Inflation has been witnessing moderation since 2014 backed by low food inflation. During the current financial year, however, food and beverages inflation has been trending differently. Food inflation has been on an upward trend mainly backed by rising vegetables, fruits and pulses prices. However, the volatility in prices of most of the essential agricultural commodities with some exceptions like pulses has been on a downward trend. Since July 2018, CPI-Urban inflation has been consistently higher than CPI-Rural inflation, which is in contrast to earlier trend where rural inflation was higher than urban inflation. Inflation has been declining in most of the States, however, the variability of inflation has been increasing. Since 2012, there has been a change in inflation dynamics. There is evidence for a strong reversion of headline inflation to core inflation. Transmission of inflation from non-core components to core components is minimal.

INTRODUCTION

5.1 The global economy has been witnessing a steep decline in inflation over the past five decades (World Bank, 2019). Inflation has declined in almost all the countries around the world. Emerging market economies have also experienced a remarkable decline in inflation over the same period. Inflation peaked in 1993 at 118.7 percent and then declined to 4.8 per cent in 2018 in emerging market and developing economies (World Economic Outlook, October 2019). There can be many reasons that could have contributed to the steep decline in inflation in the emerging market economies like the adoption of a more resilient monetary and fiscal policy frameworks, structural reforms of labour and product markets that strengthen competition, and adoption of monetary policy framework for inflation targeting. Twenty-four emerging market and developing economies have introduced monetary policy frameworks for inflation targeting, since the late 1990s (World Bank, 2019). India introduced inflation targeting on 5th August, 2016 for a period of five years ending on 31st March, 2021.

5.2 In India, inflation has been witnessing moderation since 2014. However, recently inflation has shown an uptick. Headline Consumer Price Index-Combined (CPI-C) inflation increased to 4.1 per cent in 201920 (April to December, 2019) as compared to 3.7 per cent in 2018-19 (April to December, 2018). Though, Wholesale Price Index (WPI) inflation has seen an increase between 201516 and 2018-19, it fell from 4.7 per cent in 2018-19 (April to December, 2018) to 1.5 per cent during 2019-20 (April to December, 2019) (Table 1). Fall in food inflation has been a major contributing factor in the drastic reductions observed in inflation between

Table 1: General inflation based on different price indices (in per cent)

| 2013-14 | 2014-15 | 2015-16 | 2016-17 | 2017-18 | 2018-19 | 2018-19* | 2019-20* | |

| WPI | 5.2 | 1.2 | -3.7 | 1.7 | 3.0 | 4.3 | 4.7 | 1.5 (P) |

| CPI – C | 9.4 | 5.9 | 4.9 | 4.5 | 3.6 | 3.4 | 3.7 | 4.1 (P) |

| CPI – IW | 9.7 | 6.3 | 5.6 | 4.1 | 3.1 | 5.4 | 4.9 | 7.6 |

| CPI – AL | 11.6 | 6.6 | 4.4 | 4.2 | 2.2 | 2.1 | 1.7 | 7.3 |

| CPI – RL | 11.5 | 6.9 | 4.6 | 4.2 | 2.3 | 2.2 | 1.9 | 7.1 |

Source: Office of the Economic Adviser, Department for Promotion of Industry and Internal Trade (DPIIT) for Wholesale Price Index, National Statistical Office (NSO) for CPI-C and Labour Bureau for CPI-IW, CPI-AL and CPI-RL.

Note: CPI-C inflation for 2013-14 is based on old series 2010=100; (P) – Provisional; C stands for Combined, IW stands for Industrial Workers, AL stands for Agricultural Labourers and RL stands for Rural Labourers.

* 2019-20 refers to April to December 2019 for CPI-C, WPI, CPI-AL, CPI-RL and April to November 2019 for CPI-IW.

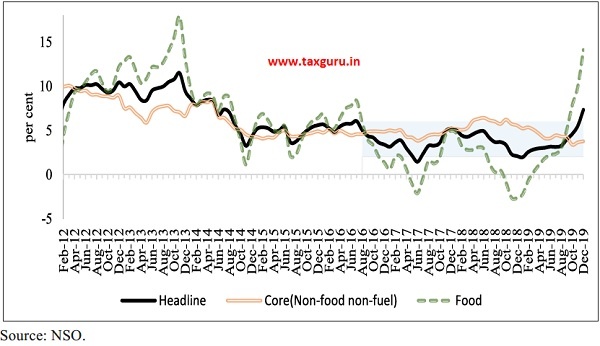

2014-15 and 2018-19. Also, it has been observed that there has been a shift in inflation dynamics. The average levels of inflation have fallen considerably since 2013-14. Not only have the average levels of inflation come down, the peak levels of inflation during the financial year are now much lower. Further, observe that there is convergence of headline towards core inflation from 2012 onwards as per CPI-C.

CURRENT TRENDS IN INFLATION

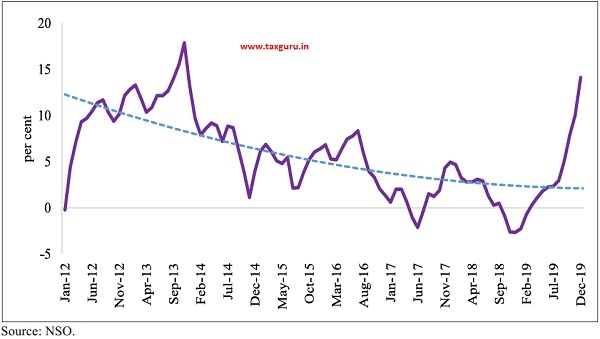

5.3 Headline inflation based on CPI-C has been sliding on a downward path since 2014 (Figure 1). The average CPI-C headline inflation, which was 5.9 per cent in 201415, has fallen continuously to around 3.4 per cent in 2018-19. This has been led by a drastic fall in food inflation, which has fallen from 6.4 per cent in 2014-15 to 0.1 per cent in

Figure 1: Trends in CPI-C Headline, Core and Food inflation

Table 2: Inflation in selected groups of CPI-C Base 2012 (in per cent)

| Description | Weights | 2017-18 | 2018-19 | 2019-20# | Jul-19 | Aug-19 | Sep-19 | Oct-19 | Nov-19 | Dec-19 (P) |

| All Groups | 100 | 3.6 | 3.4 | 4.1 | 3.2 | 3.3 | 4.0 | 4.6 | 5.5 | 7.4 |

| CFPI* | 39.1 | 1.8 | 0.1 | 5.3 | 2.4 | 3.0 | 5.1 | 7.9 | 10.0 | 14.1 |

| Food & beverages | 45.9 | 2.2 | 0.7 | 4.8 | 2.3 | 3.0 | 4.7 | 6.9 | 8.7 | 12.2 |

| Cereals & products | 9.7 | 3.5 | 2.1 | 2.0 | 1.3 | 1.3 | 1.7 | 2.2 | 3.7 | 4.4 |

| Meat & fish | 3.6 | 3.2 | 4.0 | 9.0 | 9.1 | 8.5 | 10.3 | 9.8 | 9.4 | 9.6 |

| Egg | 0.4 | 3.6 | 2.3 | 3.4 | 0.6 | 0.3 | 3.3 | 6.3 | 6.2 | 8.8 |

| Milk & products | 6.6 | 4.1 | 1.8 | 1.8 | 1.1 | 1.5 | 1.8 | 3.1 | 3.5 | 4.2 |

| Oils & fats | 3.6 | 1.6 | 2.1 | 1.4 | 0.9 | 0.6 | 1.2 | 2.0 | 2.6 | 3.1 |

| Fruits | 2.9 | 4.6 | 2.3 | -0.5 | -0.9 | -0.8 | 0.8 | 4.1 | 3.2 | 4.4 |

| Vegetables | 6.0 | 5.8 | -5.2 | 17.6 | 2.8 | 6.9 | 15.5 | 26.1 | 36.1 | 60.5 |

| Pulses & products | 2.4 | -21.0 | -8.3 | 7.8 | 6.8 | 6.9 | 8.4 | 11.7 | 13.9 | 15.4 |

| Sugar & confectionery | 1.4 | 6.1 | -7.0 | -0.2 | -2.1 | -2.4 | -0.4 | 1.3 | 2.1 | 3.4 |

| Fuel & Light | 6.8 | 6.2 | 5.7 | -0.1 | -0.3 | -1.7 | -2.2 | -2.0 | -1.9 | 0.7 |

| CPI excl. food and fuel group (Core) | 47.3 | 4.6 | 5.8 | 4.1 | 4.5 | 4.3 | 4.2 | 3.4 | 3.6 | 3.8 |

Source: NSO.

