International Financial Services Centres Authority

Circular F. No. 722/IFSCA/Banking/2022-23/1 | Dated: September 19, 2022

To,

All IFSC Banking Units

Madam / Sir,

Sub: Reporting of Transactions for India’s External Account Statistics

1. The Balance of Payment (BOP) and International Investment Position (IIP) Manual – Sixth Edition (BPM6) of the International Monetary Fund (IMF) provides a statistical framework for a comprehensive, consistent and flexible set of macroeconomic accounts and prescribes international standards for economy-wide external sector statistics (ESS). BPM 6 is produced and released under the auspices of the United Nations (UN), the European Commission (EC), the Organisation for Economic Cooperation and Development (OECD), the IMF and the World Bank (WB) Group.

2. With the signing of General Agreement on Trade in Services (GATS) under World Trade Organisation (WTO), the member countries are required to disseminate the data on international trade in services as per Manual on Statistics on International Trade in Services (MSITS). Accordingly, detailed BOP statistics are released on a quarterly basis and BOP for services are released on a monthly basis. The Reserve Bank of India (RBI), compiles and disseminates India’s BOP and other external sector statistics as per the global prescriptions, encapsulating a national perspective.

3. As you are aware, in terms of the Foreign Exchange Management (International Financial Services Centres) Regulations FEMA.339/2015-RB, dated March 2, 2015 – issued by the RBI under the Foreign Exchange Management Act, 1999 (FEMA), a financial institution or a branch of a financial institution (referred as IFSC entities) set up in the IFSC is treated as a non-resident entity, for the purposes of the FEMA. The IFSC entities shall conduct permitted business activities in such foreign currency and with such persons, whether resident or otherwise, as the concerned Regulatory Authority may determine.

4. However, as the entities operating in International Financial Services Centre (IFSC) with an Indian address, are residents of India, under the global framework of BPM6, the transactions between resident (with Indian address) and non-resident, facilitated by IFSC Banking Units (IBUs), need to be included in the external sector statistics for India. The rationale for the same is explicitly provided under BPM 6, that notes “… a free trade zone or offshore financial center may be exempt from certain taxation or other laws. Because of the need to view the whole economy, to have comprehensive global data, and to be compatible with partner data, these special zones always should be included in the economic statistics of that economy…”.

5. In view of the rapidly growing volumes and significant value of transactions in IFSC, it has been decided, in consultation with the RBI, that the IBUs shall be required to report the transactions between resident (Indian address) with the rest of the world, for the compilation of India’s BOP statistics and other external statistics as per international guidelines given by the International Monetary Fund (IMF). This information is also important for policy making and other macroeconomic management purposes. The IBUs shall capture and report the purpose, currency, amount, and country of their foreign exchange transactions in the Foreign Exchange Transaction Electronic Reporting System (FETERS) managed by the RBI, as per the formats prescribed by the RBI.

6. In this regard, the IBUs are advised to refer to the RBI circulars viz. A. P. (DIR Series) Circular No. 84 dated February 29, 2012, A.P. (DIR Series) Circular No. 50 dated February 11, 2016 and A.P.(DIR Series) Circular No. 25 dated March 25, 2019 giving guidelines for compilation and reporting of foreign exchange transactions in R-return and A .P. (DIR Series) Circular No. 3, dated August 10, 2017 for compilation and reporting of banking assets and liabilities in BAL return under the FETERS. While these AP Dir Circulars issued by the RBI under the FEMA are addressed to the Authorised Persons (AD banks) in India, they are being referred to by the IFSCA for the limited purpose of providing the relevant guidelines to IBUs in setting up their internal processes for reporting under the FETERS.

7. Accordingly, the IBUs are, hereby, directed to report the details of their foreign exchange transactions undertaken from November 1, 2022 onwards on a fortnightly basis (i.e., 15th day of the month and end of the month), within seven calendar days from the close of the reporting period to which it relates, through the designated web portal at https://bop.rbi.org.in, as per the attached R-return format (Annex I). The IBUs may also prepare themselves to report the past data on such transactions since April 1, 2022 on the same portal latest by December 31, 2022.

8. The IBUs shall also take note of the following with regard to reporting under the FETERS:

(a) The IBUs shall indicate economic activity (purpose for the transaction) for all foreign exchange transactions under FETERS, capturing the purpose codes as per the attached prescribed classification (Annex II). The IBUs shall indicate date of transaction, purpose code, currency, amount, country and other details for all foreign exchange transactions and submit data files on the FETERS.

(b) The IBUs are also required to submit a statement in form BAL giving details of their holdings of all foreign currencies for October 31, 2022 onwards through the same web-portal (https://bop.rbi.org.in) as per the format given in Annex III on a fortnightly basis (i.e., 15th day of the month and end of the month), within seven calendar days from the close of the reporting period to which it relates.

(c) The IBUs are advised to follow the attached guidelines (on file-layouts, delimiters, consistency checks, nomenclature, inter-relationship between files, glossary of external sector statistics etc.) for submission of data (Annex IV).

(d) Due to inherent difference in the scope and nature of permitted foreign exchange transactions of IBUs vis-à-vis the AD banks in India, the existing purpose codes for FETERS may not be able to capture all the relevant granular details under certain fields. Accordingly, for some specific purposes, the IBUs may be advised to provide additional information for the purpose of BOP statistics, outside of the FETERS reporting portal. In this regard, IBUs are being further directed to furnish the disaggregated information on transactions related to short-term loans and long-term loans extended and export bill discounting, under the prescribed format to the RBI under advice to IFSCA, along with the FETERS reporting beginning from November 1, 2022.

9. The IBUs shall follow the operational instructions by the RBI for such reporting and may ensure that the returns and statements reflect all the relevant foreign exchange transactions undertaken by them accurately and completely. Failure on the part of the IBUs to furnish the mandated information accurately and in a timely manner will be viewed seriously by the IFSCA.

10. Apart from the reporting formats, the enclosures to this circular also provide detailed guidelines and a glossary of key terms used in compilation of BOP statistics for facilitating the reporting by IBUs. The IFSCA, in collaboration with the Department of Statistics and Information Management (DSIM), RBI shall organize workshops / sessions for familiarization of the staff of all IBUs. The general and specific queries of the IBUs, with regard to reporting under the FETERS, shall be suitably addressed through FAQs and through such initial / periodic (need based) virtual / physical workshops.

11. The reporting by the IBUs on the FETERS to the RBI under these directions being issued by the IFSCA, shall be in addition to and separate from the regulatory reporting or supervisory returns to be filed in compliance with the directions contained in the IFSCA Banking Handbook and other circulars / directions / guidelines issued, under the IFSCA Banking Regulations.

12. The directions contained in this circular have been issued by the IFSCA in exercise of powers conferred on it by under section 35A of the Banking Regulation Act,1949 and section 13(1) of International Financial Services Centres Authority Act, 2019.

