Analysis of The Supreme Court Judgments on Permanent Establishment of Morgan Stanley & Co. INC and Formula One World Championship Ltd.

Introduction

The general principle of taxation is that a person, who is resident of a country, would normally be taxable on his/its global income. However, as a rule of exception to this general principle, a person may also be taxed in the country of source i.e., the place where the business of a person is carried on, though he may be a resident of another country.

Section 5 of the Income-tax Act, 1961 (‘the Act’) states that a non-resident shall be liable to pay income-tax only on the income, that is received or deemed to be received in India, or that accrues or arises or is deemed to accrue or arise in India. Section 9(1)(i) of the Act inter alia states that income shall be deemed to accrue or arise in India if it accrues or arises, whether directly or indirectly, through or from any ‘business connection’ in India.

However, in treaty-based international tax law, the term Permanent Establishment (PE) is a widely used concept, to determine the right of the source country, i.e., to tax the profits of a non-resident from a business carried on by such person in the source country. Nevertheless, the PE shall be liable to be taxed in the source country only to the extent of its business profits which are attributable to such PE.

Article 5 of both the “Organisation for Economic Co-operation and Development (OECD) Model Tax Convention” and the “United Nations Model Double Taxation Convention between Developed and Developing Countries (UN Model)” defines the term PE, and this definition has been adopted by countries globally in their tax treaties. The main purpose of tax treaties is to encourage international trade and commerce by avoiding double taxation, eliminating tax avoidance and providing certainty by clearly delineating the taxing rights of each jurisdiction.

Recent developments indicate that the interpretation of Article 5 (the PE article) of a treaty by each country would be with the intention of keenly trying to protect one’s tax base. A recent move to digitalised economy has created broader challenges in the international tax regime, wherein it becomes virtually difficult to determine the existence of a PE based on the traditional approach. To address this challenge, the OECD on 5th October, 2015, as part of the OECD/G20 Base Erosion and Profit Shifting (BEPS) Project published its final report on Action Plan 7 “Preventing the artificial avoidance of permanent establishment status” (BEPS Report). Action Plan 7 contains changes to the definition of PE to prevent its artificial circumvention, e.g., such as arrangements through which taxpayers replace subsidiaries that traditionally acted as distributors, by commissionnaire arrangements, with a resulting shift of profits out of the country from where the sales took place, without a substantive change in the functions performed in that country.

Action Plan 15 provides an analysis of legal issues related to the development of a multilateral instrument (MLI) to enable countries to streamline the implementation of the BEPS treaty measures. In November 2016, more than 100 countries had concluded the negotiation and finalised the text of the MLI. The MLI helps countries to fight against the multinational companies who indulge in activity that result in BEPS; by implementing the tax-related measures developed through the BEPS Project, in existing bilateral tax treaties in a synchronized and efficient manner. These measures inter alia will prevent the artificial avoidance of PE status. Further, to give effect to this underlying philosophy, Article 12 and Article 13 of the MLI deal with “Artificial Avoidance of Permanent Establishment Status through Commissionnaire Arrangements and Similar Strategies” and “Artificial Avoidance of Permanent Establishment Status through the Specific Activity Exemptions” respectively. The Government of India, on 6th June 2017, has provided the provisional list of expected reservations and notification pursuant to Article 28(7) and 29(4) of the MLI, and India has accepted certain provisions of Articles 12 and 13 of the MLI.

This Article examines the two landmark judgments of the Hon’ble Supreme Court (SC) on the subject matter of determination of PE in the case of Morgan Stanley & Co., US1 and Formula One World Championship Ltd2. The SC while deciding these cases has referred to international commentaries and international jurisprudence, with reference to how the term PE has evolved in international law.

MORGAN STANLEY & CO., INC

DIT International Taxation, Mumbai vs. Morgan Stanley & Co. INC (2007) 292 ITR 416

Facts of the case3

Morgan Stanley & Co. (‘MSCo’ or ‘taxpayer’) was incorporated in the United States. It was in the business of providing financial advisory services, corporate lending and securities underwriting services. MSCo was wholly owned subsidiary of Morgan Stanley, US. It was an investment bank and had a number of group companies in various parts of the world.

Morgan Stanley Advantage Services Private Limited (‘MSAS’) was incorporated and set up by the Morgan Stanley Group in India, to support the group members’ front office functions in their global operations.

Outsourcing support services

MSAS entered into an agreement with MSCo to provide various back office/ support services which broadly covered the functions such as equity and fixed income research, data processing, account reconciliations, IT enabled services, etc.

MSAS used the logo and brand name of Morgan Stanley. As per the agreement, MSCo provided MSAS with customer material, including hardware, intellectual property rights, software or data licenses, procurement and connectivity, etc. The products developed by MSAS were exclusive property of Morgan Stanley Group.

However, MSAS did not undertake important revenue generating functions of MSCo nor did it bear any significant market risk with respect to its transactions with MSCo. The interaction with clients was done entirely by the employees of MSCo.

