It just so happened that India had to implement a dual model GST, not that it was an inspiration from Canada or Brazil, but because of the structure of the country. Not to doubt the intentions of the government, we have come very far from the gloomy days of sales tax, [except the ones who drink (Entry 51) and drive (Entry 54)].

The dual-levy model doesn’t make a lot of difference to the Central Government (‘CG’), because one half of the tax pool of any taxable supply (be it CGST or 50% of the IGST] belongs to them. The States Governments (‘SG’) though have the fight of their own, who gets what depends on where the supply occurs. The question, therefore, this article deals is “Where?” where the supply occurs such that its tax is bestowed to that SG (or CG) where it has occurred. The Romans called it ‘Situs of a tax event’, Google calls it ‘the place to which for purposes of legal jurisdiction or taxation a property belongs’. The connotations and relative impact of ‘situs’ over the machinery provisions of the Central Goods and Services Tax Act, 2017 (‘GST law’) are conversed as below;

Page Contents

- 1. Situs – An inherent jurisdictional limitation

- 2. Interplay between Situs of supply and Place of supply

- 3. The situs test under CST Act

- 4. Extra-territorial Jurisdictional Limitation

- 5. Illustrative cases with potential disharmony

- 5.1 Situs of supply of Duty Credit Scrips (DCS)/ Intangibles

- 5.2 Consumption – where the tax chain stops

- 5.3 An off-location supply – bypassing intermediate consumption

- 5.4 An off-shore employee – situs qua taxable person?

- 5.5 Outside India but not export – Forex conundrum

- 5.6 Outside India but not export – Draining State – Enriching Centre

- 5.7 Drop Shipments

- 5.8 Mediocrity at the Airports

- 5.9 Situs of services

- 5.9.1 Activities vis-à-vis Events Outside India

- 5.9.2 Activities vis-à-vis subjects outside India

- 5.9.3 Activities vis-à-vis situs of the recipient, not beneficiary

- 5.10 Situs of services relating to Immovable Property

- 5.11 Situs of origination – Horizontal Split of IT Enabled Services (‘ITES’)

- 5.12 Situs of origination – Project Site of contractor

- 5.13 Situs of ‘Supply’ or ‘Element of Supply’

- 5.14 An illusory situs

- 5.15 The tussle between States

1. Situs – An inherent jurisdictional limitation

The world is not a global village, it is divided of powers by the mega powers. The powers that no mega powers want to dilute or give away. Indian Parliament wouldn’t permit any of the world government to collect taxes in India, and it goes both ways. Just this obvious is put in literal by Article 245 of the Constitution of India (‘the Constitution’). In terms of Article 245 (1) ibid, the Parliament/ State Legislature can make laws for the whole of the country or the state respectively. For the very reasons, the preambles of the laws incorporates the language that “It extends to the whole of India/ State”- Section 1 (2) of GST Law.

A jurisdictional limitation, therefore, flows from both Article 245 ibid and Section 1 ibid. In the body of law, Parliament can put in anything, but all the provisions shall be subject to Section 1 ibid, and anything contrary would not only be ultra-virus and unconstitutional but also in the direct conflict with the international practice also. The term “situs” qua tax event can be said to be analogous with the valid territorial jurisdiction of the event. The Supreme Court of Philippines in a century-old judgment in case of Manila Gas Corporation vs Collector of Internal Revenue[1] had brilliantly worded;

The approved doctrine is that no state may tax anything not within its jurisdiction without violating the due process clause of the constitution. The taxing power of a state does not extend beyond its territorial limits, but within such limits it may tax persons, property, income, or business. If an interest in property is taxed, the situs of either the property or interest must be found within the state. If an income is taxed, the recipient thereof must have a domicile within the state or the property or business out of which the income issues must be situated within the state so that the income may be said to have a situs therein. Personal property may be separated from its owner and he may be taxed on its account at the place where the property is although it is not a citizen or resident of the state which imposes the tax. But debts owing by corporations are obligations of the debtors, and only possess value in the hands of the creditors.”

Situs in a destination based consumption tax

In a consumption based tax, the tax goes to the place where the goods or services are consumed. In a chain where multiple persons are involved, the consumption could be intermediate or final. The ‘tax set off’ continues in the chain till the goods or services are either kept as such or converted into some other goods or services. The tax set off chain stops when the goods or services are finally extinguished in absolute. Where-ever the chain stops, the tax also stops, and it becomes a cost. Accordingly, it is commonly understood;

- the situs of an intermediate supply (B2B) is the location recipient of business

- the situs of a final supply (B2C) is the location where such supply is extinguished

2. Interplay between Situs of supply and Place of supply

In the dual-GST model, SGs get their share of tax on supply through two streams.

- SGs are themselves empowered to collect State GST component of the supply which is ‘Intra-state’ within their respective state.

- SGs also gets a share of Integrated GST component of the supply which is ‘Inter-State’ within their respective state.

To emphasise here that, States get the tax owing to “supply being within in their respective state” regardless of the fact that supply is Intra-state or Inter-state. Unlike the Central Sales Tax Act, 1956 (‘CST Act’), there are no provisions under GST Law, which confers the principles of supply to be within the state or outside the state, instead, the tax is disbursed on the basis of Place of supply (POS)[2]. The POS as proxies of situs is though could appear sufficiently competent but suffers from the practical and factual bias, hence can be labelled as good code with fine margins of errors.

Locus standi of POS for determining situs

On a fair look at the GST Law and the Integrated Goods and Services Tax Act, 2017 (‘IGST Law’), it appears that GST Model requires identification of (1) Location of Supplier (‘LOS’) (2) POS (3) Type of Supply (4) Application Law out of CGST/ SGST and IGST laws.

And the disbursement of tax goes to the Centre and to the State where there is POS. On a whole, it appears that situs of tax is made dependent upon the place of supply (with exceptions). The disguise is apparent that POS would ignore everything including situs doctrine, the pre-amble of the law and the territorial jurisdiction, and ploy a jurisdiction of their own, when in fact, POS has no locus standi in determining situs of supply.[3] The very law proceeds on an incorrect premise, that judicial interference is imminent.

Impact of Location of supplier (LOS) – Shortcomings of POS

The GST is levied under GST Law or IGST Law. The supply of whose LOS and POS are in the same state are exigible to Intra-state taxes, while if LOS and POS are in different states, supply is exigible to Inter-state tax. Regardless of the supply being intra-state or inter-state, the tax on supply in effect goes the state which encompasses the POS.

