For who would bear the Whips and Scorns of time,

The Oppressor’s wrong …

… the Law’s delay

Hamlet

The government’s efforts to make business and commerce easy have been widely acknowledged. The next frontier on the ease of doing business is addressing pendency, delays and backlogs in the appellate and judicial arenas. These are hampering dispute resolution and contract enforcement, discouraging investment, stalling projects, hampering tax collections but also stressing tax payers, and escalating legal costs. Coordinated action between government and the judiciary– a kind of horizontal Cooperative Separation of Powers to complement vertical Cooperative Federalism between the central and state governments– would address the “Law’s delay” and boost economic activity.

INTRODUCTION

9.1 The now iconic scream of Tarikh-par-Tarikh, Tarikh-par-Tarikh (“dates followed by dates followed by dates”) by Sunny Deol was Bollywood’s counterpart to Shakespeare: two different expressional forms–the one loud and melodramatic, the other brooding and self-reflective–but both nevertheless united in forcefully articulating the frustrations of delayed-and-hence-denied justice.

9.2 India jumped thirty places to break into the top 100 for the first time in the World Bank’s Ease of Doing Business Report (EODB), 2018. The rankings reflect the government’s reform measures on a wide range of indicators. India leaped 53 and 33 spots in the taxation and insolvency indices, respectively, on the back of administrative reforms in taxation and passage of the Insolvency and Bankruptcy Code (IBC), 2016 (See Box No. 3.1 and 3.2 in Chapter 3 of Volume 2 of the Economic Survey). It also made strides on protecting minority investors and obtaining credit, and retained a high rank on getting electricity, after a 70 spot rise in EODB, 2017 due to the government’s electricity reforms. This year’s report did not cover other measures such as the Goods and Services Tax (GST), which are expected to further boost India’s ranking in the coming years.

9.3 This striking progress notwithstanding, India continues to lag on the indicator on enforcing contracts, marginally improving its position from 172 to 164 in the latest report, behind Pakistan, Congo and Sudan (See Annex I).

9.4 The importance of an effective, efficient and expeditious contract enforcement regime to economic growth and development cannot be overstated. A clear and certain legislative and executive regime backed by an efficient judiciary that fairly and punctually protects property rights, preserves sanctity of contracts, and enforces the rights and liabilities of parties is a prerequisite for business and commerce.1

9.5 The government has taken a number of actions to expedite and improve the contract enforcement regime. For example, the government: scrapped over 1000 redundant legislations; rationalized tribunals; amended The Arbitration and Conciliation Act, 2015; passed The Commercial Courts, Commercial Division and Commercial Appellate Division of High Courts Act, 2015; reduced intra- government litigation; and expanded the Lok Adalat Programme to reduce the burden on the judiciary. The government has also advanced a prospective legislative regime to ensure legal consistency, reducing chaos due to unpredictable changes in regulations. The judiciary has simultaneously expanded the seminal National Judicial Data Grid (NJDG) and is close to ensuring that every High Court of the country is digitized, an endeavor recognized in EODB, 2018. However, economic activity is being affected by the realities and long shadow of delays and pendency across the legal landscape. This chapter is a preliminary stab at quantitatively highlighting these developments based on new data that has been compiled for the Economic Survey.2

9.6 The finds are simple and stark :

(i) Delays and pendency3 of economic cases are high and mounting in the Supreme Court, High Courts, Economic Tribunals, and Tax Department, which is taking a severe toll on the economy in terms of stalled projects, mounting legal costs, contested tax revenues, and reduced investment more broadly;

(ii) Delays and pendency stem from the increase in the overall workload of the judiciary, in turn due to expanding jurisdictions and the use of injunctions and stays; in the case of tax litigation, this stems from government persisting with litigation despite high rates of failure at every stage of the appellate process; and

(iii) Actions by the Courts and government acting together can considerably improve the situation.

PENDENCY AND DELAY: FACTS

Economic Tribunals

9.7 Analysis of six prominent appellate tribunals that deal exclusively with high stakes commercial matters reveal two patterns. First, there is a high level of pendency across the six tribunals, estimated at about 1.8 lakh cases (Figure 1). Second, pendency has risen sharply over time. As Figure 2 shows, nearly every tribunal started with manageable caseloads, disposing instituted cases every year, but that soon spiraled out of control. Compared to 2012, there is now a 25 percent increase in the size of unresolved cases. The average age of pending cases across these tribunals is 3.8 years. It is noteworthy that in two cases—telecommunications and electricity—the explosion in pendency resulted from interventions by the Supreme Court (See Annex II).

