Article explains implications of Notification No. 10/2020-(CT) to Notification 36/2020(CT), Circular 133 to Circular 136, Notification No. 2/2020- CT (Rate) to Notification No. 3/2020-CT (Rate) and Press Release dated 14.03.2020 post GST Council 39th Meeting.

RECENT CHANGES IN GST

NOTIFICATIONS 30 TO 36(CT) & Circular No. 136/2020

| 1. Composition Dealer | ||||

| a) Opting to pay tax under sec. 10 of the CGST Act or those availing option to pay tax under the notification 02/2019-CT(Rate) dated 07.03.2019 | ||||

| Nature of form | Period | Actual date | Extended date | Notification No. |

| Form GST CMP-02(Intimation) | F.Y. 2020-21 | Prior to commencement of F.Y.(Rule 3(3)) | 30.06.2020 | N.N.30/2020 dated 03.04.2020 |

| Form GST ITC-03 (For Lapse of credit) | F.Y. 2020-21 | Within 60 days from commencement of relevant F.Y.( Rule 3(3)) | 31.07.2020 | N.N. 30/2020 dated 03.04.2020 |

| b) Returns of composition dealer | ||||

| Nature of form | Period | Actual date | Extended date | Notification No. |

| Form GST CMP -08 | Quarter ending March | 18th day of succeeding quarter i.e 18th April | 7th July 2020 | 34/2020 dated 03.04.2020 |

| Form GSTR-4 | F.Y. ending 31.03.2020 | 30th April 2020 | 15th July 2020 | 34/2020 dated 03.04.2020 |

Notification No. 30/2020-CT dated 3rd April 2020

Proviso inserted in Rule 36(4)- capping 10% of ITC as per eligible credit of Form GSTR-2A

(“Provided that the said condition shall apply cumulatively for the period February, March, April, May, June, July and August, 2020 and the return in FORM GSTR-3B for the tax period September, 2020 shall be furnished with the cumulative adjustment of input tax credit for the said months in accordance with the condition above.”.

Feb- Aug, 2020

Month- wise 36(4)—————————————————-Relaxed

Cumulative in the return of September month from Feb – Aug, 2020——–Mandatory

| Particulars | Abbreviation | Tax period |

| Cumulative 2A eligible credit | A |

Feb- Aug, 2020

|

| Books Total | B | |

| 3B Total (generally B should be =C) | C | |

| 110% of (A) | D | A*110% |

| Compare D with C (short, payable) | ||

–

| Particulars | Abbreviation | Tax period |

| 2A September eligible credit | A |

Sept, 2020 |

| Books September | B | |

| 3B Sept. (generally B should be =C) | C | |

| 110% of (A) | D | A*110% |

| Compare D with C (excess) | ||

Can be adjusted (Hence cumulative download for Feb-Sep,2020)

RULE – 36(4)

| Month | ITC as per Books | Itc as per 2A | ITC availed in 3B |

| Feb, 2020 | 2000 | 1600 | 2000 |

| March 2020 | 3000 | 2400 | 3000 |

| April 2020 | 2400 | 1600 | 2400 |

| May 2020 | 2000 | 1400 | 2000 |

| June 2020 | 2400 | 2000 | 2400 |

| July 2020 | 1000 | 800 | 1000 |

| Aug 2020 | 1800 | 1600 | 1800 |

| Sept 2020 | 2800 | 3000 | 1240* |

| Total | 17400 | 14400 | 15840 |

Note:- Adjustment of total shortfall of ITC as per Rule 36(4) shall be done in Sept. 2020

*14400*110%= 15840

- ITC Claimed= 17400

- Excess claimed=17400-15840=1560 to be adjusted from Sept. month’s ITC

- ITC=2800-1560=1240

| 1. GSTR 3B | |||||

| a) Taxpayers having aggregate turnover of more than Rs. 5crore in the preceding Financial year | |||||

| Month | Due date (Not extended) | Cut off Date | Interest | Late Fees | Notification no. |

| Feb 2020 | 20.03.2020 | 24.06.2020 (Interest /Late fee waiver last cut off date) | Nil till 04/04/2020 i.e (15 days from due date)

and thereafter, @ 9% p.a (to be calculated on basis of days of default) If the return is filled up to 24.06.2020. Note: If return is filed after 24.06.2020 then 18% interest will be charged from due date i.e 20-03-2020. |

Complete Waiver of Late fees if filed on or before 24/06/2020 | N.N. 31/2020 (Interest), 32/2020(Late Fee) |

| Mar, 2020 | 20.04.2020 | Nil till 05/05/2020 and thereafter, @ 9% p.a (to be calculated on basis of days of default), If the return is filled up to 24.06.2020.

Note: If return is filed after 24.06.2020 then 18% interest will be charged from due date i.e 20-04-2020. |

|||

| Apr 2020 | 20.05.2020 | Nil till 04/06/2020 and thereafter, @ 9% p.a (to be calculated on basis of days of default), If the return is filled up to 24.06.2020.

Note: If return is filed after 24.06.2020 then 18% interest will be charged from due date i.e 20-05-2020. |

|||

| May 2020 | GSTR 3B

20.06.2020 |

27.06.2020

(Extended date) |

Interest @18% if filed after 27.06.2020 | Applicable, if filed after 27.06.2020 | N.N 36/2020 |

Circular 136/06/2020

Illustration:- Calculation of interest for delayed filing of return for the month of March, 2020 (due date of filing being 20.04.2020) may be illustrated as per the below Table:

For Tax Payer with Turnover Exceeding Rs. 5 crore

| S. No. | Date of filing GSTR-3B for March,2020 | No. of days of delay | Whether condition for reduced interest is fulfilled? | Interest |

| 1 | 02.05.2020 | 11 | Yes | 0 |

| 2 | 20.05.2020 | 30 | Yes | 0 for 15 days + 9% p.a. for 15 days |

| 3 | 20.06.2020 | 61 | Yes | Zero interest for 15 days + interest rate @9% p.a. for 46 days |

| 4 | 24.06.2020 | 65 | Yes | Zero interest for 15 days + interest rate @9% p.a. for 50 days |

| 5 | 30.06.2020 | 71 | No | Interest rate @18% p.a. for 71 days (i.e. no benefit of reduced interest) |