To illustrative, the supplier A is located in Maharashtra, has a branch in A1 Haryana. The services are supplied to B of Haryana. An agreement is entered between A and B to provide interior services, A could ask A1 to provide such service or it can itself provide services to B. Regardless of who happens to be the actual supplier, POS is Haryana, therefore Haryana would get the tax on the supply. It might appear that, once POS is correctly determined, the location of supplier wouldn’t make any financial loss to any of the state involved, however adding a factor into the situation could prompt a situation otherwise.

Suppose the interior services in the above example are exempt. The natural consequence of exemption is reversal of ITC. For ITC reversal, it is important to identify the person who would be required to do so, A of Maharashtra or A1 of Haryana. If LOS is identified as A, Haryana government would be at disadvantage in as much as, Maharashtra government would be getting the tax arbitrage of reduction in ITC owing to a supply which is consumed in Haryana.

The natural conclusion is that POS though can determine the type of supply, the export status, the import status etc., but they cannot surpass the very test of jurisdiction, inevitably therefore recourse has to be made towards situs.

3. The situs test under CST Act

The case of 20th Century Finance Corpn. Ltd. and another vs State of Maharashtra[4] is landmark ruling delivered in the context of erstwhile Sales Tax Regime and acts as a formulation when the legislature fails to define the situs of a taxable event. The facts involved – Equipment leasing company who had executed “transfer of right to use” agreements of equipment[5] with buyers in one state while the equipment was situated in another state and was to be used therein.

The controversy arose that either of the states incorporated deeming fictions in the respective sales tax statute to provide that situs of the sale of “transfer of right to use” would accrue in the state

- if either the agreement is executed in the state or if the goods under question is in the state when the agreement is executed or

- the said equipment is to be used in the state.

The wicked effect of such deeming fiction was that more than one state depending upon different criterions tried to tax the single leasing transaction.

Ratio Decidendi

While enunciating the principles of situs of sale, the Hon’ble Supreme Court considered the limitations of a state legislature under Article 286 of the Constitution, under Section 4 of CST Act, and held as under;

- An inter-state sale shall not be within the jurisdiction of either of the state, irrespective of the fact that sale concluded in either of the states as per general law or by the fiction of the sales tax law. Parliament exercise jurisdiction over inter-state sales (supply) by virtue of Entry 92-A of the List I of Seventh Schedule to the Constitution.

- States are precluded from levying sales tax on a transaction which is outside the state by virtue of Article 286 (1) (a) of the Constitution. Further, tax can also not be imposed by a State where the sales tax place in the course of import or export into or from India

- A sale whose situs has not been fixed by the fiction can be fixed by the judicial court. Accordingly the situs of a deemed sale, in the nature of ‘transfer of right to use’, would be in line with the subject of such tax viz. ‘right of use’. The situs of such sale would be the place such ‘right to use’ is transferred. Given that the locus of such deemed sale is the place where the right to use the goods is transferred, the location of goods when the right to use them is transferred is of no relevance.

- However, in case of oral or implied transfer of right to use (where the goods are not ascertained goods), the situs would be where location where the property in goods is transferred.

The judgment in this case was rendered otiose, after the amendment in the definition of sales in the CST Act, by Finance Act, 2002. However, the principles of the judgment still hold goods where there is no situs defined by the legislature, that situs of a tax event depends upon the characteristics of the event.

4. Extra-territorial Jurisdictional Limitation

While the SGs have the limitation of their respective physical boundaries, the CG’s unfettered power to tax is circumcised by the territorial boundaries of India. The burning question being, how much competent CG is to levy a Value Added Tax over the supplies whose situs falls outside India but they are not export owing to non-fulfilment of one or more conditions?

This question shouldn’t have been there had CG had the mettle to accept the status quo. Post their own admission vide Circular No. 56/5/2003-ST dated 25 April 2003, and the judgment in case of CST vs SGS India Pvt. Ltd.[6], it was unimaginable that services provided outside would ever face the wrath of taxability[7], the CG has by means of some exemptions[8] and unflattering silence however has precluded the exemption to services provided outside India when they don’t fit into the export criterion (except exempted otherwise). The pertinent questions;

- Can they tax a service when its situs falls outside India?

- Why distinguish between services and goods vis-à-vis tendered outside India?

Post the adoption of the Constitution, the Hon’ble Supreme Court had the first occasion to examine the territorial power of a State to exercise jurisdiction over a taxable event originating in the State and concluding in another State in the case Poppatlal Shah vs State of Madras[9]. When the erstwhile tax entry, Entry 48 spoke of “taxes on the sale of goods and on advertisements”, the Court observed that there is no suggestion that it channels Province’s power to tax sales only concluding within the boundaries Province, the Province is also competent to tax sales which conclude outside the Province provided that there was real and sufficient territorial nexus between such sales and the Province.

The Court held that an event sales has multiple ingredients[10], tax on sales can be levied by a Province on any ingredient of sale being happening within the Province provided the Province incorporates any such ingredient within the levy of the sales tax statute. The state of Madrad has the jurisdiction to tax sales concluding outside the Province when the state of Madras by fiction has included such sale to have occurred within Madras, post insertion of explanation in Section 2 (h) of erstwhile Madras Sales Tax Act[11].

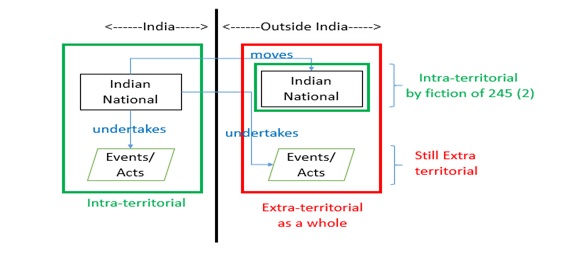

Article 245 (2) – Extra Territorial Operation

Article 245 (2) of the Constitution[12] is an extension of Article 245 (1) ibid, in as much as it saves the legislation from being invalid on grounds of extra-territorial operation. The case of ‘Bengal Immunity Company Limited vs The state of Bihar and others’[13] (‘Bengal case’), proved to be a landmark judgment in the context of Article 245 (2) wherein the Supreme Court rule upon its expression in the scheme of things. While in GVK Industries vs UOI[14] (‘GVK case’), Supreme Court went to moralize the connotations of Parliament’s power to make extra-territorial laws. The following graphic could depict the ratio of Bengal Immunity case and the objective behind Article 245 (2) ibid.

