The Directorate of Income Tax (Systems) recently Instruction No. 01 of 2023, marking a pivotal shift in the response mechanism for outstanding tax demands. The new guidelines streamline the process for taxpayers and Assessing Officers, shifting to a largely online mode of response.

The new Instruction significantly reduces the response time for taxpayers to 21 days for intimation under Section 245(1) of the Income Tax Act, a move that aims to expedite the process and prevent undue delay in issuing refunds. Furthermore, the online response system brings transparency and efficiency into the process, eliminating the need for in-person interactions.

The directive also includes a comprehensive step-by-step guide for taxpayers, detailing the procedures to follow when responding to intimation under section 245(1). The introduction of this detailed guide is commendable as it reduces ambiguity and makes it easier for taxpayers to navigate the income tax system.

However, the transition to an entirely online response system could pose challenges for certain demographics, particularly the elderly or those without reliable internet access. To address this potential digital divide, it’s crucial that adequate measures are put in place to assist these individuals.

Conclusion: Instruction No. 01 of 2023 marks a significant step towards digitizing and streamlining the income tax system in India. By shortening the response time and facilitating an online response mechanism, the directive brings much-needed efficiency to the tax regulation process. While it is a positive step overall, steps need to be taken to ensure that all taxpayers can benefit from these changes. As India continues to evolve its tax system, directives like these pave the way for a more accessible and efficient taxation landscape.

Instruction No. 01 of 2023

Directorate of Income Tax (Systems)

ARA Center, Ground Floor, E-2, Jhandewalan Extension,

New Delhi — 110055

F. No.: DGIT(Systems)/Instruction/245/2023-24/2132-2142 Dated: 31.05.2023

Subject: Communication of timelines for providing response u/s 245(1) and intimating step by step procedure to be followed by the assesses for providing response to intimation u/s 245(1) issued by Centralised Processing Centre, Bengaluru through e-filing portal -regarding

As per CPC Instruction No.1 issued in F.No. DIT(S) III/CPC/2012-13. dated 27.11.2012, instructions regarding adjustment of refunds against outstanding demands and process to be followed by the assessees/Assessing Officers on receipt of intimation u/s 245 from the Centralised Processing Centre was specified. Relevant extracts of the said Instruction are as under:

“vi. In case of refunds due, on the basis of the demand so uploaded on CPCFAS, CPC shall issue a prior Intimation u/s 245 of the I T Act, 1961 to the assessee to adjust the refund against the correct and legitimate actionable demands due. Simultaneously, CPC will inform the Chief Commissioners of Income-tax (CCs1T) concerned regarding the intimation sent for his charge fortnightly. The assessees can approach Assessing Officer regarding grievance relating to demand, if any, within 15 days of receipt of intimation.

vii. The AO within 30 days of receipt of grievance in response to the notice u/s 245 shall either rectify or confirm the demand, The demand so crystallized shall be communicated back to the CPC in reference to the same communication vide which the AO was initially communicated regarding the demand. Functionality will be developed within the next six months to Intimate CPC online by AO. In the interim period AO will intimate the CPC within 30 days from the date, the assessee approaches the AO.

viii. CPC to hold the refunds (refunds may be determined but kept on hold) in the interim period and following confirmation from the AO carry out adjustment of refund against the demands.”

2. It is observed that, at the time of Issuance of the Instruction No. 1 dated 27.11.2012, the response mechanism in online mode was yet to be developed but, subsequently, facility for the Assessees and Assessing Officers to provide responses through online mode has since been provided. Such a system of allowing the assessees and the Assessing Officers to respond through online mode has since been established and is in place for sufficiently long period.

3. Consequent to deployment of online response mode, which is in place for sufficiently long period of time and also in order to avoid delays in issue of refunds, the time limit of 21 days is provided to the assessees to respond to intimation u/s 245(1) of the Income Tax Act, 1961 issued by Centralised Processing Centre. This will apply with immediate effect. Time limit for Assessing Officers has been specified vide Instruction No.06/2022 dated 28.11.2022 issued by the Directorate of Systems.

4. In order to facilitate the assesses in furnishing response to intimation u/s 245(1) issued by Centralised Processing Centre, Bengaluru, step by step procedure to be followed by the assessees for responding on e-filing portal is as per Annexure.

Additional Director General of Income Tax (Systems)-5,

New Delhi

Copy to:

i. The Sr. P.P.S to Chairman, Member(Inv.), Member(L&S), Member(IT & R), Member(A & FS), Member(TPS), Member(A & J), CBOT for information.

ii. The P.S. to DGIT(S) – 1 & 2 for information.

iii. The Web Manager, irsoffcersonline.gov.in website with the request to upload the Instruction.

iv. The Web Manager, incometaxindia.gov.in website with the request to upload the Instruction.

v. ITBA Publisher (Pubilsher@incometax.gov.in) for https://itba.incometax.gov.in with the request to upload the Instruction on the ITBA Portal.