–

| 1. GSTR 3B | ||||||

| b) Taxpayers having aggregate turnover of more than Rs. 1.5 Cr but up to 5 Cr in the preceding Financial year | ||||||

| Month | Re

turn |

Due date | Cut off Date | Interest | Late Fees | Noti

fication no. |

| Feb 2020 | GSTR 3B | 22.03.2020/

24.03.2020 |

29.06.2020 (Interest /Late fee waiver last cut off date) | Nil, if return filed up to 29.06.2020 | Nil, if return

filed up to 29.06.2020 |

N.N. 31/2020 (Interest), 32/2020 (Late Fee) |

| Mar, 2020 | GSTR 3B | 22.04.2020/ 24.04.2020 | 29.06.2020 (Interest /Late fee waiver last cut off date) | Nil, if return filed up to 29.06.2020 | Nil, if return

filed up to 29.06.2020 |

|

| Apr 2020 | GSTR 3B | 22.05.2020/ 24.05.2020 | 30.06.2020 (Interest /Late fee waiver last cut off date) | Nil, if return filed up to 30.06.2020 | Nil, if return filed upto 30.06.2020 | |

| May 2020 | GSTR 3B | 22.06.2020/ 24.06.2020 | 12.07.2020/

14.07.2020 (As per States) (Date Extended) |

Interest @18% if return filed after extended due date | Applicable, if

filed after 12.07.2020/ 14.07.2020 |

NN 36/2020 |

–

| 1. GSTR 3B | ||||||

| c) Taxpayers having aggregate turnover of up to Rs. 1.5 Cr in the preceding Financial year | ||||||

| Month | Return | Due date | Cut off Date | Interest | Late Fees | Notification no. |

| Feb 2020 | GSTR 3B | 22.03.2020/

24.03.2020 |

30.06.2020 (Interest /Late fee waiver last cut off date) | Nil, if filed upto cut off date | Nil, if filed upto cut off date | N.N. 31/2020 (Interest), 32/2020 (Late Fee) |

| Mar, 2020 | GSTR 3B | 22.04.2020/ 24.04.2020 | 03.07.2020 (Interest /Late fee waiver last cut off date) | Nil, if filed upto cut off date | Nil, if filed upto cut off date | N.N. 31/2020 (Interest), 32/2020 (Late Fee) |

| Apr 2020 | GSTR 3B | 22.05.2020/ 24.05.2020 | 06.07.2020 (Interest /Late fee waiver last cut off date) | Nil, if filed upto cut off date | Nil, if filed upto cut off date | N.N. 31/2020 (Interest), 32/2020 (Late Fee) |

| May 2020 | GSTR 3B | 22.06.2020/ 24.06.2020 | 12.07.2020/

14.07.2020 (As per States) (Extended Date) |

Interest @18% if return filed after extended due date | Applicable, if filed after 12.07.2020/ 14.07.2020 | N.N 36/2020 |

–

| 2. GSTR -1 | ||||||

| Month | Return | Due date (Not Extended) | Cut off Date | Interest | Late Fees | Notification no. |

| Mar 2020 | GSTR 1 Monthly | 11.4.2020 | 30.06.2020 | N.A | Nil, If filed upto Cut off Date | N.N. 33/2020 |

| Apr 2020 | 11.05.2020 | 30.06.2020 | N.A | Nil, If filed upto Cut off Date | N.N. 33/2020 | |

| May 2020 | 11.06.2020 | 30.06.2020 | N.A | Nil, If filed upto Cut off Date | N.N. 33/2020 | |

| Jan – Mar 2020 | GSTR 1 Quarterly | 30.04.2020 | 30.06.2020 | N.A | Nil, If filed upto Cut off Date | N.N. 33/2020 |

Notification No. 35/2020 dated 03.04.2020

General/ Blanket Extension

As per power conferred by sec 168A (Act amended through ordinance (valid till 6 months of next Parliament Sitting) Done due to Power given to CG to give blanket exemption in case of natural calamities etc.

Due to COVID-19

On recommendation of council

Extend Time Period to 30.06.2020

a. Departmental Action

Completion of any proceedings or Passing of any order or Issuance of any notice, intimation, notification, sanction or approval or such other action by whatever name called, by any authority , commission or tribunal, by whatever name called, under the provisions of the Acts stated above.

b. Assessee Action

Filing of any appeal, reply or application or furnishing of nay report, document, return, statement or such other record, by whatever name called, under the provisions of the Acts stated above.

(Falling due from 20.03.2020 to 29.06.2020)

Exclusions to Blanket Extension

The following are Certain Exclusions provided under this notification, on which, Extension will not appl which are explained in the following Table:

| Provisions | Explanation | Remarks |

| Chapter IV | Time and Value of Supply | Time and valuation of supply provision remains unaffected |

| Section 10(3) | Lapse of Option availed by Composition dealers | Option availed u/s 10(1) by a composition dealer wrt composition levy shall stands lapsed wef date on which his aggregate turnover exceeds the specified limits. If such date falls between 20.3.20 to 30.06.2020, there shall be no extension for such person for switching to regular person. |

| Section 25 | Application for Registration | No extension for person liable to get himself registered u/s 22 and 24 within the time limits prescribed. |

| Section 27 | Casual Taxable person and Non Resident taxable person | No extension in time limits for Registration by a Casual Taxable person and Non Resident taxable person liable to register. |

| Section 31 | Tax invoices | No extension in time limits prescribed for issuance of a tax invoice as per provisions of Act. ie Tax Invoice has to be issued if any supply of Goods or Services are made between the specified period as per existing provisions only. |

| Section 37 | Details of Outward Supplies GSTR | No extension shall apply to the provisions of furnishing of details of outward supplies on the common portal i.e GSTR-1 |

| Section 47 | Late Fees | This notification shall not extend the levy of late fees applicable under the Act except for certain specific provisions under other notification issued. |

| Section 50 | Interest | This notification shall not extend the levy of any interest chargeable @ 18% or 24% under the Act except for certain specific provisions under other notification issued. For eg: if any interest is chargeable for wrong availment of ITC and its subsequent reversal, the same shall be chargeable even if done within the specified period. |

–

| Particulars | Explanation | Remarks |

| Section 69 | Power to Arrest | There is a provision for arrest u/s 132 and the accused is to be presented before the Magistrate within 24 hours in such cases. No extension shall apply in such cases also. |

| Section 90 | Partners Liability | No extension to the liability of partners of firm to pay tax, interest or penalty. |

| Section 122 | Penalty for offences | This extension shall not be applicable for any offences covered under section 122 covering TDS/TCS. |

| Section 129 | Detention, Seizure and release of goods and conveyances | This notification excludes the provisions of the Act as specified u/s 129 wrt to detention of goods and conveyances in transit and its seizure and release |

| Section 39 Except sub section (3), (4), (5) | Furnishing of Returns u/s 39 [GSTR 3b, etc] | There is no extension for the returns specified u/s 39 and to be filed except for returns under sub sections: (3)- TDS Returns (4)-ISD Returns (5)-Return- Casual Person |

| Section 68 | E Way Billing | No extension in E Way Bill provisions. The same have to be complied with before the movement of Goods as per relevant provisions of Act and Rules. |

| Further, there shall be no extension with respect to any rules made wrt to above provision of the Act | ||

Circular 136/06/2020

Issue 8:- What will be the status of e-way bills which have expired during the lockdown period?

Clarification:- In terms of notification No. 35/2020- Central Tax, dated 03.04.2020,Issued under the provisions of 168A of the CGST Act, where the validity of an e-way bill generated under rule 138 of the CGST Rules expires during the period 20th day of March, 2020 to 15th day of April, 2020, the validity period of such e-way bill has been extended till the 30th day of April, 2020.

Issue 9:- What are the measures that have been specifically taken for taxpayers who are required to deduct tax at source under section 51, Input Service Distributors and Non-resident Taxable persons?

Clarification:- Under the provisions of section 168A of the CGST Act, in terms of notification No. 35/2020- Central Tax, dated 03.04.2020, the said class of taxpayers have been allowed to furnish the respective returns specified in sub-sections (3), (4) and (5) of section 39 of the said Act, for the months of March, 2020 to May, 2020 on or before the 30th day of June, 2020.

