incurred the expenditure and not the new entity i.e. Gujarat Acrylics Ltd., which he stated had been demonstrated by the assessee, and therefore, authorities below erred in not allowing the claim of the assessee.

11. The ld. DR however, relied on the order of the ld . CIT(A).

12. We have heard the rival contentions and have gone through the directions of the ITAT in the first round. It is evident from the same that the ITAT held that the claim of expenditure incurred by the assessee on the abandoned project, amounting to Rs.20.50 lakhs, was allowable to it subject to the assessee demonstrating the fact that it had incurred the expenditure itself, and not through Gujarat Acrylics Ltd., an Joint Venture entity of the assessee and This fact, we find, has been suitably demonstrated by the assessee, by pointing out that the Shareholders agreement between the JV partners entered on 06/01/1995 required the respective parties to the JV to bear costs up to 31-12-1994 and the assessee had till then incurred this cost of 20.51 lacs. As per the terms of agreement between the JV partners costs incurred upto 31-12 -1994 was to be borne by the partners themselves. There was no question therefore of the JV company, i.e. Gujarat Acrylics Ltd, bearing any expenditure up to 31-12-1994 . The impugned expenses incurred by the assessee of 20.51 lacs have been suitably demonstrated as incurred up to 31-12-1994. The Revenue does not dispute this fact. Therefore ,there is no doubt in the fact that the said expenses of Rs.20.5 1 lacs have been incurred by the assessee itself, the Shareholders agreement ruling out in clear terms the JV company from bearing these expenses. Therefore, we find that the assessee had established clearly that this expenditure had been incurred by the assessee itself. In view of the same, we find that the assessee had sufficiently demonstrated compliance with the conditions stipulated by the ITAT for the allowance of the claim, and we hold that the assessee is entitled to the said claim of project expenses in terms of the direction of the ITAT in the first round.

Basis of the Revenue for rejecting the claim missed the crux and contents of the directions of the Tribunal, which was simply to the effect that the assessee had to demonstrate incurrence of the expenditure itself, and for the said purpose, the Tribunal had gone to the extent of directing assessee to demonstrate mode of payment and details of payment etc. Facts demonstrated by the assessee clearly showed that the expenditure had been incurred by the assessee itself. There is no question of denial of claim to the assessee. Thus, ground no.2 and 2.1 are allowed.

13. The next issue relating to claim of wage settlement, it was pointed out that the same was raised vide Ground No.3 and 3.1 as under:

“3. The learned CIT(A) erred in upholding the disallowance of Rs.81,00,000/- on account of wage settlement stating that the AO has explicitly followed the directions of Hon‘ble ITAT despite the fact that appellant had substantiated in accordance with ITAT,s directions that claim of wage settlement was finalized during the year and payment had actually been made by appellant. The learned CIT(A) failed to appreciate that the ITAT directed AO to verify that payment is made for such wage settlement and payment in the year for settlement was not required. It is submitted that it be so held now.

3.1. Without prejudice to the above, the learned CIT(A) erred in not adjudicating the ground of the appellant to allow the deduction of wages actually paid amounting to Rs.81,00,000/- in AY 2001-02. It is submitted it be so held now and direction be given.”

The direction of the ITAT in this regard in the first ground was pointed out to us from page no.84 of the order para-7 as being as under:

“7. Having heard both the sides, we have carefully gone through the orders of the authorities below as well as relevant direction of the Tribunal contained in order of the ld. CIT(A) in the assessment years 1996-97 and 1997-98. Admittedly, the department has accepted the order of the ld. CIT(A) whereby she directed the AO to allow deduction in the year of actual payment, when wage settlement is finalized. This direction is contained in para 4.2 of the order of ld. CIT(A)-I, Baroda in Appeal No. XIV/JCIT SR. 7/3/99-00 dated 27.12.2001 for the assessment year 1996-97 and in para 3.4 of the order of ld. CIT(A)-I, Baroda in Appeal No. No. XIV/JCIT SR. 7/14/99- 00 dated 09.01.2002 for the assessment year 1997-98. As per the direction of the ld. CIT(A) in appellate orders for the assessment years 1996-97 and 1997-98, wages for which provision was made and disallowed in these two assessment years is to be allowed in the year of actual payment, when wage settlement is finalized. We, therefore, set aside the order of the ld. CIT(A) on this issue and direct the AO to verify whether in the assessment year under appeal, the wage settlement was finalized. If the reply of this question is in affirmative, the AO will further verify whether the amount is actually paid. Thereafter, the AO will allow the wage amount actually paid for which provision was made in the assessment years 1996- 97 and 1997-98. The AO is directed accordingly. Resultantly, the appeal of the assessee is allowed for statistical purposes.”

14. Referring to the above it was pointed out that the directions of the ITAT were to allow claim of wage settlement on the final settlement of the wages and on its actual payment. It was on the fulfillment of both the conditions that claim was to be allowed to the assessee.

The AO in the second round denied the claim finding that to the extent of Rs.8 1 lakhs the same was not settled by the assessee in the impugned year. Our attention was drawn to the relevant finding of the ld. CIT(A) at para-6 of his order as under:

“6. So far as third ground of appeal is concerned, the direction of the ITAT was that the AO was to verify as to whether the wage settlement was finalized in the current year and if the settlement was finalized, whether the amount was actually paid or not. The AO has accordingly made verification and has found that only an amount of Rs. 78 lacs has been actually paid during the current year, and the balance Rs. 81 lacs was paid in the next year. Accordingly the AO has not allowed claim of deduction upto the extent of Rs. 81 lacs, This action of the AO is as per the explicit directions of ITAT and hence the same is upheld.:

15. The ld. counsel for the assessee was unable to controvert the factual finding that to the extent of Rs.81 lacs the claim of wages was not settled in the impugned year. In view of the same, we see no reason to interfere in the order of the ld. CIT(A) disallowing the claim of wages to the extent of Rs. 81 lakhs. At the time same, we agree with the contentions of the assessee that the said claim be allowed in the year in which it is actually paid by the assessee. With this direction to the AO, ground of appeal No.3-3. 1are allowed in the above terms.

16. In the result, the appeal of the assessee is partly allowed.

Order pronounced in the Court on 6th March, 2023 at Ahmedabad.