Additional Director General of Income Tax (Systems)-5,

New Delhi

ANNEXURE

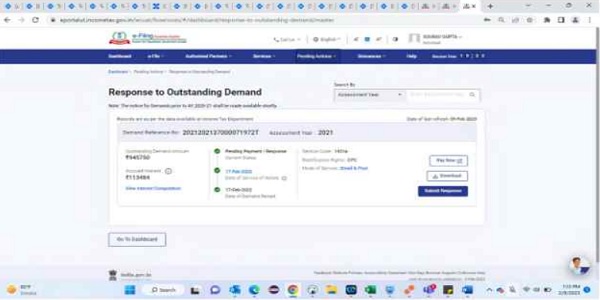

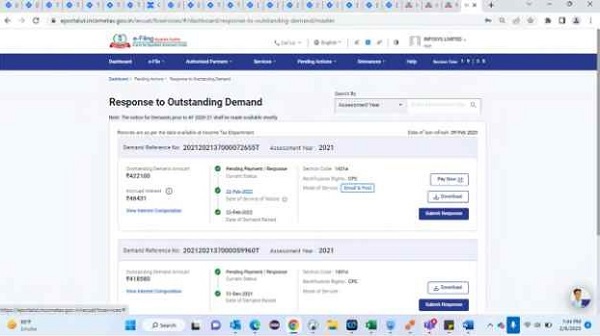

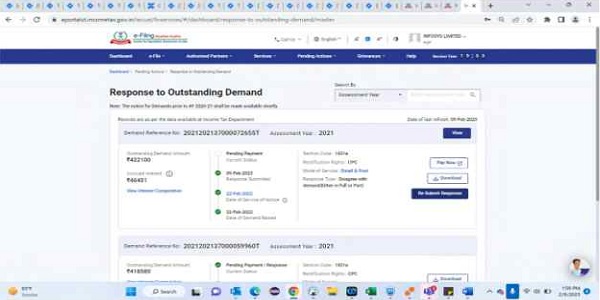

Response to Outstanding Demand

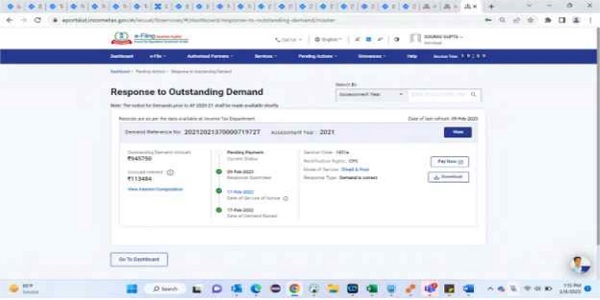

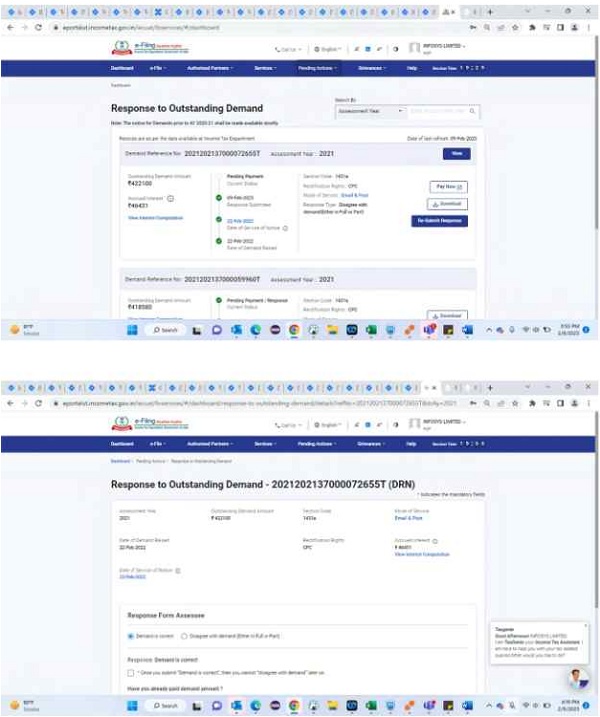

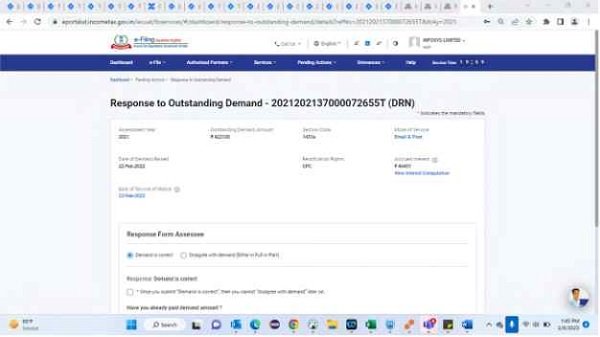

1. For filing response to the demand, taxpayer has to log on to incometax.gov.in i.e. e-filing portal of Income-tax Department and then enter their credentials i.e. User ID and password. After this, taxpayer has to navigate to “Pending Actions > “Response to Outstanding Demand”