Yours faithfully,

Kamlesh Sharma

General Manager

kamlesh.sharma27@ifsca.gov.in

Annex I: R-return format

1. IBBANKCODE_BOP6.TXT relating to transactions involving sale and purchase of foreign exchange (excluding inter-office, inter-bank) during the reporting fortnight

| Field | Format | Remarks |

| IBU branch Code | Char (7) | BSR Part-1 Uniform Code |

| Fortnight-end Date | YYYYMMDD | |

| Transaction Date | YYYYMMDD | Valid date within fortnight |

| Serial No. | Num. (4) | |

| Purpose Code | Char (5) | Purpose code starting with P/S (Part A/B of Annex II) |

| Country Code | Char (2) | Country code (ISO 3166) (of non-resident.) |

| Currency Code | Char (3) | SWIFT code |

| Amount [in Foreign Currency (FC)] | Num. (15) | |

| Date of Shipment | YYYYMMDD | |

| LC | char (1) | 1 for Yes; 0 for No |

| Country of Vostro a/c Holder | <Blank> | |

| Country Code of ultimate exporter/importer* | Char (2) | Country code (ISO 3166) (of non-resident.) |

*For services purpose groups only.

2. TXT for Cover Page Totals

| Field | Format | Remarks |

| IBU Branch Code | Char (7) | |

| Fortnight-end date | YYYYMMDD | |

| Serial Number | Num. (4) | |

| Purpose Code | Char (5) | As per Part C of Annex II |

| Country of Vostro A/c holder | Char (2) | |

| Currency | Char (3) | |

| Amount in Currency | Num. (15) | |

| Return (Nostro) | Char (1) | N for Nostro |

Annex II: List of receipt and payment purpose codes

A. Payment Purposes (for use in BOP file)

| Gr. No. | Purpose Group Name | Purpose code |

Description |

| 00 | Capital Account | S0017 | Acquisition of non-produced non-financial assets (Purchase of intangible assets like patents, copyrights, trademarks etc., land acquired by government, use of natural resources) – |

| S0019 | Acquisition of non-produced non-financial assets (Purchase of intangible assets like patents, copyrights, trademarks etc., use of natural resources) – Non-Government | ||

| S0026 | Capital transfers (Guarantees payments, Investment Grand given by the government/international organisation, exceptionally large Non-life insurance claims) – Government | ||

| S0027 | Capital transfers (Guarantees payments, Investment Grand given by the Non-government, exceptionally large Non-life insurance claims) – Non-Government | ||

| S0099 | Other capital payments not included elsewhere | ||

| Financial Account | |||

| Foreign Direct Investments | S0003 | Indian Direct investment abroad (in branches & wholly owned subsidiaries) in equity Shares | |

| S0004 | Indian Direct investment abroad (in subsidiaries and associates) in debt instruments | ||

| S0005 | Indian investment abroad – in real estate | ||

| S0006 | Repatriation of Foreign Direct Investment made by overseas Investors in India – in equity shares | ||

| S0007 | Repatriation of Foreign Direct Investment in made by overseas Investors India – in debt instruments | ||

| S0008 | Repatriation of Foreign Direct Investment made by overseas Investors in India – in real estate | ||

| S0001 | Indian Portfolio investment abroad – in equity shares | ||

| Foreign Portfolio Investments |

S0002 | Indian Portfolio investment abroad – in debt instruments | |

| S0009 | Repatriation of Foreign Portfolio Investment made by overseas Investors in India – equity shares/units of AIF, MF (mutual funds) etc. | ||

| S0010 | Repatriation of Foreign Portfolio Investment made by overseas Investors in India – in debt instruments | ||

| Loans | S0011 | Loans (short or long-term) extended to Non-Residents/ export bill discounting for exports between two non-residents | |

| S0012 | Repayment of long & medium term loans with original maturity above one year received from Non-Residents | ||

| S0013 | Repayment of short term loans with original maturity up to one year received from Non-Residents | ||

| Banking Capital | S0014 | Repatriation of Non-Resident Deposits FD, savings account | |

| S0015 | Repayment of loans & overdrafts taken by IBUs on their own/ overnight lending, placement of deposit by IBUs. | ||

| S0016 | Sale of a foreign currency against another foreign currency | ||

| Financial Derivatives and Others | S0020 | Payments made on account of margin payments, premium payment and settlement amount etc. under Financial derivative | |

| S0021 | Payments made on account of sale of share under Employee | ||

| stock option | |||

| S0022 | Investment in Indian Depositories Receipts (IDRs) | ||

| S0023 | Opening of foreign currency account abroad with a bank | ||

| External Assistance | S0024 | External Assistance extended by India. e.g. Loans and advances extended by India to Foreign governments under | |

| S0025 | Repayments made on account of External Assistance received by India. | ||

| 1 | Merchandise imports between resident and non-resident |

S0101 | Advance payment against imports made to countries other than Nepal and Bhutan |

| S0102 | Payment towards imports- settlement of invoice other than Nepal and Bhutan | ||

| S0103 | Imports by diplomatic missions other than Nepal and Bhutan | ||

| S0104 | Intermediary trade/transit trade, i.e., third country export passing through India | ||

| S0108 | Goods acquired under merchanting / Payment against import leg of merchanting trade | ||

| S0109 | Payments made for Imports from Nepal and Bhutan, if any | ||

| 2

2 |

Transport

Transport |

S0201 | Payments for surplus freight/passenger fare by foreign shipping companies operating in India |

| S0202 | Payment for operating expenses of Indian shipping companies operating abroad | ||

| S0203 | Freight on imports – Shipping companies | ||

| S0204 | Freight on exports – Shipping companies | ||

| S0205 | Operational leasing/Rental of Vessels (with crew) –Shipping companies | ||

| S0206 | Booking of passages abroad – Shipping companies | ||

| S0207 | Payments for surplus freight/passenger fare by foreign Airlines companies operating in India