High Courts

9.8 Further, the creation of tribunals at different points in time did not alter pendency at the High Courts of the country nor their ability to deal with other economic cases. Three sets of economic cases pending at five High Courts were studied for the Economic Survey: company cases, arbitration cases and taxation cases. The overall pendency of the High Courts (Annex III), and the case-wise pendency of these economic cases at High Courts (Figure 4) continue to increase. The total backlog in High Courts by the end of 2017 as per the National Judicial Data Grid was close to 3.5 million cases. While the volume of economic cases is smaller than other case categories, their average duration of pendency is arguably the worst of most cases, nearly 4.3 years for 5 major High Courts. The average pendency of tax cases is particularly acute at nearly 6 years per case (Figures 3 and 4).

9.9 Reductions in pendency, if any, were achieved either due to changes in the counting methodology of pending cases, or due to changes in pecuniary jurisdictions that led to a mass transfer of cases from the original side of the High Courts to District Courts. After such changes, the new stock of pending cases continued to grow at previous, if not higher rates (See Annex III). Intervening measures like the setting up of the National Judicial Data Grid and creation of tribunals have helped, but more is needed to improve the situation.4

PENDENCY AND DELAY: POSSIBLE REASONS

High Courts: Burden from Expansion of Discretionary Jurisdictions

9.10 One reason for the rising pendency of economic cases at the High Courts could simply be the generalized overload of cases. Further, economic and commercial cases are usually complex, require economic expertise in their handling and disposal, and hence, require more judicial time. In some instances, however, this increased overload is due to the expansion of discretionary jurisdictions by Courts, without any countervailing measures that either balance the scope of other jurisdictions or improve overall administration and efficiency.5

9.11 For example, Articles 226 and 227 of the Constitution of India empower High Courts with carefully circumscribed writ jurisdiction.6 In practice, however, High Courts have permissively and expansively interpreted this provision over a period of time, which has resulted in a substantial increase in Article 226 cases.7 There are currently one million Writ Petitions pending at the 6 High Courts studied, constituting between 50-60% of the Court backlog, with average pendency fluctuating between 3-10 years (See Annex IV). Data available for 2008- 2013 for 5 High Courts captures the continued rise in the pendency of Writ Petitions even in recent years, which is crowding out judicial time for other cases8 (Annex V).

High Courts: Burden from Original Side Jurisdiction

9.12 Some High Courts of the country retain a unique original jurisdiction, under which the High Court, and not the relevant lower court, transforms into the Court of first instance for some civil cases.9 These cases occupy a significant share of the Court’s docket. The Delhi and Bombay High Courts have original jurisdictions that occupy nearly 10-15% of their workload (Annex VII). In 2014, the share of original side cases was as high as 30% for the Delhi High Court. Data compiled for the Economic Survey suggests that the High Courts take longer to clear civil suits as compared to their district court counterparts. The average pendency of civil suits at the Delhi High Court is 5.84 years, while that at the lower courts of Delhi is 3.66 years (Table 1).10

Table 1. Average Pendency of Civil Suits in Bombay and Delhi

Supreme Court: Expansion of Special Leave Petition (SLP) Jurisdiction

9.13 The Supreme Court, like the High Courts, has less capacity to deal with mounting economic cases because of rising overall pendency (See Annex VIII). In the case of the SC, the burden derives in part from Special Leave Petitions under Article 136 of the Constitution of India, which empowers any party to approach the Supreme Court directly from any court or tribunal. Initially invoked only in “exceptional circumstances”, SLPs are now an overwhelming feature of practice at the Supreme Court.11

9.14 As Figure 5 shows, the rate at which the Supreme Court admits Special Leave Petitions under Article 136 of the Constitution increased from around 25% in 2008 to nearly 40% in 2016. In contrast, the Supreme Court of the United States of America and Canada admit 3% and 9% respectively of the cases filed before it (See Annex IX). This rising tendency to grant special leave has fundamentally altered the nature of the Court and created a high level of pendency, nearly 85% of which are SLP cases (Figure 6).12 The Court’s SLP jurisdiction does not include other cases like transfer and review petitions, each of which occupies nearly 4-6% of the Court’s docket (Annex X)13. Simultaneously, the share of writ cases has gone down from 7% in 1993 to under 2% in 2011.14

Recourse to Injunctions and Stays

9.15 Rising pendency also results from the injunction of cases by Courts. For example, in the case of Intellectual Property Rights (IPR) cases shown in Table 2 below, injunctions have led to about 60 percent of cases being stayed, whose average pendency is 4.3 years.15 Lengthy interim orders, ex parte ad interim stays, increasing rate of pendency of cases at final arguments, and few final judgments in IPR cases16 are common traits of IPR practice across different High Courts. Nearly 50% of these cases are pending at the stage of pleadings, which is the stage at which parties are required to complete formal requirements before hearing (Annex XI and Annex XII). See Chapter 8 of the Economic Survey for details on delays and pendency in filing and grant of patents.