Note: P: Provisional, * Consumer Food Price Index (CFPI), # April to December 2019.

2018-19. In 2019-20, there has been slight uptick in the headline and food inflation numbers since August, 2019. Overall, CPI -C headline inflation in December, 2019 stood at 7.4 per cent, while CPI-food inflation increased to 14.1 per cent mainly driven by the rise in vegetable prices. Core (non-food non-fuel) inflation has also increased to 3.8 per cent in December, 2019. (Table 2)

5.4 During 2019-20, WPI based inflation has been on a continuous fall declining from 3.2 per cent in April 2019 to 0.6 per cent in November 2019, but increased to 2.6 per cent in December 2019 (Figure 2). Food index which declined on an annual basis between 2017-18 and 2018-19, saw an uptick during the current financial year (April-December, 2019) (Table 3).

Figure 2: WPI inflation

Table 3: Inflation in selected groups of WPI- Base 2011-12 (in per cent)

| Weight | 2017-18 | 2018-19 | 2019-20* | Jul-19 | Aug-19 | Sep-19 | Oct-19 | Nov-19(P) | Dec-19(P) | |

| All Commodities | 100 | 3.0 | 4.3 | 1.5 | 1.2 | 1.2 | 0.3 | 0.0 | 0.6 | 2.6 |

| Food Index | 24.4 | 1.9 | 0.6 | 6.7 | 4.9 | 5.9 | 6.1 | 7.6 | 9.0 | 11.0 |

| Food articles | 15.3 | 2.1 | 0.4 | 8.6 | 6.6 | 7.8 | 7.5 | 9.8 | 11.1 | 13.2 |

| Cereals | 2.8 | 0.3 | 5.5 | 8.2 | 8.7 | 8.5 | 8.7 | 8.3 | 7.9 | 7.7 |

| Pulses | 0.6 | -27.1 | -9.4 | 17.3 | 20.0 | 16.4 | 17.9 | 16.6 | 16.6 | 13.1 |

| Vegetables | 1.9 | 18.8 | -8.4 | 31.4 | 10.5 | 12.9 | 19.3 | 39.0 | 45.3 | 69.7 |

| Fruits | 1.6 | 5.0 | -1.7 | 4.4 | 15.4 | 19.8 | 6.7 | 2.7 | 4.3 | 3.5 |

| Milk | 4.4 | 4.0 | 2.4 | 1.7 | 1.5 | 1.5 | 1.5 | 1.5 | 1.6 | 2.6 |

| Egg, meat & fish | 2.4 | 2.0 | 1.7 | 6.6 | 3.6 | 7.0 | 7.7 | 7.6 | 8.2 | 6.2 |

| Food products | 9.1 | 1.6 | 0.9 | 3.2 | 1.8 | 2.2 | 3.6 | 3.8 | 5.0 | 6.9 |

| Vegetable and animal oils and fats | 2.6 | 2.2 | 7.5 | -2.4 | -6.6 | -4.1 | -2.8 | -1.9 | 2.2 | 9.7 |

| Sugar | 1.1 | 3.4 | -10.7 | 4.0 | -1.0 | 1.4 | 4.7 | 3.2 | 3.1 | 4.7 |

| Fuel & power | 13.2 | 8.1 | 11.6 | -3.1 | -3.6 | -3.5 | -6.7 | -8.1 | -7.3 | -1.5 |

| Non-Food manu- factured products (Core) | 55.1 | 3.0 | 4.2 | -0.3 | 0.0 | -0.4 | -1.2 | -1.8 | -1.9 | -1.6 |

Source: Office of the Economic Adviser, DPIIT.

Note: P: Provisional, *April to December 2019.

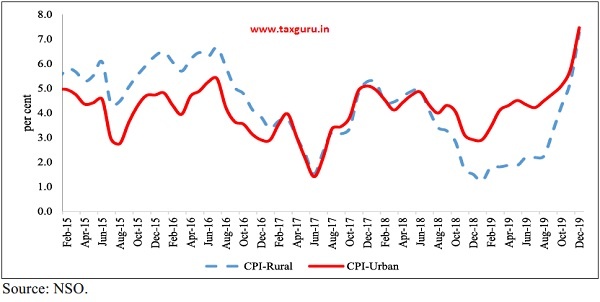

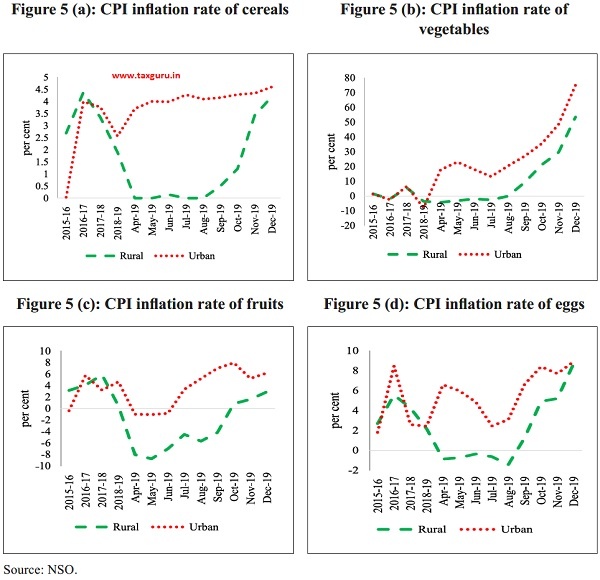

5.5 Since July 2018, CPI-Urban inflation, has been consistently above CPI-Rural inflation (Figure 3). This is in contrast to earlier experience where rural inflation has been mostly higher than urban inflation. The divergence has been mainly on account of the differential rates of food inflation between rural and urban areas witnessed during this period. In 2019-20, there has been sudden change in the trend. Since July 2019, urban areas have registered much higher food inflation when compared to rural areas (Figure 4). Divergence in rural-urban food inflation in 2019-20 was mainly led by cereals, eggs, fruits, vegetables etc. (Figures 5 (a) to (d)).

Figure 3: CPI Rural and Urban inflation

Figure 4: Rural Urban CPI food inflation

Figure 5 (a): CPI inflation rate of cereals Figure 5 (b): CPI inflation rate of vegetables

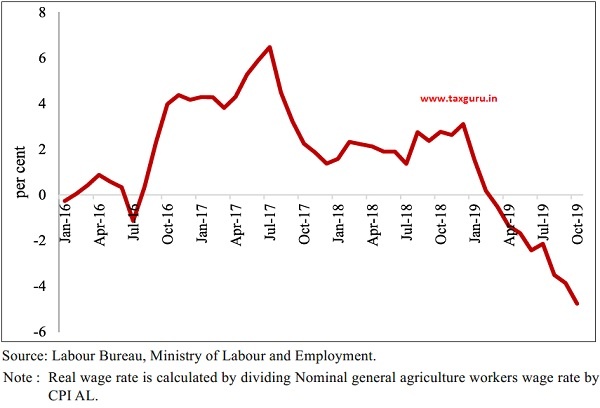

Figure 6: Year on year growth of average real wage rate for agricultural workers during 2016 to 2019 (upto October, 2019)