Under the service agreement, the consideration paid to MSAS by MSCo for the services rendered would be the total cost and a mark-up of a certain percentage of the total cost.

Stewardship activities

MSCo, like any other customer, had undertaken certain stewardship and similar activities. These activities were like briefing MSAS on the standard of services expected, monitoring the overall outsourcing operations at MSAS, acquainting the staff on various aspects of the functions by conducting briefing sessions for effective transitioning of various functions and providing basic guidance. However, MSCo was not involved in day-to-day management or other specific services to or for MSAS. This was done for ensuring that MSAS achieved the overall global value benchmarks of the Morgan Stanley Group.

Employees on Secondment / Deputation

MSCo’s staff was also sent on deputation at the request of MSAS, for periods ranging between several months to a couple of years to work under its control and supervision. It was agreed that the staff would continue to be employed or engaged and their salaries and fees would be directly paid by the MSCo. MSAS reimbursed the compensation cost to the MSCo with no profit element.

The above facts are explained by way of a diagram:

Authority of Advance Ruling

Authority of Advance Ruling

A ruling was sought from the Authority of Advance Ruling (AAR) on the following questions:

1. Whether MSCo would be regarded as having a PE in India under Article 5 of India-USA Double Taxation Avoidance Agreement (DTAA), and specifically: a fixed place PE or an agency PE or a service PE?

2. Whether transactional net margin method (TNMM) was the most appropriate method to determine the ALP in respect of transactions between the MSCo and MSAS?

3. If the transactions between MSCo and MSAS were at arm’s length, can any further income be attributed to the PE, if any?

The AAR held as follows:

1. In order to constitute a ‘fixed place PE’, an enterprise must undertake business through a fixed place. Although MSAS was rendering services to MSCo, it could not be said that MSCo by utilizing such services, undertook business activities through MSAS premises. Therefore, MSCo did not have a fixed place PE in India. However, there were some noteworthy observations by the AAR, especially in the current landscape of dynamic developments in the off-shoring of business operations and processes which aim to take comparative advantage of costs, skill sets, knowledge, etc. The AAR noted that:

- The place of business of the MSAS was a fixed place of business,

- However, no business of MS & Co. was carried on through the place of business of MSAS,

- Hence, the germane condition of carrying on business through fixed place of business of MSAS, thus, Article 5(1) of the treaty was not attracted.

The AAR held that MSAS was not a dependent agent of MSCo and hence there was no ‘agency PE’ under Article 5(4) of the DTAA. However, AAR interestingly stated that MSAS being a captive service provider was wholly and exclusively dependent on MSCo and acts on behalf of MSCo / Morgan Stanley group and it thus did not have a status of an independent agent. The conditions of Para 3 of Article 5(4) of the DTAA were not met, that is, MSAS did not conclude contracts on behalf of MSCo, did not stock goods for MSCo nor delivered the same, nor did it secure orders for MSCo and therefore, MSAS was not a dependent agent and thus no Agency PE was constituted under Article 5(4) of the DTAA.

The employees of MSCo were deputed to India, including those performing stewardship functions. These employees were actively involved in key managerial activities of MSAS and hence, AAR held that MSAS would constitute a ‘service PE’ of MSCo in India under Article 5(2)(l) of the DTAA.

2. The question on appropriateness of transfer pricing methodology for determining the ALP and margin was not addressed, since it was considered by AAR as outside its purview and jurisdiction.

3. As long as MSAS, being the PE of MSCo in India, was remunerated for its services at arm’s length by MSCo and as long as all its actual income was brought to tax, no further income could be attributed to the ‘service PE’, i.e., in the hands of the PE of MSCo.

Questions before the Hon’ble Supreme Court

The Indian Revenue authorities, aggrieved by the ruling of the AAR, in May 2006 filed a special leave petition, with the Supreme Court under Article 136 of the Constitution of India, to which MS & Co. filed a cross-appeal. The main issues raised before the Hon’ble Supreme Court (SC) were;

1. Whether MS & Co. had a PE in India under the terms of Article 5 of the DTAA? and

2. If answer to (1) is yes, then whether the payment of arm’s length remuneration by MS & Co. to MSAS extinguishes MS & Co.s tax liability in India?

Key observations and decision of the Hon’ble Supreme Court

The SC closely examined the Indian tax authorities’ contention regarding the existence of a PE of MSCo in India, by virtue of the performance of outsourced activities by MSAS. The SC observed that to decide whether a PE was constituted, there must be a functional and factual analysis of each of the activities undertaken by MSAS. The SC notably observed that under Article 5(1) of the DTAA, a PE of a multinational enterprise would come into existence in India, only if a fixed place exists in India, through which the business of the multinational enterprise (MSCo) was wholly or partly carried on.

1. Whether MSCo had a PE in India

Fixed Place of business PE under Article 5(1) of the DTAA

In terms of Article 5(1) of the DTAA there exists a fixed place PE, when there is a fixed place through which the business of the enterprise has been carried on partly or wholly. It can be observed that a general definition of PE in the first part of Article 5(1) postulates the existence of fixed place of business whereas the second part of Article 5(1) postulates that the business should be carried on through such fixed place.

