In general terms one can understand that a “Commitment fees” is being charged for some approved facility which can be drawn down in future at the same terms which has been agreed initially between lender and borrower. Banks are usually charged for some fees to provide this kind of facility which is usually called commitment charges/ fees.

And “Loan processing fees” are something which once can understand that the amount of upfront charges/ payments which are being recovered by a Bank at the time of disbursing the loan (net of loan) to the borrower which usually been called as facility/ or arrangement fees etc.

Refer below some of the extracts governing accounting policies on such issues of by one of private sector bank (listed in India) which uses current accounting practices (as Ind-As will be applicable on Banks w.e.f. from 2018 as notified by MCA) as mentioned on page 137 of the report-

Rader can download/ refer the full annual report of the Bank by using link-https://www.icicibank.com/managed-assets/docs/investor/annual-reports/2016/icici-bank-annual-report-2015-16.pdf

Now,

Let’s first understand COMMITMENT FEES which are being charged on account of certain arrangement between bank and a borrower to draw down certain facility in future or whenever it is agreed based on the agreed terms and conditions agreed initially. Ind-As 109 – “Financial Instruments” para 2.3 talks about the loan commitment which are within the scope of Financial Instruments-

2.3 The following loan commitments are within the scope of this Standard:

(a) Loan commitments that the entity designates as financial liabilities at fair value through profit or loss (see paragraph 4.2.2). An entity that has a past practice of selling the assets resulting from its loan commitments shortly after origination shall apply this Standard to all its loan commitments in the same class.

(b) Loan commitments that can be settled net in cash or by delivering or issuing another financial instrument. These loan commitments are derivatives. A loan commitment is not regarded as settled net merely because the loan is paid out in installments (for example, a mortgage construction loan that is paid out in installments in line with the progress of construction).

(c) Commitments to provide a loan at a below-market interest rate (see paragraph 4.2.1(d)).

Commitment fees is therefore a fees/ charges which are being taken by a lender (a bank) to provide a choice or an option to draw down additional bank facility (whatever is agreed) at the same terms which has agreed and It gives kind of assurance to a borrower about certain environment/ charges to be incurred without affecting any change in future economic environment.

Notes on Commitment fees-

- Loan commitment (fees related to such loans) which are in nature of derivatives e.g. those cases where it is a practice to sell these commitment frequently then it will be covered under derivatives and would be accounted at Fair value at its initial recognition and marked to market accounting will be done for all subsequent periods (Normal derivative accounting which is being done for any other derivative),

- Now, if there is a practice (a probability can be established) to draw down the loans over the period for which such commitment has been made between lender and borrower, then assuming that this is not covered under derivatives definition then such commitment fees will become part of the calculation of Effective Interest Rate (in simple terms EIR can be understood as normal IRR for any series of installments),

- However there could be other situations where it has been established that this facility will not be drawn down then this commitment fees can be recognized as revenue based on any systematic allocation (could be straight lined) over the period of such commitment,

Reader would appreciate that these practices are being followed by the entities which uses IFRS around the world and materiality could be considered while formulating any such process change within any entity.

Now,

Let’s understand the PROCESSING FEES and let’s have only practical thoughts about why it is being charged and how it is being treated in current accounting system Vs. new Ind-As pronouncements –

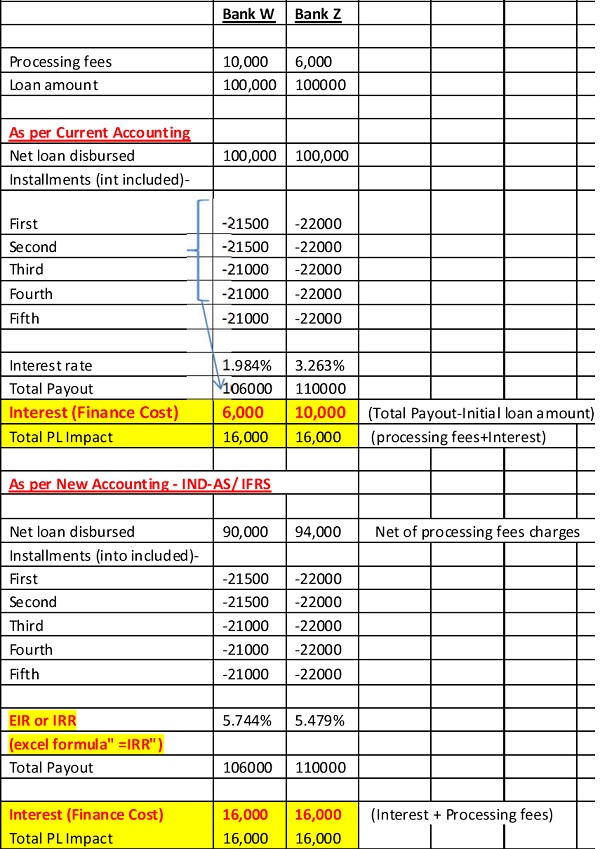

Look at the below table which shows the offers received from two different banks –