5.6 The slide in rural inflation could be because of fall in the growth of real rural wages (Figure 6).

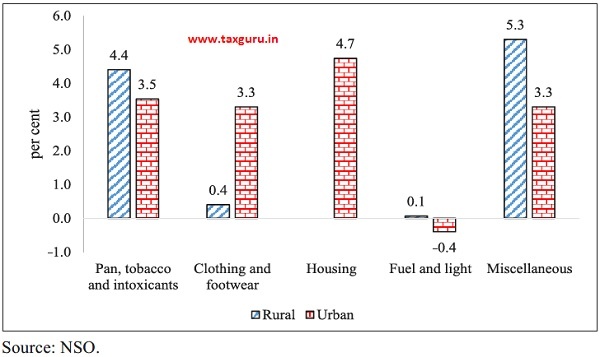

5.7 The divergence in rural-urban inflation is not just observed in the food component but in other components also. Figure 7 shows the component wise rural and urban inflation. In clothing and footwear, inflation in urban areas is 3.3 per cent in 2019-20 (April-December), approximately 3 percentage points higher than that observed in rural areas. For Pan, tobacco and intoxicants, Fuel and light and Miscellaneous groups, inflation observed in rural areas was higher than that in the urban areas. Miscellaneous basket comprises of household goods and services, health, transport and communication, recreation and amusement, education, personal care and effects. However, due to the high overall weight attached to the food and clothing & footwear groups in the rural index, the overall inflation observed in rural areas at 3.4 per cent was lower than the overall inflation observed in urban areas which was at 5.0 per cent in 2019-20 (April-December). The decline in rural inflation in items like clothing and footwear, fuel and light could be due to fall in growth of real rural wages, while rise in rural price index for items like education, health, personal care etc. also raises the question of affordability of these items to the rural segment.

INFLATION IN STATES

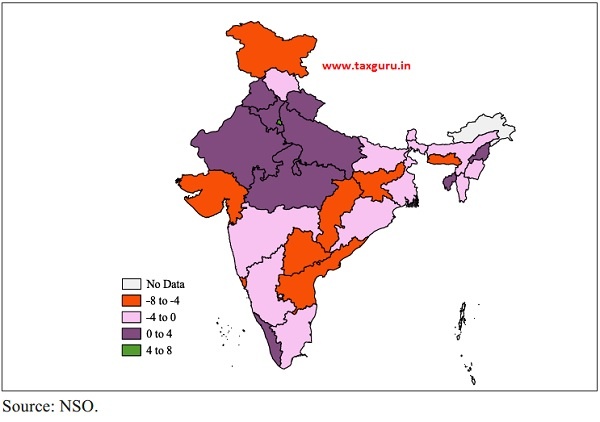

5.8 CPI-C inflation has continued to be highly variable across States. Inflation ranged between (-)0.04 per cent to 8.1 per cent across States/UTs in financial year (FY) 2019-20 (April-December) compared to (-)1.3 per cent to 9.1 per cent in FY 2018-19 (April-December). However, the overall inflation rate has been quite low in almost all the States. Inflation in fifteen States/UTs was below 4 per cent in FY 2019-20 (April- December). Comparing FY 2018-19 (April- December) with FY 2019-20 (April- December), it was observed that inflation has actually decreased in eight States. Nineteen States/UTs had inflation rate lower than All India average for FY 2019-20 (April-December) with Daman & Diu having the lowest inflation followed by Bihar and Chhattisgarh (Figure 8).

5.9 Though in most of the states the overall inflation rate in rural areas is lower than the overall inflation rate in urban areas, the overall variability of rural inflation in a particular month across States was higher than the variability of urban inflation across states. Figure 9 looks at the variability of rural and urban inflation and it was observed that the variability of rural inflation to be very high as compared to variability of urban inflation. (Figure 9 and 10).

Figure 7: Component-wise rural and urban inflation in 2019-20 (April- December)

Figure 8: CPI- Combined inflation for States/Union Territories (in per cent)

5.10 Figure 3 and 9 indicate that though the overall inflation in rural areas is lower at an All India level but due to the high variability across states some states might actually have inflation in rural areas higher than inflation in urban areas.

Figure 10 shows that in Punjab, Haryana, Uttarakhand, Delhi, Rajasthan, Uttar Pradesh, Madhya Pradesh, Nagaland, Tripura and Kerala rural inflation was indeed higher than urban inflation during April-December, 2019.

Figure 9: Variability in rural and urban inflation across States in 2019-20 (April- December)

Figure 10: Difference in rural and urban CPI inflation across States 2019-20 (April- December)

DRIVERS OF INFLATION

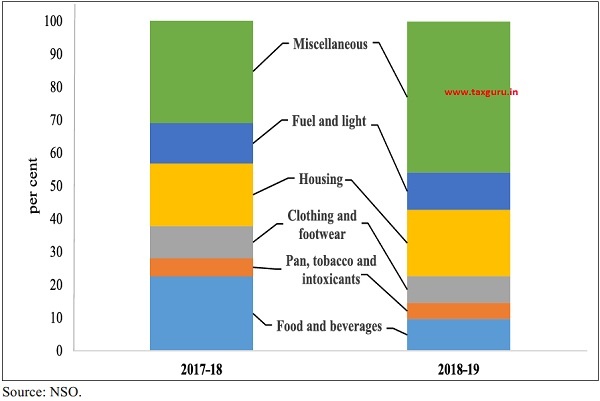

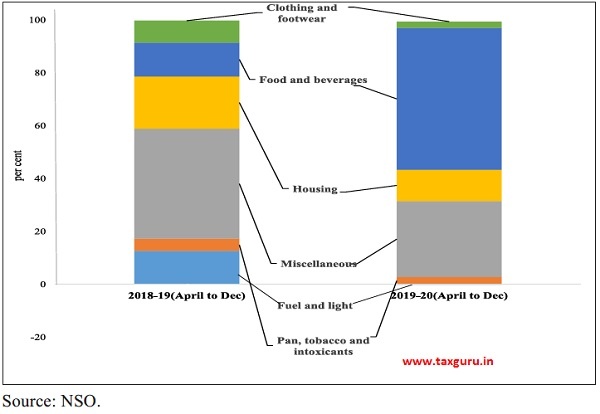

5.11 During 2018-19, the major driver of CPI-C inflation was the miscellaneous group. Compared to 2017-18, the contribution of food and beverages to total inflation was lower in 2018-19 (Figure 11). However, during 2019-20 (April- December), food and beverages emerged as the main contributor to CPI-C inflation, with 54 per cent of the inflation during this period attributable to this group. Miscellaneous group was the second largest contributor to inflation during this period (Figure 12).

CRUDE OIL AND FUEL INFLATION

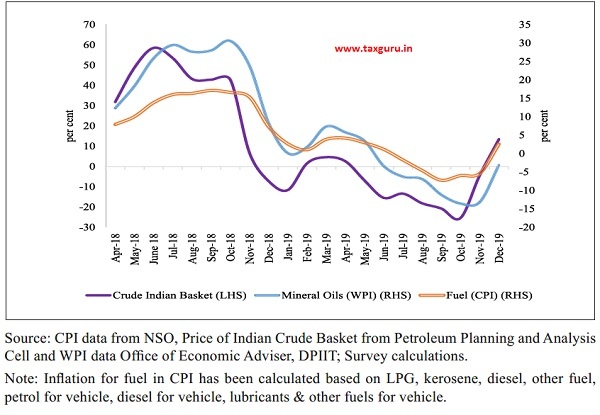

5.12 During April-December 2019, world crude oil prices declined owing to weak global demand. As oil has a major share in the country’s import basket, it impacts considerably domestic prices of petroleum products. The mineral oils group in WPI saw an inflation of 5.8 per cent in April 2019, thereafter saw continuous decline to end at (-)3.2 per cent in December 2019 (Figure 13). Actually, this group in WPI closely tracks the direction of movements in the Indian Crude Basket. The fuel components of CPI also show a movement in a similar direction (Figure 13).

DRUG PRICING

5.13 Ensuring access to affordable health care is one of the primary focus of the Government of India. Out of the total out of pocket expenditure of individuals on health, the major portion is that of medicines. This makes the provision of affordable drugs an imperative. Indian pharmaceutical sector is an important sector not only because of the welfare implications it has, but also because of its economic importance as a sector with a proven record of technical capability and global standing. The sector has grown considerably in the recent years and has potential for further development in the coming years.

