Instruction No. 07/2017

Government of India

Ministry of Finance, Department of Revenue

Central Board of Direct Taxes

Audit & Public Accounts Committee Division

F. No.240/08/2015—A& PAC – II

Dated 21/07/ 2017

Sub – Instruction laying down Standard Operating Procedure to handle Receipt / Revenue Audit Objections-Regarding

1. Introduction

1.1 The Instruction No 9 of 2006 dated 7/11/2006 as supplemented by Instruction No 16 of 2013 deal with revenue / receipt audit. In spite of a comprehensive instruction with well-defined role & responsibilities of various authorities, the pendency of outstanding objections has not abated. Further, indiscriminate remedial measures result in frivolous litigations causing undue hardship to tax payers. The Board has reviewed entire workflow to handle receipt audit observations with twin objectives of quick conclusion of remedial action in cases of accepted audit objections & to avoid remedial action as precautionary measure where observations are not acceptable.

1.2 With the launching of Income-tax Business Application (ITBA), the work flow would be monitored by supervisory authorities on system. This would instill accountability at every level in field formation. The perpetual problem of reconciliation of pendency will be resolved with launching of a web-based portal by the office of the C&AG “osparas.ap.nic.in” where CIT-wise / AO wise pendency have been hosted. The portal has the facility for uploading of reply by the CIT concerned. In due course of time, the interface of ITBA would also be linked with C&AG’s new portal for complete work flow automation.

1.3 With the technological assistance of ITBA and CAG portal in place, Standard Operating Procedure (SOP) have been aligned to workflow in ITBA, with defined roles and responsibilities of each functionary in the hierarchy. The timelines for each step to be executed by officer concerned has been laid down hereunder.

1.4 In supersession of all existing instructions on this subject in general and instruction No 9 of 2006, Instruction No 16 of 2013 and Circular No 8/2016 in particular, this instruction is issued for strict compliance by all concerned.

2. Audit Procedure followed by CAG office

2.1 The field offices of CAG (Comptroller and Auditor General of India) carry out normal audit of assessments which is referred to as ‘compliance audit’. Further, audit of non-assessment areas including, inter alia, expenditure is also covered in compliance audit to review the compliance of various instructions/directions of CBDT. It also undertakes study of systemic issues like implementation of any provision or functioning of any segment of the department called ‘performance audit‘ to see that the objectives are being achieved.

2.2 The audit team called Local Audit Party (LAP) visit different assessment units for the purpose of compliance audit. The LAP initially conducts what is called ‘Entry Conference’ wherein audit methodology is explained and AO’s co-operation is sought in furnishing statistical data, records and replies to pending observations of earlier cycle etc. The mistake detected by LAP in the audit process is intimated to the AO in the form of an Audit Memo (normally called Half Margin Note) and his initial response to the query is sought. After the audit of the circle / ward is over, there is Exit Conference of LAP with AO in which summary of audit conducted is discussed, AO’s confirmation is sought to the effect that points included in audit mistakes were not pointed out by IAP/SAP and no other action (issue of notice u/s 148 or 154) was taken before the issue of Audit Query. It is also confirmed that the interim replies to the audit queries given by AO have been incorporated in the audit report.

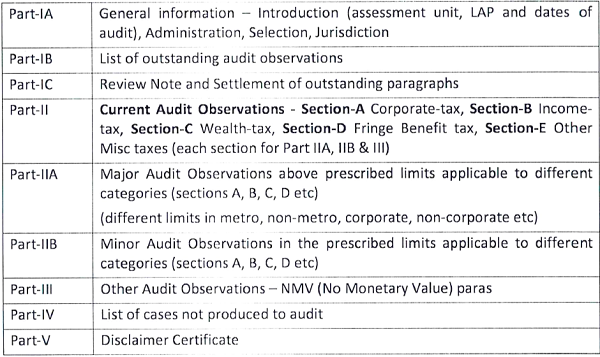

2.3 Within about a month of close of audit, a Local Audit Report (LAR) is forwarded to the PCIT concerned containing audit observations in respect of errors noticed. The LAR has various parts as under:

2.4 The objections are settled after considering the replies sent by the PCIT. The C&AG prepares an Audit Report in respect of Direct Tax which contains illustrative cases to support their conclusion regarding loss of Revenue due to mistake in making assessments. These illustrative cases are taken from Local Audit Reports based on quantum of loss of revenue, even if objections are not accepted by the department.