The SC noted that MSAS in India was engaged in supporting the front office functions in fixed income and equity research of MS & Co. and also in providing IT enabled services such as data processing support, technical services, and reconciliation of accounts.

Thus, it can be seen that only back office services had been outsourced by MSCo to MSAS in India. Further, the SC did not consider it necessary to examine the first part of Article 5(1) and directly looked at the second limb of Article 5(1), i.e., through which the business of the multinational enterprise (MSCo) was wholly or partly carried on.

The SC held that MSCo cannot be said to have a fixed place PE in India in terms of Article 5(1) of the DTAA in respect of the back office operations performed by MSAS, as the condition of carrying on of MSCo’s business through such fixed place was not satisfied.

This was based on the premise, that the back office functions carried out by MSAS, were in the nature of preparatory and auxiliary activities, and hence, such functions were covered in the negative list of activities as stated in Article 5(3) of the DTAA.

It can be observed that the SC had not analysed the first part of Article 5(1), i.e., whether MSCo had a ‘fixed place’ in India, through the off-shoring of various functions to MSAS. However, the AAR in its ruling had clearly stated that “the place of business of the MSAS is no doubt a fixed place.”

Thus, it can be presumed that the SC had examined, in detail, the nature of functions performed by MSAS for MSCo, negating the basic rule of Article 5 (PE test), only because there was an existence of a ‘fixed place’ of MSCo in India through MSAS. Otherwise, there would be no need for the SC to conclude that the activities of MSAS were ‘excepted activities’ under Article 5(3)(e) of the DTAA, and hence it was held that as regards its back office functions, MSAS would not constitute a fixed place PE under Article 5(1) of the DTAA.

The SC had gone beyond the traditional approach and observed and analysed the business activities conducted, that is, back office operations carried on by MSAS in India, to determine whether MSCo had a PE in India or not.

Another aspect of this decision that needs to be considered is the consequences; if MSAS had been carrying on front office operations instead of back office operations in India. The SC observed that in order to decide whether a PE stood constituted, one had to undertake a functional and factual analysis of each of the activities to be undertaken by the enterprise. The OECD commentaries have established criteria for a PE constituting business activity of being, a “core business activity”, as opposed to an “auxiliary or preparatory activity”. The decisive aspect for the commentaries is whether the activity forms an essential and significant part of the activity of the enterprise as a whole. All business activities which contribute to the business earnings of the enterprise are core business activities. Some activities, although undoubtedly parts of a business activity, are considered insignificant and are therefore specifically exempted under the modern tax treaties (the “negative list”).

The hypothesis for the proceeding discussion is that the “excepted activity test” looks both at the qualitative aspect, i.e., the nature of the activity (“essential”), and its relative importance (“significant”) to the whole enterprise, which is a quantitative aspect. Core business activities are those which increase the value of the enterprise, either as a going concern, or based on the asset value. In the present case, the SC held that back office operations of MSAS were preparatory and auxiliary in nature which falls under Article 5(3)(e) and therefore, the same would not give rise to a fixed place PE.

In contrast, the front office operations forms an essential and significant part of the activity of the enterprise as a whole which contribute to the business earnings of the enterprise and therefore, the same may be regarded as core business activities. If MSCo had outsourced some of its main business functions to MSAS which are substantive business functions and cannot be termed as mere auxiliary and ancillary business functions, thanin such a case it could constitute core business functions falling under the ambit of Article 5(1) of the DTAA, in terms of the SC ruling, and this could lead to the determination of a PE.

However, the SC had given great importance to the factual and functional matrix, to determine a PE. Thus, it was this matrix which would be the determinant factor, and due to various nuances prevalent in the dynamic nature of the off-shoring business, it would be necessary to strike a note of caution, that it would be premature to cloak all such arrangements with the same hue, as there could be essential differing economic parameters which would have a great bearing, for example, third party service providers, etc.

Further, it also needs consideration that the inherent nature of the offshoring business, needs the link with the parent organisation for the business to survive. Hence, the operational model of the whole industry would be under risk, which would never be in the interests of the economy of such countries, that is, the service exporting nations. Thus, a balanced approach based on the analysis of the said factual matrix, coupled with anin-depth transfer pricing analysis is critical. The said approach would capture the real economic value contributed to the income earning capacity of the service recipient, by the service provider. This could be the basis to attribute equitably a fair compensation for the service exporting countries, and a just methodology, wherein each state would be able to collect its rightful share of taxes, and thus, could be the way forward.

Hence, according to the SC, MSCo was not carrying out any business activity in India. MSAS was rendering back office operations in India and such functions were considered as ‘preparatory and auxiliary’ in nature within the meaning of Article 5(3)(e) of the DTAA. Hence, no fixed place of business was constituted under Article 5(1) of the DTAA.