Figure 11: Contributions to CPI-C inflation in 2017-18 and 2018-19

Figure 12: Contributions to CPI-C inflation in 2018-19 (April to December) and 2019-20 (April to December)

Figure 13: Year-on-year growth in price of Indian Crude Basket, inflation in Mineral oils in WPI and Fuel in CPI-C

5.14 The Government came out with National Pharmaceutical Pricing Policy, 2012 with an objective to put in place a regulatory framework for pricing of drugs so as to ensure availability of required medicines – “essential medicines” – at reasonable prices even while providing sufficient opportunity for innovation and competition to support the growth of industry, thereby meeting the goals of employment and shared economic well-being for all.

5.15 The essential drugs and medicines are placed under the National List of Essential Medicines 2011 (NLEM) and included in the First Schedule of Drug Price Control Order (DPCO), 2013 and then brought under price control. National Pharmaceutical Pricing Authority (NPPA) has so far fixed the ceiling prices of 860 formulations/packs of drugs included in First Schedule up to December 2019. The details of reduction in prices of scheduled formulations effected under DPCO, 2013 as compared to the highest price prevailing prior to the announcement of DPCO, 2013 for formulation of NLEM 2015 are shown in Table 4.

5.16 The fixation of ceiling prices/Maximum Retail Price (MRP) has resulted in a total saving of `12,447 crores to the public after implementation of DPCO, 2013. This includes the saving of `4,547 crores on account of fixation of ceiling price of coronary stents, `1,500 crores on account of price fixation of Knee implants and `984 crores on account of Trade Margin Rationalisation (TMR) on Anti-cancer drugs.

5.17 In case of cardiac stents, in the post price capping period (2017) over the period of two years, it has been observed that there is 26 per cent increase in the sales of the cardiac stents in the Indian market. It has also been observed that indigenous manufacturers have benefited from the price capping of the cardiac stents as their share in the production has increased by 10 per cent in post price capping period.

FOOD INFLATION

5.18 As discussed in para 5.3, food inflation has been the major driver of inflation during the current financial year, 2019-20. Some commodities such as onion, tomato and pulses have shown high inflation since August 2019. Untimely rains have caused lower production as well as constricted the movement of onion and tomato to the markets. In the case of pulses, the progress in sowing has been at much lower levels than in the previous year.

Table 4: Statement showing range of reduction in ceiling price of scheduled formulation with respect to the highest price prevailing prior to announcement of DPCO, 2013

| Per cent reduction with respect to Maximum Price |

No. of formulations |

| 0<= 5%* | 236 |

| 5<=10% | 138 |

| 10<=15% | 98 |

| 15<=20% | 100 |

| 20<=25% | 92 |

| 25<=30% | 65 |

| 30<=35% | 46 |

| 35<=40% | 26 |

| Above 40% | 59 |

| Total formulations in NLEM 2015 | 860 |

Source: NPPA, Department of Pharmaceuticals.

(a) Onion

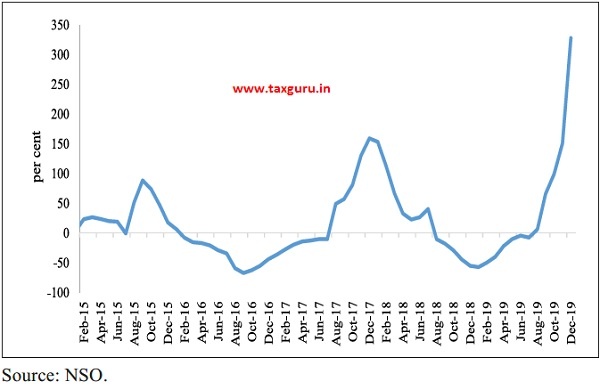

5.19 CPI based Inflation rate of onion showed an increasing trend since April, 2019 and rose up by 328.0 per cent during the month of December, 2019 as compared to December, 2018 on a Year on Year (YoY basis) (Figure 14). The WPI based inflation rate of onion during the month of December, 2019 also increased to 455.8 per cent as compared to a decline of (-) 63.8 per cent in December, 2018 on a Year on Year (YoY) basis.

Figure-14: Month-wise trends in CPI (Combined) inflation rate of Onion (in per cent during 2015-2019

Figure 15: Month-wise trends in CPI (Combined) inflation rate of Tomato (in per cent) during 2015-2019

Table-5: All India monthly arrivals of Onion

| Month | All India Arrivals (in Lakh Tonnes) | ||

| Five Year Average (2013-2017) | 2018 | 2019 | |

| January | 12.9 | 11.1 | 13.0 |

| February | 10.5 | 11.0 | 13.6 |

| March | 9.9 | 9.5 | 12.0 |

| April | 10.0 | 8.9 | 12.8 |

| May | 11.6 | 12.5 | 11.6 |

| June | 10.5 | 12.9 | 13.5 |

| July | 8.0 | 9.8 | 11.0 |

| August | 7.2 | 10.3 | 10.0 |

| September | 7.1 | 10.0 | 7.4 |

| October | 8.0 | 10.8 | 7.4 |

| November | 8.7 | 8.3 | 6.1 |

| December | 11.1 | 10.6 | N.A. |

Source: Monthly Report Onion, November 2019, Horticulture Statistics Division.

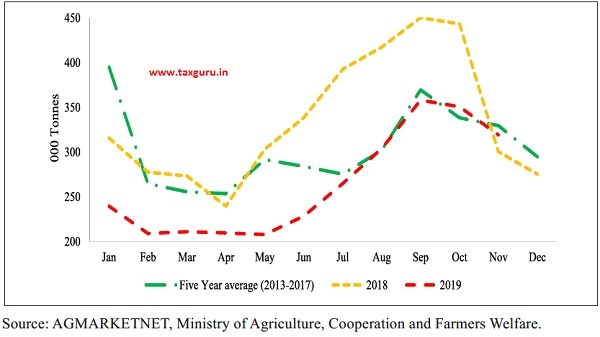

5.20 There can be many reasons for the rise in onion prices. One of the primary reasons that is observed every year is driven by demand-supply mismatch which can be primarily attributed to the seasonal factors. Other reasons that further exacerbated this demand supply mismatch are the fall in area sown and damage to Kharif onion due to rain. As reported from major Kharif growing States (Maharashtra, Karnataka, Madhya Pradesh, Andhra Pradesh, Gujarat and Rajasthan), area sown/transplanted is around 7 per cent less as compared to previous year. Damage to Kharif onion crop also occurred due to heavy rains in September/October, 2019. As reported by State Directorates of Horticulture, damage in Madhya Pradesh was 58 per cent, Karnataka 18 per cent and Andhra Pradesh 2 per cent. The crop in Maharashtra was ready for harvest but got delayed due to continuous rains which was reflected in the low market arrivals of onion during the months from July to November 2019 (Table 5).

(b) Tomato

5.21 CPI based Inflation rate of Tomato showed an increasing trend since July, 2019 and rose up by 35.2 per cent during the month of December, 2019 as compared to December, 2018 on a Year on Year (YoY basis) (Figure 15).

5.22 The price rise in tomato during July-December, 2019 was relatively lower than that observed during 2017. The current spike in the tomato prices in 2019 is mainly due to the excess rains in Maharashtra and Karnataka etc. which are major producers of tomato thus disrupting the supply of tomato.

The market arrivals of tomato in November, 2019 were lower than October, 2019 and also lower than average of five years (201317), but higher than corresponding month of last year. As the market arrivals of tomato declines, the wholesale prices of tomato tend to spike due to demand-supply mismatch as seen since September, 2019. The All India Monthly Arrivals of tomato are shown in Figure 16.