2.5 As a first step towards conversion of audit objection to “Draft Para”, the Director (ITRA) sends particulars of objections to the PCIT through a ‘Statement of Fact’ (SOF). The SOF to make Draft Para can be proposed even in cases where objection has been settled after completion of remedial action. After incorporating the response, if any, from the PCIT to the SOF, illustrations selected for inclusion in the Audit Report are sent to the Board for comment. On receipt of Draft Paras from the office of the C&AG, the A&J division of the Board, calls for report from the PCIT in Proforma A & B to prepare its response to the Audit Report.

2.6 The Audit Report of CAG for each financial year is presented to the Parliament which is examined by Public Accounts Committee. The response of CBDT is also presented before the PAC.

3. Audit program and Case Records:

3.1 The PCIT shall inform the program of compliance audit by the Local Audit Party, which is intimated to him about a month in advance, to the CIT(Audit) to ensure that the Internal Audit of those assessment units is carried out on priority.

3.2 At the beginning of audit cycle, the Assessing officer shall request the LAP to furnish Audit Memo on daily basis as soon as the mistake is observed rather than handing over all such notes on the last day of audit period. The AO shall supply the assessment and other records as required by LAP expeditiously keeping proper records.

3.3 If it is not possible to make available any particular record requisitioned, the Assessing officer shall communicate the reasons therefor to the LAP in writing with the prior approval of the PCIT concerned. Such record shall be invariably produced at the next audit cycle.

Standard Operating Procedure (SOP) for handling objections

4. Half Margin Note stage

4.1 After audit of a particular record, the Local Audit party generally issues Audit Memo (Half Margin Note) on any irregularity or mistake observed in individual cases. The Assessing officer shall categorize the objection raised as (i) factual mistake or (ii) legal question, or (iii) mixed issue, if the objection is not already so categorized by the LAP. Thereafter the AO should reply to the Half Margin Note (HMN), in all cases in the manner as discussed below.

4.2 On receipt of half margin note from audit party, in case of factual objection,

(i) if mistake pointed out by the audit is found to be correct, the AO shall initiate / take appropriate remedial action, within 5 days, and inform the LAP accordingly.

(ii) if facts in objection are not found correct, the AO shall give reply to the audit specifying correct facts.

4.3 In case of legal question or mixed issue(s), the AO shall specify as to whether or not, the factual aspect of the objection is correct and convey the correct facts relating to the factual issue(s) to the LAP. For the legal question raised as such or in a mixed issue, the Assessing officer may state that the reply would follow after due examination of the matter.

4.4 The Assessing officer shall send a status report to the PCIT as regards mistakes involving legal question / mixed issue so that a view may be prepared for response on receipt of LAR.

5. Local Audit Report (LAR) stage

5.1 The Local Audit Report (LAR) is sent by the Group Officer concerned, dealing with audit of Direct taxes in the office of Director General of Audit or Principal Director of Audit (Central) [referred to as ‘concerned CAG officer’ in this Instruction] to the Assessing officer with a copy to PCIT and CIT(Audit). Until the time the process of receiving LAR on system begins, the Assessing officer shall enter all the objections in the LAR in ‘Revenue Audit’ Module of ITBA in the columns given at Annexure-1 to this instruction.

5.2 The PCIT shall, after calling for the report from AO and Range head, if needed, take a decision as to, whether or not, the objection is acceptable.

Action when objection is acceptable

5.3 Where the Revenue Audit objection is accepted, the PCIT shall decide if the relevant order under audit requires revision u/s 263 as remedial action. If yes, he shall call for the relevant records and proceed to initiate action u/s 263.

5.4 In other cases, the PCIT shall communicate his decision not to invoke section 263 to the Assessing Officer who shall examine the facts of each case and take a suitable action as per his independent application of mind on the facts of each case.

5.5 In case the Assessing Officer decides to choose section 154 as the appropriate remedial measure in 5.4 above, he shall initiate the action after approval of the Range head.

5.6 The remedial action in case of accepted audit objection shall be initiated within three months and shall be completed within further period of six months from initiation. The objection shall be treated as settled once the intimation of completion of remedial action and issue of demand notice is given to concerned CAG officer.

Process when Objection is not acceptable

5.7 Where the audit objection is not accepted, the PCIT shall send a reply to the concerned CAG officer specifying reasons for non-acceptance of objection within two months of receiving LAR. A copy of the reply shall also be marked to the CIT(Audit). Where the view of PCIT is accepted, the objection will be dropped and no further action would be required.

