Dr. Sanjiv Agarwal, FCA, FCS

The GST law contains a unique provision on anti-profiteering measure as a deterrent for trade and industry to enjoy unjust enrichment in terms of profit arising out of implementation of Goods and Services Tax in India, i.e., anti-profiteering measure would obligate the businesses to pass on the cost benefit arising out of GST implementation to their customers.

The provisions on anti-profiteering are contained in the GST law as per following provisions:

| CGST Act, 2017 | Section 171 on Anti-profiteering measures. |

| IGST Act, 2017 | Section 20 which stipulate that provisions of the GST Act, 2017 shall apply mutatis mutandis to IGST Act. |

| UTGST Act, 2017 | Section 21 which stipulate that provisions of GST Act, 2017 shall apply mutatis mutandis to UTGST Act. |

| SGST Act, 2017 | Section 171 on Anti-profiteering measures. |

The Rules for Anti Profiteering are contained in Chapter XV (Rule Nos. 122 to 137) of the Central Goods and Services Tax Rules, 2017.

Objective of Anti-Profiteering Measure

Section 171 provides that it is mandatory to pass on the benefit due to reduction in rate of tax or from input tax credit to the consumer by way of commensurate reduction in prices.

Concept of Anti profiteering Measure

While every business would like to earn more and more profits from business, given an opportunity, it is a fact that GST is a new concept being introduced in India for first time and claimed as a major tax reform and that experience suggests that GST may bring in general inflation in the introductory phase. The Government wants that GST should not lead to general inflation and for this, it becomes necessary to ensure that benefits arising out of GST implementation be transferred to customers so that it may not lead to inflation. For this, anti profiteering measures will help check price rise and also put a legal obligation on businesses to pass on the benefit. This will also help in instilling confidence in citizens.

Statutory Provisions

As per section 171 of the CGST/SGST Act, any reduction in rate of tax on any supply of goods or services or the benefit of input tax credit shall be passed on to the recipient by way of commensurate reduction in prices. An authority may be constituted by the government to examine whether input tax credits availed by any registered person or the reduction in the tax rate have actually resulted in a commensurate reduction in the price of the goods or services or both supplied by him.

As per rule 127, Anti-Profiteering Authority (APA) shall be duty bound to:

- determine whether any reduction in rate of tax on any supply of goods or services or the benefit of the input tax credit has been passed on to the recipient by way of commensurate reduction in prices.

- identify the registered person who has not passed on the benefit of reduction in rate of tax on supply of goods or services or the benefit of input tax credit to the recipient by way of commensurate reduction in prices.

- pass an appropriate order.

The powers to take action are also listed as duties whereby it can order price reduction, refund of profit, recovery, penalty or even cancellation of GST registration.

Anti-profiteering Authority

The Authority constituted by Central Government shall have powers to impose a penalty in case it finds that the price being charged has not been reduced consequent to reduction in rate of tax or allowance of input tax credit.

Section 17 on anti-profiteering means shall have a sunset clause. The rules framed for anti-profiteering as approved by the GST Council indicate that it would operate for a period of only two years. Thus, it would lease to exist after two years of being in force.

During the two years of initial transition into GST regime, Anti-Profiteering Authority (APA) shall step in and may ask businesses that have not passed on full benefits of reduced tax burden to consumers to make up for such benefit, with interest.

Authority for Checking Anti-profiteering Activities

The Government has notified anti-profiteering authority (APA) which will check any undue increase in prices of products of companies under GST. The APA will work to check any undue increase in prices of products by taxpayer companies under the GST regime.

It will work in a three-tier structure- a Standing Committee on Anti-profiteering as well as State-level Screening Committees. The National Anti-Profiteering Authority would consist of five members, including a Chairman.

It will also constitute State-level Screening Committees, which will have one officer of the State Government, to be nominated by the Commissioner, and one officer of the Central Government, to be nominated by the Chief Commissioner. The Additional Director General of Safeguards will be the Secretary to the Authority.

