Directorate of Legal Affairs

Central Board of Excise and Customs

New Delhi

The Standard Operating Procedures for handling litigation in the Supreme Court, High Court and CESTAT has been a long felt need. This Manual of SOP is one of the flagship documents published from the Directorate of Legal Affairs, to streamline handling of litigation in the Department.

It has been our endeavour to ensure clarity and brevity while covering the minutest issue relating to litigation at various forums. Specific chapters have been written given the format of examination of the orders in accordance with the provisions of law.

A chapter, detailing the manner of preparation of paper book, so as to avoid the common defects observed during the filing of Appeals/ SLP and counter-affidavit, has been incorporated.

Though every care has been taken to ensure that this manual is most user friendly and answers to the needs of Departmental officers handling the litigation, yet scope for improvement remains. Any suggestions for improvement are welcome.

Contents

1. Appellate Mechanism

Standard Operating Procedure for:

2. Filing Appeals/ SLP before the Supreme Court 6

3. Filing CAVEAT/ counter-affidavit in SLPs/ CAs in the Supreme Court

4. Filing Appeal/ Writ Petitions in High Court

5. On the receipt of the Order of the CESTAT

6. Filing appeals to the CESTAT

7. Precautions to be taken to avoid Defective Appeals/Objections being raised in filing Appeals

Download Standard Operating Procedures on Litigation in Appellate Forums

List of Abbreviations

AoR: Advocate on Record

ASG: Additional Solicitor General

CA: Civil Appeal

CAS: Central Agency Section

CBEC: Central Board of Excise and Customs

CESTAT: Customs Excise Service Tax Appellate Tribunal

DLA: Directorate of Legal Affairs

HC: High Court

LPA: Letter Patent Appeals

SC: Supreme Court

SG: Solicitor General

SLP: Special Leave Petition

WP: Writ Petition

1. Appellate Mechanism

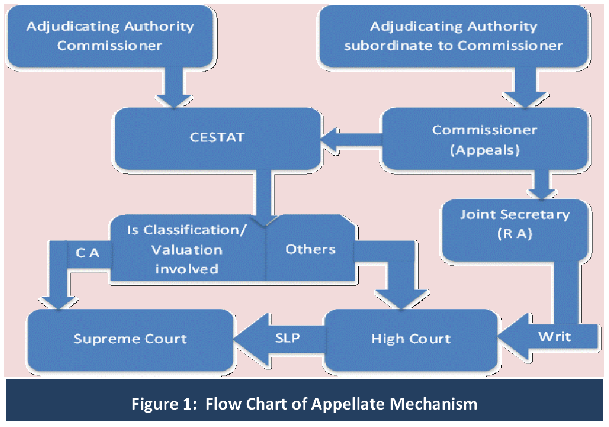

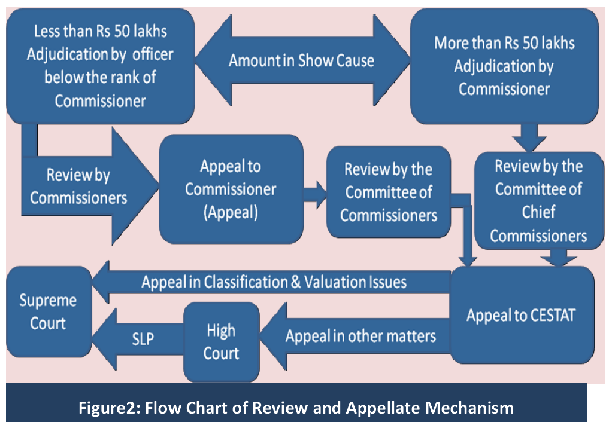

1.1 A multi-tier appellate mechanism has been provided in the Customs Act, 1962, Central Excise Act, 1944, Service Tax (Chapter V of Finance Act, 1994) against the adjudication orders passed by the Departmental officers. The scheme of the Appellate mechanism under the various Acts is explained as per the flow charts as per Figure 1 & Figure 2.

The timelines for filing the appeals before various authorities by the department are as indicated in Table 1.

| Table 1: Timelines for filing appeals by the Department | ||||

| S No | Order By | Appeal to | Period for | |

| Review | Filing Appeal | |||

| 1 | Subordinate to Commissioner | Commissioner (Appeal) | 3 months | 1 month |

| 2 | Commissioner (Appeal) | CESTAT | 3 months | |

| 3 | Commissioner | CESTAT | 3 month | 1 month |

| 4 | CESTAT | High Court | 180 days | |

| 5 | CESTAT | Supreme Court | 60 days | |

| 6 | High Court | Supreme Court | 90 days | |

As is evident from the Figure 1 above, there is well defined manner of the movement of the matter from the stage of adjudication to the Appeal/ SLP in the Supreme Court/High Courts. The flow of appeals through various stage though appears to be streamlined, but has some complexities involved and the same have been explained in the Figure 2 below. The decisions to file the appeal against the order of the Commissioner or the Commissioner (Appeal) are now vested in the Committee of Chief Commissioners or the Committee of the Commissioners as the case may be.

The Department has also been restricted from filing the appeals to the higher forums for the reason of amounts being lower then threshold limit. (Supreme Court Rs 25 lakhs, High Court Rs 10 lakhs, CESTAT Rs 5 lakhs) involved in the matter.

1.2 The provisions for appeal are contained in the Central Excise Act, 1944, Customs Act, 1962 and Chapter V of the Finance Act, 1994. The Rules pertaining to Appeals also notified in the Central Excise (Appeals) Rules, 2001 and Customs Appeal Rules, 1982.These provisions provide for appeals to Commissioner (Appeals), Appellate Tribunal, procedure, orders of Appellate Tribunal, powers of revision of the Board, revision by the Central Government, statements of case to High Courts, application to High Courts, appeal to the Supreme Court, transfer of certain pending proceedings and transitional provisions.

1.3 As per the provisions of respective Acts, any person aggrieved by the order passed by the Central Excise Officer can file an appeal to the following authorities:-

| Table 3: Appeal Provisions | |

| Order Passed by | Appeal Lies to |

| All officers subordinate in rank to Commissioner. |

Commissioner(Appeals) |

| Commissioner or Commissioner (Appeals) | CESTAT except in cases where order relates to:–

1. a case of loss of goods, where the loss occurs in transit from a factory to a warehouse or to another factory, or from one warehouse to another, or during the course of processing of the goods in a warehouse or in storage, whether in a factory or in a warehouse; 2. a rebate of duty of excise on goods exported to any country or territory outside India or on excisable materials used in the manufacture of goods which are exported to any country or territory outside India; 3. goods exported outside India (except to Nepal or Bhutan) without payment of duty; 4. Credit of any duty allowed to be utilized towards payment of excise duty on final products under the provisions of Central Excise Act, 1944, or the rules made there under and such order is passed by the Commissioner (Appeals) on or after the date appointed under section 109 of the Finance (No.2) Act, 1998]. |

| Commissioner or Commissioner (Appeals) | Revision Application to Central Govt. (in matters relating to baggage, drawback, export without payment of duty, goods short landed, loss of goods in transit). No further Appeal. |

| CESTAT | Supreme Court (Classification and Valuation cases) |

| CESTAT | High Court (Other than classification and valuation matters) |

| High Court | Supreme Court |

1.5 As per the scheme of law, every person who intends to file an appeal before the Commissioner (Appeals) or CESTAT is required to deposit the entire amount of duty fine and penalty confirmed against the person by the adjudicating/ appellate authority until the recovery of the same has been waived in part or total by the Appellate Authority.

1.6 The appeals filed before the Commissioner (Appeals) or CESTAT are filed in the forms as prescribed by the Central Excise (Appeals) Rules, 2001 and the Customs Appeal Rules, 1982. The procedure of filing the Appeals and the procedure of the Tribunal is regulated by the CESTAT Procedure Rules, 1982.

1.7 Though the appeals to the High Court and the Supreme Court are prescribed by the respective laws, the procedure of filing the appeals, writs and SLPs to these courts are governed by the rules of the respective High Court and the Supreme Court.

2. Standard Operating Procedure for filing Appeals/ SLP before the Supreme Court

2.1 Appeal Provisions

(a) Against the order of the High Court, appeal can be made to the Supreme Court by way of Civil Appeal u/s 35L(a) of the Central Excise Act, 1944 or u/s 130E(a) of the Customs Act, 1962 or Special Leave Petition under article 136 of the Constitution of India.

(b) Civil Appeal against any order passed by the Appellate Tribunal relating among other things, to the determination of any question having a relation to the rate of duty of Customs / Central Excise or Service Tax or to the value of goods/services for purpose of assessment, can be filed in the Supreme Court u/s 35L (b) of the Central Excise Act, 1944 or u/s 130E (b) of the Customs Act, 1962.

