GST on Real Estate Transactions, Transfer of Developments Rights and Joint Development Agreements (JDAs)

Construction and Real Estate is a complex business with multiple stakeholders involved in it. It has been a growing sector in India, but ironically has been riddled with litigation owing to multiplicity of taxes and dual administration mechanism; thereby exposing it to the conundrums of both Central and State level complex indirect taxation levy prior to GST regime.

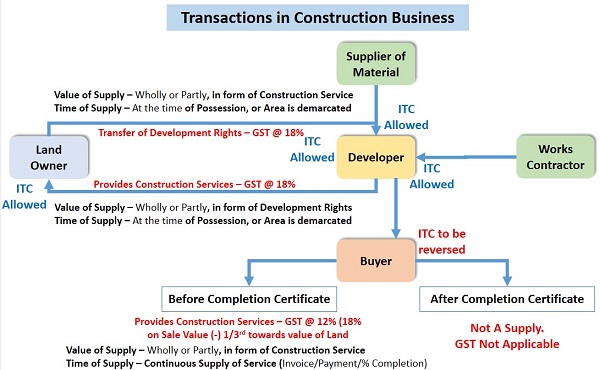

Lets now understand the various parties that could possibly be involved in a typical real estate transaction end-to-end and the implications of GST on each of these transactions.

Typically, any real estate transaction starts with Developer acquiring land for constructing a building (Residential/Commercial) upon it. Land is either purchased outright from the Landowner, or the Developer enters in to “Joint Development Agreement” (JDA) with the Landowner, whereby

- The Developer Acquires the Development Rights from Landowner with respect to the Land

- The Development rights entitles the Developer to obtain various types of licenses and approvals from the Government authorities and construct a complex, building, civil structure on the land, either by himself, by acqiring material and labour from Suppliers or getting work done through Works Contractors

- In return for the transfer of development rights by landowner, the Developer gives the Landowner consideration in the form of Cash (Revenue Sharing) or certain number of flats/offices/shops (Area Sharing) or both

- The remaining Flats/Offices/Shops are retained by Developer and sold to other Buyers

So in a nutshell, there are 5 parties typically involved in a Real Estate transaction, which has an impact of GST – Landowner, Developer, Supplier, Works Contractor and Buyer.

Various Transactions in a JDA type of agreement and its GST Impact:

We will consider the below 4 points with respect to each of the transactions:

1. Supply definition,

2. Type of transactions and its taxability,

3. Allowability of Input Tax Credit (ITC),

4. Valuation of Supply

1. Supply Definition:

As per para 5(b) of Schedule II of CGST Act, the following is ‘supply of service“:

- ..(b) Construction of a complex, building, civil structure or a part thereof, including a complex or building intended for sale to a buyer, wholly or partly, except where the entire consideration has been received after issuance of completion certificate, where required, by the competent authority or after its first occupation, whichever is earlier

As per para 6(a) of Schedule II of CGST Act, the following composite supplies shall be treated as a supply of services, namely:

- ..(a) works contract as defined in clause (119) of section 2

2. Type of transactions and its taxability

Transaction 1: Landowner – Developer: Transfer of development rights by Landowner to Developer is treated as Supply** in which Development Rights are transferred in return for consideration that involves in kind by way of wholly or partly, in the form of Construction Service of Complex, Building or Civil Structure.

Notification No. 4/2018-Central Tax (Rate), dated 25th January, 2018 which reads as follows, establishes liability of payment of GST by the Landowner for Transfer of Development Rights in consideration of receiving Construction Services from the Developer:

..(a) registered persons who supply development rights to a developer, builder, construction company or any other registered person against consideration, wholly or partly, in the form of construction service of complex, building or civil structure;

as the registered persons in whose case the liability to pay central tax on supply of the said services, on the consideration received in the form of construction service referred to in clause (a) above………. …… ……shall arise at the time when the said developer, builder, construction company or any other registered person, as the case may be, transfers possession or the right in the constructed complex, building or civil structure, to the person supplying the development rights by entering into a conveyance deed or similar instrument (for example allotment letter)

From the above Notification, it can be deduced that:

- The Landowner must be Registered Person to attract GST liability

- Supply in the Transaction: Development Rights

- Value of Supply (Consideration): wholly or partly, in the form of Construction service of complex, building or civil structure

- Time of Supply: when the Developer transfers possession or the right – example Allotment letter.

Bigger question which arises here is – How do you arrive at the value of supply of Construction Services in this case? This is answered in the section 4 below.

Since there is Supply with Consideration being Construction Service, the transaction of Transfer of Development Rights is treated as Supply as per Sec 7 (1)(a) of CGST Act and therefore GST is payable by the Landowner @ 18% (SAC Code: 999799) at the time when the Developer transfers possession or the right through a conveyance deed or similar instrument like allotment letter.

