Deepak Kumar

♦ INTRODUCTION:

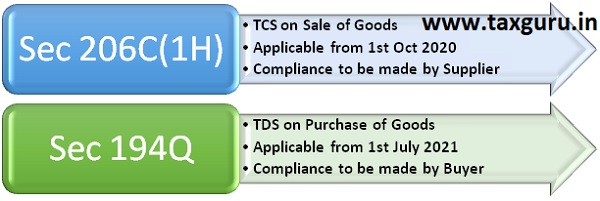

Government in year 2020 has made important change in TCS provisions by making it applicable on Goods sector at large scale. Vide Finance Act 2020, Section 206C was amended by inserting new sub section (1H) to allow government to collect TCS on Sale of Goods. This provision has been made effective from 1st October, 2020. It is interesting here to note that, in spite of Covid challenge, said provision has got implemented and there was no extension for it. As per said provisions, supplier is required to collect and pay tax at 0.10% to government on amount received from customer. There are some conditions for application of this provisions. It was first attempt to include Goods sector at large scale under TCS provisions.

Till date, TDS provisions were applicable primarily on receipt of Services. However, in order to increase scope of TDS provisions on Goods sector, the Government has introduced new Section 194Q (TDS on Purchase of Goods) in the Finance Act 2021 which is going to be applicable from 1st July, 2021. As per said provisions, now TDS is required to be deducted at 0.10% on purchase of goods, if conditions are satisfied.

As many taxpayer are still facing difficulties in complying with provisions of section 206C(1H), insertion of new section 194Q has created lots of confusion among Professionals and Trade as to which section to be complied with.

In this article we have tried to analyse applicability of both the provisions and which provision should be applied

- Legal Provision – Section 206C(1H) and Sec 194Q

- Interplay / Comparison of Both the Sections.

- Example on Applicability and Calculation for Better Understanding

- Standard Operating Procedure to be followed by Accountant/Finance person for compliance of TDS/TCS

- Some Important FAQs.

♦ LEGAL PROVISIONS – SEC 206C (1H) AND SEC 194Q:

- Section 206C (1H) TCS on Sale of Goods:

Every person, being a seller, who receives any amount as consideration for sale of any goods of the value or aggregate of such value exceeding fifty lakh rupees in any previous year, other than the goods being exported out of India or goods covered in sub-section (1) or sub-section (1F) or sub-section (1G) shall, at the time of receipt of such amount, collect from the buyer, a sum equal to 0.1%. Of the sale consideration exceeding fifty lakh rupees as income-tax.

“Seller” means

- A person whose total sales, gross receipts or turnover from the business carried on by him exceed ten crore rupees during the financial year immediately preceding the financial year in which the sale of goods is carried out.

- Not being a person as the Central Government may, by notification in the Official Gazette, specify for this purpose, subject to such conditions as may be specified therein.

- Section 194Q TDS on Purchase of Goods:

Any person, being a buyer who is responsible for paying any sum to any resident (hereafter in this section referred to as the seller) for purchase of any goods of the value or aggregate of such value exceeding fifty lakh rupees in any previous year, shall,

- at the time of credit of such sum to the account of the seller or

- at the time of payment thereof by any mode,

Whichever is earlier,

Deduct an amount equal to 0.1% of such sum exceeding fifty lakh rupees as income-tax.

“Buyer” means a person

- whose total sales, gross receipts or turnover from the business carried on by him exceed ten crore rupees during the financial year immediately preceding the financial year in which the purchase of goods is carried out,

- Not being a person, as the Central Government may, by notification in the Official Gazette, specify for this purpose, subject to such conditions as may be specified therein.

♦ INTERPLAY/COMPARISON OF SECTION 194Q AND SEC 206C (1H)

| PARTICULARS | DETAILS OF SEC 194Q | DETAILS OF SEC 206C(1H) |

| Who is Liable to deduct TDS or collect TCS? | ‘Buyer’

Whose total sales, gross receipts or turnover from the business exceeds Rs. 10 Crores during the financial year immediately preceding the financial year in which such goods are purchased. |

‘Seller’