2.2 Limitation for filing Civil Appeal/ Special Leave Petition

(a) The limitation prescribed under the Supreme Court Rules, 1966 for filing Civil Appeal before the Supreme Court against the order of the Tribunal is 60 days from the date of receipt of the order.

(b) In a case where the High court on its own motion or on an oral application made by the aggrieved party, immediately after passing of the judgment, certifies the case to be fit for appeal to the Supreme Court, a Civil Appeal is filed against the High Court order under Sec. 35L of the Act for which limitation is 60 days from the date of the order (and not the date of receipt of order). However, in most of the cases no such application is made by the aggrieved party before the High Court and therefore, in such cases, if aggrieved party intends to agitate the order / judgment of the High Court before the Supreme Court, then it can be done by way of filing a Special Leave Petition under Article 136 of the Constitution.

(c) The limitation for filing of SLP is 90 days from the date of the High Court’s order. The time taken by the Court from the date of filing of application for certified copy of the order till the copy is ready for delivery is excluded from the computation of the period of limitation.

(d) Timelines as indicated in the Table in Annexure 1, shall be strictly followed for processing the Civil Appeals/ SLP proposals in the Supreme Court

(e) Office of the CC(AR)would directly communicate the orders in important matters to the Commissioners, after their pronouncement. For proper coordination, the Chief Commissioner/ Commissioner (AR) will hold regular interaction meetings with the Chief Commissioners. The Chief Commissioners would work out a mechanism for making available one officer (for a period of about three months by rotation) for collection of the orders passed by the Tribunal in respect of their Zones.

(f) The delay in applying for the certified copy of the order is attributed to the Department/party. Therefore, the procedure for obtaining the certified copy of the order of High Court should be initiated immediately on pronouncement of the order, preferably the date of pronouncement or a day after. It shall be impressed upon the Standing Counsels that it is their responsibility to apply for the certified copy of the order in time and to ensure that it is sent to the Department immediately.

2.3 Forwarding of proposal to file Civil Appeal / SLP by the Commissionerate to the Board

(a) All the proposals to file CAs/SLPs should be sent by the Commissioner only after obtaining the concurrence of the jurisdictional Chief Commissioner. While forwarding the proposal, the Commissioner shall also submit a certificate to the effect that legible copies of requisite documents are enclosed along with the proposal and that the proposal is sent within the time prescribed in the concerned circular.

(b) The proposal for filing of Appeal/SLP before the Supreme Court against the order of Tribunal/ High Court respectively, should be sent to the Board within:

i. 15 days of receipt of the order.

ii. 20 days of the pronouncement of the order.

(c) The proposal against the High Court’s order shall be initiated on the strength of the copy of the order circulated by the Court on its own motion or copy downloaded from the website of the Court i.e. www.indiancourts.nic.in or www.courtnic.nic.in without waiting for the certified copy of the order. The certified copy of the order may be sent separately thereafter. All the proposals should invariably be sent along with all the proforma as specified in Chapter 5 of this manual.

(d) The Chief Commissioners should ensure that the time limit prescribed is strictly adhered to.

(e) Serious view would be taken by the Board, if the proposal is received beyond 20 days of the receipt of the CESTAT’s order/ date of the order of the High Court.

(f) The Commissionerates should not take legal opinion from the Standing Counsels in respect of the High Court’s orders while forwarding proposal to file SLP, as the SLPs against the High Court’s orders are filed by the Board only after obtaining the legal opinion from the Ministry of Law & Justice and the Law officer of the Government of India.

(g) Similarly, the orders of the Tribunal should be examined within the prescribed time without waiting for the recommendations of the CC(AR) and proposal for filing appeal before the Supreme Court should be sent as stipulated supra. As and when the recommendation of the AR is received, the same may be sent to Board in continuation of the earlier communication.

(h) In cases, where the proposals are sent with delay beyond the prescribed period, the Commissioner should, along with the proposal, indicate the reasons for the delay.

(i) Where the proposal is sent belatedly (beyond 30 days) or where revenue involved is 1 Crore or more, the appeal proposal should be sent through a special messenger. Such messenger should preferably be an officer well conversant with the case.

(j) In matters relating to challenge to constitutional validity of certain provisions of the statute, compliance of the directions of the Tribunal / High court within certain time less than the period of limitation, filing of contempt petitions against the Department, grant of anticipatory bail, return of passports etc, and the proposal should be sent through a well conversant officer. He should be prepared to stay in Delhi for 3-7 days with the possibility of making another trip at the time of vetting.

(k) The Commissionerates must send soft copy of all the proposals with statement of facts and the grounds of appeal by e-mail to sojc-cbec@nic.in in respect of CA proposals against CESTAT order, and to dirlegal_cbec@nic.in in respect of CA / SLP proposals against the High Court’s order as soon as hard copy of the proposal along with all documents is sent by post or through messenger. This should be followed by sending the soft copy of the impugned order, and orders of the lower appellate authorities such as Commissioner (A) and /or CESTAT as the case may be, order in original and the show cause notice along with all the requisite documents as soft copies of these documents are required while preparing the paper book.

(l) It is noticed that many a time the proposals are sent by the Commissionerates to the sections of the Board not dealing with the same and redirection of such proposals adds to delay. Therefore, it is important for the field formations to note the sections of the Board to whom the proposals for filing Civil appeals and Special Leave Petitions are to be sent:-

| Table 4: Section handling the proposal of CA/ SLP in Board | ||

| S No | Category of Proposal | Concerned Person/Section |

| 1 | SLP/ Civil Appeal against the orders of High Court except cases mentioned in 3 below | Commissioner Legal, CBEC 5th Floor Hudco Vishala Building Bhikaji Cama Palace, New Delhi, 110066 |

| 2 | Civil Appeal against the orders Tribunal |

Joint Secretary (Review), CBEC 4th Floor Hudco Vishala Building Bhikaji Cama Palace, New Delhi, 110066 |

| 3 | Administration matters/ CAT orders, Vigilance Cases | Joint Secretary (Administration), CBEC North Block, New Delhi, 110001 |

2.4 Documentation with the Civil Appeal / Special Leave Petitions

(a) For proper representation of the Department’s case, it is necessary that all papers or documents presented by either side before the Tribunal or the High Court are available to the Law Officer or Counsel representing the Revenue.

(b) The Court insists that the status of the relied upon decisions of the Tribunal / High Courts is invariably indicated by the appellant, absence of which causes considerable inconvenience for proper appreciation of law and delivery of justice by the Hon’ble Judges. The Hon’ble Supreme Court had passed a judicial order stating that unless the status of connected/relied upon cases/judgment referred to by the Tribunal and the High Courts is made clear in the forefront of the synopsis of the cases annexed with the Civil Appeal/Special Leave Petition, the Registrar of the Apex Court should not number the revenue cases.

(c) Accordingly, the proposal to file civil appeal against CESTAT orders should be sent along with all related documents viz.

i. Copies of SCNs along with relied upon documents; Copy of Order-in-Original/Order-in-Appeal;

ii. Certified copy of CESTAT order indicating date of receipt by the Commissioner;

iii. Copies of relevant rules, notifications, Boards circulars, instructions quoted in the order;

iv. Copies of relied upon decisions in the CESTAT order along with their status;

v. Copy of the paper book, additional documents and counter-affidavits etc filed by any side and

vi. Any other relevant document.

(d) The proposal to file Appeal / SLP should contain the brief facts of the case, the gist of the orders of Appellate Authority/Tribunal and of the High Court and the proposed grounds of appeals along with the question of law to be framed before the Supreme Court. Apart from the documents as stated at (c) above (not all may be filed in certain cases such as in a writ petition), the following documents may also be enclosed with the proposal-

i. Copy of the writ petition under the Constitution of India / copy of the appeal / reference application under the Central Excise Act, 1944 / Customs Act, 1962 / Finance Act, 1994 as the case may be,

ii. Counter-affidavit/rejoinder filed by either side, Interim order of the court, if any.

iii. Miscellaneous application if any, filed during the course of the hearing.

(e) In criminal matters, copy of the documents seized, the statements recorded and other relevant documents prepared during the course of investigation should be sent. If these documents are in vernacular, then their proper English translation duly authenticated by an officer not below the rank of Assistant Commissioner certifying the correctness of the translation should be sent.