Transaction 2: Developer – Landowner: Developer provides Construction service to Landowner over a period. The Developer hands over the Qwnership Rights of certain percentage of the developed area ie. Super Structures like complex, building or civil structure or flats to the landowner (in Area Sharing JDA).

Again referring to the Notification No. 4/2018-Central Tax (Rate), dated 25th January, 2018, establishes liability of payment of GST by the Developer for receiving Consideration in the form of Development rights from the Landowner for providing Construction Services to the Landowner.

..(b) registered persons who supply construction service of complex, building or civil structure to supplier of development rights against consideration, wholly or partly, in the form of transfer of development rights, as the registered persons in whose case the liability to pay central tax on supply of the said services ….. ….. in the form of development rights ….. …..shall arise at the time when the said developer, builder, construction company or any other registered person, as the case may be, transfers possession or the right in the constructed complex, building or civil structure, to the person supplying the development rights by entering into a conveyance deed or similar instrument (for example allotment letter).

From the above Notification it can be deduced that:

- The Developer must be Registered Person to attract GST liability

- Supply in the Transaction: Supply of Construction Service of complex, building or civil structure, etc.

- Value of Supply (Consideration): wholly or partly, wholly or partly, in the form of transfer of development rights

- Time of Supply: when the developer transfers possession or the right

To conclude from the above, it is clear that Supply of Construction Services by the Developer to Landowner (supplier of Development Rights) is a Supply for a consideration in the form of Transfer of Development Rights and therefore GST is payable by the Developer when he transfers possession of flats to the Landowner.

Again, bigger question which arises here and in previous case – How do you arrive at the value of supply of Construction Services and Development Rights in this case? Refer section 4 below.

Transaction 3: Supplier – Developer: Supplier provides various material and labour services to Developer where Developer on his provides Construction service. Supplies attract GST and Developer gets Input Tax Credit (ITC) for the same (refer next section for details). This is a simple GST transaction and hence not covered in details hereunder.

Transaction 4: Works Contractor – Developer: Works contract is treated as supply of service and GST would be charged accordingly (not as goods or part goods/part services). Developer gets Input Tax Credit (ITC) for the same (refer next section for details). This is a simple GST transaction and hence not covered in details hereunder.

Transaction 5: Developer/Landowner – Buyer: Sells Flats to Buyers. In this transaction, either the Developer and/or Landowner sells flats/shops/offices to the Buyer. This is a simple transaction with the Buyer and GST would be leviable as below:

1. If the consideration is received (property is sold) before receipt of Completion Certificate or before its first occupation, GST is leviable at 18% of the Value of property as per agreement of sale, as reduced by the value of land. However, in case of construction of complex, the builder charges an amount which is inclusive of land or undivided share of land. In that case, as per para 2 of Notification No. 11/2017-CT Rate) and No. 8/2017-IT (Rate) both dated 28-6-2017, the land value will be deemed to be one third (33.33%) of total amount (i.e. value including land value) and GST is payable on balance amount. Thus, effectively GST rate is 12% (6% CGST plus 6% SGST/UTGST). Note that GST rate continues to be 18% only. The effective rate comes to 12% only because value of construction is reduced by deducting land value from total amount charged by builder/developer to buyer.

2. If the entire consideration for the property is recived after receipt of Completion Certificate or before its first occupation, then it is not considered as a Supply and hence GST is not applicable in such transaction. In this case, proportionate ITC availavle by the Developer/Landowner would need to be reversed at the time of supply of such service tio the buyer

Time of Supply – Continuous supply as per %Completion/Invoicing or payments received.

3. Allowability of Input Tax Credit (ITC)

♦ ITC for GST paid on Works Contract

- As per section 17(5) (c) of the CGST Act, 2017, input tax credit shall not be available in respect of the following:

- works contract services when supplied for construction of an immovable property (other than plant and machinery) except where it is an input service for further supply of works contract service.

- goods or services or both received by a taxable person for construction of an immovable property (other than plant or machinery) on his own account including when such goods or services or both are used in the course or furtherance of business.

- Thus, ITC for works contract can be availed only by one who is in the same line of business and is using such services received for further supply of works contract service. For example a building developer may engage services of a sub-contractor for certain portion of the whole work. The sub-contractor will charge GST in the tax invoice raised on the main contractor. The main contractor will be entitled to take ITC on the tax invoice raised by his subcontractor as his output is works contract service. However if the main contractor provides works contract service (other than for plant and machinery) to a company say in the IT business, the ITC of GST paid on the invoice raised by the works contractor will not be available to the IT Company.