Operating expenses of Indian Airlines companies operating |

||

| S0208 | |||

| S0209 | Freight on imports – Airlines companies | ||

| S0210 | Freight on exports – Airlines companies | ||

| S0211 | Operational leasing / Rental of Vessels (with crew) – Airline companies | ||

| S0212 | Booking of passages abroad – Airlines companies | ||

| S0214 | Payments on account of stevedoring, demurrage, port handling charges etc.(Shipping companies) | ||

| S0215 | Payments on account of stevedoring, demurrage, port handling charges, etc.(Airlines companies) | ||

| S0216 | Payments for Passenger – Shipping companies | ||

| S0217 | Other payments by Shipping companies | ||

| S0218 | Payments for Passenger – Airlines companies | ||

| S0219 | Other Payments by Airlines companies | ||

| S0220 | Payments on account of freight under other modes of transport (Internal Waterways, Roadways, Railways, Pipeline transports and others) | ||

| S0221 | Payments on account of passenger fare under other modes of | ||

| transport (Internal Waterways, Roadways, Railways, Pipeline transports and others) | |||

| S0222 | Postal & Courier services by Air | ||

| S0223 | Postal & Courier services by Sea | ||

| S0224 | Postal & Courier services by others | ||

| 3 | Travel | S0301 | Business travel. |

| S0303 | Travel for pilgrimage | ||

| S0304 | Travel for medical treatment | ||

| S0305 | Travel for education (including fees, hostel expenses etc.) | ||

| S0306 | Other travel (including holiday trips and payments for settling international credit cards transactions) | ||

| 5 | Construction services | S0501 | Construction of projects abroad by Indian

companies including import of goods at project site abroad |

| S0502 | cost of construction etc. of projects executed by foreign companies in India. | ||

| 06

06 |

Insurance and Pension Services

Insurance and Pension Services |

S0601 | Life Insurance premium except term insurance |

| S0602 | Freight insurance – relating to import & export of goods | ||

| S0603 | Other general insurance premium including reinsurance premium; and term life insurance premium | ||

| S0605 | Auxiliary services including commission on insurance | ||

| S0607 | Insurance claim Settlement of non-life insurance; and life insurance (only term insurance) | ||

| S0608 | Life Insurance Claim Settlements | ||

| S0609 | Standardised guarantee services | ||

| S0610 | Premium for pension funds | ||

| S0611 | Periodic pension entitlements e.g. monthly quarterly or yearly payments of pension amounts by Indian Pension Fund | ||

| S0612 | Invoking of standardised guarantees | ||

| 07 | Financial Services |

S0701 | Financial intermediation, except investment banking – Bank charges, collection charges, LC charges etc. |

| S0702 | Investment banking – brokerage, under writing commission | ||

| S0703 | Auxiliary services – charges on operation & regulatory fees, custodial services, depository services etc. | ||

| 08 | Telecom, Computer & Information Services | S0801 | Hardware consultancy/implementation |

| S0802 | Software consultancy / implementation | ||

| S0803 | Data base, data processing charges | ||

| S0804 | Repair and maintenance of computer and software | ||

| S0805 | News agency services | ||

| S0806 | Other information services- Subscription to newspapers, | ||

| S0807 | Off-site software imports | ||

| S0808 | Telecommunication services including electronic mail services and voice mail services | ||

| S0809 | Satellite services including space shuttle and rockets etc. | ||

| 09 | Charges for the use of intellectual property n.i.e | S0901 | Franchises services |

| S0902 | Payment for use, through licensing arrangements, of produced originals or prototypes (such as manuscripts and films), patents, copyrights, trademarks and industrial processes etc. | ||

| 10 | Other Business Services | S1002 | Trade related services – commission on exports / imports |

| 10 | Other Business Services | S1003 | Operational leasing services (other than financial leasing) without operating crew, including charter hire- Airlines companies |

| S1004 | Legal services | ||

| S1005 | Accounting, auditing, book-keeping services | ||

| S1006 | Business and management consultancy and public relations | ||

| S1007 | Advertising, trade fair service | ||

| S1008 | Research & Development services | ||

| S1009 | Architectural services | ||

| S1010 | Agricultural services like protection against insects & disease, increasing of harvest yields, forestry services. | ||

| S1011 | Payments for maintenance of offices abroad | ||

| S1013 | Environmental Services | ||

| S1014 | Engineering Services | ||

| S1015 | Tax consulting services | ||

| S1016 | Market research and public opinion polling service | ||

| S1017 | Publishing and printing services | ||

| S1018 | Mining services like on–site processing services analysis of | ||

| S1020 | Commission agent services | ||

| S1021 | Wholesale and retailing trade services. | ||

| S1022 | Operational leasing services (other than financial leasing) without operating crew, including charter hire- Shipping | ||

| S1023 | Other Technical Services including scientific/space services. |

||

| S1099 | Other services not included elsewhere | ||

| 11 | Personal, Cultural & Recreational services |

S1101 | Audio-visual and related services like Motion picture and video tape production, distribution and projection services. |

| S1103 | Radio and television production, distribution and transmission services | ||

| S1104 | Entertainment services | ||

| S1105 | Museums, library and archival services | ||

| S1106 | Recreation and sporting activities services | ||

| S1107 | Education (e.g. fees for correspondence courses abroad) | ||

| S1108 | Health Service (payment towards services received from hospitals, doctors, nurses, paramedical and similar services etc. rendered remotely or on-site) | ||

| S1109 | Other Personal, Cultural & Recreational services | ||

| 12 | Govt. not included elsewhere (G.n.i.e.) | S1201 | Maintenance of Indian embassies abroad |

| S1202 | Remittances by foreign embassies in India | ||

| 13 | Secondary Income | S1301 | Remittance for family maintenance and savings |

| S1302 | Remittance towards personal gifts and donations | ||

| S1303 | Remittance towards donations to religious and charitable institutions abroad | ||

| S1304 | Remittance towards grants and donations to other governments and charitable institutions established by the | ||

| S1305 | Contributions/donations by the Government to international institutions | ||

| S1306 | Remittance towards payment / refund of taxes. | ||

| S1307 | Outflows on account of migrant transfers including personal | ||

| 14

14 |

Primary Income

Primary Income |

S1401 | Compensation of employees |

| S1402 | Remittance towards interest on Non-Resident deposits (FD, Savings Deposits) | ||

| S1403 | Remittance towards interest on loans from Non-Residents (ST/MT/LT loans), Trade Credits, etc. | ||

| S1405 | Remittance towards interest payment by IBUs on their own account or the OD on NOSTRO a/c.) | ||

| S1408 | Remittance of profit by FDI enterprises in India (by branches of foreign companies including bank branches) | ||

| S1409 | Remittance of dividends by FDI enterprises in India (other than branches) on equity and investment fund shares | ||

| S1410 | Payment of interest by FDI enterprises in India to their Parent company abroad. | ||

| S1411 | Remittance of interest income on account of Portfolio Investment in India | ||

| S1412 | Remittance of dividends on account of Portfolio Investment in India on equity and investment fund shares | ||

| 15 | Others | S1501 | Refunds / rebates / reduction in invoice value on account of exports |

| S1502 | Reversal of wrong entries, refunds of amount remitted for non-exports | ||

| S1503 | Payments by residents for international bidding | ||

| S1504 | Notional sales when export bills negotiated/ purchased/ discounted are dishonored/ crystallised/ cancelled and reversed from suspense account | ||

| S1505 | Deemed Imports (exports between SEZ, EPZs and Domestic tariff areas) | ||

| 16 | Maintenance

and repair services n.i.e |

S1601 | Payments on account of maintenance and repair services

rendered for Vessels, ships, boats, warships, etc. |

| S1602 | Payments on account of maintenance and repair services rendered for aircrafts, space shuttles, rockets, military aircrafts, | ||

| 17 | Manufacturing services (goods for processing) | S1701 | Payments for processing of goods |