9.16 Another 12% of these cases are pending for final disposal. The average age of cases waiting for final judgment is inordinately high at 7.9 years, showing that more attention needs to be given to cases pending at the stage of final disposal (Figure 7).

Table 2. Pending IPR

Cases- Stock (Delhi HC)

PENDENCY AND DELAY: COSTS

Costs of delay

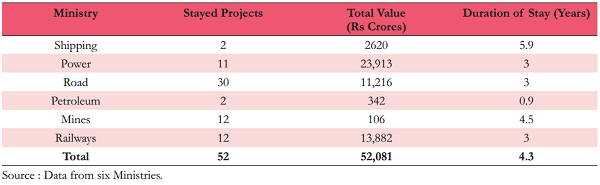

9.17 It is difficult to estimate the costs of pendency and delays. But some illustrative data are instructive in conveying a sense of potential magnitudes involved. Table 3 provides the number and value of government projects in six infrastructure ministries that are currently stayed by court injunctions, as well as the average duration of their stays. It does not include other central government projects or the multitude of state level projects that are similarly stalled by Court injunctions, nor past projects that suffered delays due to injunctions but were subsequently allowed to resume operations. The project costs (stocks) of stayed projects—at the time they were originally stayed—amounted close to 52,000 crores.

9.18 The Ministries of Power, Roads and Railways have been the hardest hit. Since project costs were predominantly debt-financed, it is likely that project costs have increased by close to 60 percent given the average duration of stay. Data collected from the State Bank of India (Table 4) revealed a similar picture for private sector infrastructure projects that sought extensions under Para 4.3.15.3 of an RBI Master circular due to arbitration proceedings or court cases (Annex XIII).

Table 3. Stayed Projects- Stock (6 Ministries, as on 31.10.2017)

Table 4. Projects Financed by SBI That Sought RBI Extensions- Last 3 Years

9.19 The overall impact of rising pendency at Appellate Tribunals, High Courts and the Supreme Court, coupled with the rising use of injunctions and other blunt instruments has led to spiraling legal expenses of Corporate India, as shown in Figure 8.

Figure 8. Legal Expenses of Corporate

India: Flow (1988- 2016, in thousand crores)

CENTRAL GOVERNMENT TAXES: A CASE STUDY

9.20 Pendency, arrears and delays are not just a feature of courts and tribunals, but also the Tax Departments and their multi-layered process.18

9.21 As of March 2017, there were approximately 1,37,176 direct tax cases under consideration at the level of ITAT, High Courts and Supreme Court (Figure 9). Just 0.2% of these cases constituted nearly 56% of the total demand value; and 66% of pending cases, each less than Rs. 10 lakhs in claim amount, added up to a mere 1.8% of the total locked-up value of pending cases.

9.22 The picture is not dissimilar in the case of indirect taxes shown in Figure 10. As of the quarter ending March 2017, a total of 1.45 lakh appeals were pending with the Commissioner (Appeals), CESTAT, HCs and the SC together, that were valued by the Department at 2.62 lakh crores. Together, the claims for indirect and direct tax stuck in litigation (Appellate Tribunal and upwards) by the quarter ending March, 2017 amounted to nearly 7.58 lakh crores, over 4.7 percent of GDP. For the Department, these numbers, especially the value of amounts involved have been rising sharply over time (See Annex XIV).

9.23 What is interesting is that the success rate of the Department at all three levels of appeal-Appellate Tribunals, High Courts, and Supreme Court– and for both direct and indirect tax litigation is under 30%. In some cases it is as low as 12% (See Table 5). The Department unambiguosuly loses 65% of its cases. Over a period of time, the success rate of the Department has only been declining, while that of the assessees has been increasing (Annex XV).

9.24 Nonetheless, the Department is the largest litigant. As Table 5 shows, the Department’s appeals constitute nearly 85% of the total number of appeals filed in the case of direct taxes, though that number seems to have improved in the case of indirect taxes. Of the total number of direct tax cases pending by the quarter ending March, 2017, the Department initiated 88% of the litigation at ITATs and the Supreme Court and 83% of the litigation pending at High Courts.