In Bengal case supra, the Supreme Court traced the legislative history of Article 245 from several colonial rule enactments and observed that Parliament has the jurisdiction to make laws with respect to (1) Nationals acceding to India and (2) Events/ Acts occurring in India. The Parliament also has jurisdiction to make laws with respect to the nationals’ events/ acts outside India, which may sound ‘extra-territorial’ but is nothing but ‘intra-territorial’, and what Article 245 (2) ibid make sure that there be no challenge as to constitutionality of this subject on the ground of extra-territorial operation. Article 245 (2) ibid doesn’t save events/ acts that do not occur in India, and any exercise of law over the said would be extra-territorial not save by it.

The GVK case was in context of the Income Tax Act, the Court held that it is constitutionally restricted from enacting legislation with extra-territorial aspects or causes that do not have, nor expected to have any, direct or indirect, tangible or intangible impact/ effect/ consequences for (a) territory of India, or any part of India; or (b) interests of, welfare of, wellbeing of, or security of inhabitants of India, and Indians – Where such impact/effect/consequences exist, Parliament can exercise its extra-territorial legislative powers under Article 245 (1) ibid with a saving Article 245 (2) ibid. The verdict in GVK very diplomatic in as much as it doesn’t lay down a clear ratio as to the power of Parliament when it comes to making laws having extra-territorial excursions, instead ruled out the negatives which were never even doubtful. The case could be said to be candid tool of the sudden change in status quo from service tax to GST.

Can they tax a services when its situs falls outside India under GST?

Applying the ratio of Poppatlal and Bengal Immunity case supra in the present case, the straight forward answer is no, they cannot. CG can only tax an event which occurs and conclude in India. On that premise, a supply of service which originate in India and conclude outside India (situs/ POS outside India) can be said to be an event not within the CG’s power. To reiterate, in Poppatlal case, the Court had held that a Province can tax a sale not concluding in other Province provided the province by fiction provides sale to include “sales originating in the Province” for the purpose of sales tax legislation, in the absence of which, the Province cannot tax sale concluded outside that Province.

Juxtaposing, there is no apparent fiction in the CGST Law or IGST Law which could even remotely insist on that mere supply originating in India is also taxable supply, instead there are ample inverse illustrations that enshrines that only supply concluding in India are taxable. Therefore, there is sound argument in saying that levy of GST suffers from the vice of extra-territorial jurisdiction, in violation of Section 1 (2) ibid, not saved by Article 245 (2) ibid. However, in the light of verdict in GVK case, the argument might needs to be revisited by the Apex Court afresh.

Why distinguish between services and goods vis-à-vis tendered outside India?

While for export of goods, mere delivery outside India is suffice, for export of services, however not only the delivery but there are several other extraneous conditions that needs to be ticked. Why so? The only one I can think of is that services being intangibles are easy to the camouflage by the related parties. Further the increasing international cliché of BEPS must have forced the government to change its status quo from the service tax regime.

5. Illustrative cases with potential disharmony

5.1 Situs of supply of Duty Credit Scrips (DCS)/ Intangibles

The Foreign Trade Policy 2015-20 (‘the FTP’) employs certain fiscal schemes to boost the export sector. Amongst them are DCS namely, MEIS, SEIS, DFIA. The DCS are piece of paper which entitles the hold to save Basic Customs Duty (BCD) on the imports of goods. The DCS can either be used by the holder or it can be sold to other importers. The DCS were taxable to GST @ 12% or 5% until 14th November 2017, when the same were exempted from GST. The DFIA is still taxable @ 5% if one were to believe the Advance Ruling Authority in case of Spaceage Syntax Pvt. Ltd.[15].

The DCS falls under Customs Tariff Heading (CTH) 4907, the place of supply for goods involving movement of goods is the place where the movement is terminated for delivery to the recipient. The problem with DCS is not the POS[16], but the situs thereof.

To illustrate, a textile export company “Horrendous” has 15 branches in different states from where the goods are exported to outside India, although the brain (HO) sits at Delhi. Fortunately or unfortunately, the FTP treats all branches of a company as one with common IEC Code. The export performance of all 15 branches fetches MEIS for Horrendous, the decision to sale out MEIS is taken at Delhi, further all the administrative action for selling MEIS is also undertaken at Delhi. In as much as MEIS is exempted from GST, the natural consequence of ITC reversal has to be undertaken by Horrendous.[17] But the problem is where such ITC reversal should be undertaken? At all 15 branches or merely at Delhi? The twofold arguments for the situs of MEIS Scrip is as follows;

- MEIS Scrip belongs to HO in as much as the HO employs the administrative staff for undertaking the supply of it

- The argument that MEIS Scrip may belong to Branch is also tangible in as much as the procurement of MEIS is implicit in the exports executed by the Branch and the HO merely undertakes administration of the same as it does for other things

In a recent decision in case of Lal Products and others vs Intelligence Officer and others[18], the Hon’ble Kerala High Court had an occasion to determine the situs of sale of incorporeal goods namely, patents and trademarks when the contract of sale was executed by the Appellant in the state of Gujarat where they had one operating manufacturing plant while the HO of the Appellant was in the state of Kerala. The High Court while distinguishing the decision of Gujarat High Court in case of Ambalal Sarabhai Enterprise Ltd.[19], and relying upon the decision of Delhi High Court in case of CUB PTY Limited v. UOI and Ors.[20], held that situs of the owner of an intangible asset, would be the closest approximation of the situs of an intangible asset.

The exercise of the right to a trademark or a patent right obtained by Appellant, who had their principal places of business in the State of Kerala, is held to be exercised from the principal place of business (Sic). When transferring their rights obtained under a statute, to another entity having its place of business in another State; from where the transferee intends to exercise such rights thereafter, postulates a movement of the intangible, corporeal goods from one State to another and, hence, would be an inter-State sale assessable to tax under the CST Act. The transferor’s principal place of business being within the State of Kerala, the sale would be an inter-State sale.