Agency PE under Article 5(4) of the DTAA

The SC further observed that MSAS had no authority to enter into or conclude contracts on behalf of MSCo and the contracts would be concluded only in US. The implementation of the contracts only to the extent of back office functions would be carried out in India and therefore, MSAS would not constitute an agency PE in India under Article 5(4) of the DTAA.

Service PE under Article 5(2)(l) of the DTAA

In the instant case, two activities were performed by employees of MSCo in India, i.e., stewardship activities and the work performed by the employees on deputation in India. There is no definition of stewardship activities given either in domestic tax law or DTAA except in the Transfer Pricing and Multinational Enterprises Report, 1979 (“1979 Report”). As per 1979 Report, stewardship activities cover a range of activities by a shareholder that may include the provision of services to other group members, for example services that would be provided by a co-ordinating centre.

The stewardship activities involved briefing of the MSAS staff to ensure that the output meets the requirements of MSCo. These activities included monitoring of the outsourcing operations at MSAS. The stewardship activities are rendered in order to protect the interest of the customers. A customer is entitled to protect its interest both in terms of confidentiality and in terms of quality control. Since, MSCo had worldwide operations; it was entitled to insist on quality control and confidentiality from the service provider. The stewards were neither involved in day to day management nor any specific services undertaken by the service provider. In such a case, it could not be said that MSCo had been rendering services to MSAS. Accordingly, the SC held that stewardship activities would not fall under Article 5(2)(l) of the DTAA and could not constitute a Service PE. Hence, on this aspect, the SC deferred with AAR’s decision and held in favour of MSCo.

Under Article 5(2)(l) of the DTAA, even a single day in which services are provided by employees of a non-resident enterprise to a related enterprise through a fixed place in India can constitute a PE. The SC observed that an employee of MSCo, when deputed to MSAS, does not become an employee of MSAS. The deputed employee had a lien on his employment with MSCo and as long as the lien remains with MSCo, the company may be considered to retain control over the deputed employee’s terms and employment. Thus, the deputed person cannot be considered as an employee of MSAS. The SC then found that when the activities of a multinational enterprise entail it being responsible for the work of deputed employees and the employees continue to be on the payroll of “the multinational enterprise or they continue to have their lien on their jobs with the multinational enterprise”, a service PE can emerge.

Further, the SC appears to have taken into consideration that the request/requisition for the deputation of employees with specialised skills, generally comes from MSAS. Furthermore, MSCo retains a degree of control and supervision over the employees to the extent they remain on MSCo’s payroll, and any disciplinary action against them may not be taken by MSAS without consultation with MSCo. The services were not for MSCo, but for and to MSAS. Since, the deputed employees remain employees of MSCo, and provide services to and for MSAS, a service PE is created under the terms of Article 5(2)(l) of the DTAA.

2. Attribution of Profits to a PE and Transfer Pricing

Article 7 of the OECD Model Convention and the UN Model state that a foreign enterprise is liable to tax in the source country on its business profits to the extent the profits are attributable to the PE in the source country. This provision specifies how such business profits should be ascertained, and states that a PE is to be treated as if it is an independent enterprise (profit centre) apart from the head office and which deals with the head office at arm’s length. Article 7(2) of the UN Model advocates the arm’s length approach for attribution of profits to a PE. Under Article 7(2), economic nexus is an important issue on the principle of profit attribution to a PE. Therefore, in the current case, the SC held that only the profits of MSCo that had an economic nexus with the PE in India was taxable in India.

The SC held that because the remuneration to MSAS was justified by a transfer pricing analysis, no further income could be attributed to the PE, i.e., where an associated enterprise that also constitutes a PE (in this case, MSAS) is remunerated on an arm’s length basis, taking into account all the risk-taking functions of the enterprise (PE), no further profit was attributable to the PE. However, where the transfer pricing analysis did not adequately reflect the functions performed and the risks borne by the enterprise, it would be necessary to further attribute profits to the PE for those functions/ risks that had not been considered. This determination would depend on the functional and factual analysis undertaken in each case. It was further held that the TNMM was the most appropriate method for determination of the arm’s length consideration of the transactions between MSCo and MSAS.

The above indicates that the tax liability of a non-resident entity is extinguished if an associated enterprise (that also constitutes a PE) is remunerated on an arm’s length basis, taking into account all the risk-taking functions of the enterprise (PE). As such, this decision will apply only in those cases where the PE is also constituted by the functioning of the associated enterprise and the associated enterprise is remunerated on an arm’s length basis after taking into account all the risk-taking functions of the PE, i.e., the functions performed and risks borne by the PE are appropriately captured by the associated enterprise.

Further, it seems that the SC had adopted an approach that was almost similar to the single-taxpayer approach for the attribution of profits which was in contrast to the authorised approach of the OECD; indeed the judgment leaves room for further profits to be attributed to a PE if the factual and functional analysis of the associated entity does not fully capture the functionality of the PE. The OECD Report on the Attribution of Profits to a permanent establishment provides that, for tax purposes, in the source country there are two taxpayers, namely the dependent agent (resident) and the dependent agent PE (non-resident). The functions carried out and the risks borne by these two are to be considered and compensated separately. In the source country, two separate tax returns must be filed, one for the dependent agent (resident) and one for the non-resident (PE). The OECD Report also suggests that the source country could have the right to tax the dependent agent PE even where the dependent agent has been compensated by an arm’s length consideration.

