NATIONAL PENSION SYSTEM (N.P.S.)

BACKGROUND

The National Pension System is a defined contribution scheme launched by Pension Fund Regulatory & Development Authority (P.F.R.D.A) in 2004 for government employees & subsequently in 2009 for all citizen.

The eligible subscribers are allotted a 12 digit unique Permanent Retirement Account Number (P.R.A.N) on registration with N.P.S.

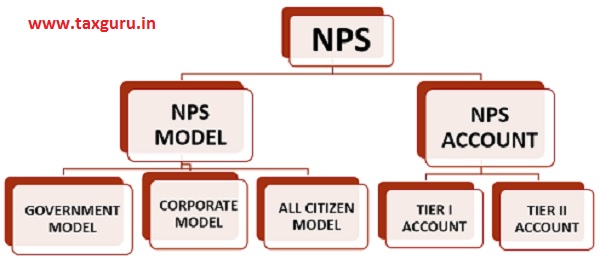

MODELS UNDER N.P.S

- GOVERNMENT MODEL :- This model is for all central & state government/ undertaking employees, who have joined service on & after 1 January 2004. The contribution made is invested in equity (15%) and rest in fixed income securities.

- ALL CITIZEN MODEL:– This model covers all citizens meeting eligibility, the subscriber can decide how the funds will be contributed in equity & debt.

- CORPORATE MODEL:- This model is for corporate who can extend the benefit to their employees, here the contribution can be made by employee alone or employer alone or by both in the decided portion.

- ATAL PENSION YOJANA:- This was launched to provide pension to the weaker section of society, working in unorganized sector.

TYPES OF N.P.S ACCOUNT

- TIER I Account :– Primary retirement saving account, tier I account is the retirement account hence it has restriction on withdrawals & its end use. The subscriber can make 3 nominee with specific percentage to each.

- TIER II Account :– TIER II account is voluntary investment account. The subscriber must have tier I account to open tier II account, funds can be withdrawn at any time from tier II account, funds can also be transferred from tier II to tier I account.

INVESTMENT OPTION UNDER N.P.S

- EQUITY( E ) – High Return, High Risk – funds invest in equity oriented instruments.

- CORPORATE BONDS (C ) – Medium Return, Medium Risk – funds invest in fixed income securities.

- GOVERNMENT SECURITIES (G) – Low Return, Low Risk – funds invest in government securities.

INVESTMENT CHOICE UNDER N.P.S

- ACTIVE CHOICE – the subscriber may choose the proportion of the funds that may be invested in each investment option according to his risk capacity.

- AUTO CHOICE – under this choice the subscriber contribution will be invested in the life cycle fund. It’s the dynamic allocation of wealth in three asset class according to the age of investor.

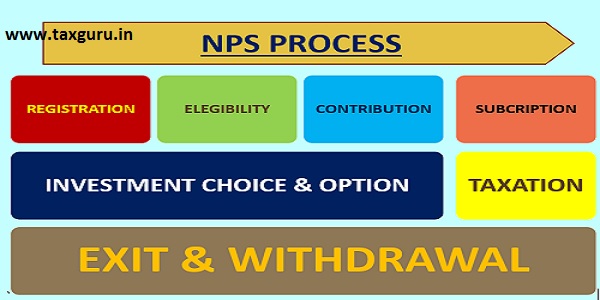

SUBSCRIBING TO N.P.S

- K.Y.C PROCESS – The investor before entering into any financial transaction must be known & verified, this is done through K.Y.C process.K.Y.C involves verification of proof of identity & address. Identity having photograph.

- BANK ACCOUNT DETAIL – While opening Tier I account it is not mandatory to give bank account detail but for Tier II account bank details are mandatory.if the subscriber is N.R.I then his N.R.E/N.R.O account detail should be provided

ELIGIBILITY & DISQUALIFICATION

| ELIGIBILITY | DISQUALIFICATION |

| Any citizen – resident/ non resident | Undischarged insolvent |

| Age 18 – 60 years of age | Person of unsound mind |

| One N.P.S account for subscriber, shift from government, private or corporate model can be done. | Person with existing N.P.S account. |

| N.R.I can also open N.P.S account, copy of passport & proof of address is required. |

REGISTRATION

- THROUGH POP – The subscriber will have to fill the registration form along with the K.Y.C documents to the POP- SP. The generated P.R.A.N card shall be generated & dispatched within 10 days.

- ONLINE – The applicant shall have to visit e-N.P.S website and get himself registered through PAN/AADHAAR. Online portal is much faster can be completed in few minutes through e-sign.

CONTRIBUTION

A Subscriber is required to make initial contribution (minimum of Rs. 500 for Tier I and a minimum of Rs. 1000 for Tier II) at the time of registration.

| Tier I: Minimum amount per contribution – Rs. 500 Minimum contribution per Financial Year – Rs. 1,000 Minimum number of contributions in a Financial Year – one |

| Tier II: Minimum amount per contribution – Rs. 250 No minimum balance required |

TAXATION

- N.P.S comes under partial E.E.T tax regime

- The subscriber receive tax benefit at the time of making investment ( E)

- There is no taxation when return is earned on the contribution made( E)

- At the stage of exit, tax is applicable (T)

TAXATION STAGES

- INVESTMENT STAGE – Contribution made by the subscriber in the pension account is exempt from tax up to Rs 1,50,000 under 80 (c) plus additional deduction of Rs 50,000 under sec 80 (ccd) in N.P.S scheme.

- RETURN/ EARNING STAGE – There is no tax implication in the accumulation stage, where the returns earned are reinvested.

- EXIT STAGE – 40% of the accumulated corpus is tax exempt. further 40% has to be used to purchased annuity. 20% of the accumulated pension will be taxable.

EXIT & WITHDRAWAL

- UPON SUPER ANNUATION – Reaching the age of 60 years, but 40% of the amount shall be used to buy Annuity, if the amount is less than Rs 200,000 then 100% amount shall be withdrawn.

- PRE-MATURE EXIT – In case of pre-mature exit at least 80% of the amount shall be used to buy Annuity rest will be paid in lump sum, if the amount is less than Rs 100,000 then full amount can be withdrawn.

- UPON THE DEATH OF SUBSCRIBER – The entire corpus shall be paid to the nominee or the legal heir.

FAQ:

Q.1 Why should one open N.P.S account.?

Ans. Opening N.P.S account has its own advantages as compared to other pension product available. Below are few features which make N.P.S different from others:

Low cost product Tax breaks for Individuals, Employees and Employers Attractive market linked returns Easily portable Professionally managed by experienced Pension Funds Regulated by P.F.R.D.A, a regulator set up through an act of Parliament.

Q.2 Can I open N.P.S jointly with spouse or child.?

Ans. No, N.P.S account can be opened only in individual capacity and cannot be opened or operated jointly or for and on behalf of H.U.F.

Q.3 How does N.P.S works.?

Ans. A large fund is created by taking small amount of capital from individual investors, which is invested in Government / Corporate /Equity as per the option of the investor, which results in the creation of a balanced fund and its profitability comes in the face of maturity.

Q.4 How will market effect N.P.S.?

Ans. Equity/Corporate bonds are market driven they can garner good returns, but in strain circumstances they give less/ negative returns, However, government security segment will give constant return but in the long run market forces are suggested to give sufficient returns.

Q.5 Why should I chose Tier II Account.?

Ans. No additional annual maintenance Charge. Saving for your day to day need (withdrawal at any point of time). Transfer fund to pension account (Tier I) any time. No minimum balance required. No levy of exit load. Separate Nomination facility available. Option to select different Investment pattern from Tier I.

Author Bio