(f) Information on connected matters would mean details and status of the case/cases referred to and relied upon by the Tribunal or Court in the impugned order, as well as the judgments of Tribunal/High Courts or the Apex Court which are sought to be relied upon by the Department in support of their appeal. The correctness of the citations incorporated in the impugned orders, as well as applicability of these relied upon decisions to the case i.e., to say, whether CESTAT has correctly applied the ratio of a particular decision to the case under examination, should be verified. After ascertaining the correctness of the citation and applicability thereof, it shall be the responsibility of the Commissioner sending the appeal proposal to ascertain full information about the status of the relied upon cases, i.e. to say whether any appeal was filed against the said order/orders, what was the outcome of such appeal/appeals etc. Commissioners should ascertain this information from the Commissioners concerned and furnish the same to the Board.

(g) It has further been felt that a procedure must be devised by which technical literature, court orders, judgments, copies of written submissions as well as material including technical literature which is handed over to the Tribunal by the Counsel of the assessee at the time of oral submissions must be supplied to the Department. The CC(AR) shall ensure that the documents stated above are preserved and sent to the Commissioner concerned immediately after the pronouncement of the order so that the said documents can be made a part of the Paper Book in case it is decided to agitate the matter before the Supreme Court. In case the documents have not been received by the Commissioner at the time of sending the CA proposal to the Board, the same should be procured by the Commissioners from AR’s office and sent to the Board soon after dispatching the CA proposal or latest after filing of appeal.

2.5 Review of judgments of the Supreme Court

(a) Every decision of the Hon’ble Supreme Court is final and needs to be implemented without waiting for any administrative concurrence. The DLA receives the certified copy of the order from the Supreme Court registry through the Central Agency Section (CAS) and dispatches the same to the concerned Commissioner for compliance in the matter.

(b) It is pointed out that review of the Hon’ble Supreme Court’s order is rarely contemplated by the Department and a Review Petition filed. The limitation for filing of Review Petition is 30 days from the date of the order / judgment of the Supreme Court. The proposal for review must be sent by the Commissioner with the concurrence of the Chief Commissioner within 7 days of the pronouncement of order with reasons thereof.

(c) Legal, Judicial and Policy sections in the Board should also examine the orders and in cases where the order is contrary to policies of the government either by way of proposing the review or by clarifying the policy intent in light of the decision of the Supreme Court.

(d) Indicative timelines for processing the review proposal are as in Annexure

(e) The Article 137 of the Constitution, Order XLVII – Review (the I schedule) of Civil Procedure Code, 1908 and Order XL of Supreme Court Rules, 1966 may be seen for understanding the basic criteria for filing of review against the order / judgment of the Supreme Court.

3. Standard Operating Procedure for filing CAVEAT/ counter-affidavit in SLPs/ Cas in the Supreme Court

3.1 Following procedure needs to be followed by the jurisdictional officers in the cases where the High Court/ CESTAT have given the order in favour of the Department.

(a) After the pronouncement of the order Commissioner shall obtain the certified copy of the said order and examine the same to decide further course of action.

i. In case Commissioner proposes to file a CAVEAT in the Supreme Court he shall forward a proposal for the same to Central Agency Section in the manner laid down in Annexure 2. While making such a proposal, the Commissioner shall give detailed reasons for making such a proposal. The proposal shall be accompanied with the vakalatnama in favour of the Advocate on Record (AoR) and the copy of order of High Court/ CESTAT.

ii. If Commissioner decides against the filing of CAVEAT, he shall record in the case file the reasons for the same.

(b) Every month, the Commissioner shall prepare a list of all the cases of High Court/ CESTAT decided in the favour of the Department and forward the same to DLA, clearly indicating the cases in which CAVEAT has been filed.

(c) Once the High Court/ CESTAT has pronounced the judgment, the Commissioner shall observe the cause-list/advance cause-list of Supreme Court (SC) on the website-www.supremecourtofindia.nic.in with a view to monitoring fixation for hearing of any SLP filed against the order of High Court/ CESTAT. DLA shall also be suitably informed so that the any such SLP/ Appeal filed by the party against such favourable order of the High Court/ CESTAT is suitably tracked in time and proper action initiated.

(d) If the SLP/ CA has been filed by the party and Central Agency Section has obtained the copy of the same, then the date for filing the counter-affidavit starts from the date of receipt of SLP/ CA by the Central Agency Section. The timelines for filing the counter-affidavit are as indicated in Annexure 2.

(e) At the preliminary stage of admission, except where a CAVEAT has been filed, the Supreme Court hears the appellant only and decides whether the SLP/ CA is to be admitted or not. In case of SLP being dismissed, no further action is called for. Even though the Supreme Court may admit SLP without giving any opportunity to the opposite party, the general practice is that if the Supreme Court is of the view that SLP/CA needs to be admitted, a notice is issued to the respondent before admission. Record of proceedings of hearing in the Supreme Court is posted on the above mentioned website on the following day after hearing from which it could be verified whether the preliminary hearing of SLP resulted into its dismissal or further fixation for admission purpose. If the SLP is directed to be fixed for admission purpose, the Commissioner shall send vakalatnama in favour of the concerned AoR to DLA for obtaining copy of the SLP and other documents.

(f) If the Commissioner receiving the notice issued by the Registry of the Supreme Court, directly or through assessee, does not have jurisdiction over the case, he shall forward the notice to the jurisdictional Commissioner immediately under intimation to the DLA. If the Vakalatnama in favour of AoR has not yet been sent, it shall be sent to the DLA for obtaining copy of SLP and other documents.

3.2 Preparation of counter-affidavit –

DLA shall forward the Vakalatnama to AoR in CAS with a request to obtain the copy of SLP and other documents. DLA shall send the copy of SLP and other documents as received from AoR to Commissioner for furnishing para-wise comments on SLP. The Commissioner shall prepare and forward the para-wise comments on SLP along with the copy of notice and paper book, if any, received from the registry of Supreme Court, to DLA for preparation of Counter-affidavit by AoR. The DLA shall provide these papers to AoR in CAS and shall obtain draft Counter-affidavit as prepared by AoR.

3.3 Vetting and filing of counter-affidavit –

Draft counter-affidavit as received from CAS shall be forwarded by DLA to the Commissioner for vetting. The Commissioner shall vet the counter-affidavit and send it to the DLA along with the corrections suggested, if any. The DLA shall send the vetted draft along with the corrections to AoR for preparation of final Counter-affidavit. Counter-affidavit, as prepared by CAS, shall be forwarded by the DLA to the Commissioner for signature. In case the Commissioner suggests any further changes to the draft counter-affidavit, above procedure will be followed until the Counter-affidavit is prepared to the satisfaction of the Commissioner. The Commissioner shall sign the final Counter-affidavit and send it to the DLA for onward transmission to CAS for filing before the Supreme Court.

3.4 Monitoring of the SIP/Appeal coming up for hearing –

After the Counter-affidavit has been filed, the Commissioner shall continue to watch the cause list /advance cause-list for any SLP filed against the Department to come up for hearing for admission. Regarding the SLPs which have been admitted and converted into Civil/Criminal Appeals, the Commissioner shall also watch the cause-list/advance cause list for such appeals to come up for regular hearing.

3.5 Assistance to Law Officers /Appearing Counsels –

(i) The Commissioner shall ensure that the Law Officer/Appearing Counsel representing the case is briefed properly before the hearing for admission of SLP. Once the case appears in the advance list of hearing of cases on the Supreme Court website, the Commissioner shall prepare a ‘brief about the facts of the case and other relevant factual/legal developments since the time of filing of the SLP by the assessee. A soft copy of ‘Brief shall be provided to the DLA by the Commissioner within 7 days of the case getting listed in the advance cause list. In all cases where the briefing/appearing counsel desires a personal briefing or the Commissioner is of the opinion, considering the importance/revenue potential of the case, that the Counsel should be briefed, the Commissioner or Addl. Commissioner concerned shall visit New Delhi to arrange for such a briefing. DLA shall facilitate arranging of such briefing. Whenever any clarification/instruction is sought by the Law officer/ Appearing Counsel in a case, it must be provided by the Commissioner on priority.

(ii) The above procedure for preparation of the brief and briefing of the Law Officer/appearing counsel shall also be followed where after the admission of SLP and conversion of it into a Civil/Criminal Appeal, such appeal comes up for hearing before the Supreme Court.

(iii) While preparing the counter-affidavit or brief, reliance may be placed on any decided cases or provisions of law in any Act. A paper book shall be prepared containing copies of all such decisions relied upon and provisions of law in any Act referred to. The paper book shall be page-numbered and case laws shall be organized proposition wise.

3.6 Compliance of directions of Hon’ble Supreme Court

Directions issued by the Hon’ble Supreme Court must be complied with, within the time allowed. The Commissioner shall personally ensure compliance of the directions relating to Dasti service, filing of counter or rejoinder affidavit or other directions, to avoid adverse observations.

