The Goods and Services Tax (GST) regime, ‘mother of all tax reforms’ in India, has completed three years on July 1, 2020. The GST which was expected to create utter chaos and uncertainty for at least the next 4 to 5 years, as the initial response to the compliance platform designed by GSTN was too complicated and the initial hiccups in the GSTN portal added fuel to the fire, now shows some sign of settling down. The credit for this goes to government officers, GST council, resilient tax payers and last but not the least numerous professionals across the country.

This article is penned down to emphasise the significant provision which is often overlooked by numerous taxpayers and professionals even though we are in the second year of filing Annual return (GSTR-9) and Audit (GSTR-9C) under the Goods and Services Act, 2017.

One of those significant sections from the GST Audit checklist that requires strict compliance, which also acts as a kingpin when there is a sale or transfer or disposal of capital goods under the GST law, is Section 18(6) of the Central Goods and Services Act, 2017 and is being reproduced below:

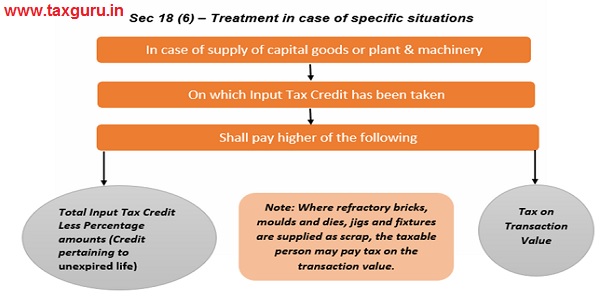

Section 18 (6) of CGST Act – In case of supply of Capital Goods

In case of supply of capital goods or plant and machinery, on which input tax credit has been taken, the registered person shall pay an:

Amount equal to the input tax credit taken on the said capital goods or plant and machinery reduced by such percentage points as may be prescribed or

the tax on the transaction value of such capital goods or plant and machinery determined under section 15, whichever is higher.

Provided that where refractory bricks, moulds and dies, jigs and fixtures are supplied as scrap, the taxable person may pay tax on the transaction value of such goods prescribed under section 15.

Rule 44(6) read with Rule 44(1)(b) of the CGST Rules also prescribes the method of determining an amount for the purpose of Section 18(6), by stating that input tax credit involved in the remaining useful life in months shall be computed on pro rata basis, taking useful life as five years.

Now let us understand the calculations as per this section in accordance with prescribed rule with the help of the following example:

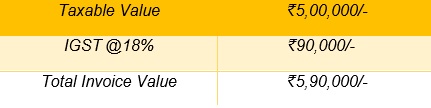

Suppose Mr. X (Delhi) sold his machinery to Mr. Y (Haryana) on 4th July,2020 for ₹5,00,000/- which he purchased on 01st Apr, 2018 at ₹11,80,000/- inclusive of GST of ₹1,80,000/- @18%.

According to Sec 18 (6) of the CGST Act, 2017, Mr. X has to pay an amount equivalent to higher of the following:

a. an amount equal to the GST levied on transaction value on supply (sale) of the machinery, that is ₹5,00,000*18% i.e. ₹90,000/- or

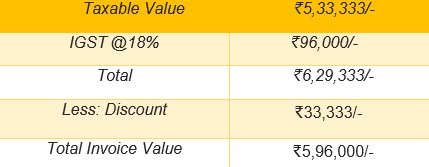

b. An amount of input tax credit as reduced by such percentage point as prescribed under the rules i.e. ₹96,000/- (which is determined below).

Calculation of ITC reversal as per Rule 44(6) read with Rule 44 (1)(b) are as follows:

Useful life of the asset is 2yrs 3months 4days (Useful life the capital goods is 5 yrs under GST)

Unexpired life of an asset in months= 32 months ignoring a part of the month

No. of months used= 28 months

Credit relating to unexpired life= 1,80,000*32/60= ₹96,000

Hence, Mr. X has to pay GST of ₹ 96,000/- on sale of this machinery.

Generally, taxpayers make the following tax invoice for this transaction:

But this practice followed by the taxpayers ended up to make an excess payment of ₹6,000/- (₹96,000 – ₹90,000) along with an amount of interest from his pocket itself at the time of Audit.

So, the correct invoicing method for selling the capital goods on which quantum of ITC reversal exceeds the tax payable on transactional value shall be as follows in order to preclude that excess payment of ₹6,000/-:

After analysing the points of paramount importance, now let us jump upon the further discussion on GST Audit in respect of this section.

As we all know that as per Sec 35 (5), every registered person whose turnover during a financial year exceeds the prescribed limit shall get his accounts audited by a chartered accountant or a cost accountant and shall submit a copy of the audited annual accounts, the reconciliation statement under section 44(2) of CGST Act and such other documents in such form and manner as may be prescribed.

Furthermore, while filing GSTR-9C, every registered person shall need to “upload his/her financial statements” and Section 18(6) triggers when there is a deletion of capital goods in the financial statements (Balance Sheet-Depreciation charts) of a regular taxpayer on which Input tax credit is availed under GST thereby should be verified and complied carefully by the GST auditor (Chartered Accountant or Cost Accountant).

Even though, 30th September, 2020, the due date for filing GSTR-9 and GSTR-9C for F.Y. 2018-19 is approaching soon but still it is advisable that the GST auditor shall examine all the crucial areas under GST Audit meticulously with the reliance placed on the proverb that is “Haste is of the devil”.

Now, it would, however, be interesting to see how govt. would take a step further against assessee in respect of violation of the said section, if any.

In our next article, we will discuss a Sec 18(6) of the CGST Act, 2017 in detail.

*****

The author is a Practicing Chartered Accountant offers a plethora of services such as GST, GST refunds, Income Tax, MSME, ROC and other tax related matters and can be reached at tax.bkansalco@gmail.com.

Disclaimer: The views presented are in personal and generic form and not as a legal advice. Users of this information are expected to refer to the relevant existing provisions of the applicable laws.

Author Bio