Figure 16: Month wise All India monthly arrivals of Tomato

(c) Pulses

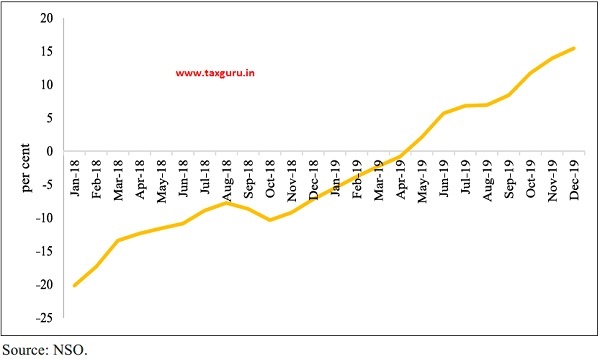

5.23 The CPI inflation rate of pulses increased from -20.2 per cent in January 2018 to 15.4 per cent in December 2019.

The overall rate of inflation, based on CPI, for Pulses during the month of December 2019 stood at 15.4 per cent as compared to -7.2 per cent during December 2018 (Figure 17).

Figure 17: CPI based inflation rates in Pulses (in per cent)

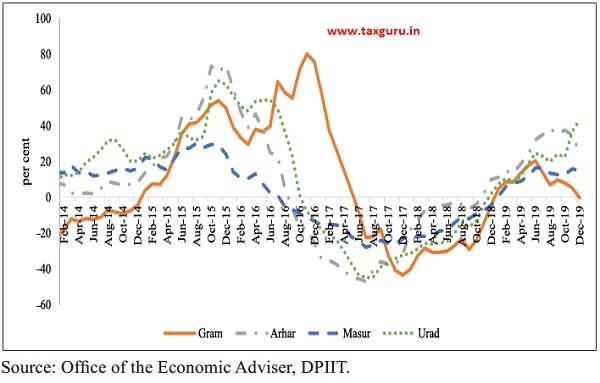

5.24 However, a comparison of the inflation trend of pulses item-wise reveals that the current hike in prices of various pulses compared to their long-term trends is not very high (Figure 18).

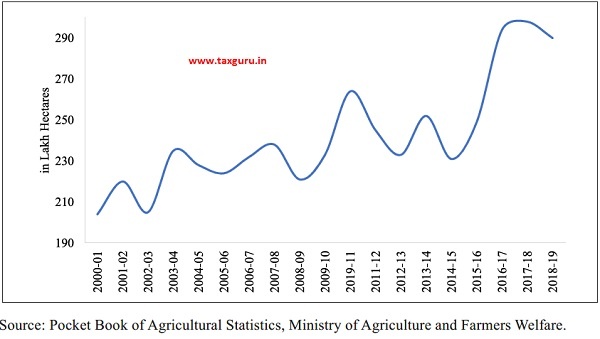

5.25 The phase of price rise during 2019 could be due to fall in acreage resulting from rains in the growing states and also because of low price realisation due to glut in the market following increased production of earlier years. It may be noted here that the production of pulses increased to 231.3 mn tonnes in 2016-17 from 163.5 mn tonnes in 2015-16 – a jump of 41 per cent in a span of one year. In 2018-19 the acreage marginally declined to 290 lakh ha as compared to 298 lakh ha and 294 lakh ha in 2017-18 and 201617 (Figure 19). Low market prices during 2018-19 may have resulted in significant reduction in acreage of some pulses.

Figure 18: Long term inflation trend of various Pulses

Figure 19: Area under Pulses in India

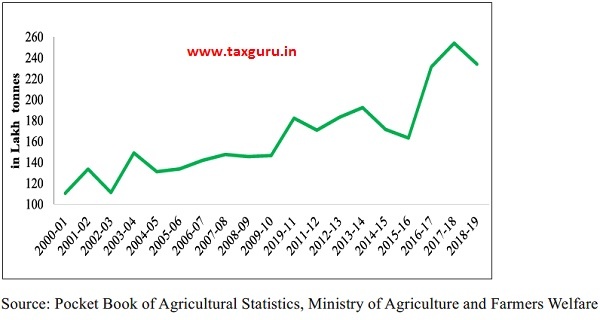

5.26 Production of pulses in which there was a steady increase in production since 201516 shows a steady decline from 2017-18 to 2018-19- a decline of 7.9 per cent during 2018-19 over the previous year (Figure 20).

Box 1 presents the analysis to check for the possibility of presence of cobweb phenomenon in Pulses.

Figure 20: Production of Pulses in India (in Lakh Tonnes)

BOX 1: The cobweb phenomeon in Pulses

Cobweb theory is the idea that price fluctuations can lead to fluctuations in supply which cause a cycle of rising and falling prices. The farmers are caught in the cobweb phenomenon when they base their sowing decisions on prices witnessed in the previous marketing period. So, if the farmer observes a higher price for a specific crop in period ‘t-1’, he would opt to produce more of it in period ‘t’. However, if the production of the crop exceeds market demand, prices fall in period ‘t’, signalling farmers to produce less of the commodity in period ‘t+1’.

The figure below shows the trend of inflation rate of pulses. High peaks are observed on either side. The current peak observed is less than the peak observed in 2015-16. The presence of peaks might indicate towards the presence of cobweb phenomeon in pulses.

WPI inflation rate of Pulses from April 2012 to December 2019

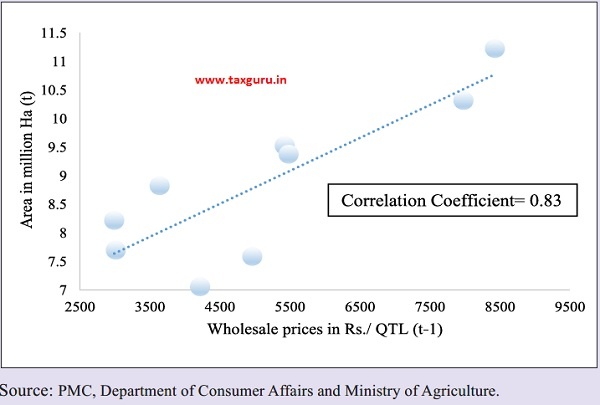

Relation between wholesale price of Gram in Period (t-1) and area sown in period t

Analysing the area sown and wholesale prices for Gram, Tur, Urad and Moong for the period 200910 to 2017-18. Area sown in period ‘t’ and wholesale prices of period ‘t-1’ are considered.

The figure above shows a positive relation between wholesale prices in period t-1 and area sown in period t. The correlation coefficient measures the strength and direction of relation between the two variables. In the case of Gram the correlation coefficient comes out to be 0.83.

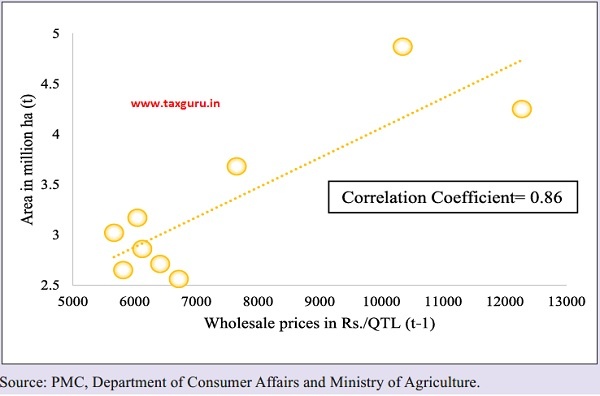

Even in the case of Tur, the association between the two variables is positive and turns out to be even more strong (0.86) as indicated by the value of correlation coefficient.

Relation between wholesale price of Tur in Period (t-1) and area sown in period t

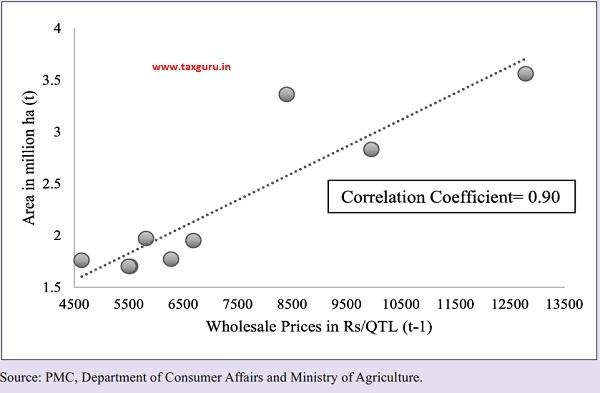

Relation between wholesale price of Urad in Period (t-1)

and area sown in period t

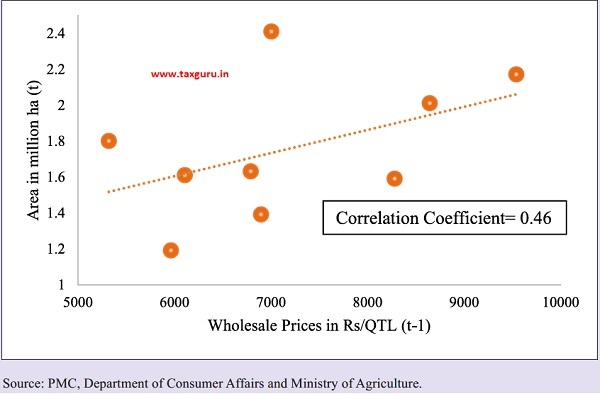

Relation between wholesale price of Moong in Period (t-1) and area sown in period t.