2. To submit response, user has to click on “Submit response”. On clicking “Submit Response”, following screen will appear.

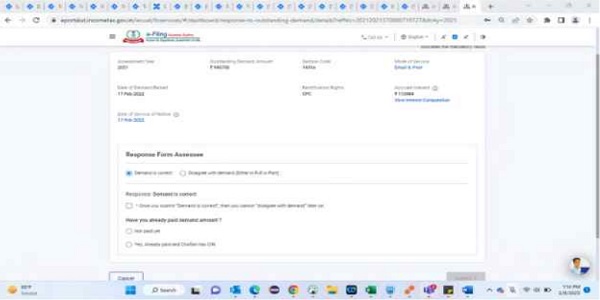

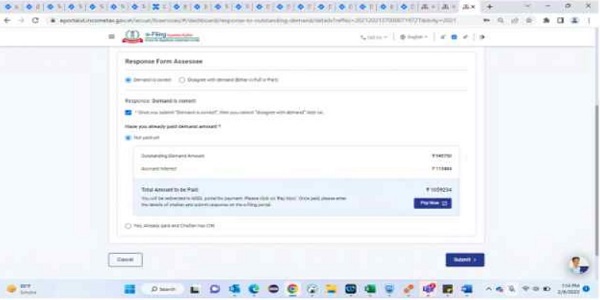

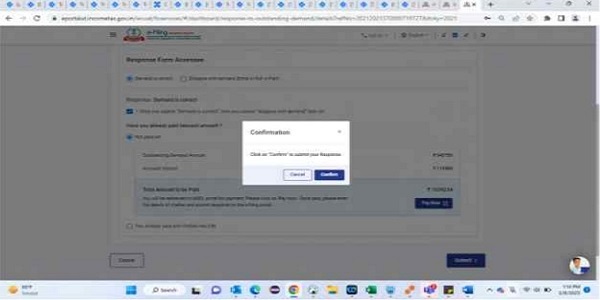

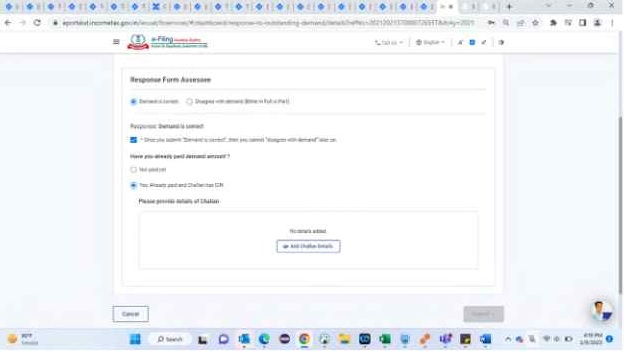

3. If the taxpayer is satisfied with the demand, option “Demand is correct” may be selected and submit his response.

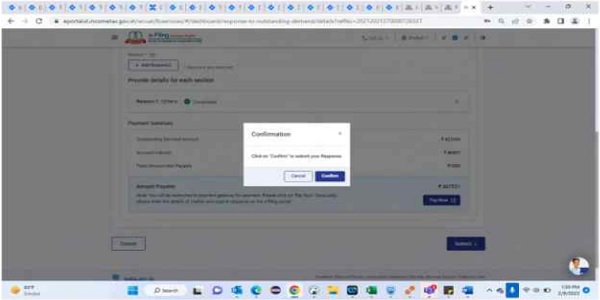

4. After submitting the response, same needs to be confirmed by clicking the “Confirm” Button.

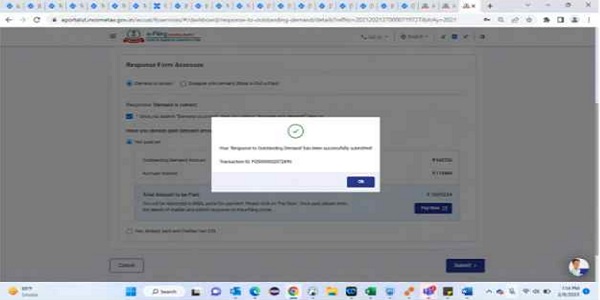

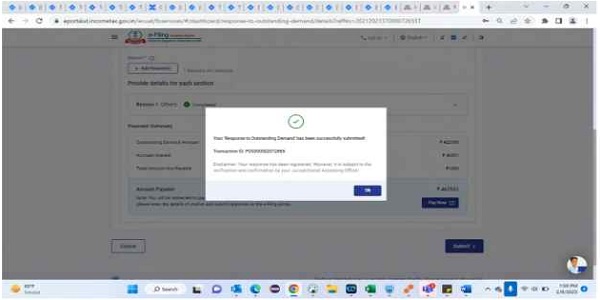

5. Once confirmed, a transaction id will be generated and shown to the tax payer.

6. After submission of response, response type will be reflected as “Demand Is correct”.