9.25 The picture that emerges over a period of time is the following: even though the Department’s

Table 5. Petition Rate and Success Rate ofthe Tax Department, as on 31.03.2017

Box 1. Supreme Court’s Successful Management ofTax Litigation

The Supreme Court is the highest court of the land that deals with a wide array of cases. When not dealing with substantial questions of law or constitutional issues requiring the constitution of special-sized benches, the Court sits in benches comprising of two judges to decide cases from High Courts and other forums of the country. The benches are expected to hear and decide cases from a wide range of subject matters inter alia constitutional law, criminal law, civil law, commercial law, and taxation.

However, the Court’s recent experiment with constituting an exclusive bench for taxation produced impressive results, which may be replicated for other subject matters, and emulated by other High Courts that do not have special rosters for daily hearings. Figure 1 shows that since the constitution of the tax bench in 2014, the Supreme Court has been able to reverse the trend of burgeoning pendency of tax cases. It is noteworthy that during this period, the SC reduced its reliance on staying claims of the Department, and focused on hearing and disposing cases, as evident from Figure 2.

Besides reducing pendency and backlog, this phase of the Supreme Court saw a large number of judgments on law, and permitted the Court to discharge its envisaged role of clarifying and settling legal questions. The special bench authored 197 judgments in 2015, nearly three times as many passed in the previous three years.1

There are other profound benefits of dedicated subject- matter benches. Such benches ensure that the Supreme Court speaks in one voice, and there is continuity and consistency of legal jurisprudence. Further, they create efficiencies by allowing the judge to focus on the specialized branch of law placed before her. The model may be replicated for other commercial and economic areas of law as and when necessary at the Supreme Court, and should be replicated by every High Court of the country.

The Supreme Court’s experience also confirms that Courts can take steps within existing design and capacity constraints to ameliorate pendency, particularly through specialized treatments of cases. For instance, there may be merit in handling different stages of cases also through specialized benches. Currently, most High Court judges hear cases in the following order: supplementary matters (new cases), advanced matters (admitted cases), and regular matters (cases listed for final disposal). Every judge starts the day with fresh cases, and reaches old cases only during the second half of the day, if at all. The experience of the SC’s management indicates that it may be more prudent to create category-wise benches that exclusively deal with cases at the stage of final hearing for the entire working week, so that they are given the attention that the IPR data (Table 2) show are necessary.

1 http://www.livemint.com/Politics/EFALB5X66jz0i2KkiE7WeL/The-apex-courts-tax-bench-experiment.html.

Table 6. Positions and Vacancies in High Courts and the Supreme Court

strike rate has been falling considerably over a period of time, it is undeterred, and persists in pursuing litigation at every level of the judicial hierarchy (See Annex XV and Annex XVI). Since tax litigation constitutes a large share of the workload of High Courts and the Supreme Court, Courts and the Department may gain from a reduction in appeals pursued at higher levels of the judiciary. Less might be more.

EXPENDITURE ON ADMINISTRATION OF JUSTICE

9.26 Total spending on Administration of Justice by States and the Centre constitutes approximately 0.08- 0.09% of GDP which is low when compared to other countries, especially common law countries (Figure 11). Research shows that while general spending on the judiciary may not impact pendency, spending on modernization, computerization and technology leads to shorter average trial lengths.21

9.27 The Government may consider including efforts and progress made in alleviating pendency in the lower judiciary as a performance-based incentive for States. Further, expenditure may be prioritized for filing, service and other delivery related issues that tend to cause the maximum delays. Data compiled for the Economic Survey reveals that nearly 30% of a case’s life is taken up by formal proceedings like service of summons and notices (See Annex XVII), issues that may be easily resolved through technological up gradation for filing and service mechanisms.

9.28 However, building additional judicial capacity may not be effective unless existing capacity is fully utilized. The higher judiciary is currently operating at 63.6% of existing capacity (Table 6). Experience from the 1990s confirms that increasing judicial capacity in the case of Income Tax Appellate Tribunals in the mid-1990s substantially reduced pendency (See Annex XVIII).

