1. Mutual Funds are one of the common and simplest avenues of investment for many of us. It is a mechanism for pooling money managed by a professional Fund Manager.

For Income Tax purpose, Mutual fund investment can be broadly classified into three categories i.e. (a) Equity Oriented Funds (b) Debt Funds (c) Hybrid Funds

2. DEBT-BASED MUTUAL FUNDS (DBMF) Debt Fund is a mutual fund scheme that invests in debt instruments generating fixed income. They are also known as Income Funds or Bond Funds. Debt mutual funds are managed by professional fund Managers. Their job is to invest the corpus in bonds issued by private or public companies and the government as per the fund’s investment objective.

3. BASIS OF TAXATION: Mutual funds are taxed, based on asset categorization and duration of the investment. The duration for which a person holds on to his Mutual Fund Investment is called the holding period. Short-term investments attract a tax rate different from long-term investments

4. WHICH ITR IS TO BE FILED: Capital Gains/ Losses from Debt Based Mutual Funds are to be reported in Form ITR-2 / ITR-3. A salaried person who is otherwise eligible to file ITR-1 will have to choose ITR-2 to report the capital gains. The taxpayer having income from business or profession needs to report Capital gains/ losses in ITR 3.

5. PREREQUISITE DOCUMENTS: The Capital Gain Statement is the most important document required for the purpose. It contains details of Short term / Long term Capital Gain on redemption of Mutual Funds in a financial year.

5.1 How to Access Capital Gain Statement: An Individual earning capital gains from a particular mutual fund house can download the Capital Gain Statement by login into the official website of the mutual fund house.

However, it can be quite a cumbersome task to get details of all the schemes, if an individual has invested in schemes offered by multiple fund houses. In that case, a consolidated mutual fund statement can be downloaded from RTAs (Registrar and Transfer Agents) i.e. Kaveri, or AMCs (Assets Management Services) i.e. CAMS (Computer Age Management Services)

These are SEBI-approved entities that deal with various back-office operations of fund houses, thereby allowing them to focus on investment management activities.

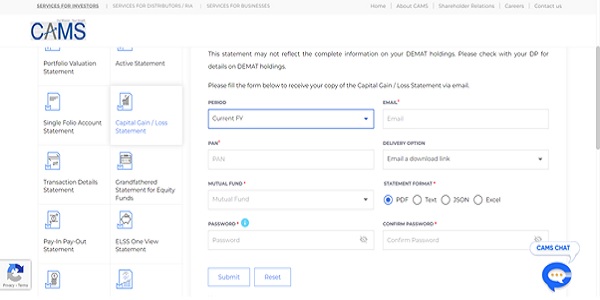

5.2. Download Mutual Fund Statement Online from CAMS:

(a) Login to CAMS (Computer Age Management Services) online portal and click on Statements/ Capital Gain/ Loss Statement.

(b) Provide a valid email address and choose a password. CAMS will use this password to encrypt the file sent to your e-mail address. Now login to your email.

(c) Click on e-mail from CAMS, and use the password chosen by you at the time of entering details on the CAMS website.

(d) Statement indicating Short Term / Long Term Capital Gain / Loss from Mutual Fund Transactions will be available for reporting the details in ITR.

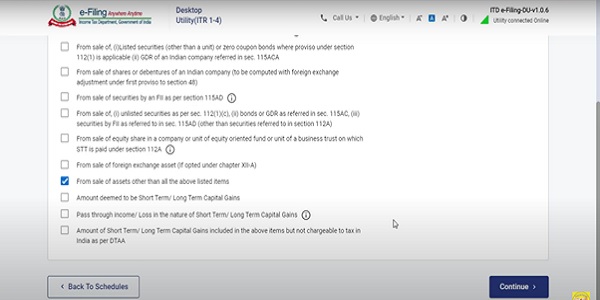

6. REPORTING OF DBMF DETAILS IN ITR 2:

(a) Login to www.incometax.gov.in

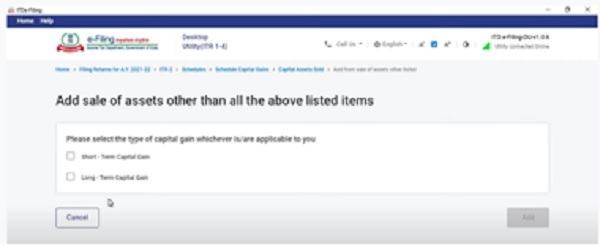

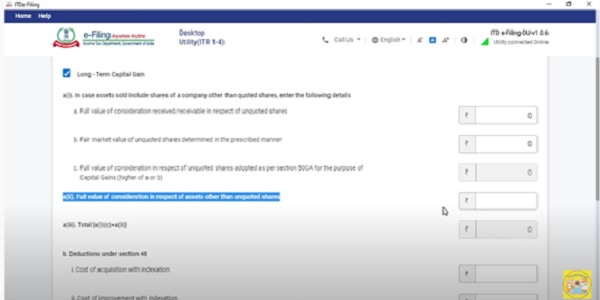

(b) Go to Schedule Capital Gain. Select “From Sale of Assets other than all the above-listed items”

The following window will be displayed: –

7. Capital gains tax on Debt Oriented Mutual Funds can be Long-term or Short-term, depending on the duration for which the individual holds the Mutual Funds.