Both MEIS and Patents are incorporeal goods and are in simile to the products of Chapter 4907 of the Common Tariff, therefore the judgment seems to have a persuasive effect for Horrendous also. If Horrendous were to reverse ITC, in the light of above decision, it has to be undertaken at Delhi GSTIN viz. HO. Horrendous could also manipulate the ratio by taking a vertical registration at Delhi to reverse ITC at the minimal possible. Similar ratio can also be found in Mayco Mosanto Biotech (India) Pvt. Ltd. vs UOI[21].

5.2 Consumption – where the tax chain stops

In case where the supply involves movement of goods, Section 10 (1) (a) ibid ascribes that POS is the place where the goods are at the time, when the movement of goods terminates for delivery to the recipient. It tries to identify consumption, but fails miserably in case of goods of personal effect. The provisions of Section 10 ibid are de hors the nature of supply, be it Business to Business or Business to Consumer. In Kun Motor Co Pvt. Ltd. vs Assistant STO[22], the Hon’ble Kerala High Court explored the contours of Section 10 (1) (a) ibid, which can potentially lead to multiple anomalies.

The Appellant, a dealer of Cars being operational in Puthuchery (Puducherry), had sold a car to a consumer who resided in Kerala. Since the car were not available in Kerala he had come to buy the goods from Puducherry. The Appellant sold the car to consumer ex-showroom charging IGST on the pretext that car would be taken and used in the state of Kerala. The Appellant also undertook the delivery of the car through its logistics wing. The state tax authorities of Kerala intercepted and seized the car while the goods were in movement, levying penalties on the ground that EWB was not uploaded by the Appellant. The High Court in the context of applicability of EWB, outline following observations vis-à-vis Situs of Supply;

- The nature of the transaction whether it is inter-State or intra-State supply is to be decided from the provisions in the statute and not by the intention or understanding of the parties to the transaction.

- Section 10 (1) (a) ibid applies when the movement of goods is occasioned by the transaction of supply, as evident from the words “where the supply involves movement of goods”. The transaction of supply itself, should occasion the movement of the goods.

- When a Business recipient buys goods from another state and transport them to its own state, then though the sale occurs in the outside state but the POS is in his state since the transaction of sale occasions the movement of goods from one state to another state, and supply is said to be terminated in his State, whether the movement is by the supplier or the recipient himself.

- When a Consumer recipient buys goods from another state ‘for his own us’, then the supply terminates as soon as he takes possession of the goods. The movement of goods post that, from outside the state to his own state makes no cause to the supply at all.

Applying the principles above, the Court held that the property in car occasioned on temporary registration in Puducherry and sale was completed therein. An intra-state supply got converted into inter-state supply merely on the basis of mere transportation is out of the place. The incidence of supply is on the supply and not on the nature of transport. The supply of car was held to be completed in Puducherry and subsequent movement from Puducherry to Kerala doesn’t require EWB. The Court however, didn’t mandated the dealer to correct the incorrect tax charged by him. The principles enumerated by the Court are Questionable on following counts;

5.2.1 Dilution of application of Section 10

The Court distinguished the application of Section 10 (1) (a) ibid, depending upon whether the recipient is a business entity or consumer. There seems to be no rationale in the peeling off the Section 10 (1) (a) ibid based on B2B and B2C, in as much as such concepts have relevance only in case of services. Goods because they are tangible themselves determine where they are consumed for the purpose of POS. Different clauses of Section 10 (1) elucidates different circumstances when POS is to be determined based on different criterions, but none on the basis of the status of recipient. The observation not only dilutes the structure of POS provisions but also complicates the strict and plain application thereof.

5.2.2 Supply includes subsequent occasioned movement

In an attempt to align the provisions of POS with EWB requirement, the court appears to have extended the contours of the term supply. A sale of goods completes when the property in goods is transferred, but supply continues until the goods are moved at the prescribed place either by supplier or recipient, only if the case is of a B2B transaction. The observation appears to have resolved the complications with Ex-works sales, however again the challenge is to why such supply extension shouldn’t be seen for B2C supplies also.[23]

The judgment give rise to inharmonious gap as to interpretation of POS vis-à-vis consumption. The POS if read literally implies no facts to facts interpretation, however reading them reasonably can create distort. Consider following situations, where POS if read literally and if read reasonably have different results;

- Ex-works Supplies: The location of goods ex-factory or location of recipient

- Auction Sales: The location of auction or location of recipient

- Services to employees: Location of performance or registered location of employer

If the ratio of judgment is accepted, then the shortfalls of the POS are explicitly clear in as much as POS fails to identify the correct place of consumption in the eyes of both the assessee and revenue. Also pertinent to mention that Europeans jurisdictions employ Asset labelling test wherein it is left upon the assessee to prove the onus of use of inward supply in its business and be entitled to ITC.[24]

5.3 An off-location supply – bypassing intermediate consumption

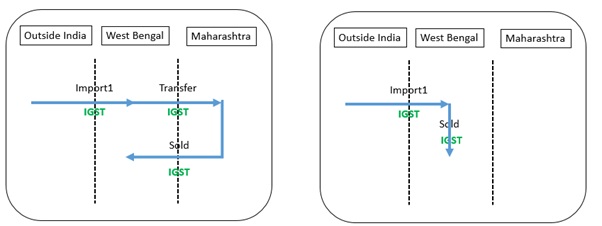

It’s just ill-fated that GST had to make way for ‘distinct-person’ concept. Section 25 of the GST Law for the sake of fair distribution amongst states, deems one single person as different person. The deeming fiction has multiple flaws, gruesomely reflected from a Maharashtra Advance Ruling in case of Sonkamal Enterprises Private Limited[25]. The applicant importer (‘Sonkamal’), based out of the state of Maharashtra (‘MH’) took GST registration therein. Section 22 of the GST Law envisage that a person requires registration in state ‘from where’ he makes taxably supplies above the given threshold. The expression ‘from where’ is prone to be decoded in numerous ways.

Sonkamal imported goods at the Haldia port (‘West Bengal’ or ‘WB’) and in-bonded the same in a rented Customs bonded warehouse. Sonkamal based on the orders executed a sales to a registered person based out of Gujarat by filing ex-bond bill of entries. The question before the Hon’ble AAR was whether Sonkamal is required to take GST registration in WB or can it execute such transaction from the GST Registration of MH. The AAR held the latter, that Sonkamal can do the transaction with the GST registration of MH.

