Introduction

GSTR 9 is the form prescribed for filing Annual Return under Goods and Services Tax. Whether forcibly or voluntarily, businesses across nation now have become familiar with the provisions of the Goods and Services Tax including various amendments done on almost daily basis. Within a few months of the GST implementation there was a flood of amendment notifications and one of them concerns GST Audit and GST Returns. The last date of filing of GSTR 9 i.e. the Annual Return has been revised and finalized as 30th June 2019 i.e. return for the period July 2017- March 2018 is 30th June 2019. Prior this the return was required to be filed by 31st Dec 2018 which was extended to 30th June 2019 during 31st GST Council Meeting held on 22nd Dec 2018.

The Annual Return is an important document as the facts/ figures/ data disclosed in this document carries various implications. Any incorrect information may attract serious amount of litigations and dipsutes with the concerned tax authorities and accordingly the assesse may face various hardships. In this article, an attempt has been made to explore the inclusions and parts of the return for the ease of understanding of the readers and assesses.

Page Contents

- 1. What is a GSTR-9 Annual Return?

- 2. Terms of Reference

- 3. Who is required to file GSTR -9 Annual Return?

- 4. What are the details required in the GSTR-9 form?

- 5. Key Points one must keep in mind before filing of Annual Return

- 6. How GSTR 9 is prepared?

- 7. Issue/s with the Annual Return- GSTR 9

- 8. Penalty for filing GSTR with a delay?

- 9. Can GSTR 9 be revised?

1. What is a GSTR-9 Annual Return?

GSTR 9 form is an annual return to be filed once in a year by the registered taxpayers under GST. It consists of details regarding the supplies made and received during the year under different tax heads i.e. CGST, SGST and IGST. It consolidates the information furnished in the monthly or quarterly returns during the year.

2. Terms of Reference

– It is an Annual Return, in other words it is a consolidation of all the GST returns filed in the particular year.

– It is to be filed by the GST registered taxpayer

– Following are the exceptions i.e. the assesees who are not required to file GSTR 9

- Casual Taxable Person

- Non Resident Taxable person

- Input service distributor

- Composition Dealers

- Assesees subject to TCS and TDS provisions

– Certification by CA/ CMA not required instead attestation by the tax payer using a digital signature

3. Who is required to file GSTR -9 Annual Return?

As per Chapter 8 – Sec 80 of the act, every registered person except a few stated in the law is required to furnish an annual return electronically in FORM GSTR 9 through a common portal either directly or through a facilitation centre.

The exceptions here are

– Input Service Distributor

– a person paying tax under section 51 or section 52

– a casual taxable person and a non-resident taxable person

4. What are the details required in the GSTR-9 form?

There are 6 parts of the Annual Return Form GSTR 9 which have been explained as follows-

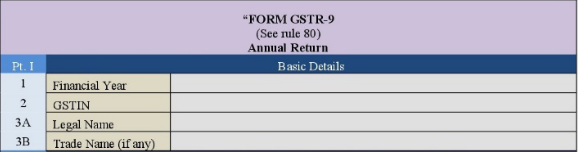

Part 1

This part of the Return form consists of the basic details of the tax payer and this gets auto populated when the basis information is entered into the system.

Part 2

This part of the return covers the outward and inward supply details declared during the financial year. It is important to note that this detail must be taken from the consolidated values of the GST returns filed during the previous year by the assesee.