B. Receipt Purposes (for use in BOP file)

|

Gr. No |

Purpose Group Name |

Purpose Code | Description |

| 00 | Capital Account | P0017 | Receipts on account of Sale of non-produced non-financial assets (Sale of intangible assets like patents, copyrights, trademarks etc., land acquired by government, use of natural resources) – Government |

| P0019 | Receipts on account of Sale of non-produced non-financial assets (Sale of intangible assets like patents, copyrights, trademarks etc., use of natural resources)–Non-Government | ||

| P0028 | Capital transfer receipts (Guarantee payments, Investment Grant given by the government/international organisation, exceptionally large Non-life insurance claims including claims arising out of natural calamity) – Government | ||

| P0029 | Capital transfer receipts (Guarantee payments, Investment Grant given by the Non-government, exceptionally large Non-life insurance claims including claims arising out of natural calamity) – Non-Government | ||

| P0099 | Other capital receipts not included elsewhere | ||

| Financial Account | |||

| Foreign Direct Investment | P0003 | Repatriation of Indian Direct investment abroad (by branches & wholly owned subsidiaries and associates) in equity shares | |

| P0004 | Repatriation Indian Direct investment abroad (by branches &

wholly owned subsidiaries and associates) in debt instruments |

||

| P0005 | Repatriation of Indian investment abroad in real estate | ||

| P0006 | Foreign Direct Investment made by overseas Investors in India in equity shares | ||

| P0007 | Foreign Direct Investment made by overseas Investors in India in debt instruments. | ||

| P0008 | Foreign Direct Investment made by overseas Investors in India in real estate | ||

| Foreign Portfolio Investment | P0001 | Repatriation of Indian Portfolio investment abroad in equity capital (shares) | |

| P0002 | Repatriation of Indian Portfolio investment abroad in debt instruments. |

||

| P0009 | Foreign Portfolio Investment made by overseas Investors in India in equity shares/units of AIF, MF (mutual funds) etc. |

||

| P0010 | Foreign Portfolio Investment made by overseas Investors in India in debt Instruments. | ||

| Loans | P0011 | Repayment of loans (short & long term) extended to Non-Residents/ Realization of discounted export bills for exports between two non-residents | |

| P0012 | Long & medium term loans, with original maturity of above one year, from Non-Residents to India | ||

| P0013 | Short term loans with original maturity upto one year from Non- Residents to India (Short-term Trade Credit) | ||

| Banking Capital | P0014 | Receipts o/a Non-Resident deposits (FDs, savings account) | |

| P0015 | Loans & overdrafts taken by IBUs on their own account. (Any amount of loan credited to the NOSTRO account which may not be swapped into Rupees should also be reported) overnight borrowing, placement of deposit with IBUs. | ||

| P0016 | Purchase of a foreign currency against another currency. | ||

| P0020 | Receipts on account of margin payments, premium payment and settlement amount etc. under Financial derivative transactions |

||

| Financial

Derivatives and |

P0021 | Receipts on account of sale of share under Employee stock option | |

| P0022 | Receipts on account of other investment in ADRs/GDRs | ||

| External Assistance |

P0024 | External Assistance received by India e.g. Multilateral and bilateral loans received by Govt. of India under agreements with other govt. / international institutions. | |

| P0025 | Repayments received on account of External Assistance extended by India |

||

| 01 | Merchandise exports between resident and non- resident |

P0101 | Value of export bills negotiated / purchased/discounted etc. (covered under GR/PP/SOFTEX/EC copy of shipping bills etc.) – Other than Nepal and Bhutan |

| P0102 | Realisation of export bills (in respect of goods) sent on collection (full invoice value) – Other than Nepal and Bhutan | ||

| P0103 P0103 |

Advance receipts against export contracts, which will be covered later by GR/PP/SOFTEX/SDF – other than Nepal and Bhutan | ||

| P0104 | Receipts against export of goods not covered by the GR /PP /SOFTEX /EC copy of shipping bill etc. (under Intermediary/transit trade, i.e., third country export passing through India | ||

| P0105 | Export bills (in respect of goods) sent on collection – other than Nepal and Bhutan | ||

| P0107 | Realisation of NPD export bills (full value of bill to be reported) – other than Nepal and Bhutan | ||

| P0108 | Goods sold under merchanting / Receipt against export leg of merchanting trade* | ||

| P0201 | Receipts of surplus freight/passenger fare by Indian shipping companies operating abroad | ||

| 02

02 |

Transport

Transport |

P0202 | Receipts on account of operating expenses of Foreign shipping companies operating in India |

| P0205 | Receipts on account of operational leasing (with crew) – Shipping companies | ||

| P0207 | Receipts of surplus freight/passenger fare by Indian Airlines companies operating abroad. | ||

| P0208 | Receipt on account of operating expenses of Foreign Airlines companies operating in India |

||

| P0211 | Receipt on account of operational leasing (with crew) – Airlines Companies | ||

| P0214 | Receipts on account of other transportation services (stevedoring, demurrage, port handling charges etc).(Shipping Companies) | ||

| P0214 P0215 |

Receipts on account of other transportation services (stevedoring, demurrage, port handling charges etc).(Shipping Companies)

Receipts on account of other transportation services (stevedoring, demurrage, port handling charges etc).( Airlines companies) |

||

| P0216 | Receipts of freight fare -Shipping companies operating abroad | ||

| P0217 | Receipts of passenger fare by Indian Shipping companies operating abroad |

||

| P0218 | Other receipts by Shipping companies | ||

| P0219 | Receipts of freight fare by Indian Airlines companies operating abroad | ||

| P0220 | Receipts of passenger fare –Airlines | ||

| P0221 | Other receipts by Airlines companies | ||

| P0222 | Receipts on account of freights under other modes of transport (Internal Waterways, Roadways, Railways, Pipeline transports and Others) | ||

| P0223 | Receipts on account of passenger fare under other modes of transport (Internal Waterways, Roadways, Railways, Pipeline transports and Others) | ||

| P0224 | Postal & Courier services by Air | ||

| P0225 | Postal & Courier services by Sea | ||

| P0226 | Postal & Courier services by others | ||

| 03 | Travel

Travel |

P0301 | Purchases towards travel (Includes purchases of foreign TCs, currency notes etc over the counter, by hotels, Emporiums, institutions etc. as well as amount received by TT/SWIFT transfers or debit to Non-Resident account). |

| P0302 | Business travel | ||

| 03 | P0304 | Travel for medical treatment including TCs purchased by hospitals | |

| P0305 | Travel for education including TCs purchased by educational institutions | ||

| P0306 | Other travel receipts | ||

| P0308 | Foreign Currencies/TCs surrendered by returning Indian tourists. | ||

| 05 | Construction Services | P0501 | Receipts on account of services relating to cost of construction of projects in India |