In the graphic the left hand side depicts that the sale and purchase are executed in MH and WB and assuming Sonkamal had taken registration in both MH and WB, while the graphic on the right depicts that sales and purchase are executed from MH. Following complications exists

The AAR accords that Location of importer (and POS[26] thereof) can be MH in as much as, in WB there is no warehouse (fixed location) of the applicant. The implicit therein is that “from where” would always be one location if the taxpayer has only one “fixed establishment”, regardless of where the sales/ purchases are executed. The said articulation runs in direct contrast to the interpretation propounded by CBIC (then CBEC) Circular No. 61/35/2018-GST dated 04th September 2018 (‘the Circular’ – issued in the context of EWB), which states that registration is required for every “place of business”[27] where a taxable person stores his goods, Para 4.

Stocking-Points registration

Juxtaposing, the principle to the OEM Tier-1s, who have to supply goods in JIT Model to OEMs and maintain goods at transporter godowns/ stocking points in states outside their states, the Tier-1s can avoid taking registrations at such stocking points, if they were to rely on the AAR[28]. However, how are they supposed to comply with EWB that the CG and SGs have together colluded with and shoved down their throat? Anybody’s guess, who will be their Olga Tellis?

The inherent Jurisdictional vice

Section 97 (2) of the GST Law bounds the AAR to rule upon only on the specified matters, the matters doesn’t include ruling upon POS. Sub clause (f) of Section 97 (2) ibid prescribe that a ruling can be sought “whether” a person is required to be registered, the questions “whether” doesn’t include “where”, unfortunately. The order of the AAR suffers from the vice of jurisdictional error, Sonkamal basically bamboozled the AAR.

5.4 An off-shore employee – situs qua taxable person?

The territorial bounds of the GST Law prohibit the Parliament to extract tax over a supply not occurring in India. The company had sent his employee to outside India, the employee in order to cater to his human needs procured certain supplies viz. Food at a restaurant, renting a hotel and cab commutation services outside India. The supplies stood consumed overseas, no part of the supplies is brought to India for the consumption herein. Ideally therefore, there should be no GST on such supplies. Section 5 (3) of the IGST Law [29] read with 2nd limb of Section 2 (93) of GST Law[30], purports to treat said supplies as receipt of services by the company for tax purpose. Also here is how S. No. 1 of Notification No. 10/2017-IT (R) goes;

Any service supplied by any person who is located in a non-taxable territory to any person other than non-taxable online recipient.

A perusal of the above reveals that the company has to bear GST under RCM on supplies consumed outside India by the employee in the capacity of the company, because

- They are any service

- Are supplied by any person (located outside India)

- To any person (located in India other than NTOR)

- No. 1 ibid callously extends the jurisdiction of the Parliament without calling for the application of situs or the cliché proxy POS. Could this be an oversight or an over-exaggeration? Maybe?

5.5 Outside India but not export – Forex conundrum

What do you call a services whose POS is outside India, but does not fetches you Forex for the needy government – a camouflage. Section 9 and 5 ibid can levy tax on any supply originating from India, but the leeway has been to supplies that qualifies zero rated supplies (ZRS). When a supply doesn’t qualify as ZRS, it doesn’t enjoys the benefits associated with the ZRS (including the tax exemption). Section 16 of IGST Law is not de hors Section 5 ibid, but only an exception of it.

The conundrum lies in destination of supply (or its proxy POS). In the scheme of things, the Indian Parliament assumes jurisdiction over the supply whose destination/ POS is India vide Section 5 (3) ibid regardless of whether the Indian recipient pays out of Forex or not. On the above count, the Parliament also disguise jurisdiction over supply whose destination (POS) is outside India. Therefore, by their own the Parliament has rendered POS toothless vis-à-vis cross border supplies. The exaggerated exercise of jurisdiction is open to the challenge of extra-territorial jurisdictional vice.

5.6 Outside India but not export – Draining State – Enriching Centre

Another lacuna, with the imposing a tax a supply of services whose POS is outside India but they are not export owing to non-receipt of Forex is that such tax remains unfungible i.e. the GST on such supply is the last point of tax in India (‘bottled IGST’). The distribution of such collected tax is to be undertaken as per Article 269A of the Constitution in proportions to the Centre and the State(s). Such mapping of such distribution is undertaken under Section 17 of the IGST Law.

- Section 17 (1) ibid enshrines various other unfungible IGST collections by Centre and stipulates that “central tax” element of such IGST shall be apportioned to the Centre.

- Section 17 (2) ibid states that such “balance after apportioning central tax element”, IGST shall be apportioned to the states as per;

- At Invoice level on the basis of Place of Supply of respective States

- Total supplies ratio on the basis of Place of Supply of respective States

- Section 17 ibid doesn’t provide for distribution of bottled IGST

- Coming now to Section 53 of State GST Law stipulates that on utilization of ITC of SGST for payment of IGST, then State Government shall transfer equivalent amount to the Centre.

Illustration: “A-ten” is a registrant of Haryana and has availed ITC of local procurements to the tune of CGST – INR 100 and HR-GST – INR 100. A-ten provides services to a business house sitting in Kuwait, the POS being Kuwait, but the consideration is received in INR.

In scenario 1, In line with the trauma under 4.5 above, A-ten decides to pay IGST on output supplies, declaring the same at INR 240. He pays IGST – by utilizing CGST 100 and HR-GST – 100, and the rest by bank payments.

In scenario 2, A-ten avoids paying IGST and reverse ITC as availed by him.

| Scenario 1 | Scenario 2 | ||||

| Centre | State | Centre | State | ||

| Procures tax paid input/ input service | +100 | +100 | Procures tax paid input/ input service | +100 | +100 |

| Avails ITC of input/ input service | -100 | -100 | Avails ITC of input/ input service | -100 | -100 |

| Pays tax on output services | +240 | – | Does not pay tax on output services | – | – |

| Utilize ITC | – | – | Reverse ITC | +100 | +100 |

| Net Funds to the Treasury | +240 | – | Net Funds to the Treasury | +100 | +100 |

By levying tax on the states with intermediate inward supply gets to loose INR 100 out of its pocket, while on non-taxability, the state gets to retain such tax in the form of ITC reversal. There I give you something States, 1.2.3 Fight!