8. SHORT TERM CAPITAL GAIN (STCG): Debt funds that are held for less than three years are taxed as Short Term Capital Gain. STCG for debt mutual funds are taxed as per the individual’s tax slab. So, if the income tax slab applicable to the taxpayer is 20%, then the debt mutual funds will be taxed at the same rate.

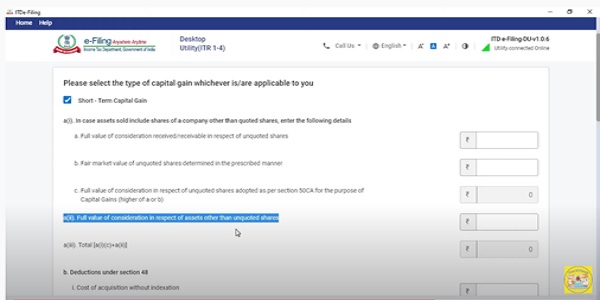

8.1. REPORTING OF SHORT TERM CAPITAL GAIN: Enter the consolidated amount of consideration received in the financial year from the sale of Short term capital Assets held under the heading “Full Value of consideration in respect of assets other than unquoted shares”.

Enter the cost of acquisition without indexation. (Indexation is not considered for calculating the Cost of Acquisition / Improvement in the case of Short Term Capital Gain.)

9. LONG TERM CAPITAL GAIN (LTCG) Debt funds that are held for more than three years are taxed as Long-Term Capital Gain. The current tax rate for LTCG on Debt Mutual Fund is 20% with indexation.

Indexation is a process by which the cost of investment in a mutual fund can be adjusted to bring it to current prices after considering inflation.

9.1 ILLUSTRATION: Mr. Anupam invested Rs. 5000/- in debt-based Mutual Fund in July 2018. The redemption value for the said investment in July 2021 is Rs. 10000/-. As the holding period was more than three years, he will get the benefit of indexation to reduce the value of long-term capital gains.

The Indexed Cost of Acquisition (ICOA) and Long Term Capital Gain (LTCG) will be computed as follows:

ICOA = Original cost of acquisition * (CII of the year of sale/CII of year of purchase)

Rs. 5000*317/280 = Rs 5661/-

LTCG = Capital Gain: Redemption Value – The indexed cost of acquisition

Rs. 10000- 5661 = Rs. 4339/-

Note: The Central Government specifies the Cost Inflation Index (CCI) by notifying in the official gazette. CCI for 2018-19 was Rs 280 and for 2021-22, it was Rs 317

9.2 REPORTING OF LONG TERM CAPITAL GAIN (LTCG)

Enter the full value of consideration in a(ii) and cost of acquisition with indexation in table (b) of the above Schedule.

10. Submit the ITR after filling in all the other details. Don’t forget to e-verify the ITR as the tax filing process is not complete without it.

Disclaimer: The article is for educational purpose only.

The author can be approached at caanitabhadra@gmail.com

Author Bio

Thank you Ms. Anita for your detailed explanation and very well written article.

Just a small clarification and will appreciate your advise on my below query ?

LTCG on debt funds if earned on multiple funds need to be shown individually or as consolidated value whilst entering data ? Pls advise ?

Hello Anita madam, I did a web search on how to reflect CG from non equity MFs in ITR. Of the very few results, Taxguru is the most credible platform that springs up with your post and I have come across your well illustrated explanations even before on individual taxation matters. Kudos to your inputs and tips which carry a great regard from DIY people like me (an ex- tech sr.manager from ONGC) and I file for many within my close family & friends

Hello @CA Anita Bhadra,

I can’t thank you enough for saving my (at least) 2 hours and approx. Rs. 2000 (fees for filing ITR-2 with someone’s help).

(This is only useful resource I found for – including STCG on debt MF in ITR-2)

I rarely comment anywhere online, but I must say – I am genuinely grateful! Keep it up! 🙂

Thank you sir for humble comment . It really means a lot to me , get motivated to do even better.

Glad that it helped you in filing Return .

Very well explained, helped a lot.

Your guide for LT gain on bond/hybrid fund is very helpful to me. I am 70 years age trying to self submitting return. Thanks.

Thank you so much Sir for your humble comment . Feeling really motivated to do even better .

Very nice article. I could complete my filing of IT using ITR 2 by referring to your demonstration. Thanks and Regards.

Thanks for your humble comment . It really motivates a lot to do better.

Mam, Where and how to show income from bit coins? Regards. Partha Sarathi Chowdhury.

Thanks for your humble comment.

Yes , you can set off Short term Debt-Mutual-fund from short term Equity-Mutual fund and vice versa.

You need to enter the details in the schedule CG and then go to Schedule CYLA ( Current Year Loss Adjustments)

You will find the figures reflecting there . Click on confirm . Setting off will take place automatically.

Nice article, informative.

I have a question : Can I setoff loss from Short term Debt-Mutual-fund from short term Equity-Mutual fund and vice versa? Is yes, how to indicate on ITR-2?

Thanks