In the interest of avoiding litigations and trembling investor confidence, the advance ruling plays a very important role. Through this facility, an investor gets clarity over the ambiguous and complex provisions of the law and gets more stability as far as the taxation is concerned. The concept for Advance ruling was first introduced in Income tax laws and later on into the indirect taxes as well.

The Indian system for Advance ruling is also better than some developed nations including United States of America, Australia etc. In India, the Authority for Advance Ruling (AAR) delivers the judgment which is a separate quasi-judicial body which works independently of the Income tax department. However, in some developed nations, the advance ruling is given by the revenue department which in any case cannot be said as an independent body.

Advance Ruling in GST provides certainty in circumstances where law is ambiguous and vague. AR provides full amount of relief from litigation which may leads to heavy amount of penalties and interest in case of there is any demand . it is way of avoiding dispute in future. Section 95 to 106 of the CGST Act,2017 governs the provision for Advance ruling

Page Contents

- Concept of Advance Ruling under GST

- Application for Advance Ruling under GST

- Procedure after receipt of Application

- Appellate Authority for Advance Ruling under GST

- Appeal to the Appellate Authority for Advance Ruling

- Rectification of advance ruling

- Applicability of Advance Ruling

- When the advance ruling may be void

- Conclusion

Concept of Advance Ruling under GST

1. Under this chapter, two separate bodies have been constituted; namely Authority for Advance Ruling or Appellate Authority for Advance Ruling. The application shall be applied in Authority for Advance Ruling (AAR) and if anyone is aggrieved with the order for Advance ruling, then he may appeal to Appellate Authority for Advance Ruling.

2. Authority for Advance Ruling shall be located in each state and shall comprise of one member of CGST and one member of SGST which is to be appointed by the Central Government and the state government..

3. Appellate Authority for Advance Ruling shall be located in each state and shall comprise of the Chief Commissioner of CGST as designated by the Board and the Commissioner of SGST having jurisdiction over the applicant.

Application for Advance Ruling under GST

Any registered person desirous of taking AR shall apply on Form No. ARA01 with deposit of fees of Rs. 5000.

Question on which advance ruling may be taken pertains to ;

(a) classification of any goods or services or both;

(b) applicability of a notification issued under the provisions of this Act;

(c) determination of time and value of supply of goods or services or both;

(d) admissibility of input tax credit of tax paid or deemed to have been paid;

(e) determination of the liability to pay tax on any goods or services or both;

(f) whether applicant is required to be registered;

(g) whether any particular thing done by the applicant with respect to any goods or services or both

amounts to or results in a supply of goods or services or both, within the meaning of that term.

Application can not be admitted which pertains to any question which is already pending or decided in any proceeding under any provision of this Act.

Procedure after receipt of Application

- Application received shall be forwarded to the concerned officer along with any documents if demanded with regards to application.

- Application can not be admitted which pertains to any question which is already pending or decided in any proceeding under any provision of this Act.

- Where members of the authority differs on any question on which AR is sought, make reference to Appellate Authority for hearing and decision.

- Authority shall pronounce its decision with 90 days from the date of receipt of application .

Appellate Authority for Advance Ruling under GST

Appellate Authority for this chapter under the SGST Act or UGST Act shall be deemed to be authority of State or Union Territory.

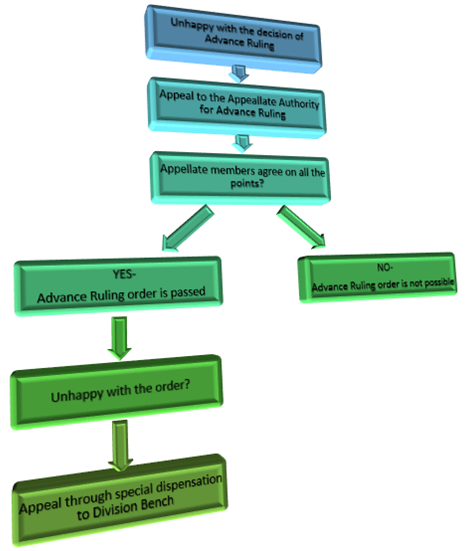

Appeal to the Appellate Authority for Advance Ruling

Appeal to the Appellate Authority for Advance Ruling

Applicant or concerned / jurisdictional officer aggrieved by the order of AAR may appeal to AAAR within 30 days from the date of order of AAR communicated to officer or applicant. This may be further extended to 30 days on submission of proper reasoning. The Appeal shall be filed on Form-ARA-02 with deposit of Fees of Rs. 10000. The same appeal if filed by the concerned officer it shall be on Form-ARA-03 with deposit of NIL fees.

The order of the AAAR shall be made within 90 days from the date of filing the appeal.

Where members of the Appellate Authority differ on any point of the appeal , it shall be deemed that no advance ruling can be issued in respect of that question under appeal.

Rectification of advance ruling

Both the authority can amend its order if there is error apparent on the face of the record within period of six months from the date of its order.

Provided that no order of enhancing the liability or reducing the ITC can be passed unless the opportunity to heard to applicant or appellant has been provided.

Applicability of Advance Ruling

Advance Ruling pronounced by AAR or AAAR shall be binding on applicant and concerned officer or jurisdictional officer. It is not applicable on other persons but certainly the facts of the issue may be guiding factors.

When the advance ruling may be void

where applicant or appellant has obtained the AR by fraud or suppression of material fact or misrepresentation of facts, it may, by order declare the order to be void or ab-initio .

Conclusion

Conclusion

Advance ruling is good for those having doubt on their decision related to matter mentioned above. The benefit of AR that One can avoid the cost of litigation , Penalty, interest. This may be due to vague provision of GST law or lack of clarification on the subject matter or confusion in interpretation of law. But on the contrary , being binding on the applicant, can not deviate with its own interpretation which may be correct in law.

Abbreviations ;

AR …..> advance ruling

AAR — > authority of advance ruling

AAAR-> appellate authority of advance ruling

Disclaimer : The contents of this article are solely for information and knowledge and does not constitute any professional advice or recommendation. Author does not accept any liability for any loss or damage of any kind arising out of this information set out in the article and any action taken based thereon.

About the Author: Author is practicing chartered accountant in Gurugram [ Haryana] and having practice in Goods and Service Tax . He can be reached at sanjeev.singhal@skaca.in. WWW. skaca.in

Author Bio