5.7 Drop Shipments

There are numerous examples in the GST Law and IGST Law indicative of the fact that POS is nothing more than just the nature determination tools of a supply. The CGST Amendment Act, 2018 adds following to the Schedule III;

- Supply of goods from a place in the non-taxable territory to another place in the non-taxable territory without such goods entering into India.

Evidently, what S. No. 7 excludes a supply as supply if it is “to a place in the non-taxable territory”, wait? Isn’t GST Law per se applicable to supplies made in the taxable territory? Even if S. No. 7 might get away with the constitutional challenge of Article 245 ibid, but it certainly cannot get away with the jurisdictional challenge of Section 1(2) ibid.

The situs of a supply in the non-taxable territory is non-taxable territory, Indian Parliament has no jurisdiction to tax or no tax (exempt/ otherwise) the same.

5.8 Mediocrity at the Airports

Before the GST was implemented in India, foreign tourists had something to cheer while buying merchandise from India. Procurements from Duty Free Shops (DFS), a sophisticated label for a bonded warehouse, had no component of Excise Duty/ Sales Tax (Eh?). The intention behind the concept of DFS was plain and simple, the goods the foreign customers bought was more of penultimate sale in the nature of export, and to avoid the hassles of refund of duties, the duties and taxes made per se exempted. In the heart of hearts, the Parliament knew that goods bought by foreign customers would somehow get exported out of India, the situs of the sales by DFS is outside India in as much as such goods are before the custom frontiers of India.

Ever since that eventful day, DFS scheme has been scrapped[31], and the Parliament has lulled the tourists into another similar scheme alike[32], namely refund to international tourist. Section 15 of IGST Law inherently acknowledges that situs of the supplies (at Airport or otherwise) to international tourists is outside India, but owing to lag of technology, the alternative refund scheme has yet to see the light of day. Unless Section 15 ibid is implemented, taxes are getting exported. In your face Parliament!

5.9 Situs of services

In 20th Century case supra, the principles for situs of sale of goods were formulated, however, as of date services has nothing cogent to call for their situs. Though the Courts in multiple decisions have given a hint about the situs which could be used for determining as to when a situs falls outside India;

5.9.1 Activities vis-à-vis Events Outside India

In Indian Association of Tour Operators vs UOI case supra, the Hon’ble Delhi High Court held that Indian Tour operators while arranging tours for outside India undertakes several tasks, including planning, scheduling and organising the tour, fixing the probable dates and venues, finalising the itinerary, booking of accommodation in hotels in India and foreign countries, making travel and transport arrangements,……….. etc. In the fantasy of the Court, some of these services can be said to be provided in the territory outside India, while some possibly within India. In the eyes of Court, the conduct of these events has situs of bouquet of these services is outside India. Similarly in in ETC Networks Ltd vs Comm. of Customs, C. Excise and Service Tax[33], the Mumbai CESTAT held that when an event is performed outside India, it is not amenable to service tax. The matter as to situs of services in case of tour operators is pending transfer to the Larger Bench of CESTAT in case of Cox & Kings Ltd[34].

5.9.2 Activities vis-à-vis subjects outside India

In Bnazrum Agro Exports Pvt Ltd vs Comm. of Ex. and ST.[35], and Sundaram Industries Ltd vs Comm. of GST and C. Ex.[36], it was held that clearing and forwarding agent services over the goods situated outside India is performed outside India and not taxable to service tax.

5.9.3 Activities vis-à-vis situs of the recipient, not beneficiary

In Paul Merchants Ltd. vs CCEx.[37], the majority of the Hon’ble CESTAT held that, the situs of services belongs to place of consumption and not place of performance, for the services alike Business Auxiliary. When services are of such nature that “their ultimate consumption” in not “performance”, but “the deliverables out the performance”, in that case situs of the recipient mirrors the situs of services, and not the beneficiary of services.

As it stands, the situs of services is more tilted towards its consumption. The consumption being intangible are prune to misuse, therefore in all fairness to the government, the exact rules for situs remains unexplored. OECD have tried to set out guidelines for the situs of services, but we’ve seen them fail miserably. There is still hope, one day!

5.10 Situs of services relating to Immovable Property

Transfer of property in immovable property (‘IM’) is not taxable under the GST Law, it just out, by the fiction of Schedule III, the land and buildings are out. However, any services in relation to IM are not out. Services vis-à-vis IM could be of two specie;

- Services via IM:

Services via IM implies, letting the enjoyment of the IM e.g. renting, leasing, etc. These very provision of these services is by way of existence of IM. It would be unthinkable to say that the consumption of services via IM could take place at a place other than the very place of IM. If a consumer rent in IM for staying, no doubt he is enjoying his stay (consuming) at the very place of IM.

In fact in case where a company based out of MH rent in IM in the state of WB for his stay, it cannot present its case that company is consuming services in MH. In other words, the deliverables of rent is the very stay, not that the tenant would submit a report to the company about his leisure. The services basically ends at WB, period. The situs of services via IM could therefore be said that the very place where IM is located.

- Other services over IM

Things get messy here, if one were to bemoan. A company based out of MH hired a surveyor to survey the IM located at WB. The surveyor surveyed the same and delivered his report to the company in the form of a report in MH. So, where does the services could be said consumed? The consumption is probably the thin line between the services via IM and other services over IM. In the pertinent case, the consumption situs to an extent mirror the case of Paul Merchants supra. Unlike services via IM, the situs of the consumption is not enjoyment of IM in the case, but the enjoyment of some other service that just happens to be over the IM. Accordingly, the situs should again be the place where the deliverable is consumed viz. MH.

The POS proxies however cans the said analogy and binds the consumption of services over IM services to the place of where the IM is located. The expression “included services provided by architects, interior decorators, surveyors, engineers and other related experts or estate agents…..” in Section 12 (3) of IGST Law literally demolish the principles of VAT.

Services over/ via IM located outside India

Another provision which accepts the above analogy and literally highlights the hypocrisy of the framer is found in proviso to Section 12 (3) ibid, produced below;

Provided that if the location of the immovable property or boat or vessel is located or intended to be located outside India, the place of supply shall be the location of the recipient.