Issue 10:- What are the measures that have been specifically taken for taxpayers who are required to collect tax at source under section 52?

Clarification:- Under the provisions of section 168A of the CGST Act, in terms of notification No. 35/2020- Central Tax, dated 03.04.2020, the said class of taxpayers have been allowed to furnish the statement specified in section 52, for the months of March, 2020 to May, 2020 on or before the 30th day of June, 2020.

Issue 11:- The time limit for compliance of some of the provisions of the CGST Act is falling during the lock-down period announced by the Government. What should the taxpayer do?

Clarification:-Vide notification No. 35/2020- Central Tax, dated 03.04.2020, issued under the provisions of 168A of the CGST Act, except for few provisions covered in exclusion clause, any time limit for completion or compliance of any action which falls during the period from the 20th day of March, 2020 to the 29th day of June, 2020, and where completion or compliance of such action has not been made within such time, has been extended to 30th day of June, 2020.

CIRCULAR 135/05/2020 dated 31-03-2020

> Bunching of refund claims across Financial Years

The said restriction on the clubbing of tax periods across financial years for claiming refund thus has been continued vide Paragraph 8 of the Circular No. 125/44/2019-GST dated 18.11.2019, which is reproduced as under:

- “8. The applicant, at his option, may file a refund claim for a tax period or by clubbing successive tax The period for which refund claim has been filed, however, cannot spread across different financial years. Registered persons having aggregate turnover of up to Rs. 1.5 crore in the preceding financial year or the current financial year opting to file FORM GSTR-1 on quarterly basis, can only apply for refund on a quarterly basis or clubbing successive quarter……………..”

- Hon’ble Delhi High Court in Order dated 21.01.2020, in the case of M/s Pitambra Books Pvt Ltd., vide para 13 of the said order has stayed the rigour of paragraph 8 of Circular No. 125/44/2019-GST dated 18.11.2019 and has also directed the Government to either open the online portal so as to enable the petitioner to file the tax refund electronically, or to accept the same manually within 4 weeks from the Order. Hon’ble Delhi High Court vide para 12 of the aforesaid Order has observed that the Circulars can supplant but not supplement the law. Circulars might mitigate rigours of law by granting administrative relief beyond relevant provisions of the statute, however, Central Government is not empowered to withdraw benefits or impose stricter conditions than postulated by the law. No Restriction u/s 16(3) of IGST and 54(3) of CGST,2017

- Further, same issue has been raised in various other representations also, especially those received from the merchant exporters wherein merchant exporters have received the supplies of goods in the last quarter of a Financial Year and have made exports in the next Financial Year i.e. from April onwards. The restriction imposed vide para 8 of the master refund circular prohibits the refund of ITC accrued in such cases as well.

| BEFORE AMENDMENT | ||

| Particulars | March | April |

| Purchase Input | 100000 | 0 |

| Export | 0 | 1200000 |

| Refund | 0 | 0 |

| After Amendment | ||

| Particulars | March- April | |

| Purchase Input | 100000 | |

| Export | 1200000 | |

| Refund | 100000 | |

> Refund of accumulated input tax credit (ITC) on account of reduction in GST Rate

It has been brought to the notice of the Board that some of the applicants are seeking refund of unutilized ITC on account of inverted duty structure where the inversion is due to change in the GST rate on the same goods.

This can be explained through an illustration.

An applicant trading in goods has purchased, say goods “X” attracting 18% GST. However, subsequently, the rate of GST on “X” has been reduced to, say 12%. It is being claimed that accumulation of ITC in such a case is also covered as accumulation on account of inverted duty structure and such applicants have sought refund of accumulated ITC under clause (ii) of sub-section (3) of section 54 of the CGST Act.

It may be noted that refund of accumulated ITC in terms clause (ii) of sub-section (3) of section 54 of the CGST Act is available where the credit has accumulated on account of rate of tax on inputs being higher than the rate of tax on output supplies. It is noteworthy that, the input and output being the same in such cases, though attracting different tax rates at different points in time, do not get covered under the provisions of clause (ii) of sub-section (3) of section 54 of the CGST Act. It is hereby clarified that refund of accumulated ITC under clause (ii) of sub-section (3) of section 54 of the CGST Act would not be applicable in cases where the input and the output supplies are the same.

> Change in manner of refund of tax paid on supplies other than zero rated supplies

Circular No. 125/44/2019-GST dated 18.11.2019, in para 3, categorizes the refund applications to be filed in FORM GST RFD-01 as under:

a) Refund of unutilized input tax credit (ITC) on account of exports without payment of tax;

b) Refund of tax paid on export of services with payment of tax; .

c) Refund of unutilized ITC on account of supplies made to SEZ Unit/SEZ Developer without payment of tax;

d) Refund of tax paid on supplies made to SEZ Unit/SEZ Developer with payment of tax;

e) Refund of unutilized ITC on account of accumulation due to inverted tax structure;

f) Refund to supplier of tax paid on deemed export supplies;

g) Refund to recipient of tax paid on deemed export supplies;

h) Refund of excess balance in the electronic cash ledger;

i) Refund of excess payment of tax;

j) Refund of tax paid on intra-State supply which is subsequently held to be inter State supply and vice versa;

k) Refund on account of assessment/provisional assessment/appeal/any other order;

l) Refund on account of “any other” ground or reason.

For the refund of tax paid falling in categories specified at S. No. (i) to (l) above i.e. refund claims on supplies other than zero rated supplies, no separate debit of ITC from electronic credit ledger is required to be made by the applicant at the time of filing refund claim, being claim of tax already paid. However, the total tax would have been normally paid by the applicant by debiting tax amount from both electronic credit ledger and electronic cash ledger. At present, in these cases, the amount of admissible refund, is paid in cash even when such payment of tax or any part thereof, has been made through ITC.

As this could lead to allowing unintended encashment of credit balances, this issue has been engaging attention of the Government. Accordingly, vide notification No.16/2020-Central Tax dated 23.03.2020, sub-rule (4A) has been inserted in rule 86 of the CGST Rules, 2017which reads as under:

“(4A) Where a registered person has claimed refund of any amount paid as tax wrongly paid or paid in excess for which debit has been made from the electronic credit ledger, the said amount, if found admissible, shall be re-credited to the electronic credit ledger by the proper officer by an order made in FORM GST PMT-03.”

Further, vide the same notification, sub-rule (1A) has also been inserted in rule 92 of the CGST Rules, 2017. The same is reproduced hereunder:

“(1A)Where, upon examination of the application of refund of any amount paid as tax other than the refund of tax paid on zero-rated supplies or deemed export, the proper officer is satisfied that a refund under sub-section (5) of section 54 of the Act is due and payable to the applicant, he shall make an order in FORM RFD-06 sanctioning the amount of refund to be paid, in cash, proportionate to the amount debited in cash against the total amount paid for discharging tax liability for the relevant period, mentioning therein the amount adjusted against any outstanding demand under the Act or under any existing law and the balance amount refundable and for the remaining amount which has been debited from the electronic credit ledger for making payment of such tax, the proper officer shall issue FORM GST PMT-03 re-crediting the said amount as Input Tax Credit in electronic credit ledger.”