3.7 Timelines for processing of Counter-affidavit to be filed in the Supreme Court

With a view to ensuring timely filing of counter-affidavits in matters of SLP filed by the assessee in the Supreme Court, the timelines for processing proposals at different levels are enclosed as per Annexure-A, for strict adherence by all concerned.

3.8 Responsibility to ensure timely processing of Counter-affidavit /other procedures

The Commissioner shall ensure timely processing of caveat application andcounter-affidavit and their submission to the DLA as per the timelines given in Table 3. Any deviation from the timelines will have to be duly explained and delay occurring without any reasonable cause or due to negligence would be viewed adversely.

4. Standard Operating Procedure for filing Appeal/ Writ Petitions in High Court

4.1 Filing of appeals before High Courts

(a) The Chief Commissioner shall also be involved in the process of litigation before the High Courts. Acceptance of CESTAT’s orders or filing of appeals by the Commissioner before the High Court shall be subject to obtaining the concurrence of the Chief Commissioner. This mechanism would also ensure uniform approach in filing appeals before the High Courts within a Chief Commissioner jurisdiction.

(b) There are instances where the Commissioners filed appeals before the High Court after obtaining some legal advice even though the issue related to valuation or rate of duty. The High Courts rejected revenue appeals as non-maintainable and delayed appeals were filed before the Supreme Court. The Supreme Court does not condone delay on grounds like pursuing appeal before a wrong forum and has been dismissing such delayed appeals. While such instances show the Department in poor light, the issue also does not get examined on merit by the superior judiciary.

(c) On the other hand, there have been instances where Civil Appeal proposals have been sent by the field formations to the Board office in cases not relating to valuation or rate of duty in which cases appeals lies before the High Court. An appeal lies to the High Court against every order passed in appeal by the Customs, Excise and Service Tax Appellate Tribunal (CESTAT) where the order is not relating among other things, to the determination of any question having a relation to the rate of duty (including interpretation of an exemption notification) or valuation of the goods or services for the purpose of assessment, if the High Court is satisfied that the case involves a substantial question of law. When such proposals are received in Board office,

after examination in the Judicial Cell and after obtaining Members concurrence, these are returned back to the Commissionerate to file appeal before the High Court. Field officers are advised to refrain from sending such proposals to Board office as such an exercise leads to unnecessary wastage of resources and time.

4.2 Responsibility for filing of Appeal to High Court Subject to the Instructions for the time being in force on the monetary limits for filing appeals issued, the jurisdictional Commissioner of Customs, Central Excise or Service Tax as the case may be, shall be the authority to decide whether to contest an order of the CESTAT, in the light of the facts and circumstances of a particular case and the statutory provisions. He shall take a view in the matter after taking into consideration the recommendations of the authorities below.

4.3 Timelines for filing of Appeals in the High Court:

In terms of the Section 35G of the Central Excise Act, 1944, Section 130 of the Customs Act, 1962 and Section 83 of the Finance Act, 1994, every appeal against the order of CESTAT is to be preferred within 180 days of the receipt of the order of the CESTAT sought to be appealed against in the office of the Commissioner. Timelines indicating clearly the responsibilities of each level involved in the process of filing appeal to High Court are as indicated in Annexure 3.

4.4 Quality of appeals:

(a) An appeal to the High Court or the Supreme Court can be filed only on ‘Substantial Questions of Law’. The Commissioner shall have to convince himself that substantial question of law exists while deciding to file appeal before the High Court. The Substantial Questions of Law sought to be raised in

the appeal must be clearly identified and spelt out while sending the proposal for drafting the appeal to the Standing Counsels for their consideration.

(b) Although the expression ‘Substantial Question of law’ has not been defined anywhere in the statute, the Supreme Court in the case of Sir Chunilal Mehta & Sons v. Century Spinning & Mfg. Co. Ltd. AIR 1962 SC 1314 (applied by the Apex Court in M JanardhanaRaov. JCIT 273 ITR 50, has laid down the following tests to determine whether a ‘Substantial Question of Law’ is involved:

i. Whether the issue directly or indirectly affects substantial rights of the parties?

ii. Whether the question is of general public importance?

iii. Whether it is an open question in the sense that the issue has not been settled by pronouncement of the Supreme Court?

iv. Whether the issue is not free from difficulty?

v. Whether it calls for a discussion for alternative views?

(c) Perversity of facts also constitutes ‘Substantial Question of Law’ as it falls in (d) and (e) above. Hon’ble Supreme Court in Sudarshan Silk &Sarees v. CIT 300 ITR 205 has laid down the attributes of perversity by holding that an order or finding is perverse on facts if it falls under any of the following categories:

i. The finding is without any evidence.

ii. The finding is contrary to the evidence.

iii. There is no direct nexus between the conclusion of fact and primary fact upon which that conclusion is based?

iv. When an authority draws a conclusion which cannot be drawn by any reasonable person or authority on the material and facts placed before it.

4.5 Preparation of Memorandum of Appeals / Papers etc.

The Commissioner shall ensure that:

(a) There is proper vetting of Memorandum of Appeals as regards relevant facts therein before the appeal is actually filed;

(b) Necessary particulars relating to appellant and respondent are correctly stated.

(c) All annexures including copies of orders of authorities below are properly typed as per the High Court Rules to avoid defect/office objections.

(d) In case, any document like statements, depositions and evidences etc. Crucial to the issue involved and considered by lower authorities are included as part of the paper book and properly indexed. These documents should be properly referred to in the appeal.

(e) An illustrative list of precautions to be taken to avoid defective appeals/objections being raised in filing appeals to High Court and guidelines for typing of appeal papers etc. Are discussed in the Chapter 7. However, the Standing Counsels representing the Department’s case may be further consulted on procedural aspects, wherever considered necessary.

4.6 Filing of appeal and subsequent monitoring:

The Commissioner should ensure that:

(a) The appeal is filed in the Registry of High Court within the prescribed time limit.

(b) Diary Number / Lodging Number and Appeal Number allotted by the Registry is obtained and recorded in relevant file folder maintained in the office of Commissioner.

(c) In case the Registry of the High Court notifies any defect or office objection, immediate steps are taken to remove the same with the assistance of the filing Counsel and compliance is reported.

(d) One set of appeal memo is sent to the concerned division/ group for linking with the relevant case records maintained there.

(e) In case, the assessee files counter-affidavit, the appearing counsel makes available the same to the Commissioner to file Rejoinder affidavit to rebut the contention of the assessee.

(f) The appeals should be followed up and the Department effectively represented at every hearing/stage.

(g) Proper coordination with the appearing counsel is maintained at every stage.

(h) The details and information called for by the High Court/ appearing counsels should be furnished (in quadruplicate) at the earliest and, in any case at least three days before the date fixed for hearing before the High Court.

4.7 Appeal/Writ Petition filed by the assessee

(a) As soon as the Memo of Appeal / Writ Petition filed by the assessee is received, a file should be opened in the office of Commissioner and assigned a proper identification number incorporating the Appeal No. /WP No. allotted by the High Court.

(b) Factual comments on the Memo of Appeal / Writ Petition and judicial precedents in support of the Revenue’s stand should be forwarded by the Commissioner to the Departmental Counsel for drafting counter-affidavit. The Commissioner should ensure that the counter-affidavit is filed within the time allowed by the Court and further follow up actions taken in consultation with the counsel.

4.8 Power to defend Union of India, Ministry of Finance, Secretary (Revenue), Chairman CBEC etc. In cases before High Court

All the cases before High Court, pertaining to Indirect Taxes, wherein Union of India, Ministry of Finance, Secretary (Revenue), Chairperson CBEC, or any of these figure as respondents, should be defended by the Commissioner concerned. In all such cases, appropriate authorization is issued by the Legal Section of the Board.

4.9 Compliance of High Court directions

(a) The Commissioner shall personally ensure compliance of directions of the High Court like Dasti service, filing of counter or rejoinder affidavit or other specific directions within time frame to avoid adverse observations.

(b) There should be close co-ordination between field officers and Standing Counsels in the High Court so that directions are communicated in time and proper compliance is made to the satisfaction of the Court.

4.10 Judgments of High Court containing strictures etc.

Judgments of the High Court containing strictures or which are contrary to Board’s orders, notifications, instructions, circulars etc. Shall be brought to the notice of the Board (concerned division) immediately by the Commissioner under intimation to Legal Section of the Board.