It seems clear that the Supreme Court dissented from the view expressed by the OECD Report that, the payment of arm’s length remuneration does not necessarily extinguish the tax liability of the non-resident in the host country.

However, an analysis of the decision of the Supreme Court reveals that the concession was granted with a caveat, that the associated enterprise should completely “capture the factual and functional analysis of the PE”; then and only then, the concession of the decision will apply.

Comments

The Supreme Court decision tends to bring out the various nuances emerging from constantly changing economic scenarios, where the rapid strides of information and telecommunication technology constantly challenge the traditional concept of interpreting the PE Article in a DTAA.

The factual and economic analysis of the business as a whole seems to be the essential methodology, both for interpreting the PE Article and the profits to be attributed to the PE. This would enable one to understand the economic substance of the transactions and would hence, help in attributing equitable economic profit to such economic substance.

It is also important to understand the nuances of the ‘arm’s length standard’, and not use it as an universal methodology, because when the arm’s length standard is applied in a transfer pricing scenario, its purpose is to test whether the related party transactions adhere to the arm’s length standard and are comparable to various comparable transactions. This has a more compliance flavour. However, when the same standard is applied in a PE scenario, the focus changes from a ‘testing/compliance standard’ to a ‘profit attribution standard’, and thus becomes a more exacting standard from the perspective of taxing the foreign enterprise’s income in the Source State. In such a scenario it would become important to attribute profit for the subtle differences in the economic profile of the PE as compared to the comparable companies. Thus, the economic analysis would indicate whether, the additional risks undertaking, functions performed or investments made by the PE need to be further compensated; it is these subtle differences which may require international consensus if the ‘arm’s length standard’ is to be globally acceptable in a PE scenario.

Formula One World Championship Limited vs. CIT, International Taxation – 3 Delhi (2017) 394 ITR 80

Facts of the case

Formula One Group and various Agreements

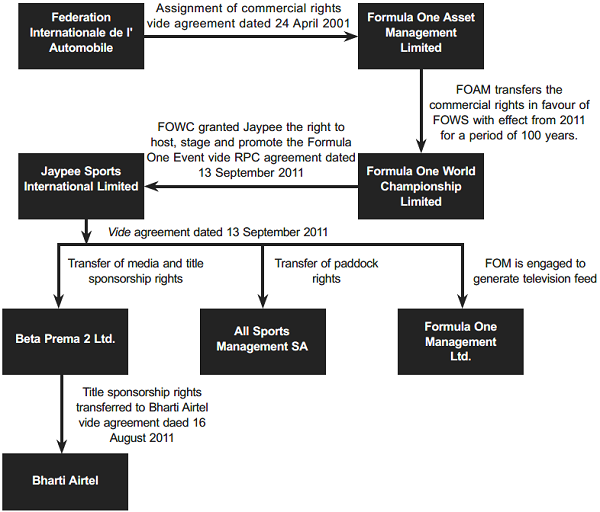

Federation Internationale de I’Automobile (FIA), a non-profit association, was established as the International Association of Recognized Automobile Clubs to represent the interests of motoring organizations and motor car users globally. FIA was a regulatory body; it regulated the FIA Formula One World Championship (Championship).

Formula One World Championship Limited (FOWC or taxpayer) was a company incorporated in UK on 7th March 2001 and a tax resident of UK.

FIA had assigned commercial rights in favour of Formula One Asset Management Limited (FOAM) vide agreement dated 24th April 2001, making FOAM the exclusive Commercial rights holder (CRH). On the same day, another agreement was signed between FOAM and FOWC vide which all these commercial rights were licensed to FOWC for 100 years with effect from 1st January 2011.

Formula One (F-1) refers to the rules and regulations that define the characteristics of the race, as opposed to any other form of motor race. About 12 to 15 teams typically compete in these Championships in any one annual racing season. The teams assemble and construct their vehicles, which comply with defined technical specifications, and engage drivers who can successfully manoeuvre the F-1 cars in the racing events.

All participating teams, known as ‘Constructors’, entered into a ‘Concorde Agreement’, with FOWC and the FIA in 2009. All the participating team bind themselves to an unequivocal negative covenant with FOWC that they would not participate in any other similar motor racing event nor would they promote in any manner any other rival event. Further, as per the Concorde Agreement, FOWC could exploit the commercial rights directly or only through its affiliates.

FOWC also signed the agreement with Jaypee Sports International Limited (Jaypee) on 25th October 2007 whereby only promotion rights were granted for the event to Jaypee, for which Jaypee constructed the Buddh International Circuit (Circuit). On 13th September 2011, the said agreement was replaced with the Race Promotion Contract (RPC), which granted Jaypee the right to host, stage and promote the event for a consideration of US$ 40 million, for a period of 5 years and which was extendable for another period of 5 years. In the event of termination of RPC, FOWC would be entitled to two years payment of the assured consideration of US$ 40 million.