In case of Urad, again positive correlation was observed and the correlation coefficient turned out to be 0.90. A similar positive association for Moong was observed as well, however, in case of Moong the correlation coefficient was relatively weak, at 0.46.

To prevent the occurrence of the cobweb phenomenon, it is essential that apart from existing measures in place to safeguard pulses farmers from crop failure/price shocks like market intervention under Price Stabilization Fund (PSF), coverage under Pradhan Mantri Fasal Bima Yojana, PM-AASHA, providing warehouses, improving transportation, price discovery through e-NAM etc, free export of pulses also needs to be encouraged for India to become self-sufficient in pulses production.

Studies have also suggested that efforts to strengthening procurement by government agencies, increasing openess of external trade, stabilising the prices, reduce transportation cost for farmers by linking them via better roads and effective marketing channels so that production as well as net availability of pulses can be increase thus, leading to improvement in supply of pulses. (CRISIL, 2017)

VOLATILITY IN ESSENTIAL COMMODITY PRICES

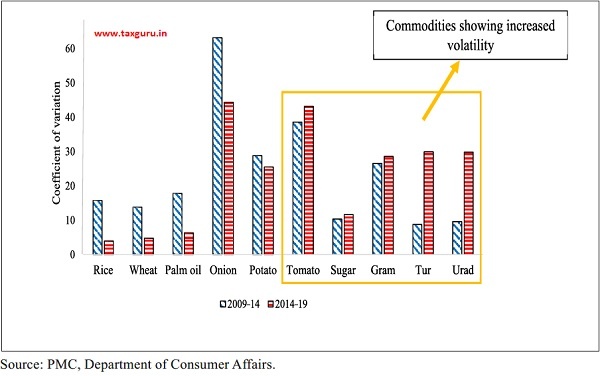

5.27 Wholesale price volatility was analysed for various essential commodities over two time periods i.e. 2009-14 and 2014-19. Coefficient of variation has been used as a measure of volatility. The coefficient of variation is a statistical measure of the dispersion of data points in a data series around the mean. Prices of rice and wheat remained stable since 2014 due to adequate supply arising out of sufficient domestic production and also due to maintenance of adequate buffer stock of rice and wheat for meeting the food security requirements. As a result, the price volatility was lower in the case of rice and wheat (Figure 21). It may be seen that overall price volatility was highest for vegetables and lowest for rice, wheat and palm oil. There was a significant rise in volatility for pulses, sugar and tomatoes during 2014 – 2019.

Figure 21: Coefficient of variation of various essential agricultural commodities

5.28 The extent to which given production and consumption shocks translate into price volatility depends on supply and demand elasticities. Stockholding and speculation can have major impact on price variability, either stabilising or destabilising. Perishability of the commodities also adds to price volatility. Presence of marketing channels, storage facilities, effective MSP system can help limit price volatility.

DIVERGENCE IN RETAIL AND WHOLESALE PRICES FOR ESSENTIAL AGRICULTURAL COMMODITIES

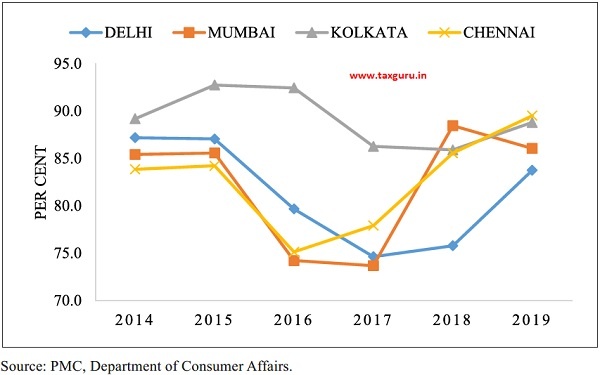

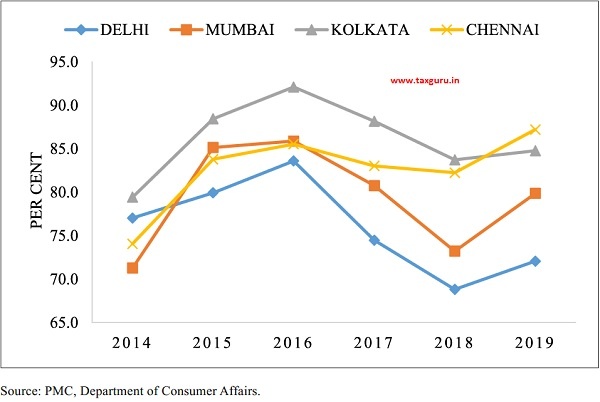

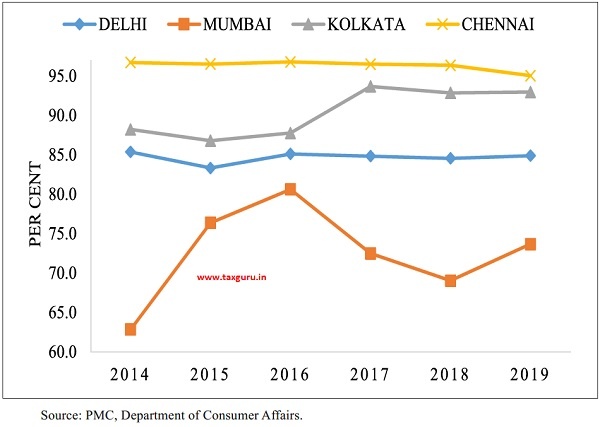

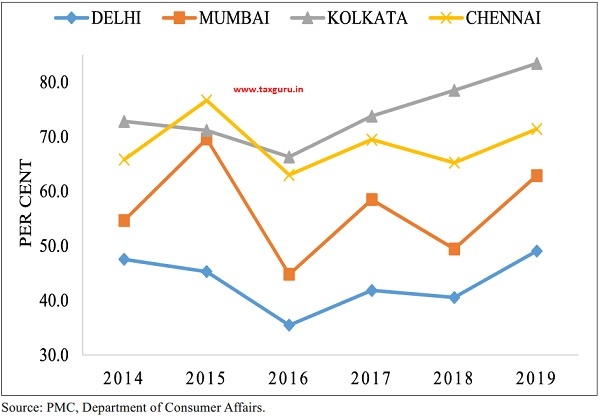

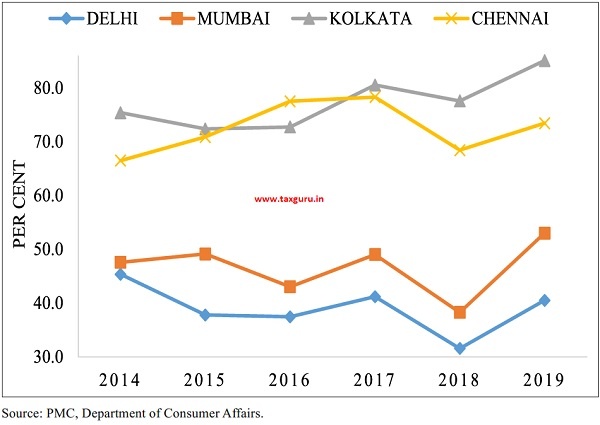

5.29 A divergence between the retail and wholesale price of various essential commodities was observed in the four metropolitan cities of the country over the period 2014 to 2019. A price wedge1 of 10 to 15 per cent per kg is not excessive if one compares this with the marketing costs and margins (Sharma & Pramod, 2001). In 2019 the margins are excessive for some of the commodities, and for all the commodities the margins are highest in Delhi and Mumbai. In case of arhar margins are low at the level of 16 per cent per kg in Delhi and 14 per cent per kg in Mumbai (Figure 22). In case of gram, the margin in Delhi turns out to be around 28 per cent per kg and around 20 per cent per kg in case of Mumbai (Figure 23). In the case of groundnut oil, margins between the wholesale and the retail prices were around 15 per cent in Delhi, while in Kolkata and Chennai margins were at 5-7 per cent. The margins were highest in Mumbai at around 26 per cent for groundnut oil (Figure 24). In the case of vegetables, onion and tomato are analysed. For both price wedge was excessive especially in Delhi and Mumbai. In Delhi, the price margin was 51 per cent for onion and in the case of tomatoes it was 59 per cent (Figure 25 and 26). This implies that vertical spreads in prices is maximum for vegetables that are perishable, then for pulses and the least for edible oils.