5.8 Where the view of PCIT is not accepted and a rejoinder is received from concerned CAG officer with reasons for disagreement, the PCIT shall first get the contents of rejoinder entered in ITBA system. He shall then reconsider the objection in the light of points raised in the CAG rejoinder. If PCIT agrees with the views of the ITRA, the procedure as in para 5.3 to 5.6 above shall follow.

5.9 Where the PCIT is still of the view that objection is not acceptable, he shall take up such cases of disagreement, in inter-departmental meeting with Director General of Audit or Principal Director of Audit (Central), along with cases where there is no response to PCIT’s replies from the CAG officer after lapse of two months.

5.10 The CIT(Audit) shall also be invited to the meeting and he shall play an active role for maintaining consistency of approach on a particular issue. In the meeting, efforts will be made to resolve the difference of opinion and arrive at common view, as far as possible. Detailed ‘Minutes of the Meeting’ shall be recorded and sent to all concerned. However no remedial action shall be initiated in respect of objections not accepted by PCIT even after discussion in meeting.

Unresolved cases:

5.11 Where a Revenue audit objection remains unresolved at field level, the PCIT shall enter in ITBA system, the outcome of meeting referred to in 5.9 above, as per minutes recorded. In such cases the ADG (Audit) shall be able to generate a summary of objection containing all information as in proforma at Annexure–2 of this Instruction in order to take up the matter in the headquarter office of C&AG.

5.12 The ADG(Audit), acting on behalf of CBDT, shall hold meeting with the Principal Director of Audit (Direct Taxes) in the Hq office of C&AG to discuss the objections remaining unresolved at field level. For this purpose, the ADG(Audit) may constitute a team of officers as deemed appropriate, including CIT(A&J), CBDT and officers from Directorate of L&R, so that the latest judicial position on a legal issue may be brought to the notice of officers of CAG during discussion. Minutes of the meeting may be recorded and sent to all concerned. However no remedial action shall be initiated if the objection raised by CAG is not found acceptable in the meeting.

6. Draft Para stage

6.1 Where Statement of Facts (SOF) proposing to include an objection as draft para in audit report is received, the PCIT shall examine the issue (irrespective of whether or not, the audit objection was accepted) from factual & legal perspective and send appropriate reply including present status of appeal etc, to the concerned CAG officer within a fortnight of the receipt thereof.

6.2 The PCIT shall upload particulars and the CCIT shall insert comments in ITBA system in revised Proforma-A, as prescribed at Annexure-3, in respect of each Draft Para, within 6 weeks from its receipt to enable the Board to submit reply to the C&AG of India. In case the draft para relates to an objection that has been accepted, report in Proforma-B as prescribed at Annexure-4, shall also be similarly uploaded. A copy of the report shall be marked to the ADG (Audit) for preparation of the Action Taken Note (ATN).

6.3 After the receipt of the Audit Report presented to the Parliament, the ADG (Audit) shall give concluding shape to the ATNs (Action Taken Notes) on Audit Paras, and send these to the Board, through the Pr.DGIT(Admn), for submission to the C&AG of India after necessary vetting and consideration in the Board.

7. Appeal to ITAT in cases involving audit objection

7.1 The adverse order of the first appellate authority in cases involving revenue audit objections should be carefully scrutinized by the PCIT. The appeal to ITAT shall be filed only if the appeal order is not acceptable on merits.

8. Registers to be maintained:

8.1 The record of entire audit work i.e. the LAR, all subsequent communications for its settlement etc with dates, shall be available in the ITBA system. The required information like pendency & settlement of major & minor revenue audit objections shall be available as MIS.

8.2 However, until the time Audit Module in ITBA system is fully functional, the registers in the format as prescribed in the existing Instruction shall continue to be maintained.

9. Reporting system:

9.1 All work including correspondence regarding revenue audit shall be done through ITBA system. The statistical and other reports, as may be required, shall be generated from the ITBA system itself. However for monitoring and control following standard MIS reports are prescribed:

(a) Statistical report, to ascertain progress, in respect of number of audit objections raised, settled, pending etc in the format given at Annexure-5.

(b) List of pending audit objections with particulars as may be required out of those prescribed in Annexure-6.