Artworks Licence Agreement as contemplated in RPC was also entered between FOWC and Jaypee on the same day, permitting the use of certain marks and intellectual property belonging to FOWC for a consideration of US$ 1 million.

Further, on the same day i.e., 13th September 2011, the rights given to Jaypee were transferred back to FOWC’s affiliates as a condition precedent to RPC, which were as follows:

i. Media and Title Sponsorship Rights to Beta Prema 2 Ltd. (Beta Prema 2);

ii. Paddock rights (rights to sell the tickets) to All Sports Management SA (All Sports) and

iii. Rights to generate television feed to Formula One Management Ltd. (FOM).

On 20th January 2011, Organisation Agreement (OA) was signed between FIA/Federation of Motors Sports Clubs of India (‘FMSCI’) and Jaypee, wherein Jaypee was to organise the event. Also, Title Sponsorship Agreement was signed on 16th August 2011 between Beta Prema 2 and Bharti Airtel, wherein Beta Prema 2 transferred title sponsorship rights to Bharti Airtel for US$ 8 million.

Facts of the case are summarised below by way of a diagram:

Assignment of commercial rights vide agreement dated 24 April 2001

Authority for Advance Ruling

After entering into the aforesaid arrangements, both FOWC and Jaypee approached Authority for

Advance Ruling (AAR) seeking its advance ruling on two main questions i.e. :

i. Whether the consideration receivable towards granting of commercial rights to Jaypee was in the nature of royalty as defined in Article 13 of the India-UK Double Taxation Avoidance Agreement (DTAA)? And

ii. Whether FOWC was having any ‘PE’ in India in terms of Article 5 of DTAA?

In reply to the above questions, the AAR held as follows;

i. The consideration receivable in terms of agreement was in the nature of royalty and not business income and

ii. FOWC had no PE in India in terms of Article 5 of the DTAA, as it had no fixed place of business in India, i.e., it neither carried out any business activity in India nor did it authorise any entity to conclude contracts on its behalf.

Delhi High Court

Aggrieved by the ruling of AAR; FOWC, Jaypee and the Revenue authorities filed a writ petition before the Delhi High Court (HC) under Article 226 of the Constitution of India. The HC while deciding the writ petitions held that FOWC had a fixed place PE in India and thus, consideration received / receivable from Japyee was chargeable to tax as business income and not royalty income. However, the HC did not accept the plea of the Revenue that FOWC had a dependent agency PE in India.

Questions before the Hon’ble Supreme Court

Aggrieved by the decision of the HC, all three parties filed an appeal before the Hon’ble Supreme

Court (SC). Thus, the main questions before the SC were as follows:

1. Whether FOWC had a PE in India in terms of Article 5 of the DTAA, that is,

i. Whether the Buddh International Circuit was put at the disposal of FOWC?

ii. Whether FOWC carried on any business and commercial activity in India or not?

2. Whether Jaypee was bound to make appropriate deduction from the amount paid u/s. 195 of the Act?

Contentions / Arguments before the Hon’ble Supreme Court

Contentions of the taxpayer (in brief)

The taxpayer made a submission before the SC that in order to constitute a PE, following conditions were necessarily to be satisfied:

- Fixed place at the disposal of FOWC and

- From the said fixed place, FOWC should carry on doing its business activity According to the taxpayer, both the conditions were not satisfied.

The taxpayer made reference to Organisation Agreement, wherein Jaypee was given the responsibility to organise the event. According to the taxpayer, all acts and obligations were performed by Jaypee, i.e., right from construction of the circuit for the motor races people till the conclusion of the Championship, with no role of FOWC therein.

The taxpayer also submitted that even after going through all the clauses of the agreement between FOWC and Jaypee with a toothcomb, it would be found that FOWC had no physical control over the said circuit. The taxpayer also argued that the entire Formula One event was a temporary model for three days in a year only and even if it was accepted that FOWC had control over this place for those three days, possession of the site for three days in a year cannot be termed as a PE.

The taxpayer’s alternate submission was that the agreement in question was signed in UK under which consideration of US$ 40 million was paid and, therefore, this income accrued in UK. It was also argued that in so far as rights to hold the events were concerned, rights were granted in UK and it was the grant of rights which was the determinative test and not the implementation of those rights, which took place in India.

Contentions of the department (in brief)

On the other hand, department made a rebuttal to the aforesaid submissions by demonstrating the ‘flow of commercial rights’ under various agreements executed between different stakeholders and the manner in which such rights were ultimately exploited by FOWC and its other group companies.

For this purpose, department referred to various agreements entered between different parties as stated in the above facts and explained certain important clauses of the agreements, which clearly manifest that FOWC and its affiliates had taken total control over the event in India. It was also submitted that Jaypee was only to host the event, whereas total access at the time of construction, as well as at the time of event was that of FOWC.