The combined effect the above mentioned changes is that any such refund of tax paid on supplies other than zero rated supplies will now be admissible proportionately in the respective original mode of payment i.e. in cases of refund, where the tax to be refunded has been paid by debiting both electronic cash and credit ledgers (other than the refund of tax paid on zero-rated supplies or deemed export), the refund to be paid in cash and credit shall be calculated in the same proportion in which the cash and credit ledger has been debited for discharging the total tax liability for the relevant period for which application for refund has been filed. Such amount, shall be accordingly paid by issuance of order in FORM GST RFD-06 for amount refundable in cash and FORM GST PMT-03 to re-credit the amount attributable to credit as ITC in the electronic credit ledger.

| Amount | CGST | SGST | ||||||||||

| Actual Sales | 100000 | 2500 | 2500 | |||||||||

| Sales Entered in 3B | 100000 | 5000 | 5000 | |||||||||

| Paid through balance in ledger | 10000

Rs. 7000 (Credit Ledger) & Rs. 3000 (Cash Ledger) |

|||||||||||

| Excess Paid | 2500 | 2500 | ||||||||||

| Refund applied | 5000

|

|||||||||||

| Amount | CGST | SGST | ||||||||||

| Actual Sales | 100000 | 2500 | 2500 | |||||||||

| Sales Entered in 3B | 100000 | 5000 | 5000 | |||||||||

| Paid through balance in ledger | 10000

Rs. 7000 (Credit Ledger) & Rs. 3000 (Cash Ledger) |

|||||||||||

| Excess Paid | 2500 | 2500 | ||||||||||

| Refund applied | 5000 | |||||||||||

| Outstanding Dues | 1000 | |||||||||||

|

||||||||||||

> Guidelines for refunds of Input Tax Credit under Section 54(3)( Refund of unutilized input tax credit)

In terms of para 36 of circular No. 125/44/2019-GST dated 18.11.2019, the refund of ITC availed in respect of invoices not reflected in FORM GSTR-2A was also admissible and copies of such invoices were required to be uploaded. However, in wake of insertion of sub-rule (4) to rule 36 of the CGST Rules, 2017 vide notification No. 49/2019-GST dated 09.10.2019, various references have been received from the field formations regarding admissibility of refund of the ITC availed on the invoices which are not reflecting in the FORM GSTR-2A of the applicant.

The matter has been examined and it has been decided that the refund of accumulated ITC shall be restricted to the ITC as per those invoices, the details of which are uploaded by the supplier in FORM GSTR-1 and are reflected in the FORM GSTR-2A of the applicant. Accordingly, para 36 of the circular No. 125/44/2019-GST, dated 18.11.2019 stands modified to that extent.

> New Requirement to mention HSN/SAC in Annexure ‘B’

References have also been received from the field formations that HSN wise details of goods and services are not available in FORM GSTR-2A and therefore it becomes very difficult to distinguish ITC on capital goods and/or input services out of total ITC for a relevant tax period. It has been recommended that a column relating to HSN/SAC Code should be added in the statement of invoices relating to inward supply as provided in Annexure–B of the circular No. 125/44/2019- GST dated 18.11.2019 so as to easily identify between the supplies of goods and services.

The issue has been examined and considering that such a distinction is important in view of the provisions relating to refund where refund of credit on Capital goods and/or services is not permissible in certain cases, it has been decided to amend the said statement. Accordingly, Annexure-B of the circular No. 125/44/2019-GST, dated 18.11.2019 stands modified to that extent.

A suitably modified statement format is attached for applicants to upload the details of invoices reflecting in their FORM GSTR-2A. The applicant is, in addition to details already prescribed, now required to mention HSN/SAC code which is mentioned on the inward invoices. In cases where supplier is not mandated to mention HSN/SAC code on invoice, the applicant need not mention HSN/SAC code in respect of such an inward supply.

Annexure-B

Statement of invoices to be submitted with application for refund of unutilized ITC

Sr. No . |

GSTIN of the Supplier |

Name of the Supplier |

Invoice Details |

Category of input supplies |

Central Tax |

State Tax/ Union Territory Tax |

Integratd Tax |

Cess |

Eligible for ITC |

Amount of eligible ITC |

||||

Invo ice No. |

Date |

Value |

Inputs/Input Services/cap ital goods |

HSN/SAC |

Yes/No/Partially |

|||||||||

1 |

2 |

3 |

4 |

5 |

6 |

7 |

8 |

9 |

10 |

11 |

12 |

13 |

14 |

|

Notification No. 16/2020 dated 23.03.2020

Rule 8(4A) inserted after Rule 8(4):-

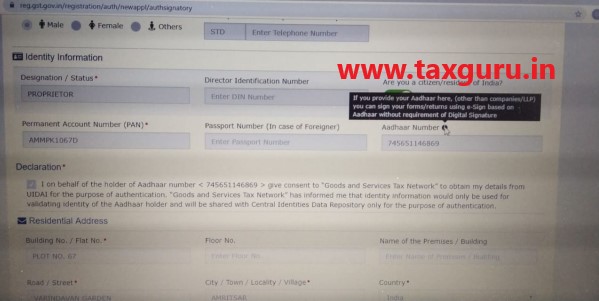

Rule 8:- Application for Registration

(4A) The applicant shall, while submitting an application under sub-rule (4), with effect from 01.04.2020, undergo authentication of Aadhaar number for grant of registration.”.

Proviso to Rule 9(1) inserted ( Rule 9 :- Verification of application and approval)

“Provided that where a person, other than those notified under sub-section (6D) of section 25, fails to undergo authentication of Aadhaar number as specified in sub-rule (4A) of rule 8, then the registration shall be granted only after physical verification of the principle place of business in the presence of the said person, not later than sixty days from the date of application, in the manner provided under rule 25 and the provisions of sub-rule (5) shall not be applicable in such cases.”.

Rule 25 substituted with following:-

“Physical verification of business premises in certain cases.-Where the proper officer is satisfied that the physical verification of the place of business of a person is required due to failure of Aadhaar authentication before the grant of registration, or due to any other reason after the grant of registration, he may get such verification of the place of business, in the presence of the said person, done and the verification report along with the other documents, including photographs, shall be uploaded in FORM GST REG-30 on the common portal within a period of fifteen working days following the date of such verification.”.

Notification No. 16/2020 dated 23.03.2020

> Proviso inserted to Rule 80(3) regarding Reconciliation Statement

80(3):- Every registered person whose aggregate turnover during a financial year exceeds two crore rupees shall get his accounts audited as specified under sub-section (5) of section 35 and he shall furnish a copy of audited annual accounts and a reconciliation statement, duly certified, in FORM GSTR-9C, electronically through the common portal either directly or through a Facilitation Centre notified by the Commissioner.

“Provided that every registered person whose aggregate turnover during the financial year 2018-2019 exceeds five crore rupees shall get his accounts audited as specified under subsection (5) of section 35 and he shall furnish a copy of audited annual accounts and a reconciliation statement, duly certified, in FORM GSTR-9C for the financial year 2018- 2019, electronically through the common portal either directly or through a Facilitation Centre notified by the Commissioner.”.