Figure 22: Arhar wholesale to retail prices ratio

Figure 23: Gram wholesale to retail prices ratio

Figure 24: Groundnut oil wholesale to retail prices ratio

Figure 25: Onion wholesale to retail prices ratio

Figure 26: Tomato wholesale to retail prices ratio

5.30 The reasons for such a high spread between the wholesale and retail prices could be due to several reasons such as high transaction costs, weak infrastructure and information systems, poor marketing facilities, huge margins of middleman etc. It is a fact that transaction costs in the northern states of the country are high compared to other States (Sharma & Pramod, 2001). The market structure is also different across States. If there is a fair amount of competition in the market between traders, price wedge will not be very high. On the other hand, if traders collude, price wedge will be much higher. Another possible reason for this could be asymmetry in the transmission of price signals from wholesale to retail prices and vice versa, this can happen due to action of intermediaries. Therefore, to reduce the wedge it is important that market barriers and structural rigidities in the system that lead to higher transaction costs are removed.

HAS THERE BEEN A SHIFT IN INFLATION DYNAMICS?

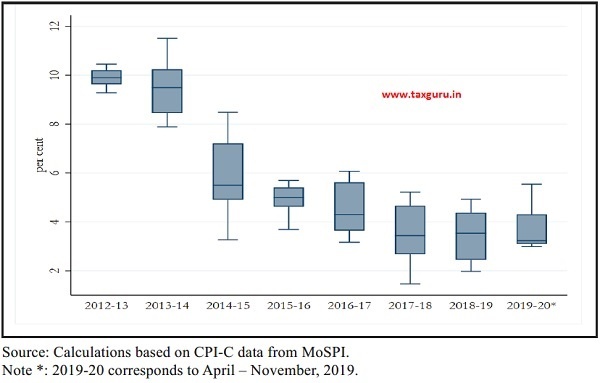

5.31 As discussed earlier in the para No. 5.3, after witnessing high levels of inflation during 2012-13, CPI-C inflation fell in 2013-14 and witnessed a drastic fall from 2014-15 onwards. Given the falling trend in inflation in the recent years, it is pertinent to ask whether there has been a shift in the inflationary process. Figure 27 presents the financial year-wise box-plots2 for CPI-C series for the periods 2012-13 to 2019-20 (Apr-Nov). The average levels of inflation have fallen considerably during this period. Not only have the average levels of inflation come down, the peak levels of inflation during the financial year are now much lower.

5.32 It has been generally believed that, food and fuel inflation in India have had strong

Figure 27: Distribution of CPI-C inflation from 2012-13 to 2019-20*

secondary effects leading to persistence in household inflation expectations. This feeds into core inflation and therefore prolongs the effects on headline inflation (Anand et. al, 2014; Raj and Misra, 2011). One way to check for the presence of secondary effects of food and fuel inflation is to look at the swiftness with which headline inflation converges to core inflation after the occurrence of a food or fuel price shock. If headline inflation does not completely revert back to core inflation within a reasonably short span of time, it may indicate the presence of strong secondary effects. The reversion of headline inflation to core inflation has considerable implications for the conduct of monetary policy in an inflation targeting framework. In an economy with strong secondary effects, monetary policy may have to be tighter in an event of a food or fuel price shock compared to an economy where such effects are minimal.

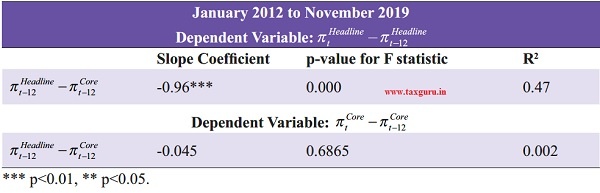

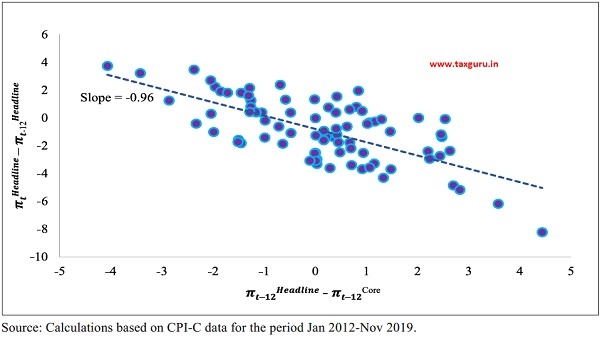

5.33 It was observed that from 2012, there is convergence of headline towards core inflation as per the CPI-C data. The analysis for monthly CPI-C inflation data between January 2012 and November, 2019 was done. The following commonly used equation to test for reversion of headline to core inflation was estimated.

5.34 The results (Table 6 and Figure 28) indicate that in the period under consideration there is evidence of strong reversion of headline inflation to core inflation. The slope for the regression for the period is negative and close to -1, indicating complete reversion of headline inflation to core within a period of 12 months. A similar regression to test for the reversion of core to headline inflation does not provide evidence for the same (Table 6). This implies that secondary effects from non-core components to core components are minimal.

This may have implications for the response of monetary policy to food and fuel price shocks: monetary policy need not become tighter in face of short-term, transitory price shocks in non-core components. However, owning to the large weightage of food and fuel in the consumption basket of consumers in India and the fact that demand-side pressures (and not just supply side factors) are important for food and fuel inflation-focus on headline inflation for monetary policy decisions may be warranted.

Table 6: Testing for reversion of CPI-C Headline to Core inflation

Figure 28: Reversion of CPI-C Headline to Core inflation

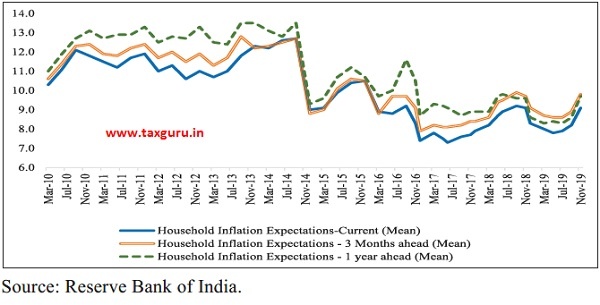

5.35 Two major factors could have contributed to the changing dynamics of inflation in India. First, it was observed that food inflation has seen a declining trend during the period under consideration (Figure 29). The decline in inflation has been witnessed in most categories of food group including those with a high weightage such as cereals and products, fruits, vegetables and pulses and products. Second, inflation expectations have been declining since 2015 (Figure 30). This could be partly because of the success

Figure 29: Consumer Food price inflation

of inflation targeting approach of monetary policy adopted by RBI in anchoring inflation expectations. On the other hand, household inflation expectations are known to move closely with food inflation. The fall in food inflation during this period could have had the effect of reducing the overall inflation expectations of the households. This is also reflected in the fact that proportion of the households expecting the prices of food products for one year ahead to increase has fallen consistently between September 2013 and November 2019.