POLICY IMPLICATIONS

9.29 Pendency, delays and injunctions are overburdening courts and severely impacting the progress of cases, especially economic cases, through the different tiers of the appellate and judicial arenas. The Government and the Courts need to both work together for large-scale reforms and incremental improvements to combat a problem that is exacting a large toll from the economy. Some of the following steps may be considered:

(i) Expanding judicial capacity in the lower courts and reducing the existing burden on the High Courts and Supreme Court;

- For a smooth contract enforcement regime, it may be imperative to build capacity in the lower judiciary to particularly deal with economic and commercial cases, and allow the High Courts to focus on streamlining and clarifying questions of law. For the same, amendments to the Code of Civil Procedure, Commercial Courts Act and other related commercial legislations should be considered (See Annex XIX). These measures must be buttressed by efforts to train judges, particularly in commercial and economic cases by judicial academies;

- Downsizing or removing original and commercial jurisdiction of High Courts, and enabling the lower judiciary to deal with such cases. Early results from the Delhi High Court suggest that reducing the size of original side jurisdiction in 2016 allowed the court more time to reduce its overall pendency (See Annex XX); 23

- Courts may revisit the size and scale of their discretionary jurisdictions and avoid resorting to them unless necessary, to reclaim the envisaged constitutional and writ stature of the higher judiciary;

- Existing judicial capacity ought to be fully utilized.

(ii) The tax department exercising greater self-restraint by limiting appeals, given its low success rate. This could either take the form of ex ante rules limiting appeals, for example, to no more than one in four High Court verdicts or no more than one in three arbitration cases; or, given the long shadow of the 3 Cs (CBI, CVC, and CAG) in inducing bureaucratic risk-aversion, perhaps an independent Panel could be created to decide on further appeals of tax verdicts against the Department. Further, the number of tiers of scrutiny may be limited to three forums for taxation cases.

(iii) Substantially increasing state expenditure on the judiciary, particularly on their modernization. The Government may consider incentivizing expenditure on court modernization and digitization. This needs to be supported with greater provision of resources for both tribunals and courts. Moreover, legislations (and perhaps even judicial decisions that expand or introduce new jurisdictions) should be accompanied by judicial capacity and public expenditure memorandums, which adequately lay out the necessary provisions required to address increasing judicial requirements, and ensure their adequate funding. The amounts required may be negligible but the returns enormous;

(iv) Building on the success of the Supreme Court in disposing tax cases, creating more subject-matter and stage-specific benches that allow the Court to build internal specializations and efficiencies in combating pendency and delay;

(v) Reducing reliance on injunctions and stays. Courts may consider prioritizing stayed cases, and impose stricter timelines within which cases with temporary injunctions may be decided, especially when they involve government infrastructure projects; and

(vi) Improving the Courts Case Management and Court Automation Systems.24 The EODB, 2018 identified specific issues with India’s poor Court Management and Court Automation systems, which may be used as a template by Courts and the Government (See Annex XXI). To free up judicial time, initiatives like the Crown Court Management Services of the UK that are dedicated to the management and handling of administrative duties, may be considered.

9.30 Discussions that dominate public discourse about relations between the judiciary and other branches of government are to some extent moot. The point is not which side is right, but that the legitimacy and effectiveness of each depend on the lack thereof of the other. According to public perception, there is some Law of Constant Overall Legitimacy and Effectiveness, with one side’s loss being the other’s gain. However, this should probably give way to the Law of Mutually Reinforcing Legitimacy and Effectiveness. It is perhaps also true that the judiciary, especially the High Courts and Supreme Court, are still considered fair and final arbiters. The lament of increasing judicialization must contend with that perception.

9.31 Recent experience with the GST has shown that vertical cooperation between the center and states–Cooperative Federalism–has brought transformational economic policy changes. Perhaps there is a horizontal variant of that-one might call it the Cooperative Separation of Powers–that could be applied to the relationship between the judiciary on the one hand, and the executive/legislature on the other. There are, of course, clear lines of demarcation and separation of powers between the two to preserve independence and legitimacy. Even while respecting these lines, it should be possible and desirable for these branches to come together to ensure speedier justice to help overall economic activity.

REFERENCES

Acemoglu, Daron, Simon Johnson, and James A. Robinson. “The colonial origins of comparative development: An empirical investigation.” American economic review 91.5 (2001): 1369-1401.

Acemoglu, Daron, and Simon Johnson. “Unbundling institutions.” Journal of political Economy 113.5 (2005): 949-995.

Balganesh, Shyamkrishna. “The Constitutionalisation of Indian Private Law ”, in Choudhry, Sujit, Madhav Khosla, and Pratap Bhanu Mehta, eds. The Oxford Handbook of the Indian Constitution. Oxford University Press, 2016.

Chemin, Matthieu. “Does court speed shape economic activity? Evidence from a court reform in India.” The Journal of Law, Economics, & Organization 28.3 (2010): 460-485.

Chowdhury, Rishad Ahmed. “Missing the Wood for the Trees: The Unseen Crisis in the Supreme Court.” NUJS L. Rev. 5 (2012): 351.