(Only Reconciliation Statement’s limit increased to 5 Crore)

Notification 16/2020

| Turnover of F.Y. 2018-19 | GSTR-9 | GSTR-9C |

| Upto 2 Crore | Optional | Optional |

| Above Rs. 2Cr but up to Rs. 5Crore | Mandatory | Optional |

| Above Rs. 5Crore | Mandatory | Mandatory |

Rule 89(4)(C) Substituted:- ( Refund on Zero Rated Supply Without Tax under Bond)

“Turnover of zero-rated supply of goods” means

> the value of zero-rated supply of goods made during the relevant period without payment of tax under bond or letter of undertaking or

> the value which is 1.5 times the value of like goods domestically supplied by the same or, similarly placed, supplier, as declared by the supplier,

whichever is less,

other than the turnover of supplies in respect of which refund is claimed under sub-rules (4A) or (4B) or both;‟.

| Particulars | Before amendment | After amendment |

| Zero Rated (10000 Kg @8036/100kg) | 803600 | 803600 |

| Domestic (2000Kg @ 5250/100kg ) | 105000 | 105000 |

| Total ales | 908600 | 908600 |

| ITC | 100000 | 100000 |

| Refund= ITC* Turnover of Zero Rated Supply

Adjusted total Turnover |

100000*803600/908600 | 100000*787500/908600 |

| Turnover of Zero Rated Supply | 803600 | 803600 or

10000*5250/100*1.5= 787500 Whichever is less i.e 787500 |

| Refund | 88443 | 86671 |

Notification No. 16/2020 dated 23.03.2020

New Rule 96B Inserted:-

“96B. Recovery of refund of unutilised input tax credit or integrated tax paid on export of goods where export proceeds not realised. –(1) Where any refund of unutilised input tax credit on account of export of goods or of integrated tax paid on export of goods has been paid to an applicant but the sale proceeds in respect of such export goods have not been realised, in full or in part, in India within the period allowed under the Foreign Exchange Management Act, 1999 (42 of 1999), including any extension of such period, the person to whom the refund has been made shall deposit the amount so refunded, to the extent of non realization of sale proceeds, along with applicable interest within thirty days of the expiry of the said period or, as the case may be, the extended period, failing which the amount refunded shall be recovered in accordance with the provisions of section 73 or 74 of the Act, as the case may be, as is applicable for recovery of erroneous refund, along with interest under section 50:

Provided that where sale proceeds, or any part thereof, in respect of such export goods are not realised by the applicant within the period allowed under the Foreign Exchange Management Act, 1999 (42 of 1999), but the Reserve Bank of India writes off the requirement of realization of sale proceeds on merits, the refund paid to the applicant shall not be recovered.

(2) Where the sale proceeds are realised by the applicant, in full or part, after the amount of refund has been recovered from him under sub-rule (1) and the applicant produces evidence about such realisation within a period of three months from the date of realisation of sale proceeds, the amount so recovered shall be refunded by the proper officer, to the applicant to the extent of realisation of sale proceeds, provided the sale proceeds have been realised within such extended period as permitted by the Reserve Bank of India.”.

Step 1 :- Export of Goods

Step 2 :- Refund

- Unutilised ITC (Export under LUT/BOND)

- Integrated Tax Paid (Export on payment of Tax)

Step 3 :- Export Proceeds not realized (Part or Full)

Within period allowed by FEMA

Step 4 :- Within expiry of 30 days from above said period (Deposit the refund amount+ Interest)

Step 5:- On Non payment= Recovery of amount u/s 73 or 74

Step 6:- Realisation of export proceeds after recovery of refund amount

AND

evidence produced by applicant within three month from realization of sale proceeds

The Amount recovered be refunded

SPECIMEN OF UNDERTAKING

1. I hereby declare that the goods exported are not subject to any export duty. No drawback has been availed / or availed at lower rate by us in respect of central tax and no refund is claimed by us in respect of the integrated tax paid on such supplies in terms of Section 54(3) of CGST/SGST Act.

2. I hereby declare that refund of input tax credit claimed does not include input tax credit availed on goods or services used for making Nil rated or fully exempted supplies.

3. I hereby declare that the incidence of tax, interest or any other amount claimed as refund has not been passed on to any other person in terms of Rule 89(2)(l) of Central Goods and Services Tax (CGST) Rules, 2017.

4. I hereby declare that the GST refund application has been made to one authority only.

5. I hereby undertake that during any period of five years immediately preceding the tax period to which the claim for refund relates, I have not been prosecuted for any offence under the Act or under an existing law where the amount of tax evaded exceeds two hundred and fifty lakh rupees.

6. I hereby undertake to pay back to the government the amount of refund sanctioned along with interest in case it is found subsequently that the requirements of Section 16(2)(c) read with Section 42 of the CGST/SGST Act have not been complied with in respect of the amount refunded.

New Clause in undertaking

“UNDERTAKING

I hereby undertake to deposit to the Government the amount of refund sanctioned along with interest in case of non-receipt of foreign exchange remittances as per the proviso to section 16 of the IGST Act, 2017 read with rule 96B of the CGST Rules 2017.

Signature

Name – Designation / Status”

Notification No. 16/2020 (Rule 43)

| Rule 43 Sub Rule (1) | ITC ON CAPITAL GOODS |

| Clause (a) | Exclusively for Exempt and Non Business Supply |

| Clause (b) | Exclusively for Taxable including Zero Rated |

| Clause (c) | Not covered above (a) and (b) i.e. used for

Commonly AND First covered under Clause (a) Subsequently under Clause (c) (From Exempt to Common) |

| Clause(d) | Commonly

And First covered under Clause (b) Subsequently under Clause (c) (From Taxable to Common) |

–

| Rule 43 (Manner of determination of input tax credit in respect of capital goods and reversal thereof in certain cases.-) | ||||

| Earlier | Now | |||

| -(1) Subject to the provisions of sub-section (3) of section 16, the input tax credit in respect of capital goods, which attract the provisions of sub-sections (1) and (2) of section 17, being partly used for the purposes of business and partly for other purposes, or partly used for effecting taxable supplies including zero rated supplies and partly for effecting exempt supplies, shall be attributed to the purposes of business or for effecting taxable supplies in the following manner, namely,-

(a) the amount of input tax in respect of capital goods used or intended to be used exclusively for non-business purposes or used or intended to be used exclusively for effecting exempt supplies shall be indicated in FORM GSTR-2 [and FORM GSTR-3B] 56 and shall not be credited to his electronic credit ledger; (b) the amount of input tax in respect of capital goods used or intended to be used exclusively for effecting supplies other than exempted supplies but including zerorated supplies shall be indicated in FORM GSTR-2 [and FORM GSTR-3B] 57 and shall be credited to the electronic credit ledger; [Explanation: For the purpose of this clause, it is hereby clarified that in case of supply of services covered by clause (b) of paragraph 5 of the Schedule II of the said Act, the amount of input tax in respect of capital goods used or intended to be used exclusively for effecting supplies other than exempted supplies but including zero rated supplies, shall be zero during the construction phase because capital goods will be commonly used for construction of apartments booked on or before the date of issuance of completion certificate or first occupation of the project, whichever is earlier, and those which are not booked by the said date.]58 |

Same |

|||

| (c) the amount of input tax in respect of capital goods not covered under clauses (a) and (b), denoted as ‗A‘, shall be credited to the electronic credit ledger and the useful life of such goods shall be taken as five years from the date of the invoice for such goods:

Provided that where any capital goods earlier covered under clause (a) is subsequently covered under this clause, the value of ‗A‘ shall be arrived at by reducing the input tax at the rate of five percentage points for every quarter or part thereof and the amount ‗A‘ shall be credited to the electronic credit ledger; Explanation.– An item of capital goods declared under clause (a) on its receipt shall not attract the provisions of sub-section (4) of section 18, if it is subsequently covered under this clause. |

“c) the amount of input tax in respect of capital goods not covered under clauses (a) and (b), denoted as ‘A’, being the amount of tax as reflected on the invoice, shall credit directly to the electronic credit ledger and the validity of the useful life of such goods shall extend upto five years from the date of the invoice for such goods:

Provided that where any capital goods earlier covered under clause (a) is subsequently covered under this clause, input tax in respect of such capital goods denoted as “A‟ shall be credited to the electronic credit ledger subject to the condition that the ineligible credit attributable to the period during which such capital goods were covered by clause (a),denoted as “Tie‟, shall be calculated at the rate of five percentage points for every quarter or part thereof and added to the output tax liability of the tax period in which such credit is claimed:

Provided further that the amount „Tie‟ shall be computed separately for input tax credit of central tax, State tax, Union territory tax and integrated tax and declared in FORM GSTR-3B. Explanation.- An item of capital goods declared under clause (a) on its receipt shall not attract the provisions of sub-section (4) of section 18, if it is subsequently covered under this clause.” |

|||

| (d) the aggregate of the amounts of ‘A‘ credited to the electronic credit ledger under clause (c), to be denoted as ‘Tc‘, shall be the common credit in respect of capital goods for a tax period:

Provided that where any capital goods earlier covered under clause (b) is subsequently covered under clause (c), the value of ‗A‘ arrived at by reducing the input tax at the rate of five percentage points for every quarter or part thereof shall be added to the aggregate value ‗Tc‘; (e) the amount of input tax credit attributable to a tax period on common capital goods during their useful life, be denoted as ‗Tm‘ and calculated as Tm= Tc÷60 |

(d)“the aggregate of the amounts of “A‟ credited to the electronic credit ledger under clause (c) in respect of common capital goods whose useful life remains during the tax period, to be denoted as “Tc‟, shall be the common credit in respect of such capital goods:

Provided that where any capital goods earlier covered under clause (b) are subsequently covered under clause (c), the input tax credit claimed in respect of such capital good(s) shall be added to arrive at the aggregate value “Tc‟; (e) the amount of input tax credit attributable to a tax period on common capital goods during their useful life, be denoted as ‗Tm‘ and calculated as Tm= Tc÷60 “Explanation.- For the removal of doubt, it is clarified that useful life of any capital goods shall be considered as five years from the date of invoice and the said formula shall be applicable during the useful life of the said capital goods.”; |

|||

| Rule 43 (Manner of determination of input tax credit in respect of capital goods and reversal thereof in certain cases.-) | ||||

| Earlier

|

Now | |||

| (f) the amount of input tax credit, at the beginning of a tax period, on all common capital goods whose useful life remains during the tax period, be denoted as ‗Tr‘ and shall be the aggregate of ‗Tm‘ for all such capital goods;

(g) the amount of common credit attributable towards exempted supplies, be denoted as ‗Te‘, and calculated as Te= (E÷ F) x Tr where, ‘E‘ is the aggregate value of exempt supplies, made, during the tax period, and ‘F‘ is the total turnover [in the State] 59 of the registered person during the tax period: [Provided that in case of supply of services covered by clause (b) of paragraph 5 of the Schedule II of the Act, the value of ‗E/F‘ for a tax period shall be calculated for each project separately, taking value of E and F as under: |

(f) the amount of input tax credit, at the beginning of a tax period, on all common capital goods whose useful life remains during the tax period, be denoted as ‗Tr‘ and shall be the aggregate of ‗Tm‘ for all such capital goods;

Omitted Same (Drafting Error(Clause f deleted but clause g not altered for Tr)

|

|||

Notification No. 16/2020 ( Rule 43)

Eg. Capital good-Machinery was purchased and received on 10.07.2017 along with invoice on which IGST charged on invoice was Rs. 6,00,000. Till December 2017, it was being used for effecting exempt supplies. But from January 2018 onwards, it was used commonly for effecting taxable supplies and exempt supplies.

| Turnover Type | January 2018 |

| Exempt | 4 Crores |

| Total | 10 Crores |

Since upto December 2017, it was being used for effecting exempt supplies, ITC would have not been taken upto December 2017.

ITC finalized upto December 2017 = ITC less 5% for every Quarter

Amount for 2 Quarters= 5%*2 of 600000=60000

So, out of Rs. 6,00,000, self-assessment of ITC of Rs. 60,000 has become final. In other words, since it was being used from July 2017 to December 2017 (i.e. for 2 quarters) for effecting exempt supplies, proportionate amount of ITC i.e. Rs. 60,000 shall not be allowed.

Balance Amount=600000-60000=Rs. 540000/-

| OLD LAW vs. NEW LAW

Calculation of ITC in respect of said capital goods for January 2018 |

|||

| Particulars | Remark / calculation | Amount (OLD) | Amount (New) |

| Amount to be credited in electronic credit ledger “A” | A | 5,40,000 | 6,00,000 |

| **Amount to be added in output tax liability (ii) | Tie

(To be calculated separately for I/C/S) |

–

(Net ITC added) |

60,000 |

| **Amendment to Rule 43(1)(C ) Proviso inserted specifies that it shall be added to output tax liability. | |||

| Input Credit Attributable to Month (When divided for Monthly Credit)(5 years Life) | Tm | 540000/60=9000 (where as the amount should have been written of in balance life) | 600000/60=10000

(Anomaly Cleared) |

| Per month | Te=Tm*E/F | 9000*4/10=3600 | 10000*4/10=4000 |

–

| Integrated Tax | |||||

| Capital Goods | Input Tax Credit (As per Invoice) |

Usage | Date of Purchase | Date of Shifting | |

| No.1 | 700000 | Used Exclusively for Taxable supply | January, 2020 | – | |

| No.2 | 200000 | Used Exclusively for Exempt Supply | January, 2020 | – | |

| No. 3 | 400000 | Commonly used | January, 2020 | – | |

| No. 4 | 480000 | 1stly used for taxable supply then common | May, 2018 | January, 2020 | Full Credit of Rs. 480000 would have already availed in May,2018 |

| No. 5 | 600000 | 1stly used for Exempt supply then common | July,2019 | January, 2020 | No credit wud have been availed in July, 2019 |

| Exempt Sales for Jan, 2020 | 4 crores | ||||

| Total Sales for Jan, 2020 | 10 crores | ||||

| For the Month of January,2020 | |||||

| No. 1 | Full Credit | 700000 | Rule 43(1)(b) | ||

| No. 2 | Credit | 0 | Rule 43(1)(a) | ||

| No. 3 | Credit | 400000 | Rule 43(1)© | Common Use | |

| No. 4 | Credit | 0 | Already Availed | Now Common Use | Shift from (b) to © |

| No. 5 | Credit | 600000 | Now Common Use | Shift from (a) to © | |

| Amount to be added in ECL in Jan, 2020 | 1700000 | ||||

–

| Reversal Calculation | ||||||

| Tie on CG No. 5 @5% per Quarter | Rule 43(1)© Proviso | 60000 | 600000*.05*2 | (Amendment) | ||