Whose total sales, gross receipts or turnover from the business exceeds Rs. 10 Crores during the financial year immediately preceding the financial year in which the sale of goods is carried out. |

| Applicable From | With effect from 1st July, 2021 | Already in motion i.e., from 1st Oct, 2020. |

| When is it Applicable? | Buyer Purchases goods from a resident person and the purchase/payment is of value or aggregate of such value exceeding 50 Lakh rupees in any previous year. | Seller receives consideration for sale of any goods from the Buyer (other than goods exported out of India) of the value or aggregate of such value exceeding 50 Lakh rupees in any previous year. |

| When to Deduct/ Collect Tax? | At the time of entry in the books of account of buyer or at the time of payment thereof by any mode, whichever is earlier | At the time of receipt of such amount. |

| Applicable Rate | 0.1% of purchase/payment exceeding 50 Lakh rupees If the deductee (i.e., seller) has not provided the Permanent Account Number to the deductor (i.e., buyer) then at the rate of 5%. | 0.1% of the sale consideration exceeding 50 Lakh rupees If the collectee (i.e., buyer) has not provided the Permanent Account Number or the Aadhaar number to the collector (i.e., seller) then at the rate of 1%. |

| What if Both the Sections “194Q and 206C(1H)” are Applicable to the same transaction? | Then Sec 194Q will prevail and Tax shall be deducted under Section 194Q only. | In this case, since the Buyer is liable to Deduct Tax (194Q) on the goods purchased from the Seller, section 206C (1H) shall not apply. |

| Cases when respective sections will not be applicable | (a)Tax is deductible under any of the provisions of this Act; and

(b)Tax is collectible under the provisions of section 206C other than a transaction to which sub-section (1H) of section 206C applies.’ (c) Payment of any sum other than to resident from whom such goods are purchased |

(a) Receipts of Consideration of goods being exported out of India or

(b) Goods which are covered under 206C(1) such as Tendu leaves, Timber, Scrap, etc or (c) Goods like Motor Vehicles covered under section 206C(1F) or (d) Goods covered under section 206C (1G) where money is received by authorized dealer for remittance. (e) The buyer is liable to deduct tax at source under any other provision of this Act on the goods purchased by him from the seller and has deducted such amount. |

| Date from which Threshold limit of Rs.50 Lakhs is to be considered. | The limit shall be computed from the start of the Financial Year i.e., from 01/04/2021 (For FY 2021-22). If the limit crosses before 01/07/2021 then from the next transaction i.e., after 01/07/2021 itself TDS shall be computed and deducted on all the transactions after 01/07/2021. | For FY 2021-22 threshold limit of 50 Lakhs shall be computed from 01-04-2021 and TCS shall be applicable as and when consideration received crosses 50 Lakhs (including any previous dues/advance received) |

♦ EXAMPLE ON APPLICABILITY AND CALCULATION FOR BETTER UNDERSTANDING:

(Amounts in CRORE)

| Particulars | Scenario 1 | Scenario 2 | Scenario 3 |

| Turnover of Seller – XYZ (In cr.) | 15 | 8 | 15 |

| Turnover of Buyer -ABC (In cr.) | 8 | 15 | 15 |

| Sale of Goods/Purchase of Goods (In cr.) | 2 | 2 | 2 |

| Sale Consideration Receipts/Payment during the year (In cr.) | 1 | 1 | 1 |

| Who is Liable to Deduct/Collect Tax? | Seller XYZ under section ‘206C(1H)’ | Buyer ABC under section ’194Q’ | Buyer ABC under section ’194Q’ |

| Rate of Tax | 0.1% | 0.1% | 0.1% |

| Amount on which Tax to be Deducted/Collected (In cr.) | 0.5 (1-0.5) | 1.5 (2-0.5) | 1.5 (2-0.5) |

| Tax to be Deducted/Collected | 5000 Rs. | 15,000 Rs. | 15,000 Rs. |

♦ SOP – STANDARD OPERATING PROCEDURES TO BE FOLLOWED FOR APPLICABILITY OF TDS/TCS ON PURCHASE/SALE OF GOODS

a) If Buyer’s turnover is more than Rs 10 crore in previous financial year, then Buyer will be required to deduct tax under sec 194 Q. [ In such case, seller is not required to collect tax under Sec 206C(1H)]

b) Buyer shall communicate to the seller, by preparing ‘declaration letter’, on its letterhead stating that the buyer is liable to deduct Tax under section 194Q, and that the seller need not collect TCS under Sec 206C(1H). This communication will reduce the confusion as to who shall comply with the provisions. The buyer shall at the time of placing an order through Purchase Order shall again choose to communicate to the seller that the buyer is liable to deduct Tax and that the Seller need not collect Tax.

(Refer Annexure Aenclosed below – for Draft “Declaration Letter” to be sent by Buyer to Seller if his turnover is more than Rs 10 Crore)

c) As there might be confusion as to who shall comply with the provisions, the seller shall also communicate with the buyer, through “confirmation letter” asking whether the buyer is liable to deduct tax under section 194Q, if the buyer’s response is positive (i.e., he is liable to deduct tax) then the seller shall not collect tax and if the reply is negative then the seller shall collect tax accordingly.

