Article discusses Meaning of Cost Inflation Index (CII) which is used for Computation of Long Term Capital Gain. Cost Inflation index are Notified by CBDT every year and till date CBDT has notified Cost Inflation Index for the Financial Year 1981-82 to Financial year 2025-26. Cost Inflation index are used for computing indexed cost of acquisition.

What is Cost Inflation Index (CII)?

It is a measure of inflation that finds application in tax law, when computing long-term capital gains on sale of assets. Section 48 of the Income-Tax Act defines the index as what is notified by the Central Government every year, having regard to 75 per cent of average rise in the consumer price index (CPI) for urban non-manual employees for the immediately preceding previous year. Therefore, if we consider that price of a capital asset has risen in tandem with base price rise, then if one want to sell an asset and replace it, the cost allowed even after indexation will be lesser than the price payable for new asset. However, in case of many capital asset the price rise is lesser than market price and in many cases it is higher.

How does Cost Inflation Index (CII) help in capital gains computation? Capital gain, as you know, arises when the net sale consideration of a capital asset is more than the cost. Since “cost of acquisition” is historical, the concept of indexed cost allows the taxpayer to factor in the impact of inflation on cost. Consequently, a lower amount of capital gains gets to be taxed than if historical cost had been considered in the computations.

Formula for computing indexed cost is (Index for the year of sale/ Index in the year of acquisition) x cost.

For example, if a property purchased in 1991-92 for Rs 20 lakh were to be sold in A.Y. 2009 -10 for Rs 80 lakh, indexed cost = (582/199) x 20 = Rs 58.49 lakh. And the long-term capital gains would be Rs 21.51, that is Rs 80 lakh minus Rs 58.49 lakh.

Cost Inflation Index:- Cost inflation index (CII) as notified by Central Government alongwith analysis of the same is as under:

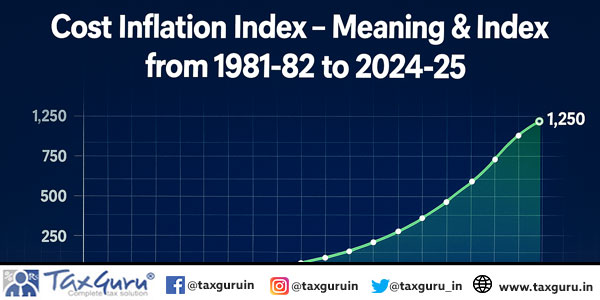

Cost Inflation Index As Applicable From Financial Year 1981-82 To Financial Year 2016-17

| FINANCIAL YEAR | COST INFLATION INDEX | Increase in CII and 75% of percentage of real inflation allowed | Real inflation % of CII Increase allowed / 3 X 4 |

| 1981-1982 | 100 | ||

| 1982-1983 | 109 | 9 = 9% | 12% |

| 1983-1984 | 116 | 7= 6.422 | 8.56% |

| 1984-1985 | 125 | 9=7.7586 | 10.34% |

| 1985-1986 | 133 | 8=6.4 | 8.53% |

| 1986-1987 | 140 | 7=5.263 | 7.02% |

| 1987-1988 | 150 | 10=7.1428% | 9.52% |

| 1988-1989 | 161 | 11=7.333% | 9.78% |

| 1989-1990 | 172 | 11=6.8323% | 9.11% |

| 1990-1991 | 182 | 10=5.8139% | 7.75% |

| 1991-1992 | 199 | 17=9.340% | 12.45% |

| 1992-1993 | 223 | 24=12.060% | 16.08% |

| 1993-1994 | 244 | 21=9.4170% | 12.56% |

| 1994-1995 | 259 | 15=6.1475% | 8.20% |

| 1995-1996 | 281 | 22=8.494% | 11.33% |

| 1996-1997 | 305 | 24=8.5409% | 11.39% |

| 1997-1998 | 331 | 26=7.8549% | 10.47% |

| 1998-1999 | 351 | 20=6.0423% | 8.06% |

| 1999-2000 | 389 | 38=10.826% | 14.44% |

| 2000-2001 | 406 | 17=4.370% | 5.83% |

| 2001-2002 | 426 | 20=4.926% | 6.57% |

| 2002-2003 | 447 | 21=4.93% | 6.57% |

| 2003-2004 | 463 | 16=3.58% | 4.77% |

| 2004-2005 | 480 | 17=3.67% | 4.90% |

| 2005-2006 | 497 | 17=3.54% | 4.72% |

| 2006-2007 | 519 | 22=4.43% | 5.90% |

| 2007-2008 | 551 | 32=6.17% | 8.22% |

| 2008-2009 | 582 | 31=5.62% | 7.50% |

| 2009-2010 | 632 | 50=8.60% | 11.46% |

| 2010-2011 | 711 | 79=12.36% | 16.49% |

| 2011-2012 | 785 | 74=10.41% | 13.88% |

| 2012-2013 | 852 | 67 = 8.54% | 11.38% |

| 2013-2014 | 939 | 87 =10.21% | 13.62% |

| 2014-2015 | 1024 | 85 = 9.05% | 12.07% |

| 2015-2016 | 1081 | 57 = 5.57% | 7.42% |

| 2016-2017 | 1125 | 44 = 4.07% | 5.43% |

Cost Inflation Index from Financial Year 2001-02 to Financial Year 2025-26

In order to revise the base year for computation of capital gains, section 55 of the Income Tax Act, 1961 was amended vide Finance Act, 2017 so as to provide that the cost of acquisition of an asset acquired before 01.04.2001 shall be allowed to be taken as fair market value as on 1st April, 2001 and the cost of improvement shall include only those capital expenses which are incurred after 01.04.2001. Cost inflation index for Long Term Capital Assets sold after 01.04.2017 as notified by CBDT Notification No. 44/2017 dated 05.06.2017 as amended from time to time.