4.11 Assistance to Departmental Counsels

(a) The Commissioner should ensure that whenever the Departmental Counsel seeks Instructions / clarifications in a case, the same are attended to by the officers concerned promptly. The counsel should be briefed properly to strengthen Revenue’s case.

(b) The Commissioner should personally involve himself in cases involving intricate issues of facts / law having wide ramifications or involving high revenue stake.

6.1 Letter Patent Appeals (LPA)-

(a) Letter Patent appeal is an intra court appeal. It is an appeal before the two judges of the same High Court against judgement of single judge. Subject to minor differences in different High Court Rules, normally a judgement and order passed under Article 226 of the Constitution is appealable as LPA and judgement and order passed under Article 227 is not appealable under this category.

(b) Proposals are being sent to the file SLP against the order of the single member bench of the High Court without examining the possibility of filing LPA. Commissioner should examine this aspect every time while making the proposal for filing SLP against the order of a Single Member Bench, and, in fact should make a mention of such examination while making the proposal to file SLP.

4.13 Performance Monitoring of the Senior and Junior Standing Counsels:-

(a) CBEC in consultation with the jurisdictional Chief Commissioners and after taking the approval of the Ministry of Law appoints a panel of Senior and Junior Standing Counsels to represent the Department before various High Courts. Every Commissioner should monitor the performance of the Senior and Junior standing counsels representing the Department in the cases in his jurisdiction, and submit a report every six months to the Chief Commissioner in the prescribed proforma.

(b) On the basis of the reports received from the Commissioners, Chief Commissioner should review the performance of the Counsels and submit a report in the prescribed proforma to the Board.

5. Standard Operating Procedure on the receipt of the Order of the CESTAT

(a) In terms of the Section 35G of the Central Excise Act, 1944, Section 130 of the Customs Act, 1962 and Section 83 of the Finance Act, 1994, appeal can be filed against the order of CESTAT in the High Court in the matters not involving the determination of any question having a relation to the rate of duty of excise or to the value of goods for purposes of assessment. In terms of the Section 35 L of the Central Excise Act, 1944, appeal in all such cases lie to the Supreme Court. However still in a number of cases involving the determination of any question having a relation to the rate of duty of excise or to the value of goods for purposes of assessment, the appeals are being regularly filed before the High Court contrary to the provisions of law.

(b) The following standardised procedure may be followed by the jurisdictional Commissioners for examining the orders of CESTAT, for determining the question of law in relation to filing of the appeals to High Court or Supreme Court.

5.1 Proforma for the Office of CC(AR) to make recommendations on the Order of CESTAT:

Office of the CC(AR) has dealt with the cases before CESTAT and their opinion in the matter will certainly act as a guiding factor to facilitate the decision making. The Board, vide its letter F. No. 390/Misc/411/07- JC dated 6th February 2008 had laid down the following mechanism in this regard respect of the Office of the CC(AR):-

a. All orders passed by CESTAT will be examined by the concerned AR’s and put up to the Chief Commissioner CC(AR) to examine the correctness and legality of the Order.

b. In case the CC(AR) is of the view that appeal needs to be filed against the Order, he will send a letter along with details in the proforma in Annexure 4 to the concerned Commissioner giving his opinion about the need for challenging the Order.

c. All orders involving revenue implications over 1 Crore will also be placed before the CC(AR).

5.2 Proforma for Scrutiny of the CESTAT Order by the Commissioner

The Commissioner should on the receipt of the order of CESTAT, and before taking any decision to file the Appeal before the Supreme Court or High Court get the all the proforma completed and should himself certify about the correctness of the information/ decision entered in the proforma specified in Annexure 5. The proforma should be signed both by the Commissioner and Chief Commissioner and should be made the part of the proposals made for filing the appeals before Supreme Court/ High Court.

5.3 Final Recommendation:

The Commissioner/ Chief Commissioner should make their final recommendations on the order of the CESTAT in the proforma as indicated in Annexure 6.

5.4 Connected Matters:

Information on connected matters would mean details and status of the case/cases referred to and relied upon by the Tribunal or Court in the impugned order, as well as the judgments of Tribunal/High Courts or the Apex Court which are sought to be relied upon by the Department in support of their appeal. The correctness of the citations incorporated in the impugned orders, as well as applicability of these relied upon decisions to the case i.e., to say, whether CESTAT has correctly applied that ratio of a particular decision to the case under examination should be verified. After ascertaining the correctness of the citation and applicability thereof it shall be the responsibility of the Commissioner sending the appeal proposal to ascertain full information about the status of the relied upon cases, i.e. to say whether any appeal was filed against the said order/orders, what was the outcome of such appeal/appeals etc. Commissioners should ascertain this information from the Commissioners concerned and furnish the same to the Board. While examining the order of CESTAT, Commissioner should also examine with regards to connected matters that might be pending in the Supreme Court/ High Court and give the details of the connected matters in proforma in Annexure 7

5.5 Recommendations of the Commissioner/ Chief Commissioner on the order of CESTAT

(a) In respect of all the orders of CESTAT, Commissioner/Chief Commissioners should ensure that the proformas specified in Annexure 5, 6 & 7 are completed in all respect and placed in the file in which the order of CESTAT is examined.

(b) In case the recommendation is to file the appeal, then a proposal along with proformas specified in Annexure 5, 6 & 7 is submitted to Standing Government Counsels in the cases where appeal is proposed to High Court or to the Board in case the appeal is proposed to the Supreme Court.

6. Standard Operating Procedure for filing appeals to the CESTAT

6.1 Legal provisions for Appeals to CESTAT

(a) Department can file appeal to CESTAT against the order of Commissioner as adjudicating authority or the order of the Commissioner (Appeal). The relevant legal provisions are enumerated in the table below:

| Table 5: Review Provisions under Indirect Tax Law | ||

| Order By | Legal Provision | Review By |

| Commissioner as adjudicating authority |

Section 35E of Central Excise Act,1944, Section 129D of Custom Act, 1962 & Section 86(2) of Finance Act,1994 |

Committee of Chief |

| Commissioner Commissioner (Appeal) | (Appeal)Section 35 B(2) of Central Excise Act,1944, Section 129 A(2) of Custom Act, 1962 & Section 86 (2A) of Finance Act, 1994 | Committee of Commissioner |

(b) While taking the decision to file the appeal against the order under consideration, the Committee of Chief Commissioners/ Commissioners will also take into account the amounts involved in the issues against which the appeal is to be filed. In case the amount involved is below the specified threshold limit then they should record that order is not appealed against because of the low amounts involved.

(c) Once the Committee of Chief Commissioner or the Committee of Commissioner communicates its decision to contest a particular order of Commissioner or Commissioner (A), it shall be the responsibility of the Adjudicating Officer or the Central Excise Officer so authorized, to ensure timely and proper filing of appeal in the CESTAT and consequential follow up actions.

6.2 Timelines for filing of Appeals in CESTAT

Time lines, indicating clearly the responsibilities of each level involved in the process, for filing appeals to CESTAT have been laid down in the Annexure 8.

6.3 Proforma for Scrutiny of the Order:

The Committee of Chief Commissioners/ Commissioners should for the purpose of scrutiny of the order of the Commissioner/ Commissioner (Appeals) gets completed and the proforma as specified in Annexure 9 completed. On the basis of their findings recorded in this proforma the committee should make final view for reviewing or otherwise in respect of the order under consideration.

6.4 Final Recommendations of the Committee:

(a) After recording the findings the Committee should record their decision in respect of the order under consideration in the proforma in Annexure 10.

(b) In case of a combined order or order in a group case, involving more than one assessee falling under jurisdiction of different Commissionerates, the jurisdictional Commissioner shall communicate the stand taken on common issues to the Commissioner having jurisdiction over other case(s).

6.5 Preparation of Memorandum of Appeals / Papers etc. The officer authorized to file appeal shall:

(a) Once the grounds and authorization under 35E of Central Excise Act,1944, Section 129D of Custom Act, 1962 & Section 86(2) of Finance Act,1994 or 35 B(2) of Central Excise Act,1962, Section 129 A(2) of Custom Act, 1962 & Section 86 (2A) of Finance Act,1994 for filing appeal are received from the Committee, Memo of Appeal is duly filled-in and filed by him, with all necessary annexure, in the registry of CESTAT before the expiry of limitation.

(b) There is proper vetting of Memorandum of Appeals as regards relevant facts therein before the appeal is actually filed.

(c) Necessary details including the revenue involved are properly and correctly mentioned.

(d) All annexures including copies of orders of authorities below are properly typed as per CESTAT Rules to avoid defects/office objections. In case, any document such as agreement, seized papers, depositions etc., and the evidences relied upon crucial to the issues involved and considered by lower authorities, are referred to at relevant place in appeal memo and their copy annexed thereto.