- The Developers are entitled to take credit of ITC for GST paid on purchase of Steel, Cement and other such items as well as on various types of services like architectural, engineering, manpower services from various registered Suppliers. They also entitled for ITC on tax paid on reverse charge mechanism for purchases made from unregistered Suppliers.

- The Landowner also may take ITC for tax collected by Developer when he hands over the possession rights of flats to the Landowner

- The Input Tax Credits so taken may be utilized by the Developer and/or Landowner towards liability of payment of GST when they sell flats to Buyers before receipt of Completion Certificate.

Generally, at the time of taking credit, the Developer / Landowner, may not know whether the flats will be sold out before or after the receipt of Completion Certificate, therefore they avail total eligible credit and in case they sell any flats after the completion certificate or decided to retain for own use, then the corresponding credit should be reversed at the time of such sales or decision to use on their own.

4. Valuation of Consideration

The valuation of Construction Services (referred to in Trasaction 1 above) or Development rights (referred to in Trasaction 2 above) for the purpose of GST will be the value of free flats/shops given to the Landowner.

- As per CBI&C circular dated 10-2-2012, the valuation of flats given free should be on basis of similar services or flats sold in Open Market. The issue is whether the value of similar flats/shops given to others is comparable with flats given free to Landowner or transferor of TDR i.e. whether that value closely or substantially resembles the value of construction of flats given ‘free’

- It is clear that GST is payable on value of supply of construction services or development rights. This value cannot include value of land, while open market value of similar flats includes value of land also. It is obvious that value of land is recovered by builder/owner from buyers of flats who pay in cash. Thus, value of land is apportioned only on flats which are sold for cash and not on all flats. Thus, the value of land is included in the price charged to buyers. In fact, it is much higher than the average value of land, if such value was apportioned on all flats/shops.

- Can we apply ‘deeming provision’ to calculate value of construction service or development rights on basis of open market value of flats?

- The general rate of GST on construction and works contract service is 18% (9% CGST plus 9% SGST/UTGST). However, in case of construction of complex, the builder charges an amount which is inclusive of land or undivided share of land. In that case, as per para 2 of Notification No. 11/2017-CT (Rate)and 8/2017-IT (Rate) both dated 28-6-2017, the land value will be deemed to be one third (33.33%) of total amount (i.e. value including land value) and GST is payable on balance amount.

- Thus, effectively GST rate is 12% (6% CGST plus 6% SGST/UTGST). Note that GST rate continues to be 18% only. The effective rate comes to 12% only

because value of construction is reduced by deducting land value from total

amount charged by builder/developer to buyer. - However, in my opinion, such deeming provision may no apply as the actual value of land as included in open market value of similar flats may be more than

33%.

- Hence, in my view, the Developer has following choices for valuation of Construction Service (which becomes the value of Development rights as well) in accordance with CGST and SGST Rules, 2017:

- Value on basis of ‘deeming provision‘ considering value of land as 33.33%, if the actual land value is around that figure or less than 33.33% [Rule 31 i.e. ‘using reasonable means’ consistent with Acts and Rules].

- Value on basis of cost plus 10% under Rule 30.

- Value on the basis of price of similar flats/shops after deducting value of land (if value of comparable land is available) as apportionable to that flat/shop [Rule 31].

** Though there is clarity vide Notification No. 4/2018-Central Tax (Rate), dated 25th January, 2018, many experts and real estate industry questioning the applicability of tax on mere transfer of land development rights by owner to a real estate developer. Some builders have dragged the GST Council, Central and Maharashtra governments, to court for including such transactions under the GST framework, citing such transactions were exempt under the previous service tax regime and the notification goes against the essence of GST framework that excludes sale of land and building from tax ambit. Also there is certain apprehensions and confusions regarding valuation of Development Rights passed on by the Landowner to Developer and Construction Services for the free flats/offices/shops provided by the Developer to the Landowner.

Disclaimer: The views, opinions and arguments presented in this article are those of the author and may not necessarily reflect legal standing.

Author: CA Rahul Jain can be reached at rahuljainassociates@gmail.com. More details on http://rahuljainassociates.in

Dear Sir,

Recently GST rate on affordable housing is reduced from 8% to 1%, Now my query is few builder has generated demand letter in March 19 with 8% of GST. However buyer’s loan will be going to disburse in April 19.

So which GST rate is applicable while processing payment 8% or 1% ??

Superb article sir,sir i have doubt if entire consideration received after it’s first occuapation is exempt even if completion certificate not obtained from authorities.Sir in yesterday cbic press release said that gst will be levied on ready to move on properties or constructed properties if completion certificate is not obatined at the time of sale.sir pls clarify

Dear Rahul Jain

Article super. It’s comprehensive.The closing comments “many experts and real estate industry questioning the applicability of tax on mere transfer of land development rights by owner to a real estate developer.” is the life line.

All the best