Functions of Authority

The Authority under section 171 shall have the following monitoring functions :

(a) Input tax credit availed by taxpayer have actually resulted in commensurate reduction in price of goods / services

(b) The reduction in prices on account of reduction in tax rates have actually resulted in a commensurate reduction in price of goods / services.

Duties of APA

As per Rule 8, APA shall be duty bound to :

- to determine whether any reduction in rate of tax on any supply of goods or services or the benefit of the input tax credit has been passed on to the recipient by way of commensurate reduction in prices.

- to identify the registered person who has not passed on the benefit of reduction in rate of tax on supply of goods or services or the benefit of input tax credit to the recipient by way of commensurate reduction in prices.

The powers to take action are also listed as duties whereby it can order price reduction, refund of profit, recovery, penalty or even cancellation of GST registration.

The Government is committed to ensure all consumers enjoy the benefit of lower prices of goods and services under GST. Under GST, suppliers of goods and services must pass on any reduction in the rate of tax or the benefit of input tax credit to consumers by way of commensurate reduction in prices.

Anti-profiteering Authority (APA) shall act a monitoring and regulatory authority to curb anti-profiteering practices of tax payers under GST regime. The APA shall be duty bound to:

- Make company reduce the prices

- Make company refund the money to the consumer alongwith interest @ 18% p.a.

- Order company to deposit the refund amount in the Consumer Welfare Fund (in case the buyer is not identifiable)

- Impose monetary penalty equivalent to amount involved in undue profiteering

- Cancel registration of the assessee

However, such action would be based on the recommendations of the Directorate General of Safeguards. Also such powers would be used in extreme cases.

Affected consumers may file an application, in the prescribed format, before the Standing Committee on Anti-profiteering if the profiteering has all-India character or before the State Screening Committees if the profiteering is of local nature.

Though there is a legal provision in the GST law itself to take action against of undue profiteering, Government has taken various steps to ensure action on the part of manufacturers and suppliers so that the benefit is passed on to ultimate beneficiaries, i.e., the consumers. Even on existing stocks lying unsold, there is going to be revised prices put by way of stickers or otherwise. Since old and new (revised) prices would be displayed, a comparison thereof will show the benefit passed on due to lower tax cascading.

Government has also recently introduced form for making application for complaint of anti-profiteering by way of a prescribed form called Form APA F-1 which has to be filed before standing committee or state level screening committee as prescribed in Rules. However, the form introduced is very complex and consumers will only be discouraged to file a complaint. Applicant is also required to mention his code, registration number, HSN code, MRP etc. It is a technical form with many annexures. Separate application has to be filed for different type of goods and services. For example, if one has a single invoice for five items, he need to file five forms with copies of invoice(s), proof of identity, price lists, detailed working street etc so much so that even any professional would find it difficult to lodge a complaint.

One of the measures to curb undue profiteering could be to take a declaration or undertaking from vendors / suppliers that the due benefits accruing to them because of GST have been passed on. In case of large clients such as public sector enterprises or banks or large listed companies, there could even be mechanism of getting verification done by any external agency / internal auditor etc. Alternatively, such vendors or suppliers could be asked to tender a Chartered Accountant / Cost Accountant certificate to this effect. CBEC may also conduct test audits in this regard.

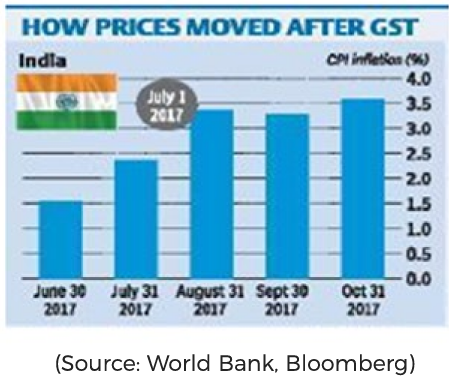

Undue or excessive (more than normal or reasonable profit) is bad, both from ethical as well as legal angle. Further, it is inflationary and does not help anyone except the profiteer itself or himself. Yes, Government’s revenue may also see a little upsurge resulting from higher turnover and profits. Prices ought to be brought down in post GST regime which have otherwise witnessed a rising trend post GST from July, 2017. This is also one of the reasons why Reserve Bank had not reduced the interest rates in this week’s monetary policy review, although GST has been introduced and propagated as non-inflationary tax due to removal of tax cascading.

