As per section 2(56) of GST Act, ISD means an office of the supplier of goods and / or services which receives tax invoices issued under section 23 towards receipt of input services and issues tax invoice or such other document as prescribed for the purposes of distributing the credit of CGST (SGST in State Acts) and / or IGST paid on the said services to a supplier of taxable goods and / or services having same PAN as that of the office referred to above;

Explanation.- For the purposes of distributing the credit of CGST (SGST in State Acts) and / or IGST, Input Service Distributor shall be deemed to be a supplier of services.

Here we will know the Manner of issue of ISD, Format of invoice to be issued by an ISD and Return of ISD.

A. Manner of issue of ISD

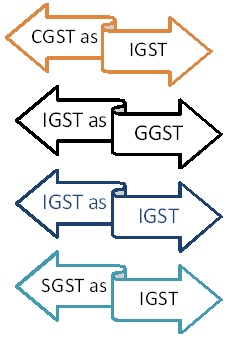

Before going through the contained of article, it would be worth to know that right now we are transferring CENVAT as ISD to our manufacturing recipient and they are using same for Excise Duty/Service Tax payment without one to one relationship.

But under GST scenario as Credit of SGST may not be used with CGST similarly Credit of CGST may not be used against SGST. Only the Credit of IGST may be used against both and itself too as per section 35 of GST Act.

1) As per section 17 specify the manner in which ISD may be distributed

Therefore a like present scenario we may not distributed consolidated credit under a head to our operating manufacturing unit, as Credit of CGST and SGST may not be used against each other.

2) The amount of the credit distributed shall not exceed the amount of credit available for distribution

3) the credit of tax paid on input services attributable to a supplier shall be distributed only to that supplier ( same as Present)

4) the credit of tax paid on input services attributable to more than one supplier shall be distributed only amongst such supplier(s) to whom the input service is attributable and such distribution shall be pro rata on the basis of the turnover in a State of such supplier, during the relevant period, to the aggregate of the turnover of all such suppliers to whom such input service is attributable and which are operational in the current year, during the said relevant period (same as Present).

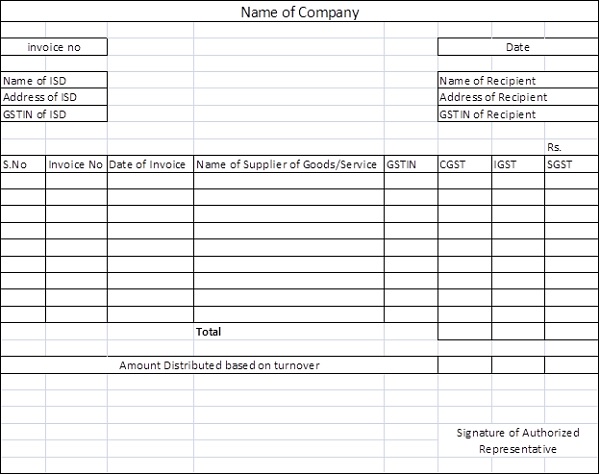

B) Input Service Distribution Invoice: Draft invoice Rule-5 specifies several content of invoice of an ISD. Based on same a format is designed for ready reference.

In respect of ISD invoice, we must know following:-

a) Invoice No shall be unique and in consecutive serial number

b) Invoice shall contain only alphabets and/or numerals (mean no special character shall be allowed)

c) No need to mention nature/type of service

d) Correct Invoice No and GSTIN shall be filled very carefully as in case mismatch with credit to manufacture may be disallowed.

e) In case of Input Service Distributor is an office of a banking company or a financial institution including a non-banking financial company, a tax invoice shall include any document in lieu thereof, by whatever name called, whether or not serially numbered but containing the information as prescribed above.

f) Two separate ISD invoice may be issued one for common credit and another for specific.

g) Invoice may be digitally signed or ink signed

C) Return of ISD:

1) Section 27(6) says that Every Input Service Distributor shall, for every calendar month or part thereof, furnish a return, electronically, in such form and in such manner as may be prescribed, within thirteen days after the end of such month

2) at present ISD is filling only two Return in a Financial Year, but now under GST they are required to file a return every month by 13th of next month, means total 12 return in year.

Author Bio