“Effective Interest rate” as per Ind-As 109 – “Financial Instrument”- The rate that exactly discounts estimated future cash payments or receipts through the expected life of the financial asset orfinancial liability to the gross carrying amount of a financial asset or to the amortized cost of a financial liability. When calculating the effective interest rate, an entity shall estimate the expected cash flows by considering all the contractual terms of the financial instrument (for example, prepayment, extension, call and similar options) but shall not consider the expected credit losses. The calculation includes all fees and points paid or received between parties to the contract that are an Integral part of the effective interest rate (see paragraphs B5.4.1–B5.4.3), transaction costs, and all other premiums Or discounts. There is a presumption that the cash flows and the expected life of a group of similar financial instruments can be estimated reliably. However, in those rare cases when it is not possible to reliably estimate the cash flows or the expected life of a financial instrument (or group of financial instruments), the entity shall use the contractual cash flows over the full contractual term of the financial instrument (or group of financial instruments).

We can summarize the above working as below –

- When we go and analyse any loan proposal from any bank or financial institution then we will have a situation where bank will provide us lower interest rate e.g. 2% from “Bank W” but requires upfront payment of INR 10,000 (on account of processing fees etc) whereas the same amount of loan offered by “Bank Z” at the rate of 3.2% approx with lower processing fees i.e. INR 6,000 (in the example above) then Treasury department works out overall IRR which will provide actual cost of funds for the deals where one bank ask more money upfront and provide lower interest rate and other provide differently. One can refer the IRR/ EIR rate calculated as per Ind-AS/ IFRS in the table above and will find that “Bank W” loan will cost around 5.74% comparing to 5.4% from “Bank Z”,

- Now, the same concept has been brought in by the new accounting standards called Ind-As/ IFRS and now all such upfront/ associated costs/ directly attributable transaction cost etc will form part of cost of funds and accordingly rate of finance expense will charge to PL,

- One can appreciate while reviewing the above table that over all finance expenses will remain same in current accounting practices and Ind-As/ IFRS BUT in current accounting practice the upfront processing fees (whatever the name you will call it) is being charged off to PL at the same time and actual loan rate is used to calculate finance expense over loan whereas under IND-AS/ IFRS a rate called Effective Interest rate (can be calculated using “=IRR” excel formula) and accordingly finance cost will flow to the profit and loss based on this EIR,

- Eventually standard wanted to amortized all such related costs under one roof and accordingly finance costs will reflect true expense while using Effective Interest rate,

This is an overall and very simplified version to understand Effective Interest rate and treatment of such fees however in practice there could be more complicated situations to calculate such EIR and to apply its accounting.

A reader will appreciate about the main objective of the standard and an approach which one can follow while keeping in mind the basis of origin of such requirements. There could possibly be some specific situations or circumstances where the interpretation of any standard will be different as we should always keep in mind that IND-AS is principle based standards and lot more areas need management judgment in line with the standards relevant interpretation and best practices.

One has to look into all related facts and patterns before concluding this type of assessment based on this concept. Readers are requested not to take this article as any kind of advice (it is not exhaustive in nature) and should evaluate all relevant factors of each individual cases separately.

For any further discussion please feel free to drop an email on anujagarwalsin@gmail.com or whats-app on +91- 9634706933

Author Bio

Can you tell me the amortization of Loan Processing Fees according to Ind AS incase of loan disbursed in tranches with different tranche maturity dates?

nice article, Thanks to bring more clarity on the subject.

A special thanks to TAXGURU commitee also who encouraged me to write and share all these articles and their efforts to reach out to maximum readers is really appreciable..turnaround time to publish articles is encouraging too…thanks

Many thanks for all your feedbacks so far which made me easier to select topics which are of most required in terms of practical approach while using latest accounting pronouncements..keep sending your all feedbacks which are really motivating..regds.