7. The tax payer needs to respond to the next set of questions about the payment status of the demand. i.e, whether the payment has already been made, or not made.

8. If the payment is not made, same may be intimated in the option “Demand not paid”, against the question “Have you already paid the demand amount?”

9. If taxpayer has paid the demand, option “Yes, already paid and challan has CIN” needs to be selected. Details of the challan are required to be entered with full challan details.

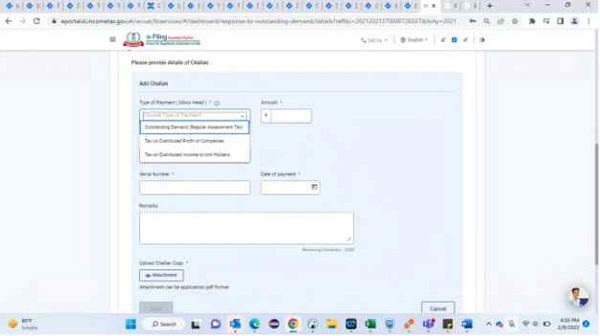

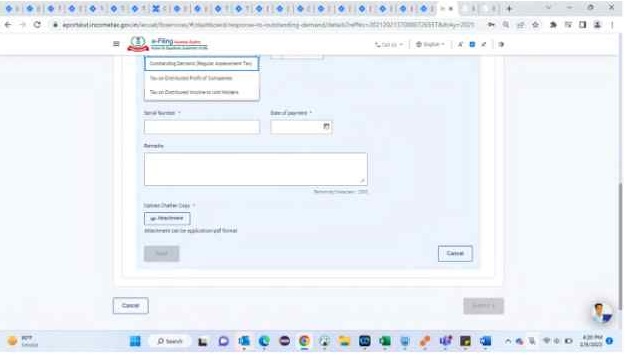

10. Details of challan to be entered are “Type of payment”, “Amount”, “Sl. No.” and “date of payment”. Copy of the challan also is required to be uploaded.

–

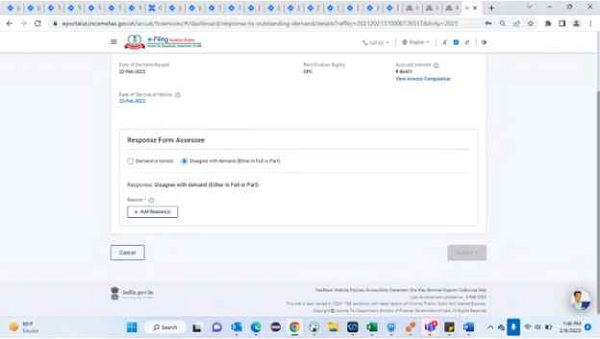

11. If the taxpayer is disagreeing with the demand, either in Part or Full, option “Disagree with demand (either In Full, or Part)” needs to be chosen.