(f) The Appeal No. of the appeal filed is obtained and recorded on other sets (including office copy) of the appeal papers. He should communicate the same to the Review Section within the prescribed time limit.

6.6 Filing of Appeal and subsequent monitoring

The Commissioner shall put in place a proper mechanism with defined responsibility of different levels of officials in his charge to ensure that:

(a) The appeal is filed in the CESTAT within prescribed time limit.

(b) Appeal Number allotted by the registry is obtained and recorded in judicial folder in Commissioner’s office.

(c) In case, the Registry of the CESTAT notifies any defect, immediate steps are taken by the concerned to remove the same with the assistance of the office of CC(AR).

(d) One set of Appeal Memo is kept with the jurisdictional Division.

(e) The appeals are followed up and the Department is effectively represented at every hearing stage.

(f) Proper coordination with the Authorized Representative is maintained at every stage.

(g) The details and information called for by the CESTAT/AR should be furnished (in quadruplicate) at the earliest and, in any case at least three days before the date fixed for hearing before the CESTAT.

6.7 Appeals/ Cross Objections filed by the assessee

(a) In cases where appeal to CESTAT against the order of Commissioner (Appeals) is filed by the assessee (whether Department has filed appeal or not), the Commissioner shall ensure to put in place proper mechanism to examine the desirability of filing cross-objections (CO) in suitable cases. As soon as the Memo of Appeal filed by the assessee is received, a file should be opened in the office of Commissioner and assigned a proper identification number incorporating the Appeal No. allotted by the CESTAT and further necessary action taken.

(b) Officers have to be alert particularly in those cases where Commissioner (A)’s order was not acceptable but appeal was not filed as revenue involved was below the prescribed limit. If the assessee has filed appeal in CESTAT in such cases, the Commissioner shall direct the Central Excise/ Custom officer to file cross objections against that part of the order to which he objects, within the statutory time limit.

6.8 Responsibilities of Chief Commissioner and Commissioners in the office CC(AR):

(a) Chief Commissioner (AR) will be responsible for the overall supervision and representation of the cases before all the benches of the CESTAT. However in addition he will be directly responsible for the representation of the cases before the bench of President in CESTAT.

(b) Improving the quality of Departmental representation and upgrading the level thereof before the Tribunal is a priority area. Board has vide D.O.F. No.390/Misc/411/07-JC dated 7th January 2008 to the Chief Commissioner(Authorized Representative) instructed that the following types of cases shall be taken up by the Commissioner in CC(AR) office before the Tribunal as far as possible:

i. On the basis of aggregate of the duty, fine, penalty and interest (if quantified):

| Act | Amount involved is more than | |

| Central Excise Act, 1944 | Rs 3 crores | |

| Customs Act, 1962 | Rs 1 crore | |

| Chapter V of Finance act, 1994 | Rs 50 lakhs | |

ii. All matters before the Larger Benches. However, in such cases, the Commissioner’s may take the assistance, if necessary, of the AR who represented the Department before the Referral Bench.

iii. All matters remanded by the Hon’ble Supreme Court or High Courts.

iv. All cases involving important question of law, cases having recurring revenue implication and cases having all India ramifications.

v. Any other case, as may be assigned by the CC(AR).

6.9 Engagement of Special Counsels in cases involving complexities of law / high revenue stake/ having all India ramifications

A panel of retired officers of the Department as Special Counsels was constituted in Aug 2006 (panel has been expanded and is constituted upto 2014) to defend the cases of Revenue with their specialized knowledge in respect of cases involving complexities of law / high revenue stake/ cases involving all India ramifications. The Chief Commissioners may assign the cases to them in accordance with the guidelines laid down in this regard. The

Commissioners may take stock of cases of the nature as specified above and recommend to the Chief Commissioner concerned for the engagement of the special counsel out of the said panel. The Chief Commissioner (Authorized Representative) may also send his recommendations to the Chief Commissioner concerned for engagement of special counsels, if need be. The Chief Commissioner (Authorized Representative) will also provide input to the Chief Commissioners in annual performance review of such special counsels.

6.10 Briefing the Departmental Representatives / Special Counsels by well conversant officers of the Commissionerate in important matters

(a) Well conversant officer(s) should be sent by the Commissioners to brief the Authorized Representative / Special Counsels in important matters for effective presentation of the case before the Tribunal. The Chief Commissioner (AR)/Commissioner (AR) should bring to the notice of the Chief Commissioners concerned, with a copy to Member (L&J), any instance of failure on the part of the Commissioner to send well conversant officer for briefing whenever the same was called for. The Chief Commissioner/ Commissioners (AR) shall undertake a review of the briefing outcomes on a monthly basis in this regard.

(b) In the case of Briefing of the Special Counsels the office of Chief Commissioner (AR) should be actively associated and such briefings should be organized in consultation and presence of the officers from the office of Chief Commissioner (AR)

6.11 Filing of written submissions in important matters:

(a) In every important case, a written submission should be filed before the Bench by the officer representing Department before the Bench. If such a submission has not been filed for any reason, then a suitable note bringing up the submission in the case file should be placed for review before the Commissioner (AR) and before the Chief Commissioner (AR) where Commissioner (AR) has appeared before the bench.

(b) In the cases where the Department has engaged a special counsel, written submissions should invariably be filed. The written submission should be filed in consultation with the office of Chief Commissioner (AR).

6.12 Compliance of CESTAT Directions

The Commissioner shall put in place proper mechanism to ensure timely and due compliance to the directions of the CESTAT. Close co-ordination between field officers, and the Office of CC(AR) in the CESTAT has to be ensured so that directions are communicated in time and proper compliance is made to the satisfaction of the Tribunal.

6.13 Orders of CESTAT contrary to the Board’s Order, Notification etc.

Orders of the CESTAT which are contrary to Board’s orders, notifications, instructions, circulars etc. shall be brought to the notice of the Board (concerned division) immediately by the Commissioner through the Chief Commissioner.

6.14 Proper Judicial Record Management System

(a) The Commissioner shall, inter alia, ensure that once appeal to CESTAT is authorized against the order of Commissioner / Commissioner (A), a separate judicial folder for the assessee is maintained in his office. Among other things, the folder should have a copy of relevant documents (along with copies of key documents used as evidence in support of additions made), a copy of the remand report, if any, and the scrutiny report submitted by at the time of review of the order.

(b) Such judicial folder should be easily retrievable for scrutiny of CESTAT order or Judgment of the High Court, as the case may be, at the time of considering further appeal in the case, if any.

(c) A similar judicial folder in respect of assessee’s appeal filed in CESTAT, containing a copy of the Appeal Memo filed by the assessee and other relevant documents should also be maintained for the aforesaid purpose.

6.15 Transfer of Jurisdiction outside Commissioner’s Charge during pendency of Appeal

(a) In case of transfer of jurisdiction over a case from one Commissioner to another Commissioner’s charge during pendency of appeal, the transferor AO shall, while transferring the case records along with the judicial folders in Commissioner’s office to the transferee AO, duly inform the change of jurisdiction to the Registrar CESTAT with a copy to his Commissioner’s office. This fact of intimation to the Registrar CESTAT shall also be mentioned by him in the transfer memo.

(b) This procedure shall apply to the appeals filed by the Department as well as by the assessee.

(c) In such cases, if the CESTAT order is received by the transferor Commissioner, he shall immediately return the same to the Registrar, CESTAT referring to the earlier intimation of transfer of jurisdiction and informing that in view of the transfer of jurisdiction it is the transferee Commissioner who holds jurisdiction over the case and as such the service of the order should be made on him. A copy of the communication to the Registrar should be endorsed to the transferee Commissioner along with the copy of Tribunal’s order for taking further necessary action.

(d) In case of transfer of jurisdiction over a case involving two different Benches of CESTAT during the pendency of appeal, necessary steps shall be taken by the transferor Commissioner to request the CESTAT Bench where the case is pending to transfer the same to the Bench of CESTAT having jurisdiction over the cases of transferee Commissioner. The matter may also be

coordinated with the transferee Commissioner.

7. Precautions to be taken to avoid Defective Appeals/Objections being raised in filing Appeals

7.1 Dates

(a) The dates should be written correctly and no blanks should be left.

(b) The relevant period, dates of order in original, appellate orders along with the date of its receipt in the Commissioner’s office should be mentioned.

(c) The date of order should be mentioned on the concerned exhibits.

(d) The dates of orders in the index, in averment of appeal and in exhibits should not mismatch.

7.2 Exhibits:-

(a) All exhibits should be marked in the margin on the left side in the Memo of Appeal, whenever an exhibit is introduced.