| P0502 | Receipts on account of construction works carried out abroad by Indian Companies | ||

| 06 | Insurance and Pension Services |

P0601 | Life Insurance premium except term insurance |

| P0602 | Freight insurance – relating to import & export of goods | ||

| P0603 | Other general insurance premium including reinsurance premium; and term life insurance premium | ||

| P0605 | Auxiliary services including commission on insurance |

||

| P0607 | Insurance claim Settlement of non-life insurance; and life insurance (only term insurance) | ||

| P0608 | Life insurance claim settlements (excluding term insurance) received by residents in India | ||

| P0609 | Standardised guarantee services | ||

| P0610 | Premium for pension funds | ||

| P0611 | Periodic pension entitlements e.g. monthly quarterly or yearly payments of pension amounts by Indian Pension Fund Companies. | ||

| P0612 | Invoking of standardised guarantees | ||

| 07

07 |

Financial Services

Financial Services |

P0701 | Financial intermediation except investment banking – Bank charges, collection charges, LC charges, etc. |

| P0702 | Investment banking – brokerage, under writing commission etc. | ||

| P0703 | Auxiliary services – charges on operation & regulatory fees, custodial services, depository services etc. | ||

| 08 | Telecom,

Computer & Information Services |

P0801 | Hardware

consultancy/implementation |

| P0802 | Software consultancy/implementation (other than those covered in SOFTEX form) | ||

| P0803 | Data base, data processing charges | ||

| P0804 | Repair and maintenance of computer and software | ||

| P0805 | News agency services | ||

| P0806 | Other information services- Subscription to newspapers, periodicals, etc. |

||

| P0807 | Off-site Software Exports | ||

| P0808 | Telecommunication services including electronic mail services and voice mail services | ||

| P0809 | Satellite services including space shuttle and rockets, etc. | ||

| 09 | Charges for the use of intellectual property n.i.e |

P0901 | Franchises services |

| P0902 | Receipts for use, through licensing arrangements, of produced originals or prototypes (such as manuscripts and films), patents, copyrights, trademarks, industrial processes, franchises etc. | ||

| 10 | Other Business ServicesOther Business Services |

P1002 | Trade related services – commission on exports / imports |

| P1003 | Operational leasing services (other than financial leasing)without operating crew, including charter hire-Airlines companies | ||

| P1004 | Legal services | ||

| P1005 | Accounting, auditing, book keeping services | ||

| P1006 | Business and management consultancy and public relations services | ||

| P1007 | Advertising, trade fair service | ||

| P1008 | Research & Development services | ||

| P1009 | Architectural services | ||

| P1010 | Agricultural services like protection against insects & disease, increasing of harvest yields, forestry services. | ||

| P1011 | Inward remittance for maintenance of offices in India | ||

| P1013 Environmental Services | |||

| P1014 | Engineering Services | ||

| P1015 | Tax consulting services | ||

| P1016 | Market research and public opinion polling service | ||

| P1017 | Publishing and printing services | ||

| P1018 | Mining services like on–site

processing services analysis of ores etc. |

||

| P1019 | Commission agent services | ||

| P1020 | Wholesale and retailing trade services. | ||

| P1021 | Operational leasing services (other than financial leasing) without operating crew, including charter hire-Shipping companies | ||

| P1022 | Other Technical Services including scientific/space services. | ||

| P1099 | Other services not included elsewhere | ||

| 11

12 |

Personal, Cultural & Recreational services |

P1101 | Audio-visual and related services like

Motion picture and video tape production, distribution and projection services. |

| P1103 | Radio and television production, distribution and transmission services | ||

| P1104 | Entertainment services | ||

| P1105 | Museums, library and archival services |

||

| P1106 | Recreation and sporting activity services | ||

| P1107 | Educational services (e.g. fees received for correspondence courses offered to non-resident by Indian institutions) | ||

| P1108 | Health Service (Receipts on account of services provided by Indian hospitals, doctors, nurses, paramedical and similar services etc. rendered remotely or onsite) | ||

| Govt not included | P1201 | Maintenance of foreign embassies in India | |

| elsewhere(G..n.i.e) | P1203 | Maintenance of international institutions such as offices of IMF mission, World Bank, UNICEF etc. in India. | |

| 13 | Secondary Income | P1301 | Inward remittance from Indian nonresidents towards family maintenance and savings |

| P1302 | Personal gifts and donations | ||

| P1303 | Donations to religious and charitable institutions in India | ||

| P1304 | Grants and donations to governments and charitable institutions established by the governments | ||

| P1306 | Receipts / Refund of taxes | ||

| P1307 | Receipts on account of migrant transfers including Personal Effects | ||

| 14 | Primary Income | P1401 | Compensation of employees |

| P1403 | Inward remittance towards interest on loans extended to non- residents (ST/MT/LT loans) | ||

| P1405 | Inward remittance towards interest receipts of IBUs on their own account (on investments.) | ||

| P1408 | Inward remittance of profit by branches of Indian FDI Enterprises (including bank branches) operating abroad. | ||

| P1409 | Inward remittance of dividends (on equity and investment fund shares) by Indian FDI Enterprises, other than branches, operating

Abroad |

||

| P1410 | Inward remittance on account of interest payment by Indian FDI enterprises operating abroad to their Parent company in India. | ||

| P1411 | Inward remittance of interest income on account of Portfolio Investment made abroad by India | ||

| P1412 | Inward remittance of dividends on account of Portfolio Investment made abroad by India on equity and investment fund shares | ||

| P1499 | Other income receipts | ||

| 15 | Others | P1501 | Refunds/rebate on account of imports |

| P1502 | Reversal of wrong entries, refunds of amount remitted for non- imports | ||

| P1503 | Remittances (receipts) by residents under international bidding process. | ||

| P1505 | Deemed Exports (exports between SEZ, EPZs and Domestic Tariff Areas) | ||

| 16 | Maintenance and repair services n.i.e |

P1601 | Receipts on account of maintenance and repair services rendered for Vessels, Ships, Boats, Warships, etc. |

| P1602 | Receipts of maintenance and repair services rendered for aircrafts, Space shuttles, Rockets, military aircrafts, etc. | ||

| 17 | Manufacturing services |

P1701 | Receipts on account of processing of goods |

C. Cover Page Purpose Codes (for use in QE file)

| P0092 | Purchase from other IBUs in India (Currency-wise Totals) | |

| P0093 | Purchase from Overseas banks & correspondents (Currency-wise Totals) | |