–

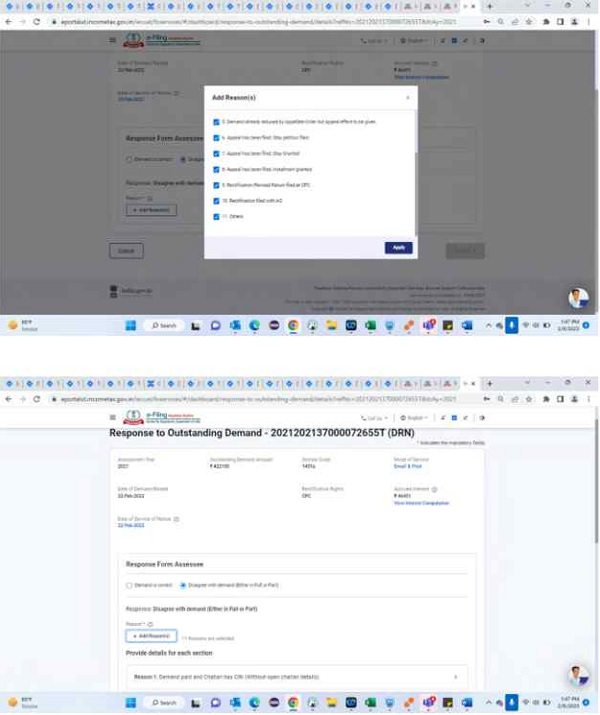

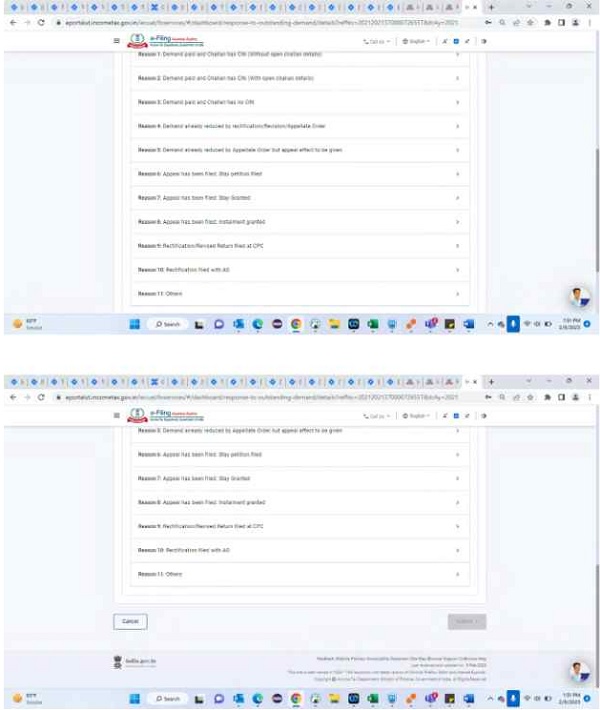

12. Taxpayer will be required to provide the reasons for disagreement, by clicking the button “+Add reasons”.

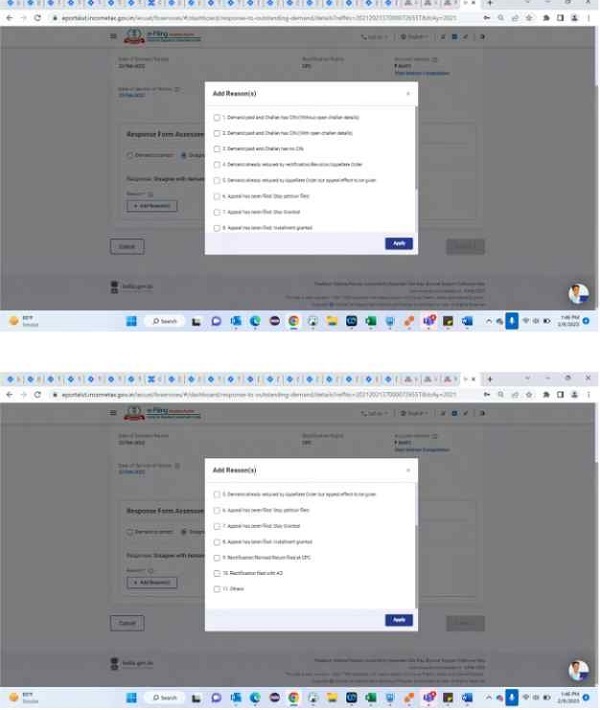

13. Taxpayer can select the appropriate reason out of the 11 reasons provided.

14. Taxpayer can select muitipe reasons, if more than one reason is applicable.

–

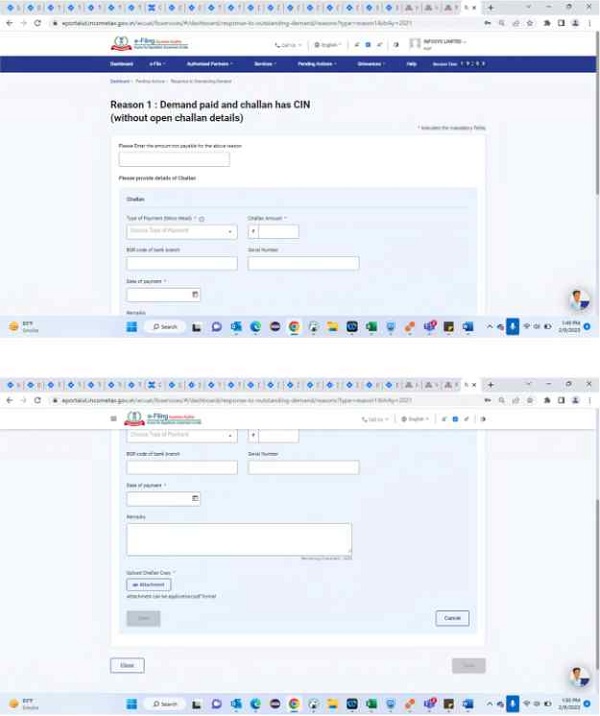

a. Reason 1: Details to be provided for challan with ON: “Minor head”, “Challan amount”, “BSR Code”, “SI No”, and “date of payment”. In addition, the amount that is not payable is required to be entered. Further, remarks of taxpayer can be provided in the box provided. Copy of the challan needs to be uploaded in pdf format.