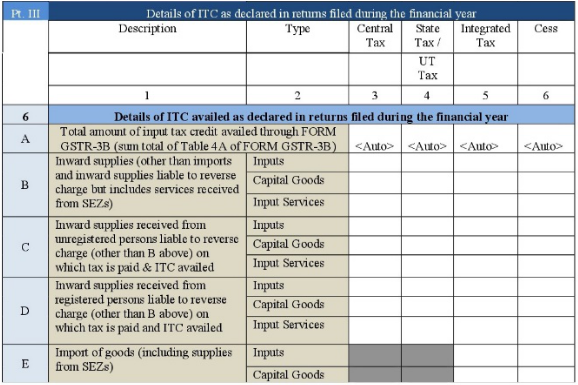

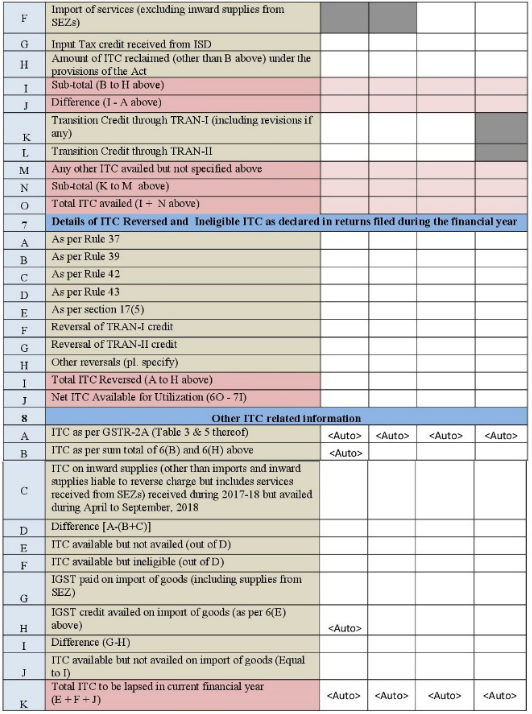

Part 3

This part of the return consists of the details of the Input Tax Credit declared in the returns filed during the Financial Year. This will also be a consolidated figure from the previous returns filed in the previous years under the GST tenure.

Part 4

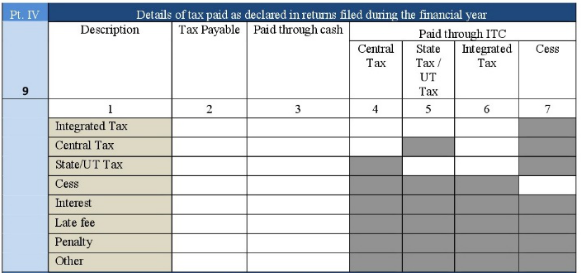

This part of the return consists of the details of the tax paid as declared in the returns filed during the Financial Year.

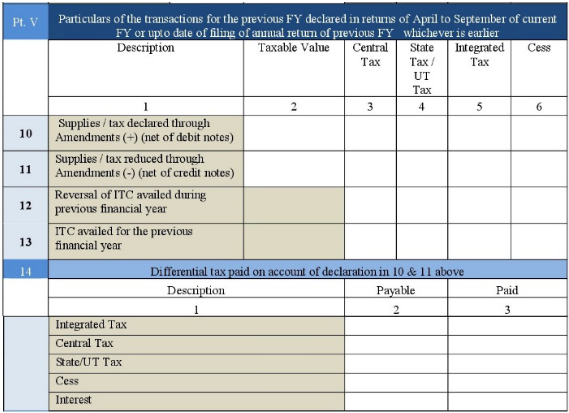

Part 5

This part of the return consists of the particulars for the previous financial year declared in returns of April to September of current financial Year or upto the date of filing of annual returns of previous financial years whichever is earlier. It may consist of the summary of the amendment or omission of the entries belonging to the previous Financial Year but reported in the current FY.