| P0095 | Aggregate Purchases at Branches (Currency-wise Totals) | |

| P0100 | Good export receipts (Currency-wise Totals) | |

| P0144 | Intermediary export receipts (Currency-wise Totals) | |

| P1590 | Non- exports receipts (Currency-wise Totals) | |

| S0092 | Sales to other IBUs in India (Currency-wise Totals) | |

| S0093 | Sales to Overseas banks & correspondents (Currency-wise Totals) | |

| S0095 | Aggregate Sales at Branches (Currency-wise Totals) | |

| S0190 | Good import payment (Currency-wise Totals) | |

| S0144 | Intermediary import payment (Currency-wise Totals) | |

| S1590 | Non-Imports payment (Currency-wise Totals) | |

| Cover Page Balance |

P2088 | Opening Balance (Credit Balance in Nostro |

| P2199 | Closing Balance (Credit Balance in Nostro | |

| S2088 | Opening Balance (Debit Balance in Nostro | |

| S2199 | Closing Balance (Debit Balance in Nostro |

Annex III: BAL file format

| Banking Asset Liability (BAL) Statement | |||||||||

| Foreign currency held abroad by IBUs and balances held in Non-Resident Rupee/ACU Dollar accounts of overseas branches and correspondents as at the end of___________ | |||||||||

| Bank Code |

Bank Name | ||||||||

| Report Date | Org/Rev | ||||||||

| Foreign Currency Balances held abroad | |||||||||

| Country | Currency | Current Account* |

Fixed Deposits |

Treasury Bills |

Securities | Loans | Total | ||

| Ct (1) | Dt

(2) |

3 | 4 | 5 | 6 | (1-6) | |||

Annex IV: Guidelines for Submission of Data:

Foreign Exchange Transactions Electronic Reporting System (FETERS)

IFSC Banking Units (IBUs) are now required to report the purpose, country, currency, amount, and Country of their foreign exchange sale and purchase transactions in the Foreign Exchange Transaction Electronic Reporting System (FETERS) to the Reserve Bank on a fortnightly basis in the prescribed format.

In order to meet the requirement of a compilation of BoP Statistics as per the guidelines under the Balance of Payments and International Investment Position Manual (6th edition) (BPM6) of the IMF, the scope of the collection of data on foreign exchange transactions is derived from the recommendations of the Working Group on Balance of Payments Manual for India (Chairman: Shri Deepak Mohanty) (For details, see report at web-link: http://rbidocs.rbi.org.in/rdocs/PublicationReport/Pdfs/IBPM221110R.pd f)

The purpose codes are given in Annex II and the structures of two ASCII files to be submitted under FETERS are given in Annex I.

1. Reporting under FETERS: IBUs may submit data files on a fortnightly basis (i.e. 15th and end of the month) by web-portal based data submission. The file-layout, delimiter, consistency checks, and interrelationship among BOP6.TXT and QE.TXT files as well as their naming convention is as detailed below:

Naming Convention: The file name should start with word “IB” and “BANKCODE_” for each FETERS file to be submitted to the Reserve Bank. For example, if bank code is 639, the file name should be:

- TXT for BoP6 file

- txt for QE file

Delimiter: The FETERS files should be ASCII files with one record per line. All fields in each file should be delimited with the delimiter “|”

Reporting of Non-applicable items: In cases where an item is not relevant for a set of transactions of certain purposes, irrelevant fields/ data items may be kept blank in the text file. The structure of this file has been designed in such a way that, many blank fields do not appear in between two relevant fields.

Consistency Checks: In order to ensure accurate reporting of data, FETERS contains consistency checks. These checks need to be ensured for the entire

| Name | Coverage (Transactions to be reported) in File BOP6.TXT | Coverage in File QE.TXT* |

| Exports (P0101, P0102, P0103 & P0109) | All the individual transactions (i.e. N/P/D, advance received during fortnight, Collection realised during fortnight) | Purpose code P0100 ~ Aggregate figure |

| Intermediary exports (P0104 & P0108) |

All the individual transactions | Purpose code P0144 ~ Aggregate figure |

| Exports (Other than Goods) | All the individual transactions related to Exports (Other than Good Exports) | Purpose code P1590 ~

Aggregate figure |

| Purchases from other IBUs | No individual Transaction to be Reported in BOP file | Purpose code P0092 ~ Aggregate figure |

| Purchases from Overseas Banks/ correspondents |

No individual Transaction to be Reported in BOP file | Purpose code P0093 ~

Aggregate figure |

| Purchases from IBU’s own branches in IFSC, India |

No individual Transaction to be Reported in BOP file | Purpose code P0095 ~

Aggregate figure |

fortnight and relevant with currency-wise x item- wise cover-page totals. Checks are also introduced for checking the closing balances using the following relationship before submitting data to the Reserve Bank:

Closing Balances = Opening Balances + Total Purchases – Total Sales

Inter-relationship among FETERS files: The following inter-relationship among files BOP6.TXT, QE.TXT should be ensured.

| Import of goods (S0101, S0102, S0103 & S0109) | All the individual transactions | Purpose code S0190 ~ Aggregate figure |

| Intermediary imports (S0104 & S0108) | All the individual transactions | Purpose code S0144 ~ Aggregate figure |

| Non- Imports (Other than Goods) | All the individual transactions related to Imports (Other than Good Imports) | Purpose code S1590 ~ Aggregate figure |

| Sales to other IBUs | No individual Transaction to be Reported in BOP file | Purpose code S0092 ~ Aggregate figure |

| Sales to Overseas Banks/Correspondents | No individual Transaction to be Reported in BOP file | Purpose code S0093 ~ Aggregate figure |

| Sales from IBU’s own branches in IFSC, India | No individual Transaction to be Reported in BOP file | Purpose code S0095 ~ Aggregate figure |

| Opening Balance | With purpose code P2088/ S2088 | |

| Closing Balance | With purpose code P2199/ |

*In case of Nostro, Currency wise fortnightly aggregate;

Helpdesk: To ensure accuracy of the format of the ASCII file generated by their

interface, if necessary, IBUs may contact us for guidance at the following address:

The Director,

Balance of Payments Statistics Division,

Department of Statistics and

Information Management, (DSIM)

Reserve Bank of India,

C-/9, Bandra-Kurla Complex,

Mumbai, India,

PIN – 400051

Helpdesk Contacts:

e-mail : feters@rbi.org.in

Tel No. : (022) 26578712 /26578416 / 26578229

2. Nodal offices of banks have to access the web-portal https://bop.rbi.org.in with the RBI-provided login-name and password, to submit data (as per the contact details provided above).

3. IBUs may download RBI-provided validator template/manuals from this portal on their computer and perform an offline check of their FETERS data file for the error, if any, before its submission on the portal. Both Java-based and Excel-based validators are provided: Use of Java-based validators is advised for larger files. This portal also gives relevant master files (g., country, currency, purpose code masters).

4. On uploading validated files, IBUs will get acknowledgment. They can view the data-files submitted by them during the previous two fortnights, with download facility. They can also revise the purpose codes for transaction submitted earlier, if required, which will be authenticated by the RBI in the system.

5. IBUs need to report addition of IBU branch code for their bank, which will be incorporated in the IBU-master database by the RBI after due authentication.