Section 12 of IGST applies where the service provider and service recipient are located in India. Section 12 (3) ibid deems the consumption (POS) of services in relation to IM to be the place where IM is, the proviso ibid however diverges from the said principle and shifts the consumption to location of recipient in case the service is between Indian counterparts. There is no explanation for this sub-standard approach of identifying consumption, the POS principles are motivated by the revenue.

5.11 Situs of origination – Horizontal Split of IT Enabled Services (‘ITES’)

When IT companies procures project from overseas, their execution involves split of work. A company ‘Knob-India’ based out of Delhi procured contract for supplying ITES to ‘Dumb’, a customer based out of USA for $50 Mn. In as much as the project involves both off-shore and on-shore execution, Knob-India has contract shifted the on-shore execution part to its USA based subsidiary Knob-USA for $10 Mn. While Knob-India would invoice Dumb for the entire gamut of services including (off-shore and onshore work), Knob-USA would invoice Knob-India for onshore work, even though the beneficiary of onshore work rendered by Knob-USA is Dumb.

In terms of the celebrated judgment of Vodafone Essar Cellular Ltd vs CCEx.[38], OECD International VAT/ GST guidelines, and CBIC’s own admission in recent Circular No. 78/52/2018-GST dated 31st December 2018, the situs of Knob-India’s services to Dumb should be outside India, while that of Knob-USA to Knob-India should be India. All things appears straight forward, however something must have gone drastically wrong in the appreciation of facts by the Hon’ble Bombay High Court before delivering judgment in case of Tech Mahindra Limited vs CCEx.[39]. The High Court somehow deduced that Knob-India is not entitled to accord onshore services its own in as much as these are not originated from India despite the fact the situs of services (admittedly) outside India. Wait, What?

The main source of unorthodoxy in the High Court’s ruling is the expression “provided from India” in Rule 3 (2) (a) of the erstwhile Export of Service Rules, 2005. The expressions got omitted with effect from 27th February 2010, but the questions still looms as to what is the origination point of services.

5.12 Situs of origination – Project Site of contractor

When something is absolutely exempt, the horrors shifts from the recipient to the supplier. As is the case with Duty Credit Scrip, pure labour construction services provided under Housing for All (Urban) Mission (‘HUM’) is exempt from GST. A company ‘Hately’ registered in Delhi procures a construction contract under HUM to be executed in Rajasthan (RAJ). Two questions;

- Does Hately requires registration in RAJ?

The Rajasthan AAR in re, Jaimin Engineering Private Limited[40], has given a ludicrous answer to the first question that Hately doesn’t require registration in RAJ in as much as Hately doesn’t have a place of business/ office in the state of RAJ. Owing to ruling being non-speaking, there is no true answer as to situs of origination of supplies.

- The onus on suppliers to Hately identify the true location of the recipient?

Every inward supply Hately would procure would be an end of the tax chain in as much his services are exempt. The suppliers therefore have the onus to determine the correct situs (POS) of their supplies. The suppliers who provide services directly in relation to IM (architects, planners) might have a good case to declare the POS of supplies as RAJ. The hammer would fall on the auditors, who might just use Delhi registration of Hately as determinant for POS. The input taxes owing to architects, planners would go to Rajasthan government while that of auditors would go to Delhi. It’s a swamp, the more you try to get out the more you get in.

5.13 Situs of ‘Supply’ or ‘Element of Supply’

An apparently easy question with no answers. When it’s about supply, is it about supply per se or is it about element of supply. Section 7 (1) (a) of GST Law articulates supply includes all forms of supply such as sale, etc. Sale is a form of supply, but the levy is no supply not sale. The situs of sale could be different from situs of sale, as Kerala High Court ornamented in Kun Motors case supra. Might not have someone thought about it, such that there is lack (or absence) of jurisprudence. Avengers 3 left us hanging, but this is probably the biggest cliff-hanger ever.

5.14 An illusory situs

The consumption vs performance conflict qua services has now have fair share of debacle over the years now, but the controversy is still in nuisance stage when it comes to goods. Following two scenarios can be perused;

- An overseas OEM asks Tier-1 based out of India to manufacture and retain Tools for him, and subsequently export components made out of such Tools overseas. The costs of the Tools may or may not get embedded in the value of components. Should GST be leviable on the Tools in as much as such goods are not exported out of India? – Yes, if one were to believe Hon’ble Karnataka High Court cue IBEX Engineering vs State of Kerala[41].

- Goods invoiced to overseas buyer, but delivered to his sister unit in India for the latter’s consumption. Should such goods be leviable to GST in as much as goods never gets exported out of India? – Yes, in terms of Bombay High Court judgment in case of Glaxosmithkline Asia Pvt. Ltd. vs Deputy Commissioner of Sales Tax[42].

Depending upon where the goods are moved or moved or not, Section 10 (1) (a) or 10 (1) (c) of IGST may apply for determining the POS of the goods. In any case, the POS would be some place in India and therefore be amenable to GST. For a minute, if the difference between goods and services is forgotten, then it might seem square that these transactions should not be taxable in India in as much as the consumption occurs outside India regardless of the physical situs. The illusory situs of the goods might appear to be within India, but the actual situs is not. Foreign Jurisdictions have come very far when it comes to adjudge the realities and practicalities of the VAT[43], but POS in IGST Law would always continue to be obsessed by revenue.

5.15 The tussle between States

For an assessee supplying goods or services, POS is just not the end of it, correct POS is. The states have and will continue to fight over the jurisdiction to extract tax from the assessee on a single transaction. The tussle between states have taken gruesome shape many a times over the course of sales tax regime[44], of which Supreme Court has tried to resolve the jurisdiction on the footprints of Article 286 ibid, CST Act, respective sales tax entries in List I and List II ibid. In multiple cases, the trodden assessee were forced to approach the highest of the courts to resolve the double taxation vows. When the assessee had paid tax treating a sale as concluding in one state but was in fact a sale concluding in other state, the Supreme Court in B.H.E.L. supra, and KG Khosla supra passed direction under its special jurisdiction under Article 136 and on reference from the High Court, to the tax authority where tax was wrongly deposit to transfer the tax to the tax authority which in fact had the authority to collect it.