| Rule 43(1)© Common Credit | ||||||

| No. 3 | A | 400000 | ||||

| No. 4 | A | 480000 | ||||

| No. 5 | A | 600000 | (Amendment) | |||

| Rule 43(1)(d) | Tc | 1480000 | Only those Assets to be taken whose life remains during Tax Period | |||

| Rule 43(1)€ | Tm=Tc/60 | 24666.67 | ||||

| Rule 43(1)(g) | Te=Tm*E/F | 9866.667 | Reversal of Credit on Capital Goods owing to Common Usage | |||

| Amount to be Reversed in January, 2020 | 69866.67 | |||||

| In the Month of Feb, 2020

|

||||||

| No. 6 | 200000 | Commonly used | February, 2020 | |||

| Amount to be added in ECL in Feb, 2020 | 200000 | |||||

–

| Reversal Calculation | |||

| Tie on CG No. 5 @5% per Quarter | 0 | ||

| Rule 43(1)© Common Credit | |||

| No. 3 | A | 400000 | |

| No. 4 | A | 480000 | |

| No. 5 | A | 600000 | |

| No. 6 | A | 200000 | |

| 1680000 | |||

| Rule 43(1)€ | Tm=Tc/60 | 28000 | |

| Rule 43(1)(g) | Te=Tm*E/F | 11200 | Reversal of Credit on Capital Goods owing to Common Usage |

| (Assuming Same Sales this month)

|

|||

| Amount to be Reversed in Feb, 2020 | 11200 | ||

Notification No. 10/2020 dated 23.03.2020

Special procedure for taxpayers in Dadra and Nagar Haveli and Daman and Diu consequent to merger of the two UTs has been notified:-

The procedure notified can be summarized as follows:

1) The transition date is 31st May 2020 and the transition period is defined from 27th January till till 31st May 2020.

2) The return period of January and February 2020 have been redefined.

3) The balance in the electronic credit ledger and the ITC registered in the account of the erstwhile GSTIN of the two Union Territories shall stand transferred to the newly allotted GSTIN in the merged Union Territory.

Notification No. 11/2020 dated 23.03.2020

Special procedure for corporate debtors undergoing the corporate insolvency resolution process under the Insolvency and Bankruptcy Code, 2016 notified.

The procedure notified can be summarised as follows:

1. The procedure is applicable to the corporate debtors who are undergoing the corporate insolvency resolution process and the management of whose affairs are being undertaken by interim resolution professionals (IRP) or resolution professionals (RP) under the Insolvency and Bankruptcy Code, 2016 (IBC).

2. New GST registration is required to be taken.

3. First return under section 40 of the CGST Act must be filed by the IRP/RP.

4. IRP/RP can avail the ITC belonging to the account of the old registration under the new GSTIN in the first return.

5. Amount in the cash ledger of the old account can be transferred to the new account.

Notification No. 12/2020 dated 23.03.2020

Waiver of GSTR-1 for the period of FY 2019-20 for the interested composition dealers who could not opt for Special Composition as per Not. 2/2019

Those taxpayers who filed GSTR-3B instead of CMP-08 are exempted from the requirement of filing GSTR-1 for all the periods in FY 2019-20.

Notification No. 13/2020 dated 23.03.2020

Certain class of registered persons are exempted from issuing e-invoices and the date for implementation of e-invoicing is extended to 1st October 2020.

The implementation of the e-Invoicing system stands deferred to 1st October 2020 for persons whose aggregate turnover in a financial year exceeds Rs. 100 crores.

Further, sectors such as banking, insurance, Goods transport agency (GTA), passenger transportation service, and selling of movie tickets are exempted from e-Invoicing.

Notification No. 14/2020 dated 23.03.2020

QR code requirement for B2C invoicing is applicable from 1st October 2020.

Dynamic Quick Response Code (QR Code) required for B2C invoices where the turnover of the taxpayer is more than Rs 500 crore in the previous financial year stands deferred to 1st October 2020.

Further, sectors such as banking, insurance, Goods transport agency (GTA), passenger transportation service, and selling of movie tickets are exempted.

Notification No. 15/2020 dated 23.03.2020

The time limit for furnishing of the annual return specified under section 44 of CGST Act, 2017 for the financial year 2018-2019 is extended

The last date for furnishing GSTR-9 and GSTR-9C stands extended for FY 2018-19 till 30th June 2020.

Notification No. 17/2020 dated 23.03.2020

The class of persons who shall be exempted from Aadhaar authentication has been notified

Any person who is not a citizen of India or belong to a class of persons, except the persons mentioned below, are not required to get an aadhaar authentication done, from 1st April 2020:

1. Individual

2. Authorised signatory of all types

3. Managing and Authorised partner, and

4. Karta of an Hindu undivided family.

Notification No. 18/2020 dated 23.03.2020

The effective date for Aadhaar authentication before obtaining GST registration is notified.

The effective date for Aadhaar authentication before obtaining GST registration is notified.

Notification No. 19/2020 dated 23.03.2020

The class of persons, other than individuals who shall undergo authentication of Aadhaar number to be eligible for registration, has been notified.

The following persons shall undergo the aadhaar authentication from 1st April 2020:

1. Authorised signatory of all types,

2. Managing and Authorised partners of a partnership firm, and

3. Karta of an Hindu undivided family

Notification No. 20/2020 dated 23.03.2020

Extension of due dates for filing GSTR-7 for the registered taxpayers of Jammu and Kashmir.

For the tax periods July 2019 to October 2019 and November 2019 to February 2020, the GSTR-7 return can be filed before 24th March 2020, by the taxpayers registered in Jammu and Kashmir. The notification comes into effect from 20th December 2019.

| Due Dates Specified Territories | |||||

| Month | Return | New Due Date | Territory | Turnover | Notification no. |

| Oct 2019 | GSTR 3B | 24.03.2020 | Jammu & Kashmir | – | N.N. 25/2020 |

| Nov 2019 to Feb 2020 | GSTR 3B | 24.03.2020 | Union territory of Jammu and Kashmir or the Union territory of Ladakh | – | N.N. 25/2020 |

| July 2019 to Sept 2019 | GSTR 3B | 24.03.2020 | Jammu & Kashmir | – | N.N. 26/2020 |

| April 2020 to June 2020 | GSTR-1 | 31.07.2020 | All States | < 1.5 cr | N.N. 27/2020 |

| July 2020 to Sept 2020 | GSTR-1 | 31.10.2020 | All States | < 1.5 cr | N.N. 27/2020 |

| Apr 2020 to Sept 2020 | GSTR-1 | 11th of Succeeding month | All States | > 1.5 cr | N.N. 28/2020 |

| July 2019 to October 2019 | GSTR 7 | 24.03.2020 | Jammu & Kashmir | – | N.N. 20/2020 |

| Nov 2019 to Feb 2020 | GSTR 7 | 24.03.2020 | Jammu & Kashmir, Union Territory of Ladakh | – | N.N. 20/2020 |

| July 2019 to Sept 2020 | GSTR-1 | 24.03.2020 | Jammu & Kashmir | < 1.5 cr | N.N. 24/2020 |

| Oct 2019 to Dec 2020 | GSTR-1 | 24.03.2020 | Jammu & Kashmir, Union Territory of Ladakh | < 1.5 cr | N.N. 21/2020 |

| July 2019 to Oct 2019 | GSTR-1 | 24.03.2020 | Jammu & Kashmir | > 1.5 cr | N.N. 22/2020, N. N. 23/2020 |

| Nov 2019 to Feb 2020 | GSTR-1 | 24.03.2020 | Jammu & Kashmir, Union Territory of Ladakh | > 1.5 cr | N.N. 22/2020 |