Reporting guidelines for IBUs

1. IBUs need to report all forex transactions under R return except the following:

- transfer between two non-resident’s current accounts under same IBU

- transfer between two resident’s current accounts under same IBU

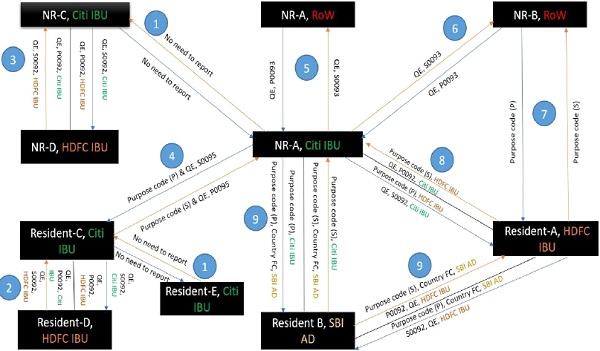

2. Transfer of funds between two residents in different IBUs: Transaction between two residents who have accounts in separate IBUs should be reported in QE file under S0092/ P0092. IBU who is issuing the transaction should report the transaction under S0092 and the acquiring IBU should report the transaction under P0092.

3. Transfer of funds between two non-residents in different IBUs: Transaction between two non-residents who have accounts in separate IBUs should be reported in QE file under S0092/ P0092. IBU who is issuing the transaction should report the transaction under S0092 and the acquiring IBU should report the transaction under P0092.

4. Transfer of funds between resident and non-resident under same IBU: Transaction between resident and non-resident under same IBU should be reported under BOP file under appropriate purpose code. If resident is the recipient, then IBU should report the transaction under P (inflow) and if nonresident is the recipient, then IBU should report the transaction under S (outflow) in BOP file.

The IBU needs to create one dummy entry under purpose code P0095/ S0095 in QE file to knock-off the BOP transaction (as no money has gone out of the IBU or came in). e.g., If an IBU reports such resident-non-resident transaction under purpose code P0006 then they need to add S0095 entry in QE file with same amount. Similarly, If an IBU reports such resident-nonresident transaction under purpose code S0006 then they need to add P0095 entry in QE file with same amount.

5. Funding in or repatriation from non-resident’s current account: Own current account funding by non-resident in IBU should be reported in QE file under P0093 and repatriation from own current account by non-resident should be reported under S0093 in QE file.

6. Transfer of funds between non-resident’s account in IBU and non-resident’s account in overseas: Transfer of funds from non-resident’s account in overseas bank to another non-resident’s account in IBU should be reported under QE file under P0093 and transfer of funds from non-resident’s account in IBU to another non-resident’s account in overseas bank should be reported under QE file under S0093.

7. Transfer of funds between resident’s account in IBU and non-resident’s account in overseas: Credit from overseas bank to resident’s account in IBU should be reported under P purpose code in BOP file and debit from resident’s account in IBU to credit non-resident’s account in overseas bank should be reported in BOP file under S purpose code.

8. Transaction between a resident and a non-resident in two separate IBUs: If resident has his account in IBU-A and non resident has his account in IBU-B, then IBU-A should report the transactions between the resident and non-resident in BOP file under proper purpose code. IBU-B needs to report the transaction in QE file under P0092/S0092. E.g., If resident (account holder in IBU-A) remits USD 5,000 to non-resident in IBU-B for business management and consultancy service, then IBU-A should report the transaction under S1006 in BOP file and IBU-B should report the transaction in QE file under P0092. On the other hand, if non-resident from IBU-B remits USD 5,000 to resident in IBU-A for business management and consultancy service, then IBU-A should report the transaction under P1006 in BOP file and IBU-B should report the transaction in QE file under S0092. In other word, the IBU which holds the resident’s account should report the transaction in BOP file. Credit to resident’s account from non-resident’s account (in other IBU) should be reported under P (inflow) and debit from resident’s account to non-resident’s account in other IBU should be reported under S (outflow).

9. Transaction between IBUs and AD banks:

Reporting guidelines for IBU: Transaction between non-resident in IBU and resident in DTA should be reported in BOP file. Transaction initiated by non-resident having account in IBU to resident in DTA having account in AD should be reported under P purpose code by IBU and transaction initiated by resident in DTA having account in AD to non-resident having account in IBU should be reported S purpose code. Transaction between two residents (one has account in IBU and the other has account in AD bank) should be reported under QE file under S0092 (IBU sending money to AD bank) and P0092 (for IBU receiving money from AD bank).

Reporting guidelines for AD banks: AD banks should report all transactions with IBUs in BOP file under appropriate purpose codes using country code FC. All outward payment by AD bank to IBU should be reported under S purpose code and inward receipts to AD bank should be reported under P purpose code.

Glossary of Key Terms used in BOP Statistics

1. Economic Territory: In the context of macroeconomic statistics, the concept of economic territory is defined as the area under the effective economic control of a single government.

2. Institutional units: An institutional unit is an economic entity that:

- is capable of owning assets and incurring liabilities

- engages in economic activities and transactions with other entities

- can exchange ownership of goods or assets

- is responsible for its actions at law

- can provide a complete set of financial statement information

- can enter into contracts.

There are two main types of institutional units:

- households (of persons or groups of persons)

- legal and social entities, which includes corporations (including quasi-corporations), government units, and nonprofit institutions

3. Institutional Sectors: In international accounts, there are four main institutional sectors: (i) central bank, (ii) deposit-taking corporations, except the central bank (iii) general government, and (iv) other sectors, which covers everything else.

4. Residence: The residence of an institutional unit is the economic territory with which it has the strongest connection, expressed as the center of its predominant economic interest. An institutional unit is resident in an economic territory where the unit engages and intends to continue engaging, either indefinitely or over a finite but long period of time, in economic activities and transactions on a significant scale. Actual or intended location for one year or more is used as an operational definition.

An institutional unit is resident in one, and only one economic territory, where it produces, consumes, or otherwise enters into economic transactions for a period of time that makes that location its center of predominant economic interest. This is the feature that underlies the whole of the macroeconomic statistical framework.

Similarly, no individual can be resident in more than one economy. This means that if a member of a family goes abroad to work, and becomes a resident of that economy, that family member cannot be considered a member of the household institutional unit in country of origin.

5. What Are Flows and Positions?

Flows reflect the creation, transformation, exchange, transfer, or extinction of economic value. This means that they involve changes in the volume, composition, or value of an institutional unit’s assets and liabilities. Flows refer to economic actions and effects of events within an accounting period.

Positions refer to the level of financial assets or liabilities at one point in time.

6. What Are Transactions?

A transaction is an interaction between two institutional units that occurs by mutual agreement or through the operation of the law and involves an exchange or transfer of economic value. For example, the export of services from Country A to Country B is considered a transaction.

7. The international accounts use three broad categories of financial instruments:

equity and investment fund shares, debt instruments, and other financial assets and liabilities.