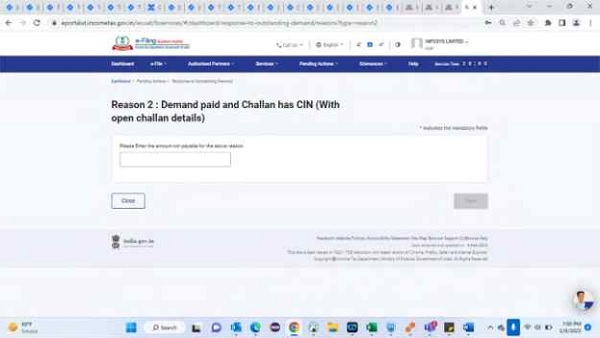

b. Reason 2: Demand paid and Challan has CIN.

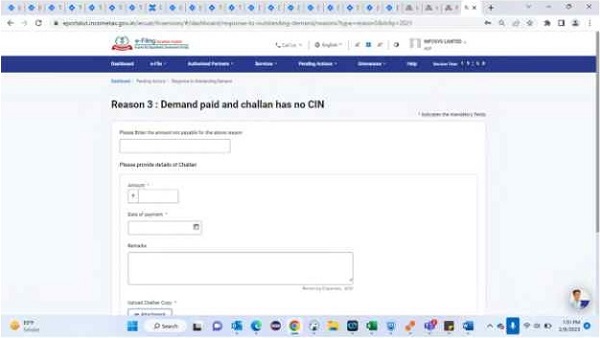

c. Reason 3: Details to be provided for challan without CIN: “Challan amount’, and “date of payment”. in addition, the amount that is not payable is required to be entered. Further, remarks of taxpayer can be provided in the box provided. Copy of the challan needs to be uploaded In pdf format. This option is meant only for the old AYs, where ON was not available.

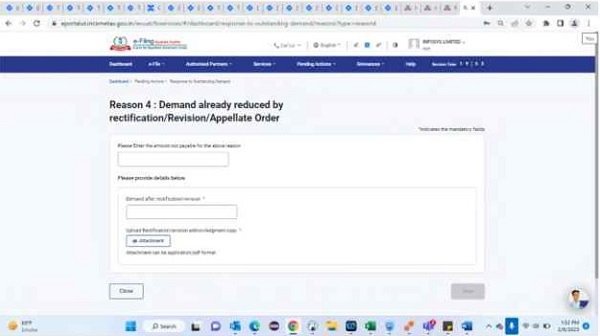

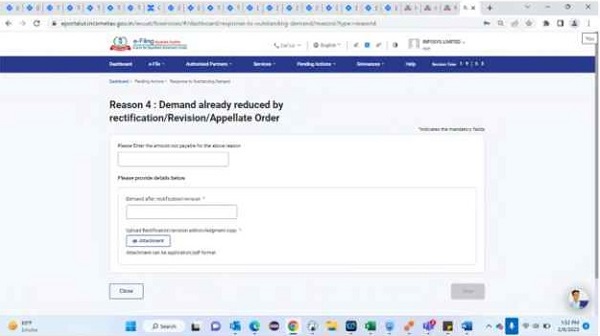

d. Reason 4: Demand already reduced by rectification/revision/Appellate Order: Details to be provided is the amount that is not payable. Further, remarks of taxpayer can be provided in the box provided. Copy of the relevant order needs to be uploaded in pdf format.

e. Reason 5: Demand already reduced by Appellate Order, but appeal effect not given: Details to be provided is the amount that is not payable. The authority passing the appellate order is required to be chosen, and the date of order needs to be entered. Further, remarks of taxpayer can be provided. copy of the order needs to be uploaded in pdf format.