Dhawan, Rajeev. “The Supreme Court under Strain: the Challenges of Arrears” MN Tripathi Pvt. Ltd. Bombay (1978).

Dhawan, Rajeev. “Litigation Explosion in India,” MN Tripathi Pvt. Ltd. Bombay (1986).

Eisenberg, Theodore, Sital Kalantry, and Nick Robinson. “Litigation as a measure of wellbeing.” DePaul L. Rev. 62 (2012): 247.

Esposito, Gianluca, Mr Sergi Lanau, and Sebastiaan Pompe. Judicial System Reform in Italy-A Key to Growth. No. 14-32. International Monetary Fund, 2014.

Galanter, Marc. “India’s Tort Deficit: Sketch for a Historical Portrait.” Fault Lines: Tort Law as Cultural Practice (2009): 47-65.

Hazra, Arnab Kumar, and Bibek Debroy, eds. Judicial reforms in India: Issues and aspects. Academic Foundation, 2007.

Islam, Roumeen. 2003. “Do More Transparent Governments Govern Better?” Policy Research Working Paper 3077, World Bank, Washington, DC.

Jones, Eric. The European miracle: environments, economies and geopolitics in the history of Europe and Asia. Cambridge University Press, 2003.

Kapur, Devesh, and Pratap Bhanu Mehta. Public Institutions in India: Performance and Design. Oxford University Press, 2007.

Kapur, Pratap Bhanu Mehta, and Milan Vaishnav (Eds), Rethinking Public Institutions in India, Oxford University Press, 2017.

Law Commission of India- Report No. 245: Arrears and Backlog: Creating Additional Judicial (wo)manpower, 2014.

Mehta, Pratap Bhanu. “India’s judiciary: The promise of uncertainty.” The Supreme Court Versus the Constitution: A Challenge to Federalism (2006): 155-177.

Moog, Robert. “Indian litigiousness and the litigation explosion: challenging the legend.” Asian Survey 33.12 (1993): 1136-1150.

North, Douglass (1990), Institutions, Institutional Change, and Economic Performance. Cambridge: Cambridge University Press.

North, Douglas E. “Institutions, Institutional Change and Public Performance” (1990).

North, Douglass C., and Robert Paul Thomas. The rise of the western world: A new economic history. Cambridge University Press, 1973.

OECD Economic Policy Papers No. 5, “Judicial Performance and its determinants: a cross-country perspective” 2013.

Porta, Rafael La, et al. “Law and finance.” Journal of political economy 106.6 (1998): 1113-1155.

Rajagopalan, Shruti. “State capacity freed is state capacity built.” Livemint, http://www.livemint.com/Opinion/cVnodqEYEF2Uiua2nxQ2oN/ State-capacity-freed-is-state-capacity-built.html (2017).

Rajamani, Lavanya, and Arghya Sengupta. “The Supreme Court of India: power, promise, and overreach.” The Oxford Companion to Politics in India (2010).

Robinson, Nick. “A quantitative analysis of the Indian Supreme Court’s workload.” Journal of Empirical Legal Studies 10.3 (2013): 570-601.

Robinson, Nick. “Structure matters: The impact of court structure on the Indian and US Supreme Courts.” The American Journal of Comparative Law 61.1 (2013): 173-208.

Robinson, Nick. “Expanding judiciaries: India and the rise of the good governance court.” Wash. U. Global Stud. L. Rev. 8 (2009): 1.

Robinson, Nick. “A court adrift.” Frontline, http:// www.frontline.in/cover-story/a-court-adrift/article4613892.ece (2013).

Rodrik, Dani, Arvind Subramanian, and Francesco Trebbi. “Institutions rule: the primacy of institutions over geography and integration in economic development.” Journal of economic growth 9.2 (2004): 131-165.

Somanathan, T. V. “The Administrative and Regulatory State”, in Choudhry, Sujit, Madhav Khosla, and Pratap Bhanu Mehta, eds. The Oxford Handbook of the Indian Constitution. Oxford University Press, 2016.

Sokoloff, Kenneth L., and Stanley L. Engerman.

“History lessons: Institutions, factors endowments, and paths of development in the new world.” The Journal of Economic Perspectives 14.3 (2000): 217-232.

Thiruvengadam, Arun. “Tribunals”, in Choudhry, Sujit, Madhav Khosla, and Pratap Bhanu Mehta, eds. The Oxford Handbook of the Indian Constitution. Oxford University Press, 2016.