Figure 30: Inflation Expectations Survey of Households

TRENDS IN GLOBAL COMMODITY PRICES

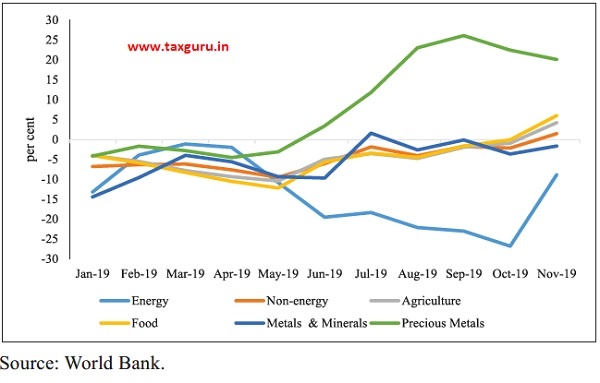

5.36 As per the commodity prices published by the World Bank, energy commodity prices have shown a decreasing trend in 2019-20 (April-November). They recorded average inflation of (-)16.8 per cent in 2019-20 (April-November) as compared to 35.5 per cent in 2018-19 (April-November). In terms of food prices, the deflationary trend continued with inflation of (-)4.3 per cent in 2019-20 (April-November) compared to 0.3 per cent in 2018-19 (April-November). The metals and minerals index also showed a deflationary trend, indicative of the gloomy global economic scenario prevalent during the year (Figure 31).

Figure 31: Inflation trend in global commodity prices (Jan 2019-Nov 2019)

MEASURES TO CONTAIN PRICE RISE OF ESSENTIAL COMMODITIES

5.37 Government takes various measures from time to time to stabilize prices of essential food items which, inter-alia, include utilizing trade and fiscal policy instruments like import duty, Minimum Export Price, export restrictions, imposition of stock limits and advising States for effective action against hoarders & black marketers etc. to regulate domestic availability and moderate prices. Also, Government incentivizes farmers by announcing Minimum Support Prices for increasing production and is implementing Schemes which, inter alia, include Mission for Integrated Development of Horticulture (MIDH), National Food Security Mission (NFSM), National Mission on Oilseeds and Oil Palm (NMOOP), etc. for increasing production and productivity through appropriate interventions. Besides, Government is also implementing Price Stabilization Fund (PSF) to help moderate the volatility in prices of agri-horticultural commodities like pulses, onion, and potato. Onion prices saw a hike during 2019-20 starting from August, 2019, and various measures were taken by the Government to ease the situation which included:

- During 2019-20, buffer stock of 57,373 metric tonnes (MT) Rabi onion was created under Price Stabilization Fund (PSF) through procurement from Maharashtra (48,184 MT) and Gujarat (9,189 MT) which was distributed to various State Governments, other agencies and also sold in various mandis through open auction.

- Onions were supplied to State Governments of Haryana, Kerala, Andhra Pradesh and Uttar Pradesh at no-profit no-loss basis to improve prices and availability situation. During July-Oct., 2019, onions were supplied from the buffer stock for direct retailing in Delhi-NCR through Mother Dairy, NCCF, NAFED and Govt. of NCT of Delhi at regulated retail rates to ensure availability of onions at reasonable prices.

- The benefit to exporters of onions under Merchandise Exports from India Scheme (MEIS) was withdrawn w.e.f. 11th June 2019.

- Minimum Export Price (MEP) of $850/ MT was imposed on onion on 13th September 2019, and subsequently its export was banned by Government on 29th September 2019 in view of its continued high prices.

- Government, on 29th September 2019, imposed stock limits on traders across the country – 100 quintals on retail traders and 500 quintals on wholesale traders under the Essential Commodities Act, 1955, which was subsequently, revised to 20 quintals (2 MT) for retailers and 250 quintals (25 MT) for wholesalers. Further, Government of India urged State Governments to hold regular meetings with the traders of Onions at State and District level to prevent hoarding, speculative trading and profiteering, unfair and illegal trade practices like cartelling, etc.

- Facilitated private imports of onions by relaxing its fumigation norms and exempting importers from stock limits.

- Government imported onions through MMTC from countries like Egypt and Turkey and directed NAFED to procure surplus Kharif onion from producing States like Rajasthan, Maharashtra and undertake distribution in deficit States.

CONCLUSION

5.38 Overall, while the WPI inflation remained low during the financial year 201920, CPI-C inflation saw a slight uptick, driven mainly by food prices. Supply-side shocks in agricultural commodities such as onion due to erratic rains led to the sudden spike in the prices of these commodities. The Government has been taking necessary measures to tackle the rising prices in these commodities. The volatility in inflation of most of the essential agricultural commodities with the exception of pulses has also come down over time. However, one major issue that still remains is the high wedge between retail and wholesale prices of some of the commodities like onion and tomato. The price wedge also varies between different centres indicating presence of large number of intermediaries and high transportation costs. Analysing inflation figures at State level, a divergence is observed in inflation across the States and also between the rural and urban areas within each state. The inflation dynamics have also been changing over time. In the current period, there is evidence for a strong reversion of headline inflation to core inflation. Future inflationary prospects and inflation dynamics crucially depend on the overall macroeconomic scenario as well as the containment of rising prices in certain agricultural commodities.

CHAPTER AT A GLANCE

> Headline Consumer Price Index (CPI) inflation was 3.7 per cent in 2018-19 (April to December, 2018), compared to 4.1 per cent in 2019-20 (April to December, 2019).

> During 2019-20, WPI based inflation has been on a continuous fall declining from 3.2 per cent in April 2019, only marginally rising in November and December to end at 2.6 per cent in December 2019.

> Food index which declined on an annual basis between 2017-18 and 2018-19, saw an uptick during the current financial year (April-December, 2019).

> Since July 2018, CPI-Urban inflation has been consistently higher than CPI-Rural inflation, which is in contrast to earlier trend where rural inflation was higher than urban inflation.

> During 2019-20 (April- December), food and beverages emerged as the main contributor to CPI-C inflation, with 54 per cent of the inflation during this period attributable to this group.

> In the four metropolitan cities of the country, retail prices of various essential commodities have diverged from wholesale prices over the years.

> Since 2012, there has been a change in inflation dynamics. There is evidence for a strong reversion of headline inflation to core inflation. However, transmission of inflation from non- core components to core components is minimal. Therefore, there may be a case for monetary policy to not respond to transitory shocks in non-core components of inflation.

> Inflation in fifteen States/Union Territories (UTs) was below 4 percent in FY 2019-20 (April- December). Comparing FY 2018-19 (April- December) with FY 2019-20 (April- December), inflation has actually decreased in eight states.

> Inflation expectations have declined thereby indicating that the inflation targeting framework has started influencing expectations of inflation in the economy.

REFERENCES

Aayog, NITI. 2018. “Strategy for New india.”

Anand R., Ding D. Tulin V. 2014. Food inflation in India: Role of Monetary policy. IMF.

CRISIL. 2017. “Pulses & Rhythms: Analysing volatility. cyclicality and cobweb phenomeon in prices.” http://www.crisil.com

Dholakia, Kadiyala. 2018. “Changing Dynamics of inflation in India.” Economic and Polictical weekly Vol LIII No 9.

IMF. 2019. World Economic Outlook.

Kundu, Sujata. 2018. Rural wage dynamics in india: What role does Inflation Play. Reserve Bank of India working paper.

Raj J., Mishra S. 2011. “Measures of Core Inflation in India: An Empirical Evaluation .” Reserve Bank of india Working paper Series No. 16/2011.

Sharma Anil, Pramod Kumar. 2001. An Analysis of the Price Behaviour of Selected Commodities. Planning Commission.

World Bank. 2019. “Inflation in Emerging & Developing Economies, Drivers & Policies.” http://www.worldbank.org/inflation

Notes:

1 Wedge= [1- (Wholesale price per kg/Retail price per kg)]*100

2 Box and whisker plots enable us to study the characteristics of a distribution. The box shows the inter-quartile range, that is the 75th and 25th points on the distribution. The horizontal line in the box indicates median of the distribution and the whiskers are lines running from the box to the maximum and minimum values.