How inflation has fared post GST in India can be seen in the following graph :

Anti-profiteering Measures Abroad

Anti-profiteering Measures Abroad

It we look at other economies where GST was introduced earlier, the consumer price inflation witnessed a download trend. For example, in New Zealand (introduced in 1991), Singapore (introduced in 1994) and Malaysia (introduced in 2016). However, in Australia, where it was introduced in 2000, there has been a mixed trend with ups and downs.

Global experience suggest that anti-profiteering provisions are only effective if there is a significant lead-in time to allow the relevant authority to educate consumers and businesses as to their respective rights and obligations. The concept of anti- profiteering provision has been perhaps borrowed from Australia which was the first country to enact similar provisions when it replaced a series of inefficient taxes with a GST in July, 2000. The Australian Competition and Consumer Commission (ACCC) was charged with the responsibility of monitoring prices 12 months before the commencement of GST. The ACCC’s focus was on educating consumers and businesses. This included the publication of pricing guidelines, communication strategies for different market segments and ‘hot lines’ for consumers and businesses to get advice. Education was supported by extensive and sophisticated monitoring of prices leading up to the introduction of GST and in the months immediately following.

Malaysia also introduced an anti-profiteering provision, along with the introduction of GST in April, 2015 but it led to widespread litigation and was found to be administratively difficult to implement.

In Malaysia, the price control mechanism on account of GST does not fall under the purview of the GST Act, but under the Ministry of Domestic Trade and Consumer Affairs. The Price Control and Anti-profiteering Act, 2011 had been enacted to control price of goods and charge for services and to prohibit unreasonably high profiteering by suppliers. The mechanism to identify unreasonably high profit is governed by the amendments brought about to the Act in 2014, read with the Price Control and Anti-Profiteering (Mechanism to Determine Unreasonably High Profit) (Net Profit Margin) Regulations, 2014. Countries like Canada and New Zealand have also similar provisions.

So far as India is concerned, the main reasons behind inflationary trend are complexities in GST law for anti tax cascading effect, lack of knowledge and availment of correct input tax credit, businesses hiking up the prices just before GST, unethical profiteering by some suppliers, lack of implementation machinery, hike in tax rates in GST regime for services, small and unorganized sector not passing on benefits etc. Apart from other reasons, if anti-profiteering measure are implemented properly and monitoring is done properly, it may help curb avoidable inflation, i.e. it becomes crucial for Government today to seriously implement anti-inflationary / profiteering measures.

The final word

It may be noted that the anti-profiteering measure in GST law is meant to be a deterrent and is an enabling clause so that reduction in tax incidence due to the GST is passed on to the consumers. This is a contentious provision which should be triggered only if there is a credible complaint. Both, centre and states in due course, shall prescribe the procedure for filing the complaints where the complainant facts that the benefit of tax cut has not been passed on to him as well as the quantum of penalty to be imposed. There are many aspects that are currently open ended. An authority is to be empowered to examine this. The finer rules and regulations and penalties are not yet known. The yardstick that would be deployed for such measurement also needs to be spelled out.

To conclude, it can be said that the anti profiteering provision should be enforced in rare case as a exception, rather than as a rule and should not become a hindrance in free business environment and as a tool to invite corruption.

Anti profiteering must equally apply to the exchequer as GST should also not result in undue tax collection (i.e., extra ordinary tax revenue growth) which is much above the GDP growth itself. Can that be thought of and explored ! Let there be level playing field for everyone-the tax collector and tax payer. The tax paid is also a cost to be recovered from customer as after all it is an indirect tax.

Compiled by GSTstreet for #GSTManthan