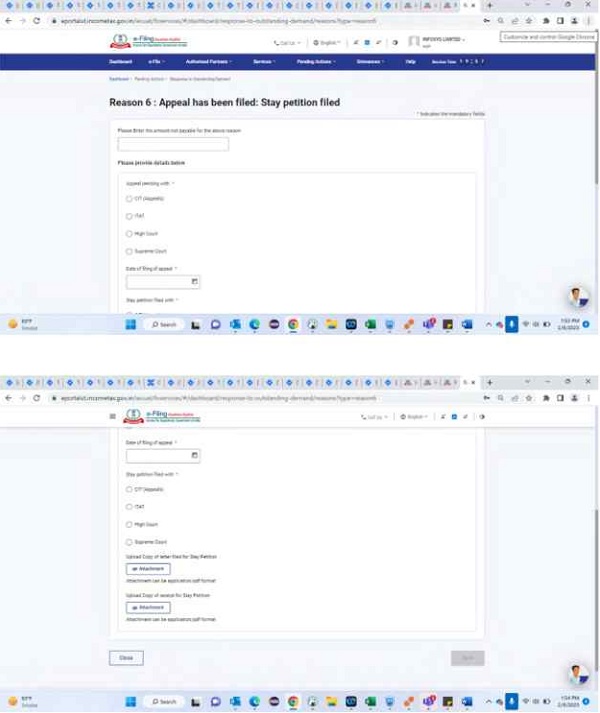

f. Reason 6: Appeal has been filed: Stay petition filed: The authority before whom the appeal is filed required to be chosen. In addition, copy of the stay petition filed and the copy of the stay order, (if stay has been granted) needs to be uploaded in pdf format. In addition, details to be provided is the amount that is not payable.

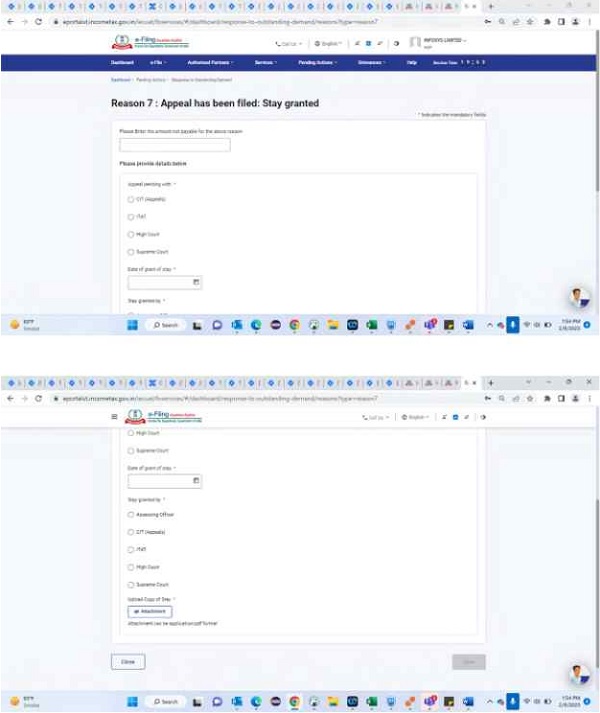

g. Reason 7: Appeal has been filed: Stay granted: The authority before whom the appeal is filed required to be chosen. In addition, the authority granting the stay needs to selected and copy of the stay petition filed and the copy of the stay order, needs to be uploaded in pdf formats. In addition, details to be provided is the amount that is not payable.

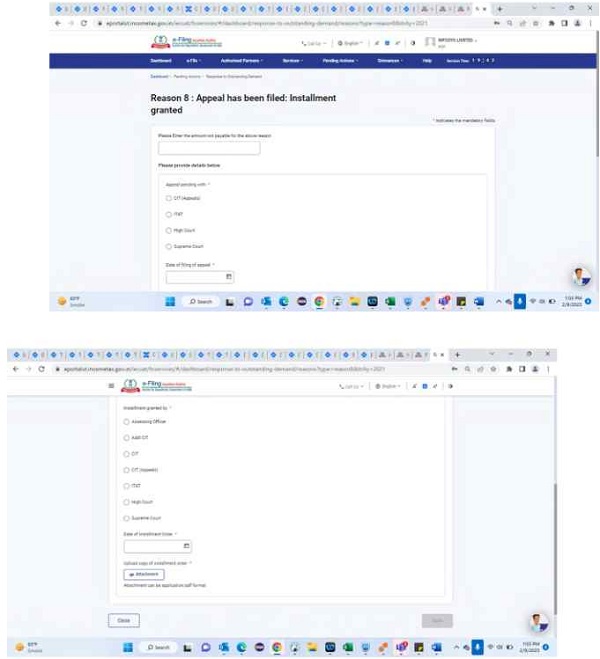

h. Reason 8: Appeal has been filed: Installment granted: The authority before whom the appeal filed is required to be chosen. In addition, the authority granting Installment needs to selected, date of installment order needs to entered and copy of the order granting Installment needs to be uploaded in pdf format. In addition, details to be provided is the amount that is not payable.