8. What Are Goods?

Goods are physical, produced items over which ownership rights can be established and whose economic ownership can be passed from one institutional unit to another by engaging in transactions.

9. What Is General Merchandise?

General merchandise on a balance of payments basis covers goods whose economic ownership is changed between a resident and a nonresident and that are not included elsewhere.

10. What are Re-exports?

Re-exports are foreign goods (goods produced in other economies and previously imported) that are exported with no substantial transformation from the state in which they were previously imported.

11. What are Re-imports?

Re-imports are domestic goods imported in the state as previously exported, without any substantial transformation occurring on the goods while they were outside the territory.

12. What Is Merchanting?

Merchanting is defined as the purchase of goods by a merchant in the compiling economy (Country A) from a nonresident (Country B) combined with the subsequent resale of the same goods to another nonresident (Country C) without the goods entering the compiling economy.

13. What Are Services?

Services are the result of production activity that changes the conditions of the consuming units, or facilitates the exchange of products or financial assets. Services are not generally separate items over which ownership rights can be established and cannot generally be separated from their production.

Note that both goods and services are the result of production, which is an activity where an enterprise transforms inputs (intermediate inputs, labor, produced and nonproduced assets) to an output that can be supplied to other units.

The classification of goods and services is not clear-cut. There are three categories of services in the balance of payments whose value includes the value of some goods — travel, construction, and government goods and services n.i.e. They are transactor-based services. All other categories of services are product-based. Some products may be treated either as a good or a service, depending on the nature of the product and the mode of delivery (e.g. customized and non-customized software).

14. What Is Transport?

Transport is the process of carriage of people and objects from one location to another as well as related supporting and auxiliary services. Also included are postal and courier services.

15. What Are Travel Credits?

Travel credits cover goods and services for own use or to give away acquired from an economy by nonresidents during visits to that economy.

16. What Are Travel Debits? Travel debits cover goods and services for own use or to give away acquired from other economies by residents during visits to these other economies.

17. What Is Construction?

Construction covers the creation, renovation, repair or extension of fixed assets in the form of buildings, land improvements of an engineering nature, and other engineering constructions such as roads, bridges, dams, and so forth. It also includes related installation and assembly work. Construction is one of the three transactor-based categories of services identified in balance of payments.

18. Insurance and Pension services includes services providing life insurance and annuities, nonlife insurance, reinsurance, freight insurance, pensions, standardized guarantees, and auxiliary services.

There are two main types of insurance: nonlife and life. Both have direct insurance and reinsurance and both pool risk, especially nonlife insurance. Through pooling, a considerable part of premiums received is paid out as claims and the risk is mitigated by facilitating the transfer of funds from all policyholders (their premiums) to a few policyholders who make claims and receive settlements.

19. Financial services cover financial intermediary and auxiliary services, except insurance and pension fund services. Financial services include services usually provided by deposit-taking corporations and other financial corporations. Financial services include deposit taking and lending, credit card services, commissions and charges related to financial leasing, factoring, underwriting, and a variety of services related to financial market activity.

20. Telecommunications, computer, and information services are based on the nature of the service, not the method of delivery.

21. Charges for the Use of Intellectual Property, n.i.e. This item covers two principal elements:

- charges for the use of proprietary rights (such as patents, trademarks, industrial processes or design, franchises); and

- charges for licenses to reproduce and/or distribute produced originals (such as copyrights of books, computer software, movies, and audio recordings, live performances, television, cable, or satellite broadcasts).

22. As the name implies, other business services cover all those business services that have not otherwise been classified, including research and development; professional and management consulting services; and technical, trade-related, and other business services.

23. Personal, cultural, and recreational services include Gambling and lotteries, Audiovisual and other related services, education and health services.

24. Government goods and services, not included elsewhere covers:

- goods and services supplied by and to an economy’s enclaves such as embassies, consulates, military bases, and by international organizations;

- goods and services acquired from the host economy by diplomats, consular staff (except locally engaged staff), military personnel, and their dependents;

- services supplied by and to governments that are not included in other categories of services.

25. Maintenance and repair services, n.i.e. covers, as the name implies, maintenance and repairs on goods owned by nonresidents and vice-versa. The repairs may be performed at the site of the repairer or elsewhere. Repairs and maintenance on ships, aircraft, and other transport equipment are included in this item. It is “not included elsewhere” because some maintenance and repairs are excluded, such as cleaning of transport equipment (included in transport services), construction maintenance and repairs (included in construction), and maintenance and repairs of computers (included in computer services).

The nature of the work done can be either regular maintenance – to keep the capital equipment in good running order – or it can be of a capital nature that would extend the life of the equipment, or improve its productive capacity.

26. Manufacturing services covers the fee payable by the owner of the product, resident in one economy, to the processor, resident in another economy. Example: Oil refining, liquefaction of natural gas, assembly of clothing or electronics, labelling, packing, and other processes related to converting raw materials (such as ore) into a finished or semi-finished manufacturing product.

27. The primary income account records:

- compensation for labor inputs to production;

- returns for the use of financial assets (such as dividends and interest); and

- returns for the use of nonproduced, nonfinancial resources (such as rent).

It also includes certain taxes and subsidies that are included in the price of commodities and production.

28. What is Compensation of employees?

Compensation of employees represents remuneration in return for the labor input to the production process contributed by an individual in an employer-employee relationship with the enterprise. In the international accounts, compensation of employees is recorded when the employer and employee are resident in different economies.

29. Secondary Income Account: The secondary income account shows redistribution of income, that is, when resources for current purposes are provided by one party without anything of economic value being supplied as a direct return by the other party. Transfers of a current nature reduce the income and consumption possibilities of the first party and increase the income and consumption possibilities of the second party.

30. What is the current account balance?

The balance of the secondary income account, together with the balances of the goods and services account and the primary income account, equals the current account balance.

31 What is Capital account?

The capital account in the international accounts shows (a) the acquisition and disposal of nonproduced, nonfinancial assets between residents and nonresidents and (b) capital transfers receivable and payable between residents and nonresidents.

32. What are Characteristics for inclusion as current transfers?

Characteristics for inclusion as current transfers:

- All transfers of a current nature (that are not capital transfers)

- The transfer directly affects the level of disposable income and influences the consumption of goods or services

- Cash transfers are not linked to the acquisition of a fixed asset

- Personal transfers made by or to households

- often linked to family members working abroad

- often small and frequent

- Non-personal current transfers cover a multitude of situations (e.g., technical assistance, current taxes on income and wealth, etc., social contributions and social benefits, nonlife insurance premiums and claims)

33. What are Characteristics for inclusion as capital transfers?

Characteristics for inclusion as capital transfers:

- They are typically large and infrequent

- They involve a change in ownership of a nonfinancial asset (i.e., fixed assets, valuables, nonproduced assets)

***