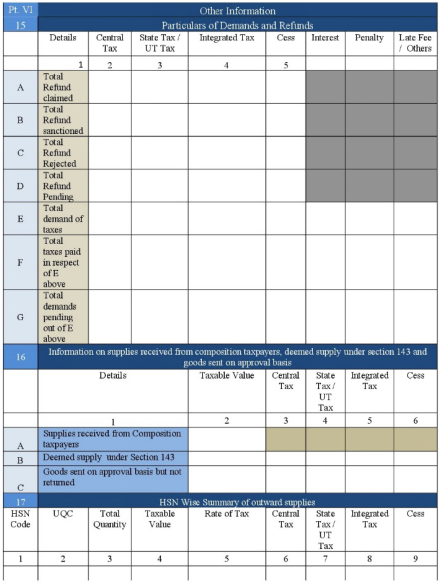

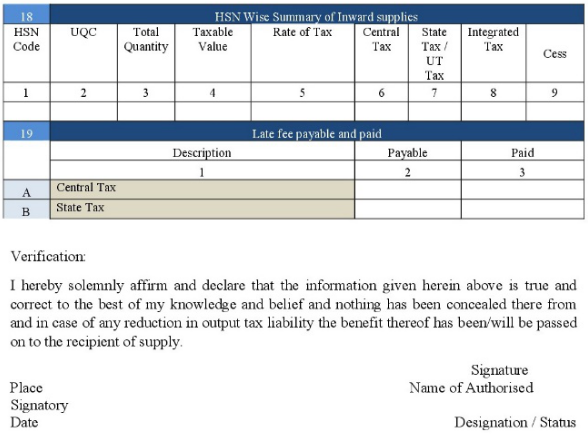

Part 6

This part of the return consists of the other information which comprises of-

– GST demands and refunds

– HSN wise summary information of the quantity of goods supplied and received

– Corresponding tax numbers of the above information

– Late fees payable and paid details

– Segregation of the inward supplies received from the different categories of taxpayers like composition dealers, deemed supply and goods supplied on approval basis.

5. Key Points one must keep in mind before filing of Annual Return

√ Reconciliation of the books of accounts and tax invoices issued since inception of GST in July 2017 till March 2018

√ The above reconciliation should match with the annual turnover declared by the businessmen in their audited financial statements.

√ Matching of the stock transfers in between the units and branches of the company with the books of accounts

√ E way bill data should be matched with the tax invoices issued since inception of GST i.e. July 2017 till March 2018.

√ Proper and correct availment of Input tax Credit should be ensured.

√ The purchase and service invoices should be accounted for properly

√ The purchase data by the suppliers should have been uploaded by the suppliers properly which will be reflected in GSTR 2A form

√ Quarterly and monthly reconciliation of all the GST Returns with the books of accounts to avoid any disparity.

√ Input Tax Credit should have been paid only on such invoives on which payment to suppliers has been made within 180 days of the invoices

√ Relevant and applicable provisions of Reverse Charge Mechanism should also be taken into account

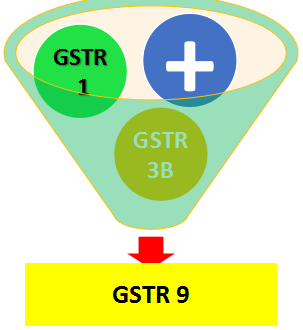

6. How GSTR 9 is prepared?

There are two main ingredients for compiling GSTR 9 i.e. GSTR 1 and GSTR 3 B

7. Issue/s with the Annual Return- GSTR 9

The Government while devising the format of GSTR 9 must have taken adequate care for including all the necessary details and its proper liking with the other two returns from which the information etc will be clubbed and included in the GSTR 9 format. However there are certain grey areas which have not been addressed in the form of Annual Return. The same have been reproduced as below-

– Bifurcated details of ITC availed are required as Inputs and Input Services and Capital goods

– The reporting of the amended transactions which are relevant to FY 2017-18 filed in the 6 monthly returns pertaining to the period April-Sept of the current FY or upto the filing of the return of fy 2017-18 i.e. 31st Dec 2018 whichever is earlier.

– The details w.r.t. to the HSN of the inward supplies was not required while filing monthly GSTR 3 B, however the HSN wise detail of the inward supplies is required in the Annual return GSTR 9.

– Restriction on the reporting of the HSN wise details i.e.the summary is restricted only to those HSN codes wherein such HSN codes accounts for atleast 10% of the total summary of inward supplies.

– The disagreements in the annual return as per the books of accounts and GST data filed during the financial year is also a matter of concern. There is an option for the assesee that either the value of the goods can be declared as per the books or as per the returns already filed by the assesee.

8. Penalty for filing GSTR with a delay?

If the GSTR 9 return is not filed on time then a penalty of Rs. 100 per day under CGST Act and Rs. 100 per day under SGST Act shall be levied i.e. a total of Rs. 200 per day. It is pertinent to mention that the maximum amount of penalty will be an amount calculated at a quarter percent of the total taxpayer turnover in the respective state or Union Territory. In addition to the late fees, the law also imposes an interest @18% per annum which will be calculated on the outstanding tax amount.

9. Can GSTR 9 be revised?

The form GSTR 9 once filed cannot be revised. Any mistake in the return can only be revised in the next month’s return when the error / omission is identified.

Good article.

Would like to highlight a grey area observed in the auto-populated GSTR-9.

I observed that for a registration, that values of b2b supplies as in auto-populated GSTR-9 differ from those in consolidated GSTR-3B.

Any inputs on the same