(Refer Annexure B enclosed below – for Draft “Declaration Letter” to be sent by Seller to Buyer if his turnover is more than Rs 10 Crore)

| ANNEXURE A

DECLARATION LETTER (Draft “Declaration Letter” to be sent by Buyer to Seller if his turnover is more than Rs 10 Crore To be printed on the letter head of the Buyer, who is liable to Deduct TDS under section 194Q) Date: To, Name and Address of Supplier (From whom goods are bought/might be bought more than Rs 50 lakhs) Subject: Declaration of applicability of TDS under Sec 194Q on purchases made from you. Dear Sir/Madam, We ——————-( Name)……………(address)………. having PAN_________, hereby inform you that Our total sales, gross receipts or turnover from the business exceeded Rs. 10 Crores during the FY 2020-21 and therefore we are liable to deduct Tax as per the new section 194Q on purchases made by us from you. This provision is applicable from 1st day of July 2021. Accordingly, you are requested not to collect Tax under section 206C(1H). For ————————– Authorised Signatory |

–

| ANNEXURE B

CONFIRMATION LETTER ( Draft “Confirmation Letter” to be sent by Seller to Buyer if his turnover is more than Rs 10 Crore. To be printed on the letter head of the seller, Who is liable to collect TCS under section Sec 206C(1H) ) To, Name and Address of Buyer (To whom goods are sold/might be sold more than Rs 50 lakhs) Subject: Confirmation requested from you on applicability of TDS under Sec 194Q to you, else we will be collecting TCS on Sale made to you Dear Sir/Madam, As per the newly inserted section 194Q of Income Tax Act 1961, Buyer (who is satisfying the conditions of said provision) is liable to deduct TDS. At the same time, on supply made by us to you, we are also required to collect Tax under Sec 206C(1H). However at the same time, there cannot be two tax on same transaction. Therefore we ——————-( Name)……………(address)………. having PAN _________, hereby request for your confirmation, that whether you are liable to deduct TDS u/s Section 194Q or not, on purchases made by you from us. Please choose from the below options and let us know. a) We confirm that we are liable to deduct TDS, on purchase made by us, from you, u/s 194Q. b) We confirm that we are not liable to deduct TDS on purchase made by us from you, u/s 194Q. Please note that, If we don’t receive your reply within one week, then our accounts department will collect TCS u/s 206(1H). For ————————– Authorised Signatory |

♦ IMPORTANT FAQ’S:

Q.1 Is a buyer importing goods from outside India required to deduct TDS under this section?

Ans. The obligation to deduct tax under this provision arises only when the payment is made to a resident seller. As in the case of import, the seller is a non-resident, the buyer will not have any obligation to deduct tax under this provision. However, the TDS under Section 195 may be required in respect of such transaction.

Q.2 Whether tax to be deducted on the purchase of goods by one branch from another?

Ans. The TDS under this section is required to be deducted by any person, being a buyer, responsible for making payment to the seller for the purchase of goods. Thus, the existence of two distinct parties as ‘seller’ and ‘buyer’ is a pre-requisite to construe a transaction as a purchase. The condition of purchase is not fulfilled in the context of branch transfer. Therefore, the provisions of this section shall not apply in the case of branch transfers.

Q.3 Which Return form to furnish TDS/TCS?

Ans. Statement of TDS deducted shall be furnished quarterly in Form 26Q.

Statement of TCS collected shall be furnished quarterly in Form 27EQ.

CONCLUSION:

As explained above, sometimes, TDS and TCS on Goods may have overriding effect and there seems to be chances of errors because of confusions in the minds of the Buyer or Seller. It may be that everyone tries to comply his part of legal obligation as a part of his safety. Therefore, it is important that taxpayer should ensure to have proper understanding and clarity about compliances of both the sections in order to avoid errors.It is highly recommended that, Taxpayer if his turnover is more than Rs 10 crore, he should send “Declaration Letter” as per Annexure A, to all his supplier from whom purchase is more than Rs 50 lakhs. And also should send “Confirmation Letter” as per Annexure B, where sale to any of customer is more than Rs 50 lakhs.

We thanks to Shri Santosh Sharma for vetting this article and for valuable contribution.

(Disclaimer – The contents of this document are solely for information purpose. It does not constitute professional advice or a formal recommendation. The presentation is made with utmost professional caution but in no manner guarantees the content for use by any person. It is professional advice or a formal recommendation. It is suggested to go through original statute/notification/circular/pronouncements before relying on the matter given)

My question is the threshold limit of 50lac exclude the gst or include the gst. On what amount should I deduct the tds u/s 194Q??

Is this section applicable to Local Authority as a deductor or not?

In the definition of Person as per Section 2(31) of Income Tax Act, person includes “Local Authority”. So this section 194Q is applicable to Local Authority, they have not been exempted so far by any notification hence they are liable if they satisfy the conditions of Section 194Q.

Is this section applicable to Local Authority as a deductor or not??