Notes:

1. See North (1990); Engerman and Sokoloff (2000); Acemoglu, Johnson and Robinson (2001); Rodrik, Subramanian and Trebbi (2004); Acemoglu and Johnson (2005); La Porta et al. (1998, 1999); On India, see Kapur and Mehta (2007); Kapur, Mehta and Vaishnav (2017) and Chemin (2012).

2. The data relate to the Supreme Court, five of the major High Courts (Delhi, Madras, Bombay, Calcutta, and Allahabad), and six of the arguably most significant economic tribunals: telecommunications (Telecom Dispute Settlement and Appellate Tribunal- TDSAT), electricity (Appellate Tribunal for Electricity- APTEL), environment (National Green Tribunal- NGT), consumer protection (National Consumer Disputes Redressal Commission- NCDRC), central income tax (Income Tax Appellate Tribunal- ITAT), and central indirect taxes (Customs, Excise and Service Tax Appellate Tribunal-

CESTAT).

3 For the purpose of this chapter, the expression “pendency” denotes all cases instituted but not disposed of, regardless of when the case was instituted. The chapter does not separately calculate the life of“delayed” cases i.e. a case that has been in the judicial system for longer than the normal life ofa case (See Report No. 245 Arrears and Backlog: Creating Additional Judicial (wo)Manpower, Law Commission of India (2014).

4. In the case of the Bombay High Court, which has a critical role to play in economic and commercial cases, total pendency has soared from 23 lakh cases in 1993 to nearly 41 lakh cases in 2016 (See Annex III).

5. The higher judiciary has transformed into Courts of first rather than last resort, and have consistently fused constitutional law and tort law, dissolving traditional distinctions between public and private law. The immediate fallout of this expansion has been the steady de-legitimization of the capacity of lower courts’ private law mechanisms (Balganesh, 2016).

6 The Supreme Court in 1958 limited this jurisdiction to seeing that courts and tribunals “do not exercise their powers in excess of their statutory jurisdiction, but correctly administer the law within the ambit ofthe statute creating them or entrusting those functions to them” (G. Verrappa Pillai v. Raman & Ramon Ltd, AIR 1952 SC 192). The Supreme Court warned against exercising appellate powers under writ jurisdiction, and held that “so long as those Authorities function within the letter and spirit of the law, the High Court has no concern with the manner in which those powers have been exercised” (Nagendra Nath Bora v. Commissioner of Hills Division and Appeals, Assam, AIR 1958 SC 398).

7 Several of these writ petitions pertain to administrative law, service law, taxation law, labour law, and orders of tribunals.

8 Annex VI captures the expansion of Writ Jurisdiction and criminal quashing jurisdiction over a longer period of time, from 1980- 2016, on the basis of the number of High Court judgments that rely on Article 226 of the Constitution of India and Section 482 of the Code of Criminal Procedure.

9 A Single Judge hears the cases; registrars conduct their trials; and an appeal from them lies before the Division Bench within the same High Court. The proportion of original side cases in these Courts has fluctuated with increases in pecuniary jurisdiction. For instance, in the case of the Delhi High Court, pecuniary jurisdiction was increased from 5 to 20 lakh in 2003, and from 20 lakh to 2 crores in 2016.

10. The Supreme Court of India is currently monitoring delays in disposal of civil suits by the High Court of Delhi in Re: Case Management of Original Suits Suo Moto Writ Petition (Civil) No. 8/2017. Pursuant to the said case, the High Court of Delhi notified the Delhi High Court (Original Side) Rules, 2018, due to come in force on March 1, 2018.

11. In 1950, the Court observed that it would “not grant special leave, unless it is shown that exceptional and special circumstances exist, that substantial and grave injustice has been done and that the case in question presents features of sufficient gravity to warrant a review of the decision appealed against” (Pritam Singh v. State, 1950 SCR 453; AIR 1950 SC 169). This high standard has been relaxed over decades, leading the Court to observe in 2004 that “in spite of the clear constitutional overtones that the jurisdiction is intended to settle the law so as to enable the High Courts and the courts subordinate to follow the principles of law propounded and settled by this Court and that this Court was not meant for redeeming injustice in individual cases, experience shows that such self-imposed restrictions placed as fetters on its own discretionary power under Article 136 have not hindered the Court from leaping into resolution of individual controversies” (Jamshed Hormusji Wadia v. Board of Trustes, Port of-Mumbai (2004) 3 SCC 214).