NOTIFIED COST INFLATION INDEX UNDER SECTION 48, EXPLANATION (V)

As per Notification 70/2025, dated 01-07-2025, the following table should be used for the Cost Inflation Index :-

| TABLE | ||

| SI. No. | Financial Year | Cost Inflation Index |

| (1) | (2) | (3) |

| 1 | 2001-02 | 100 |

| 2 | 2002-03 | 105 |

| 3 | 2003-04 | 109 |

| 4 | 2004-05 | 113 |

| 5 | 2005-06 | 117 |

| 6 | 2006-07 | 122 |

| 7 | 2007-08 | 129 |

| 8 | 2008-09 | 137 |

| 9 | 2009-10 | 148 |

| 10 | 2010-11 | 167 |

| 11 | 2011-12 | 184 |

| 12 | 2012-13 | 200 |

| 13 | 2013-14 | 220 |

| 14 | 2014-15 | 240 |

| 15 | 2015-16 | 254 |

| 16 | 2016-17 | 264 |

| 17 | 2017-18 | 272 |

| 18 | 2018-19 | 280 |

| 19 | 2019-20 | 289 |

| 20 | 2020-21 | 301 |

| 21 | 2021-22 | 317 |

| 22 | 2022-23 | 331 |

| 23 | 2023-24 | 348 |

| 24 | 2024-25 | 363 |

| 25 | 2025-26 | 376 |

(Republished with Amendment, Source -Income Tax Website)

Author Bio

my flat purchased in 1993 January for 3.1 lacs sold in Oct 2025 for 49 lacs.

what is the long term capital gain with indexation ?

I have a flat, purchased in 1996 of Rs, 1,25,060.00.

If I sold it to Rs. 49,00,000.00 in fy 2025-26, what would be LTCG applicable in this case ?

I purchased flat No. 107, 1st floor, Kumardhara, N. G. H. P. Kormangala, Bengaluru-560047 for Rs.20,00, 000/- (Including stamp duty and other expenses) and sold for Rs.96,00,000 on 22/09/2025. What is Capital Gain and tax?

Sir, I have purchased a flat worth Rs 3853000 in the year 2011 on instalment basis and the possession was handed over by builder in 2015. The same was got financed from bank and instalment of bank completed in 2017. I invested Rs 10 on improvement in 2015 after possession. Now i want to sell it, but i have get the conveyance deed executed till now. Pl advise how much I have to pay under LTCG. WAITING FOR YOUR REPLY

i sold flat in year 2017 to my tenant who was residing since 1963 actually i got flat through probate the tenant is not ready to pay more than 52 lakhs of the flat but market valve is above 9000000

how to manage in income tax

i sold flat in year 2017 to my tenant who was residing since 1963 actually i got flat through probate the tenant is not ready to pay more than 52 lakhs of the but market valve is above 9000000

how to manage in income tax

i puchased residential plot from GDA GHAZIABAD at vaishali sector 1 infront ,9mtr road on 3 Aughst 1996.cost 62800/-.sold same land without any construction 70lakh on 30 april 2024.pl tell any LTCG arise, how much & for valuation how can approach you

i purchase land 1000 + 125000 lacs exp chardiwari and bhart and khui in 1982 and sale in 2024 i.e. 200000 lacs any capital gain tax applicable

I sold residential plot for 2000000 inv2024 which was purchase in1988 for rs.7000 . what will be LTCG ?

i purchase land 10000+ 125000 lacs exp chardiwari and bhart i.e. total cost is 135000

I purchased a property 4 lakhs in 1998 and sold this year 33.5 lakhs.. what is the capital gain. how much i need to pay income tax . Pls advise me on this.

I had purchased residential flat in Thane (Badlapur) for 18 Lakhs in the year 2011 and sold for 24 lakhs in year August 2023

any capital gain tax applicable

I purchased a 2BHK 1050 sq ft (BU) flat with a parking slot in Mangaluru in February 1994 for Rs3.76 lakhs including stamp duty of Rs 35,000/-. I sold the Property in September for Rs 40 lakhs. After 1.4.2001 I have spent Rs 10000 ( 2009), Rs 5000 (2012), Rs 10,000 (2015) and Rs 40,000/-(2018) on improvement/renovation and incurred expenses of Rs 65,000/- on brokerage, legal documentation to collect E-Khata and Two Encumbrance Certificates, touch up, one paint coat, electrical fittings, switch Boards etc in August 2025. What is Capital Gain for me under CII and the Fair Market Value of my sold flat as on 1.4.2001. Thanks a lot. Awaiting for your reply. S.R.Nayak