It was further submitted that the so-called rights given to Jaypee were transferred back to FOWC affiliates in as much as Beta Prema 2 acquired media and title sponsorship rights, and All Sports acquired paddock rights. Since the business was carried from the circuit, paddock, etc., it cannot be said that no business activity was carried from the circuit.

Reference to relevant statutory provisions & DTAA regime

In order to determine the existence of a PE in India, the SC examined the provisions of section 9 of the Act, which states that a foreign company may be taxed in India on an income which accrues or arises in India (directly or indirectly) through or from any business connection in India.

The SC had also examined the term ‘business connection’ as defined in Explanation 2 to section 9(1)(i) of the Act, and the term ‘PE’ as defined in Article 5 of the DTAA. The SC stated that if a non-resident had a PE in India in terms of Article 5 of the DTAA, then business connection in India stands established as per section 9(1)(i) of the Act.

The SC, for the purpose of determining whether there exists a PE in India or not in the facts of the present case, relied heavily on:

- A Manual on the OECD Model Tax Convention on Income and on Capital by Philip Baker Q.C. (Philip Baker),

- Klaus Vogel on Double Taxation Conventions (Klaus Vogel),

- Condensed version on Model Tax Convention on Income and on Capital by OECD (OECD Commentary), and

- Indian (and a few foreign) judicial decisions.

Philip Baker

Philip Baker discerns two types of PEs contemplated under Article 5 of OECD Model:

- First, an establishment which is part of the same enterprise under common ownership and control, that is, an office, branch, etc., to which he gives his own description as an ‘associated PE’.

- The second type is an agent, though legally separate from the enterprise, nevertheless who is dependent on the enterprise to the point of forming a PE. Such PE is given the nomenclature of ‘unassociated PE’.

In the first type of PE, primary requirement is that there must be a fixed place of business through which the business of an enterprise is wholly or partly carried on. Thus, it entails two requirements which need to be fulfilled:

- There must be a business of an enterprise of a Contracting State (FOWC in the instant case); and

- PE must be a fixed place of business, i.e., a place which is at the disposal of the enterprise.

Further, as per Philip Baker, it is universally accepted that for ascertaining whether there is a fixed place of business or not, PE must possess three characteristics, that is, stability, productivity and dependence.

Philip Baker also quoted the following passage from the judgment of the Andhra Pradesh High Court in Visakhapatnam Port Trust4 case, to explain the concept of PE:

“The words ‘permanent establishment’ postulate the existence of a substantial element of an enduring or permanent nature of a foreign enterprise in another country which can be attributed to a fixed place of business in that country. It should be of such a nature that it would amount to a virtual projection of the foreign enterprise of one country into the soil of another country.”

From the various examples as stated in his commentary, it was observed by the SC that in order to ascertain as to whether an establishment had a fixed place of business or not, the physically located premises had to be ‘at the disposal’ of the enterprise. It would be irrelevant whether the premises were owned or rented by the enterprise, and the place would be treated as ‘at the disposal’ of the enterprise, only when the enterprise had right to use the said place and had control thereupon.

Klaus Vogel

According to Vogel, the term ‘business’ is broad, vague and of little relevance for the PE definition. The crucial element is the term ‘place’. For this purpose, the SC had critically examined the definition of the term ‘place’ as stated by Vogel.

The SC observed that Vogel had also emphasised that the place of business qualifies only if the place is ‘at the disposal’ of the enterprise, when one takes cue from the word ‘through’ in the Article 5. According to him, the enterprise will be unable to use the place of business as an instrument for carrying on its business, unless it controls the place of business to a considerable extent.

OECD commentary

OECD commentary on Model Tax Convention mentions that a general definition of the term ‘PE’ brings out its essential characteristics, i.e. a distinct ‘situs, a ‘fixed place of business’. The definition, therefore, contains the following conditions:

- the existence of a ‘place of business’, i.e., a facility such as premises or, in certain instances, machinery of equipment, and such place of business must be ‘fixed’, i.e., it must be established at a distinct place with a certain degree of permanence;

- the carrying on of the business of the enterprise through this fixed place of business.

OECD commentary also states that the words ‘through which’ must be given a wide meaning, so as to apply to any situation, where business activities are carried on at a particular location, which is at the disposal of the enterprise for that purpose.

Key observations and decision of the Hon’ble Supreme Court

1. Whether FOWC had a PE in India in terms of Article 5 of the DTAA, i.e.,

i. Whether Buddh International Circuit was put at the disposal of FOWC?

The SC had placed more reliance on crucial parameters and agreements, namely, the manner in which commercial rights, which were held by FOWC and its affiliates, have been exploited in the instant case. For this purpose, the entire arrangement between FOWC and its associates on the one hand and Jaypee on the other hand, needs to be considered, to bring out the real economic substance of the transaction between the parties.

The SC while evaluating the various agreements and arrangements, made critical observations, which clearly captured the substance of the said transactions, they are as follows:

- Commercial rights as allegedly given to Jaypee were transferred back to the taxpayer’s affiliates viz. Beta Prema 2, All Sports and FOM, as stated in the above facts.