12 A Division Bench of the Supreme Court of India in Mathai @ Joby v George (2016) 7 SCC 700 had referred a case to a constitution bench to review the criterion for granting leave under Article 136 to reverse its transformation into a regular appellate court. However, on January 11 2016, a five-Judge constitution bench refused to reduce the scope of Article 136 either by issuing guidelines or by limiting the types of cases that could be granted special leave to appeal.

13 Evidence also shows that this enhanced workload is largely from those with money, the government, and appellants geographically situated closer to New Delhi. (Robinson 2013).

14 Interestingly, this precise concern of an increased SLP workload had been foreseen and debated during the Constituent Assembly Debates: “The question of possible congestion of work in the Supreme Court has included many honorable Members to oppose the provisions of these amendments… The fear of creating a serious congestion in that Court and also the fear that we will have to employ more Judges to deal with those cases is behind this opposition. I submit, however, that this fear is unjustified. So far as the question of law is concerned, it is only a ‘substantial question of law’, which will enable a party successfully to obtain a certificate or special leave” Constituent Assembly Debate dated 14th June 1949. The debates clarified that SLP jurisdiction would be invoked only in case of “a serious breach of-some principle in the administration of justice, or breach of certain principles which strike at the very root of administration of justice as between man and man.” In light of the relaxation of standards of access to SLP jurisdiction, it is perhaps time for the Court to reconsider the scope of Article 136 of the Constitution, and lay down criteria similar to the Australian Judiciary Act, 1903 or the US Supreme Court Rules, for the sake of curbing not just the pendency of economic and other cases at the Court, but for preserving its character as the highest constitutional court of the country.

15. The increasing tendency (See Annexure 10) to grant injunctions at the interim stage has fundamentally altered the nature of IPR litigation before the High Courts, which led the Supreme Court in a recent case to ask “if the High Court had thought it proper to write such an exhaustive (interim) judgment only because of acceptance of the fact that the interim orders in Intellectual Property Rights (IPR) matters in the Delhi High Court would govern the parties for a long duration of time and disposal of the main suit is a far cry.” M/s AZ Tech (India) & Anr. v. M/s Intex Technologies (India) Ltd. & Anr.

16. https://spicyip.com/2017/06/143-patent-infringement-lawsuits-between-2005-and-2015-only-5-judgments.html.

17. Prowess is a database of the financial performance of over 27,000 companies. It includes all companies traded on the National Stock Exchange and the Bombay Stock Exchange, thousands of unlisted public limited companies and hundreds of private limited companies. It also includes a number of important business entities that are not registered companies.

18. After scrutiny, the Department or assesses have the option of approaching the Commissioner of Income Tax-Appeals (CIT-A), the Income Tax Appellate Tribunals (ITAT), the High Courts (HC) and finally the Supreme Court of India (SC). Similarly, in the case of indirect tax litigation, the Department and assesse have the option of-approaching the Commissioner (Appeals), the Customs, Excise and Service Tax Appellate Tribunal (CESTAT), the High Courts and the Supreme Court of India.

19. The success rate of the Department is calculated as the proportion of cases in which the respective court or tribunal rules totally or partially in of the Department. Cases that are set aside by the judicial authority are excluded from this calculation.

20 The Petition Rate of the Department is the percentage of the total number of appeals filed by the Department. The remaining appeals are those filed by the assessees.

21. Judicial performance and its determinants: a cross-country perspective, OECD Economic Policy Papers No. 5, June 2013.

22. Jap- Japan, Nor- Norway, Aus- Australia, Ice- Iceland, Ind- India, Den- Denmark, Ire- Ireland, Eng- England and Wales, Sco- Scotland, Fin- Finland, Swe- Sweden, Net- Netherlands, Est- Estonia, Ita- Italy, SloR- Slovak Republic, Swi- Switzerland, Cze- Czech Republic, NorI- Northern Ireland, Rus- Russia, New- New Zealand, Hun- Hungary, Por- Portugal, Pol- Poland, Slo- Slovenia, Isr- Israel.

23. The government task force formed to discuss reform measures for ease of doing business noted: “Measures introduced to streamline commercial disputes under the Commercial Courts Act has had nio impact on the indicator’s data. As Mumbai and Delhi High Courts have original jurisdiction, commercial courts have not been established at the district level, rather commercial divisions of High Courts have been established. In this regard, the High Courts of Delhi and Mumbai are being consulted and inputs from the Department of Legal Affairs has been sought.”

24. Devesh Kapur and Milan Vaishna, Strengthening India’s Rule of Law http://www.livemint.com/Opinion/N3pY337lNutBRtXQs7GO3O/Strengthening- Indias-rule-of-law.html.

Source- Economic Survey 2017-18