For Audit Set-up

9.2 The CIT(Audit) shall be able to generate MIS report in Annexure-4 for his jurisdiction or for each PCIT charge. The PCCIT shall be able to generate similar MIS report for his jurisdiction or CIT(Audit) wise, or CCIT wise or PCIT wise as may be required. The ADG(Audit) shall be able to generate similar MIS report for all or any of the PCCIT or CCIT or PCIT or any CIT(Audit) in India.

For CCIT or PCIT

9.3 The PCIT shall be able to generate, as and when required, MIS report in Annexure-4 for his charge with break-up for each Range or AO in his charge. The PCIT shall also be able to generate list of all pending audit objections in Annexure-5 for his charge or any Range or any AO in his charge.

9.4 The ADG(Audit) may, with the approval of Member(A&J), specify any other periodic

MIS that is required to be generated through ITBA.

9.5 Until such time as Audit Module in ITBA becomes functional, the reports as per

existing guidelines shall continue to be sent.

10. Monitoring by CCIT

10.1 PCCIT shall review the progress of settlement of revenue objections in the CCIT Regions under his administrative control on quarterly basis and take necessary steps to achieve Action Plan targets for the year in this regard. He shall submit a report within a fortnight of each quarterly review to the Member (A&J), CBDT.

11. Calling for Explanation of officers:

11.1 Where the Major Revenue Audit Objection has been accepted, the PCIT may call for explanation of Officer/staff concerned in appropriate cases, keeping in view the nature of objection and facts of the case, and take suitable action as deemed appropriate.

11.2 The PCIT may also call for explanation of the officers who delayed the process of remedial action beyond the time line laid down in this instruction and of those who failed to take remedial action in cases of accepted audit objection in time, causing irretrievable loss of revenue.

11.3 Where a Major Revenue Audit Objection has been accepted by the department in a case which was audited by the internal audit earlier and such objection was not pointed out by the Internal Audit Officer, the CIT (Audit) may call for explanation of such Internal Audit Officer in appropriate cases and may take suitable action as deemed fit.

11.4 Any officer / staff whose explanation has been called for as above shall furnish

explanation through ITBA system.

12. Ledger Cards

12.1 Proper maintenance of record of mistakes committed by a particular officer is an essential step to enforce accountability and take reformative steps. This is to be done by maintaining Ledger Cards. The ledger card in respect of erring assessing officers shall be maintained on the ITBA system and would be available to supervisory officers.

12.2 However, until the time Audit Module in ITBA system is fully functional, the ledger card will continue to be maintained in the offices of the PCIT concerned as well as the CIT(Audit) in the format as in existence prior to this Instruction coming into force.

13. The ADG (Audit)

13.1 ADG (Audit) shall act as the coordinating agency for the various CsIT (Audit) to promote uniformity of view on same issue.

13.2 He shall monitor progress of settlement of objections both internal and revenue.

13.3 The ADG (Audit) shall try to reconcile the view of department and CAG in cases remaining unresolved at field level so that the number of draft paras may be minimized.

14. The above instructions would apply mutatis mutandis to the Revenue Audit’s observations in cases covered in Performance Review so far as taking of remedial action, accountability measures and necessary action against the officer / staff responsible for the mistake is concerned.

15. When the Audit Module of ITBA becomes functional, entire work flow of audit, including all correspondence, shall be through ITBA system. The correspondence with C&AG official, if received in physical form, shall be entered in the system by the authority

16. These instructions may be brought to the knowledge of all concerned for strict

This issues with the approval of the Board.

Hindi version of the Instruction will follow.

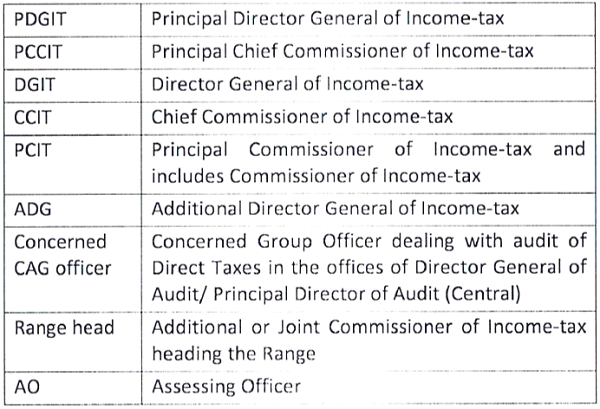

Abbreviations used in this Instruction

(Sunita Verma)

Addl. CIT (OSD) A&PAC,

CBDT, New Delhi.