- Beta Prema 2, though, was given media rights, etc., on September 13, 2011, it had entered into ‘Title Sponsorship Agreement’ with Bharti Airtel on August 16, 2011 (i.e., more than a month before getting the rights from Jaypee) whereby it transferred the said rights to Bharti Airtel for a consideration of US$ 8 million.

The SC disregarded taxpayer’s argument that the racing event did not constitute a PE because the duration of the event was only three days. The SC held that the HC had rightly concluded that having regard to the duration of the event, even though it was for limited days, FOWC had full and exclusive access through its personnel to the circuit for the entire duration of the event; thus, number of days for which the access was there would not make any difference, in coming to the conclusion that FOWC had the circuit to its disposal.

The SC for coming to the aforesaid conclusion, referred to the reasoning given by the High Court which in turn depended on the OECD commentary and Klaus Vogel’s commentary on PE, e.g.:

- A stand at a trade fair, occupied regularly for three weeks a year, through which an enterprise obtained contracts for a significant part of its annual sales, was held to constitute a PE.

- Likewise, a temporary restaurant operated in a mirror tent at a Dutch flower show for a period of seven months was held to constitute a PE.

ii. Whether FOWC carried on any business and commercial activity in India or not?

The SC observed that the substantial part of this aspect had already been discussed in the first question. It was also observed that FOWC was the Commercial Right Holder and these rights can be exploited with the conduct of F-1 Championship, which is organised in various countries.

The SC also observed that in order to organise the event, FOWC would require track, teams to participate in competition, public/viewers, etc. Further, for augmenting the earnings in these events, there would be advertisements, media rights, etc. as well and it was FOWC and its affiliates which had been responsible for all the aforesaid activities. All possible commercial rights, including advertisement, media rights, etc. and even right to sell paddock seats, were assumed by FOWC and its associates.

The SC concluded that the taxpayer had carried on business in India under Article 5(1) of the DTAA, i.e., dealing with determination of a fixed place PE, and concurring with the view of the HC, wherein the HC held that:

“57…………. The conceptualization of the event and the right to include it in any particular circuit, such as Buddh Circuit is that of the FOWC; it decides the venue and the participating teams are bound to it to compete in the race in the terms agreed with the FOWC. All these, in the opinion of the Court, unequivocally, show that the FOWC carried on business in India for the duration of the race (and for two weeks before the race and a week thereafter). Every right, which it possessed was monetized; the US$ 40 million which Jaypee paid was only a part of that commercial exploitation by the FOWC.

58. Consequently, the Court concludes that the FOWC carried on business in India within the meaning of expression under Article 5(1) of the DTAA ”

The SC held that the test laid down in Visakhapatnam Port Trust case (supra) stands fully satisfied, i.e., the Buddh International Circuit is a fixed place where the commercial/economic activity of conducting F-1 Championship was carried out, and one could also clearly discern that it was a virtual projection of the foreign enterprise, namely, Formula One (i.e., FOWC) on the soil of this country (India).

The SC also observed that all three characteristics of a fixed place PE i.e., stability, productivity and dependence were present in this case. The SC held that:

“Fixed place of business in the form of physical location, i.e., Buddh International Circuit, was at the disposal of FOWC through which it conducted business. Aesthetics of law and taxation jurisprudence leave no doubt in our mind that taxable event has taken place in India and non-resident FOWC is liable to pay tax in India on the income it has earned on this soil.”

2. Whether Jaypee was bound to make appropriate deduction from the amount paid u/s. 195 of the Act?

On this incidental issue, SC has held that Jaypee was bound to make appropriate deductions from the amount paid u/s. 195 of the Act. However, only that portion of the income of FOWC, which is attributable to the said PE, would be treated as business income of FOWC and only on that part of the income, deduction was required to be made u/s. 195 of the Act.

Comments

The judgment of the Hon’ble SC clearly highlights that in the present day, the tests to determine whether a non-resident carries on business in the source state, especially due to the advancement of information technology and communication, the methodology of conduct of business will be considered more broadly than yesteryears. The tests of permanence, duration, will breakdown and will need to be interpreted in a more dynamic and broad setting.

The SC while arriving at the judgment had considered the various agreements between the group companies to determine the real intention of the parties to the transaction. The SC had also looked into the economic substance of the transaction over its form, by reading the various agreements in a holistic and combined manner, rather than independently and in a disjointed manner.

Notes:-

1 DIT International Taxation, Mumbai vs. M/s. Morgan Stanley & Company Inc. (2007) 292 ITR 416 (SC)

2. Formula One World Championship Ltd. vs. Commissioner of Income Tax, International Taxation-3, Delhi & Anr. – Civil Appeal No. 3849, 3850 and 3851 of 2017 (SC)

3. Facts of the case are adopted from Authority for Advance Rulings in Morgan Stanley & Co. – AAR No. 661/2005

4. CIT vs. Visakhapatnam Port Trust [1983] 144 ITR 146 (Andhra Pradesh High Court)

Author Bio