(b) All exhibits should be marked separately in the index along with dates.

(c) The exhibits should be clear and copies attached should be legible.

(d) Certified true copies of exhibits should bear the signature of the person making the averment of the correctness of the appeal filed.

(e) There should be no mistake in typing and a comparison should be made of the typed copy with the original before filing.

7.3 Time-barred appeals:-

(a) If appeals are time barred by limitation, an application for condonation of delay along with the affidavit explaining the delay should be attached.

(b) In cases of extraordinary delay, a detailed affidavit explaining each day of delay should be attached.

7.4 Appeal title:-

(a) The Appeal title should show specific Commissioner Charge and place for example Commissioner II Mumbai.

(b) The CESTAT Appeal number, i.e. the Appeal Number given by the Appellate Tribunal should be correctly mentioned in Appeal Title in the Memo of Appeal.

(c) The relevant section under which appeal is filed should be mentioned in the title.

7.5 Numbering of pages:-

(a) The pages should be correctly numbered and no blanks should be left either in the pages or in the index.

(b) All pages should be initialled.

7.6 Note of appearance:-

The note of appearance must be dated by the Counsel (the lawyer who files the Vakalatnama)

7.7 Flagging of relevant papers:-

(a) The proforma, synopsis, prayers, impugned orders and exhibits should be duly flagged.

(b) The prayer clause must be flagged.

7.8 Other details:-

(a) The synopsis should be complete and should contain a list of case laws relied upon.

(b) Details of disputed claim must be given in rupees.

(c) Valuation clause for Court fee payment to be written.

(d) Denomination of Court fee stamps to be given.

(e) Confirmation of Court fee payment should be made.

(f) The original set should be carefully prepared and no part of duplicate sets should come into or be made a part of original sets.

(g) The paras in the Appeal Memo must be correctly numbered.

7.9 Guidelines for typing and preparation of application

(a) Typing should be in double space throughout on full-scape paper. One and a half space may be used, but single space typing is forbidden.

(b) A margin of two inches on the left and right side of the paper and at least one inch on the top and bottom of paper should be left.

(c) The pleadings to be filed in the High Court are stitched on the left side and proper space should be left for stitching, so that the typed matter should not get hidden inside the stitches.

(d) All the blanks regarding dates, names etc. should be filled in after minutely checking up the matter. No blanks should be left.

(e) The signing officer should write at the end of each Exhibit- “True Copy” and put his signature and name below it.

(f) In all the exhibits, on the first page, the exhibit number should be written in good handwriting on the top right hand corner.

(g) In the body of the petition when an exhibit is first introduced, a clarification must follow as to what it is – e.g. ” ……… hereto annexed and marked as ‘Exhibit – A’ being a copy of the order of the Assessing Officer……… ” Therefore, the words “Exhibit – A” should be written on the left hand margin. At the end of each exhibit, the date of passing of the order (of the relevant exhibit) should be written.

(h) The signing officer should sign both sets of papers which are meant for judges.

(i) The High Court rules require advance service of appeal/Writ petition, reply affidavit, counter-affidavit, rejoinder etc. and attachment of proof of service. The proof of service is to be attached with the original set.

(j) Certified true copy of the impugned order should be attached with the original set. In case of common order disposing off a number of appeals, a separate application seeking permission of the court for not filing the original copy of CESTAT order should be moved.

(k) Court fees stamps should be affixed on the right top corner and not in the margin.

(l) Any cuts or erasures on the application should be initialled by the Signing Officer in the presence of the Court Officer while filing the appeal. (m) Each and every section of the application should be duly flagged.

Annexure 1

| Time frame for filing Civil Appeal/ SIP in cases relating to Central Excise Customs and Service Tax and Recommended Time Frame | |

| Civil Appeal (CA) | Special Ieave Petition (SIP) |

| Impugned order passed by CESTAT | Impugned Order-High Court |

| Receipt of impugned order through post (Day 0) | Application for Certified Copy same day |

| Receipt of Certified Copy (Day 0) | |

| Preparation and submission of proposal for challenging order in form of comments by concerned Commissionerate (15 days) | Preparation and submission of proposal for challenging order in form of comments by concerned Commissionerate (20 days) |

| All case papers including proposal sent to Judicial Cell, CBEC in cases relating to rate of duty and valuation papers, which takes decision to challenge order (10 days) | Examination of SLP proposal against High Court order by Legal Cell (10 days) |

| Consultation with the concerned policy section (2 days) | |

| Case papers sent to Central Agency Section for drafting Appeal | Case Papers to be examined by the Law Ministry and forwarding the same to Central Agency Section (CAS) with their opinion- CAS seeks the opinion of the Law Officer as to the feasibility of challenging the order by way of SLP. (7 Days) |

| CAS marks file to panel counsel for drafting Appeal/SLP (1 day) | |

–

| Drafting Counsel returns draft SLP/ Appeal to CAS (7 days) | |

| CAS forwards draft SLP/ Appeal to CBEC (Legal / Judicial Cell), D/o Rev. M/o Finance for vetting (1 day) | |

| Vetted drafts are returned to CAS for filing with marked Annexures-(2 days) | |

| Preparation of paper book (typing/copying) by CAS (5 days) | |

| Total Time for filing the CA against the order of CESTAT – 41 days | Total Time for filing the SLP against the order of High Court – 55 days |

Annexure 2

| Timeline in case of SLP filed by the Assessee/taxpayer | ||||

| S No | Description of Action Point | Number of Days | ||

| Absolute | Cumulative | |||

| If CAVEAT is to be filed in the Supreme Court | ||||

| 1 | Date of pronouncement of judgment by High Court | – | – | |

| 2 | Commissioner to examine the order of High Court and to decide whether Caveat is to be filed | 5 | 5 | |

| 3 | If Caveat is to be filed, Commissioner should send proposal to Directorate of Legal Affairs (DLA) for filing of CAVEAT | 5 | 10 | |

| 4 | DLA to send proposal for filing of Caveat to CAS | 3 | 13 | |

| 5 | CAS to file Caveat and inform (DLA). | 3 | 16 | |

| 6 | DLA will inform Commissioner about CAVEAT having been filed |

3 | 19 | |

| To file the Counter to the SLP/ CA filed by the party against the orders of the High Court/ CESTAT | ||||

| 1. | Commissioner/ DLA to keep a watch on the daily and advance cause list uploaded on the website of supreme court (www.supremecourtofindia.nic.in) to identify the SLPs/ CAs filed by the party and take the notice of them. | – | – | |

| 2. | DLA to inform the Commissioner concerned within 2 days of the information being uploaded on the website |

|||

| 3. | In case the Supreme Court is of the view that prima facilely the SLP/ CA filed by the party needs to be admitted a notice is issued to the Department/ concerned Commissioner. | 0 | 0 | |

| 4.

|

Commissioner should prepare the Vakalatnama in the name of concerned Advocate on Record (AoR) in the standard format and send the same to CAS under intimation to DLA. | 2 | 2 | |

| 5. | DLA to get in touch with the Central Agency Section to obtain the Copy of SLP/ CA and forward the same to concerned Commissioner | 7 | 9 | |

| 6. | Commissioner should get the SLP/ CA examined and furnishes the para-wise comments on the same for preparation of counter-affidavit to CAS under intimation to DLA. While sending the intimation to DLA, Commissioner should

invariably forward the copy of para-wise |

10 | 19 | |

| 7. | Preparation of draft counter-affidavit by AoR& dispatch to Commissioner / DLA for vetting | 7 | 26 | |

| 8. | Vetting of draft Counter-affidavit by Commissioner and returning it to Central Agency Section under intimation to DLA. | 2 | 28 | |

| 9. | Preparation of counter-affidavit by CAS and dispatch to concerned Commissioner under intimation to DLA. |

4 | 32 | |

| 10 | Dispatch of signed counter-affidavit by Commissioner to CAS under intimation to DLA. | 3 | 35 | |

| 11. | CAS to file the counter-affidavit in registry of the Supreme Court and inform the concerned Commissioner under intimation to DLA. | 3 | 38 | |

| 12. | DLA to confirm about filing of the Counter to Commissioner | 2 | 40 | |

Annexure 3

| Timelines for filing of the Appeal to High Court | |||

| S No | Stage | Number of days | |

| Absolute | Cumulative | ||

| 1 | Receipt of CESTAT order in the office of Commissioner | 0 | 0 |

| 2 | Entry in the Records in Commissioner Office and linking with the earlier files and folders | 2 | 2 |

| 3 | Consultation within the Commissionerate, i.e. with the Division and Range etc and taking prima facie view on the order by the Commissioner | 45 | 47 |

| 4 | Consultation with the Chief Commissioner and Board, if required | 15 | 62 |

| 5 | Consultation with the Standing Counsel | 10 | 72 |

| 6 | Final Decision by the Commissioner to file Appeal in the High Court | 3 | 75 |

| 7 | Sending appeal folder to the Standing Counsel for drafting Appeal Memo by Commissioner |