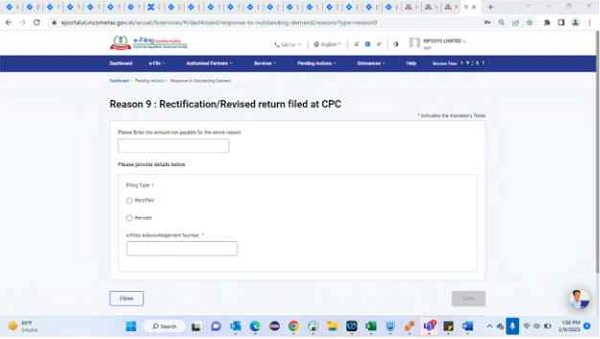

i. Reason 9: Rectification/ Revised return filed at CPC: Details to be provided is the amount that is not payable.. In addition, whether the revised return has been filed or rectification has been sought needs to be entered, alongwith the acknowledgement number.

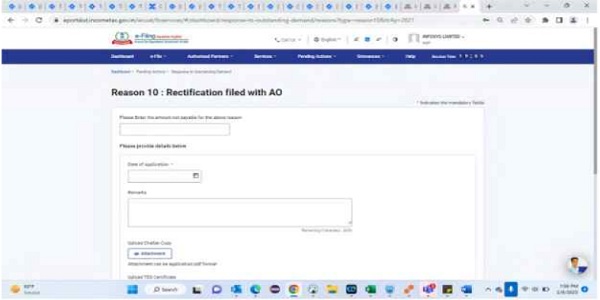

j. Reason 10: Rectification filed with AO: Details to be provided is the amount that is not payable. In addition, date of application needs to be entered and remarks to be entered. Upload facility has been provided to upload copies of challan, TDS certificate, Application, indemnity bond etc.

–

–

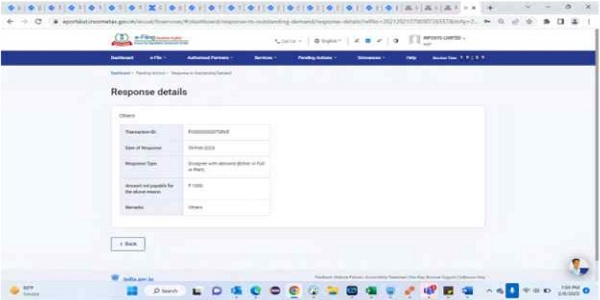

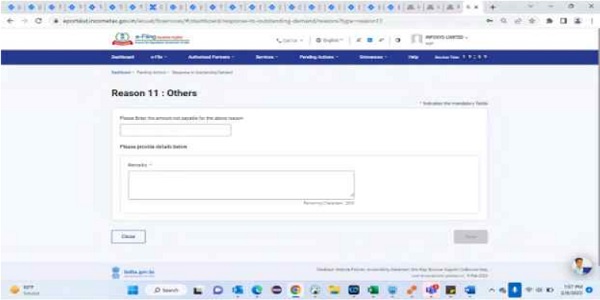

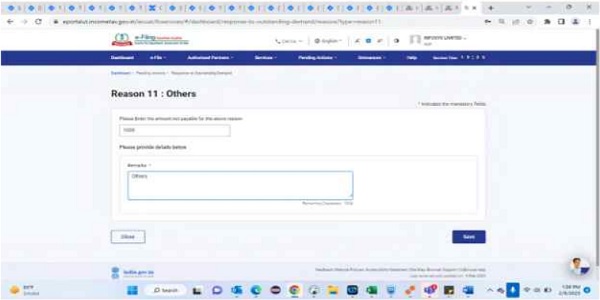

k. Reason 11: Others: Any other reason can be furnished along with amount that is not payable and remarks of the taxpayer.

–

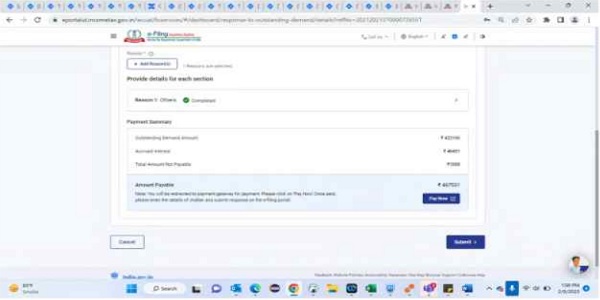

15. Once the details are entered, same is required to be submitted, and confirmed. Once confirmed, the transaction id will be provided to the assessee.

–

–

–

–

16. The Taxpayer can click on “View” to View the response submitted.