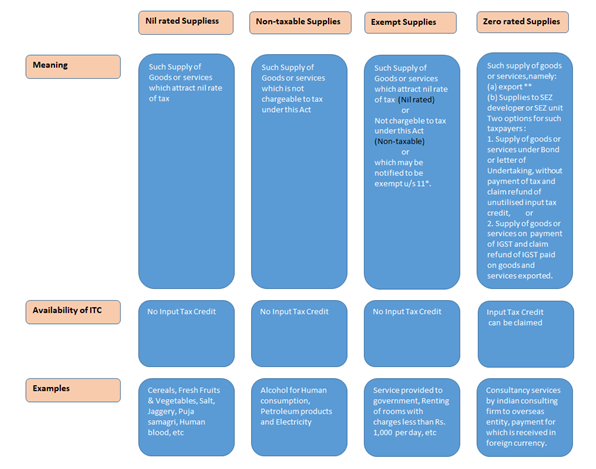

With the Introduction of Goods and service Tax(GST), the traders are left confused with some of the provisions of the Act. Taking into consideration one such tangled provision, as to what is the difference between Nil rated and zero rated supplies, as well as non-taxable and exempt supplies.

While the end result of all these supplies is the same, i.e. GST is not charged on the supply. But, from the reporting point of view, a clear bifurcation is required to be furnished in the GST Returns.

Schedule to GST law prescribe the rate of GST for supply of goods and services. These rates are fixed by the parliament and changing these rates is time consuming.

However, Government needs flexibility in operating of taxing statute. As the circumstances change, quick adoption to changing situation is required.

* Hence, As per section 11(1), of CGST and SGST Act, Central/State government has been granted the power to reduce GST rates as per requirements, by issuing a general exemption notification. The notification can be issued only on the basis of recommendation of the GST council. The exemption should be in public interest.

The general exemption can be general either absolutely or subject to such conditions as may be specified in the notification. The exemption can be absolute (unconditional) or subject to conditions. The exemption can be in respect of goods or services or both of any specified description. Exemption can be from the whole or any part of the tax leviable thereon.

There is identical provision in section 6(1) of IGST Act.

** Export of Goods or Services

“Export of goods” means taking goods out of India to a place outside India.

“Export of services” means the supply of any service when:

(a) the supplier of service is located in India,

(b) the recipient of service is located outside India,

(c) the place of supply of service is outside India,

(d) the payment for such service has been received by the supplier of service in convertible foreign exchange, and

(e) the supplier of service and recipient of service are not merely establishments of a distinct person in accordance with explanation 1 of section 5;

As per Explanation 1 of Section 5:

(i) an establishment of a person in India and any of his establishments outside India, or

(ii)an establishment of a person in a state and any of his other establishments outside that state,

shall be treated as establishments of distinct persons.

Deemed export means the goods supplied, do not leave India and the payment for such supplies is received either in Indian rupees or in convertible foreign exchange, if such goods are manufactured in India.

Author Bio

Alcohol for human consumption is not the right example for non-taxable supplies.

Dear mam

Will schedule III items which are non supply ,come under exempt supply ? Also 28th GSTC has made some changes in ITC with respect to Schedule III. Can you explain ?

Respected mam,

I am trading in grains and pulses item HSN code 0713

can u tell me that these item r NIL rated Or EXEMPT item please guide me for proper bifurgation , and secondly I am selling these goods to interstate supplies

attarcts E-Way bill

Thanks

Dear Madam / Sir,

i have two following question……………

1.Fresh Mushroom (hsn code -07095100)

Compost (3100000) both are fully exempt tell me can i claim itc on purchase taxable raw material & claim refund Tax which i pay against taxable purchase.

2. Is applicable RCM on freight for Exempt Suppliers because mushroom cultivation is agriculture activity.

A person gives costumes, dress materials to school children and participants for functions in school colleges and artificial jewellery on rent basis. The receipts are hardly Rs. 1 lakh a year. GST is levialble on such services?? Kindly clarify.

atulkakkad@gmail.com

Thank you mam for your posting. Please refer examples quoted by you for Non taxable supplies i.e Electricity. If you see the Section 2 ( 78) and Section 9 of CGST act it is no where mentioned that the ” Electricity” as non taxable supply. Please clarify

Thanks Shikha.

CAN A CHARTERED ACCOUNTANT , WHO IS THE EXISTING MEMBER OF THE INSTITUTE BUT NOT HOLDING THE CERTIFICATE OF PRACTICE ,

APPLY TO GST AUTHORITIES FOR PRACTICING

GST MATTERS ONLY ?

Can u brief diff BTW Nil rated n zero rated

Dear Sir,

you have mentioned Electricity under Non- Taxable supplies but in my opinion , electricity comes under Exempt category.

Kindly refer following.

Explanation is given in section should be 8 (1) instead of 5(1).

As per Explanation 1 of Section 5:

(i) an establishment of a person in India and any of his establishments outside India, or

(ii)an establishment of a person in a state and any of his other establishments outside that state,

shall be treated as establishments of distinct persons.

Is there any logjam in enrollment of GST Practitioner ? From last 7/8 months application for GST Practitioner are not processed. Can you enlighten in your article ?