Section 77 of GST Law and Section 19 of IGST Law embarks upon an assessee to rectify their mistake, however the assessee have and would always have the mantle to ride over such procedural block shoved down by the government by approaching the superior courts. In fact, in a sort of resembling case, the Hon’ble Kerala High Court in the case of Saji S. vs Comm. of SGST[45] has already passed one such direction wherein the assessee had sought release of goods but the tax was incorrectly deposited under SGST Tax Ledger instead of IGST Tax Ledger, the High Court directed the tax authorities to transfer tax within the ledgers.

Chronology of Taxability, Situs, and POS

Having gone through multiple illustrations and advantages and limitations of situs and POS, it can be safely concluded that the chronology of the levy and administration should move in the chronological order of;

Situs >>>>> Taxability >>>>> POS (if in sync with situs)

India has such rich jurisprudence when it comes to implementing the realities of the VAT law and deducing where the VAT law could be cruel. The principles promulgated by the jurisprudence should have been the heart and soul of POS principles, instead the principles have been made a source of revenue. Disputes are inevitable.

Apologies for the Grammar.

Manish Sachdeva

manish619sachdeva@yahoo.in

[1] G.R. No. 42780. January 17, 1936

[2] In fact POS are the only proxy that enables CG disburses the tax on account of Inter State supplies.

[3] There is in fact a situation of Catch-22 when it comes to locus standi of POS, observed in the decisions of Kun Motors Co Pvt Ltd vs Asstt State Tax Officer (Ker HC WA No. 1803 of 2018, and Indian Association of Tour Operators vs UOI (Delhi HC – WP 5267 of 2013).

[4] 2000 AIR 2436

[5] Deemed sales under Article 366 (29A) (d) of the Constitution

[6] 2014 (34) S.T.R. 554 (Bom.)

[7] Accepted that exports benefits may not be provided

[8] S. No. 10D and 10F of Notification No. 09/2017-IT (Rate) as amended

[9] 1953 4 STC 188 (SC), 1953 AIR 274, rendered in the context of para materia provisions in Government of India Act, 1935

[10] The expression “sale of goods” is a composite expression consisting of various ingredients or elements. Thus, there are the elements of a bargain or contract of sale, the payment or promise of payment of price, the delivery of goods and the actual passing of title, and each one of them is essential to a transaction of sale though the sale is not completed or concluded unless the purchaser becomes the owner of the property.

[11] This position was altered by Article 286 which barred the jurisdiction of state to fix situs of sales occurring in the course of inter-state trade

[12] (2) No law made by Parliament shall be deemed to be invalid on the ground that it would have extra territorial operation

[13] 1955 6 STC 446 (SC), 1955 AIR 661

[14] 2017 (48) S.T.R. 177 (S.C.)

[15] AAR Maharashtra in GST-ARA-13/2018-19/B-86

[16] in as much as the DCS are goods and Section 10 (1) (a) of IGST Act unequivocally spelt out that POS is where the delivery is terminated viz. the location at which the DCS are delivered to the recipient.

[17] MEIS/ SEIS supplies might not require reversal of ITC depending upon Section 17 of GST Law is jolted

[18] 2018-TIOL-2639-HC-KERALA-VAT

[19] [2006] 145 STC 523 (Guj)

[20] [2016) 388 ITR 617 (Delhi)

[21] 2016 (44) S.T.R. 161 (Bom.)

[22] 2018-TIOL-185-HC-KERALA-GST

[23] The inconsistent situs for B2B and B2C can garner huge loss for SGs, in as much as the supplier would assume all B2C supplies as intra-state and declare “Zero” in Table 3.2 in Form GSTR 3B, and no disbursal would ever be made to a SG despite the fact that consumption happens in that SG. An apparel retail outlet in Delhi can raise its invoices as B2CS for all the buyers coming from Haryana and Utter Pradesh. The apparels goes with buyers in Haryana and Utter Pradesh, but the tax remains with Delhi. Ruck Fools Delhi!

[24] For more reading, refer Wolfgang Seeling vs Finanzamt Starnberg, CJEU in Case C-269/00

[25] Maharashtra AAR in GST-ARA-48/2018-19/B-123

[26] Section 11(a) of IGST Law – The place of supply of goods,–– (a) imported into India shall be the location of the importer;

[27] Section 2 (85) “place of business” includes––

(a) a place from where the business is ordinarily carried on, and includes a warehouse, a godown or any other place where a taxable person stores his goods, supplies or receives goods or services or both; or……

[28] In WS Retail Services (P) Ltd vs UOI [CWP No. 18339 of 2015 (O&M)], the P&H High Court held that the registration is not required for stocking points, provided the supplier of the goods proves that goods stored at stocking points are inconsequence of the purchase orders.

[29] (3) The Government may, on the recommendations of the Council, by notification, specify categories of supply of goods or services or both, the tax on which shall be paid on reverse charge basis by the recipient of such goods or services or both and all the provisions of this Act shall apply to such recipient as if he is the person liable for paying the tax in relation to the supply of such goods or services or both.

[30] and any reference to a person to whom a supply is made shall be construed as a reference to the recipient of the supply and shall include an agent acting as such on behalf of the recipient in relation to the goods or services or both supplied

[31] Although they do enjoy BCD exemptions on their imports

[32] Also being operated more successfully overseas

[33] Appeal No. ST/90072/2014 dated 29.11.2018

[34] 2018-TIOL-2536-CESTAT-MUM-LB

[35] 2018-TIOL-1532-CESTAT-MAD

[36] 2018-TIOL-3875-CESTAT-MAD

[37] 2013 (29) S.T.R. 257 (Tri. – Del.)

[38] 2013 (31) S.T.R. 738 (Tri. – Mumbai)

[39] 2014 (36) S.T.R. 241 (Bom.)

[40] Advance Ruling No. RAJ/AAR/2018-19/07

[41] [2012] 49 VST 302 (Kar)

[42] 2018-TIOL-2560-HC-MUM-VAT

[43] Tool Development Charges – Export or not under GST – an article elaborating the context

[44] B.H.E.L vs UOI 1996 AIR 1854, 1996 SCC (4) 230, Ashok Leyland vs UOI 1997 105 STC 152 (SC), 20th Century Finance Corpn. Ltd. supra, UOI vs KG Khosla 1979 AIR 1160, TISCO vs S R Sarkar 1960 11 STC 655, Maganese Ore (India) Ltd vs Regional Assistant Commissioner of Sales Tax [1976] 37 STC 489

[45] WP (C) No. 35868 of 2018