1 | 76 |

| 8 | Drafting of Appeal Memorandum by the counsel | 30 | 106 |

| 9 | Obtaining Appeal Memorandum from Counsel, vetting, preparation of sets with annexures in the office of the Counsel and sending to the Standing counsel for filing | 10 | 116 |

| 10. | Actual filing in the High Court Registry | 2 | 118 |

| 11. | Intimation of Diary/ Lodging No to the Office of the Commissioner and making of the entries in the relevant records and registers |

2 | 120 |

Annexure 4: Proforma for Recommendation by the Chief Commissioner (AR)

| 1 | Appeal No | |

| 2 | Cause title | |

| 3 | CESTAT Final order number and date | |

| 4 | Issue involved (in brief) | |

| 5 | Submission of the AR before the Bench | |

| 6 | Decision of the Bench | |

| 7 | Reasons for filing appeal against the order |

Annexure 5: Proforma for examination of CESTAT order by the Commissioner/ Chief Commissioner

| S. No. | Points | Particulars | ||||

| i | Name and address of the assessee | |||||

| ii | Period of Dispute | |||||

| iii | CESTAT Order No. and date of the order | |||||

| iv | Date of receipt of the order in the office of Commissioner | |||||

| v | Who was the Appellant (Please tick the applicable) | Department | ||||

| Assessee | ||||||

| Both | ||||||

| vi | Amount involved in the Appeal | Duty/ Tax | ||||

| Interest | ||||||

| Fine | ||||||

| Penalty | ||||||

| vii | Amount confirmed by the Tribunal in favour of Department |

Duty/ Tax | ||||

| Interest | ||||||

| Fine | ||||||

| Penalty | ||||||

| viii | Whether issued involved includes the issue relating to the determination of any question having a relation to the rate of duty of excise or to the value of goods for purposes of assessment | |||||

| ix | Issue Involved | Decision in OIO/ OIA | Decision of Tribunal |

Whether issue is covered by any decision of High Court/ Supreme Court | ||

| x | Whether on any of the issues mentioned in (viii) matter is being agitated before the High Court or Supreme Court. If “yes”, give the details of the cases. | |||||

| xi. | Whether on any of the issues mentioned in (viii) matter covered by a Board Circular/ Instruction. If “yes”, give the details. | |||||

| xii. | Whether on any of the issues mentioned in (viii) matter is related to an audit objection. If “yes”, give the details | |||||

| xiii. | Whether the order of the Tribunal in any way contrary to the facts and evidences adduced by the Department. | |||||

| xiv | Is there any prosecution proposal under consideration or pending in respect of the issues and persons involved in this case? | |||||

| xv | If the order of the Tribunal is acceptable in respect of some issues please indicate the same along with reasons for the same. | |||||

| xvi | Issues in respect of which the order of Tribunal is not acceptable and the reasons for the same | |||||

| xvii | Total impact on the duty amount, in view of the recommendations made at “xvi” | |||||

Commissioner

Chief Commissioner

Annexure 6: Proforma for making final recommendations against the order of CESTAT

| i | Order of the Tribunal is Acceptable on merits in respect of the issues at “xv” in proforma in Annexure 5 | |

| ii | Order in respect of the issues mentioned at “xvi” in proforma in Annexure 5 is not acceptable on merits. | |

| iii. | Though the order is not acceptable in respect of certain issues mentioned at “ii” above the appeal is not recommended in view of the low amount involved, (amount being below the prescribed threshold limit). | |

| iv | Appeal is recommended in respect of the issues mentioned at “ii” above. | |

| v | Whether the appeal is to be filed before Supreme Court or High Court. | |

| vi | Question of Law to be agitated in the appeal being filed before the High Court or Supreme Court. |

Commissioner

Chief Commissioner

Annexure 7: Proforma for giving the details of Connected Matters.

| S No | Description | Details | |||

| 1 | Name of Commissionerate | ||||

| 2 | Cause title | ||||

| 3 | Order No. and date of impugned order | ||||

| 4 | Details of cases relied upon by the CESTAT / High Court | ||||

| Cause Title | Citation/ Order No and date | If challenged in Supreme Court, CA or CAD No./ SLP No Board Reference No. If challenged in High Court, appeal No. | Present Status | ||

| 5 | If some of the matters mentioned in 4 have been disposed of give the details of the decision | ||||

| 6 | Whether the orders mentioned in 5 have been accepted by the Department. | ||||

| 7 | Details of the decisions relied for recommending the Appeal | ||||

| Cause Title | Citation/ Order No and date | If challenged in Supreme Court, CA or CAD No./ SLP No Board Reference No. If challenged in High Court, appeal No. | Present Status | ||

| 8 | If some of the matters mentioned in 7 have been disposed of give the details of the decision | ||||

| 9 | Whether the orders mentioned in 8 have been accepted by the Department. | ||||

Commissioner

Chief Commissioner

Annexure 8

| Appeals to the CESTAT under Section 35E of Central Excise Act,1944, Section 129D of Custom Act, 1962 & Section 86(2) of Finance Act,1994 | ||||

| S.No | Stages | No. of days | ||

| Absolute | Cumulative | |||

| 1 | Receipt of the Order of the Commissioner in the Office of Jurisdictional Chief Commissioner | 0 | 0 | |

| 2 | Making the entry of the Order in the relevant records by the Review Branch | 1 | 1 | |

| 3 | Processing of the file in the Review Section in the office of Chief Commissioner | 15 | 16 | |

| 4 | Forwarding of the Orders along with all the relevant material to the Committee of Chief Commissioners | 2 | 18 | |

| 5 | Decision to be taken by the Committee of the Chief Commissioners | 15 | 33 | |

| 6 | In case of the difference of opinion, the Committee should make the reference to the Board, stating the point of differences | 2 | 35 | |

| 7 | Processing of the File in the Review Section and decision by the Board | 15 | 50 | |

| 8 | Communication of the decision of the Board to the Committee | 5 | 55 | |

| 9 | Communication of the decision of the Committee/ Board to contest the order of the Commissioner along with properauthorization to the Officer responsible forfiling the appeal | 5 | 60 | |

| 10 | Preparation of the Appeal and the Paper book in proper format | 10 | 70 | |

| 11 | Filing of the Appeal by the Authorized officer to the Registry of CESTAT | 15 | 85 | |

| 12 | Intimation about filing the appeal along with the Appeal No, Diary/lodging to the Review Branch | 2 | 87 | |

| Section 35 B(2) of Central Excise Act,1944, Section 129 A(2) of Custom Act, 1962 & Section 86 (2A) of Finance Act,1994 | ||||

| 1 | Receipt of the Order of the Commissioner (A) in the Office of Jurisdictional Commissioner | 0 | 0 | |

| 2 | Making the entry of the Order in the relevant records by the Review Section | 1 | 1 | |

| 3 | Processing of the file in the Review Section of the Commissionerate | 15 | 16 | |

| 4 | Forwarding of the Orders along with all the relevant material to the Committee of Commissioners | 2 | 18 | |

| 5 | Decision to be taken by the Committee of the Commissioners | 5 | 23 | |

| 6 | In case of the difference of opinion, the Committee should make the reference to the Jurisdictional Chief Commissioner, stating the point of differences | 2 | 25 | |

| 7 | Communication of the decision of the Chief Commissioner to the Committee | 5 | 30 | |

| 8 | Communication of the decision of the Committee to contest the order of the Commissioner (Appeals) along with proper authorization to the Central Excise Officer responsible for filing the appeal | 5 | 35 | |

| 9 | Preparation of the Appeal and the Paper book in proper format | 10 | 45 | |

| 10 | Filing of the Appeal by the Authorized Officer to the Registry of CESTAT | 15 | 60 | |

| 11 | Intimation about filing the appeal along with the Appeal No, Diary/lodging to the Review Branch | 2 | 62 | |

Annexure 5: Proforma for examination of CESTAT order by the Commissioner/ Chief Commissioner

| S. No. | Points | Particulars | |||

| i | Name and address of the assessee | ||||

| ii | Period of Dispute | ||||

| iii | Order No. and date of the order | ||||

| iv | Date of receipt of the order in the office of Commissioner | ||||

| v | Who was the Appellant (Please tick the applicable)

(applicable only in case of order of |