–

| Due Dates Specified Territories | |||||

| Month | Return | New Due Date | Territory | Turnover | Notification no. |

| April 2020 to Sept 2020 | GSTR 3B | 20th of Succeeding month | Chhattisgarh, Madhya Pradesh, Gujarat, Maharashtra, Karnataka, Goa, Kerala, Tamil Nadu, Telangana, Andhra Pradesh, the Union territories of Daman and Diu and Dadra and Nagar Haveli, Puducherry, Andaman and Nicobar Islands or Lakshadweep | – | N.N. 29/2020 |

| 24th of succeeding month | GSTR 3B | 24th of succeeding month | Himachal Pradesh, Punjab, Uttarakhand, Haryana, Rajasthan, Uttar Pradesh, Bihar, Sikkim, Arunachal Pradesh, Nagaland, Manipur, Mizoram, Tripura, Meghalaya, Assam, West Bengal, Jharkhand or Odisha, the Union territories of Jammu and Kashmir, Ladakh, Chandigarh or Delhi | – | N.N. 29/2020 |

List of Notifications

| Notification No. | Description |

| 10/2020 | Seeks to provide special procedure for taxpayers in Dadra and Nagar Haveli and Daman and Diu consequent to merger of the two Uts |

| 11/2020 | Seeks to provide special procedure for corporate debtors undergoing the corporate insolvency resolution process under the Insolvency and Bankruptcy Code, 2016 |

| 12/2020 | Seeks to waive off the requirement for furnishing FORM GSTR-1 for 2019-20 for taxpayers who could not opt for availing the option of special composition scheme under notification No. 2/2019-Central Tax (Rate) |

| 13/2020 | Seeks to exempt certain class of registered persons from issuing e-invoices and the date for implementation of e-invoicing extended to 01.10.2020 |

| 14/2020 | Seeks to exempt certain class of registered persons capturing dynamic QR code and the date for implementation of QR Code to be extended to 01.10.2020 |

| 15/2020 | Seeks to extend the time limit for furnishing of the annual return specified under section 44 of CGST Act, 2017 for the financial year 2018-2019 till 30.06.2020. |

| 16/2020 | Seeks to make third amendment (2020) to CGST Rules |

| 17/2020 | Seeks to specify the class of persons who shall be exempted from aadhar authentication. |

| 18/2020 | Seeks to notify the date from which an individual shall undergo authentication, of Aadhaar number in order to be eligible for registration. |

| 19/2020 | Seeks to specify class of persons, other than individuals who shall undergo authentication, of Aadhaar number in order to be eligible for registration. |

| 20/2020 | Seeks to extend due date for furnishing FORM GSTR-7 for those taxpayers whose principal place of business is in the erstwhile State of Jammu and Kashmir for the July, 2019 to October,2019 and November, 2019 to February, 2020 . |

| 21/2020 | Seeks to extend due date for furnishing FORM GSTR-1 for registered persons whose principal place of business is in the erstwhile State of Jammu and Kashmir or the Union territory of Jammu and Kashmir or the Union territory of Ladakh for the quarter October-December, 2019 till 24th March, 2020 |

| 22/2020 | Seeks to extend due date for furnishing FORM GSTR-1 for registered persons whose principal place of business is in the erstwhile State of Jammu and Kashmir, and having aggregate turnover of more than 1.5 crore rupees in the preceding financial year or current financial year, for the month of October, 2019 and November, 2019 to February till 24th March, 2020. |

| 23/2020 | Seeks to extend due date for furnishing FORM GSTR-1 for registered persons whose principal place of business is in the erstwhile State of Jammu and Kashmir, by such class of registered persons having aggregate turnover of more than 1.5 crore rupees in the preceding financial year or current financial year, for each of the months from July, 2019 to September, 2019 till 24th March, 2020. |

| 24/2020 | Seeks to extend due date for furnishing FORM GSTR-1 for registered persons whose principal place of business is in the erstwhile State of Jammu and Kashmir, for the quarter July-September, 2019 till 24th March,2020. |

| 25/2020 | Seeks to extend due date for furnishing FORM GSTR-3B for the months of October, 2019 , November, 2019 to February, 2020 for registered persons whose principal place of business is in the erstwhile State of Jammu and Kashmir on or before the 24th March, 2020. |

| 26/2020 | Seeks to extend due date for furnishing FORM GSTR-3B of the said rules for the months of July,2019 to September, 2019 for registered persons whose principal place of business is in the erstwhile State of Jammu and Kashmir, shall be furnished electronically through the common portal, on or before the 24th March, 2020 |

| 27/2020 | Seeks to prescribe the due date for furnishing FORM GSTR-1 for the quarters April, 2020 to June, 2020 and July, 2020 to September, 2020 for registered persons having aggregate turnover of up to 1.5 crore rupees in the preceding financial year or the current financial year. |

| 28/2020 | Seeks to prescribe the due date for furnishing FORM GSTR-1 by such class of registered persons having aggregate turnover of more than 1.5 crore rupees in the preceding financial year or the current financial year, for each of the months from April,2020 to September, 2020. |

| 29/2020 | Seeks to prescribe return in FORM GSTR-3B of CGST Rules, 2017 along with due dates of furnishing the said form for April, 2020 to September, 2020 |

| 30/2020 | Seeks to amend CGST Rules (Fourth Amendment) in order to allow opting Composition Scheme for FY 2020-21 till 30.06.2020 and to allow cumulative application of condition in rule 36(4). |

| 31/2020 | Seeks to provide relief by conditional lowering of interest rate for tax periods of February, 2020 to April, 2020. |

| 32/2020 | Seeks to provide relief by conditional waiver of late fee for delay in furnishing returns in FORM GSTR-3B for tax periods of February, 2020 to April, 2020. |

| 33/2020 | Seeks to provide relief by conditional waiver of late fee for delay in furnishing outward statement in FORM GSTR-1 for tax periods of February, 2020 to April, 2020. |

| 34/2020 | Seeks to extend due date of furnishing FORM GST CMP-08 for the quarter ending March, 2020 till 07.07.2020 and filing FORM GSTR-4 for FY 2020-21 till 15.07.2020. |

| 35/2020 | Seeks to extend due date of compliance which falls during the period from “20.03.2020 to 29.06.2020” till 30.06.2020 and to extend validity of e-way bills. |

| 36/2020 | Seeks to extend due date for furnishing FORM GSTR-3B for supply made in the month of May, 2020. |

| CA Aanchal Kapoor | CA Rohit Kapoor |

| aanchalkapoor_ca@yahoo.com | rohitkapoorca@yahoo.com |