Poornima Madhava

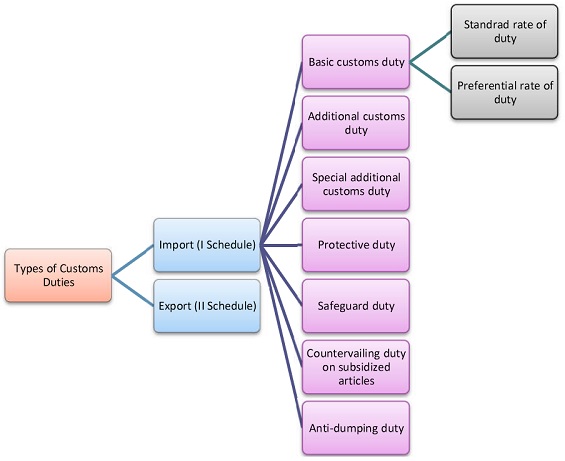

Various duties under Customs can be levied on almost all imports whereas only few goods are subject to export duty. Let us understand different types of duties under Customs Law for the purpose of import of goods.

Various duties under Customs can be levied on almost all imports whereas only few goods are subject to export duty. Let us understand different types of duties under Customs Law for the purpose of import of goods.

Let us study each of the above in detail:

Basic Customs Duty

Goods imported into India are chargeable to basic customs duty (BCD) under Customs Act, 1962. The rates of BCD are indicated in I Schedule (for Imports) of Customs Tariff Act, 1975. Education cess (EC) @2% and secondary & higher education cess (SHEC) @1% are applicable extra.

Generally, BCD is levied at standard rate of duty but if certain conditions are satisfied (below), the importer can avail the benefit of preferential rate of duty on imported goods.

Conditions for availing the benefit of preferential rate of duty:

1. Specific claim for preferential rate must be made by the importer, Import must be from preferential area as notified by the Central Government,

2. The goods should be produced/manufactured in such preferential area.

3. For more details on preferential rate of duty: http://www.cbec.gov.in/customs/cst2012-13/cs-gen/cs-gen69-93.pdf.

National Calamity Contingent Duty (NCCD)

It is levied on import of pan masala, chewing tobacco & cigarettes at different rates as applicable. It is levied @1% on PFY, motor cars, multi utility vehicles and 2-wheelers and Rs.50 per ton on crude oil vide section 169 of Finance Act, 2003.

Additional Duty of Customs or Countervailing Duty (CVD)

As per section 3(1) of Customs Tariff Act, any article imported into India is liable to duty (in addition to BCD) equal to excise duty for the time being leviable on a like article if produced/manufactured (or could be or capable of being produced/manufactured) in India.

If goods manufactured in India are exempt from excise duty, then there is no CVD – CCE Vs J K Synthetics (2000) (SC).

CVD cannot be levied, if exemption from central excise duty is based on goods manufactured by SSI units or goods manufactured without aid of power – CC Vs Malwa Industries (2009) 235 ELT 214 (SC). If the importer is the manufacturer availing benefit of SSI exemption under notification 8/2003 under Central Excise, thereby not paying excise duty on final product manufactured. Such manufacturer is not liable to pay CVD on imports, even if not liable to pay any duty under Central Excise Act, 1944.

If imported goods are used by the importer in the same factory or factory belonging to the importer, then no CVD attracted on such imported goods – CC Vs Malwa Industries (2009) 235 ELT 214 (SC).

If imported goods attract excise duty in India as per section 4A of Central Excise Act, then CVD will be calculated on MRP basis only.

CVD can be levied only when the importer has imported manufactured goods. It means CVD can be levied only if goods are obtained by a process of manufacture – Hyderabad Industries Ltd Vs Union of India (1995) (SC).

CVD can be imposed even if there is exemption from BCD.

If the importer is the manufacturer, he can claim cenvat credit of CVD.

No EC and SHEC applicable on CVD w.e.f 1/3/2015.

No CVD on Anti-dumping duty, Safeguard duty, Protective duty or Countervailing duty on subsidized articles.

Special Additional Customs Duty (Special CVD)

U/s 3(5) of Customs Tariff Act, imported goods in addition to BCD & CVD shall also be liable to Special CVD at the rate notified by Central Government (CG) (at present, it is @4%).

Special CVD is fully exempt in respect of the following imported goods:

a) Goods packed for retail sales covered under Standards of Weight & Measurement Act (Legal Metrology Act, 2009)

b) Wrist watches & pocket watches

c) Telephones for cellular networks

d) Articles of apparel excluding parts of made-up clothing accessories

A manufacturer is eligible to claim cenvat credit of Special CVD paid. A dealer is allowed refund of Special CVD provided such dealer is liable for VAT. A service provider is not eligible to avail cenvat credit of Special CVD.

Protective Duty

As per section 6(1) of Customs Tariff Act, protective duty is levied by the CG upon recommendation made by the Tariff Committee and upon CG being satisfied that it is necessary to provide protection to any industry established in India. At present, this duty is not in force. No CVD, EC & SHEC are applicable.

Safeguard Duty

As per section 8B(1) of Customs Tariff Act, safeguard duty is imposed for protecting the interests of any domestic industry in India and it is product specific. CG can impose provisional safeguard duty, pending final determination up to 200 days. Effective from 6th August 2014, if imported goods are cleared in Domestic Tariff Area (DTA) then safeguard duty is payable. No CVD, EC & SHEC are applicable.

Countervailing Duty on Subsidized Articles

As per section 9 of Customs Tariff Act, it is levied on articles which are imported by getting subsidies from other country. No CVD, EC & SHEC are applicable.

Anti-dumping Duty

As per section 9A of Customs Tariff Act, it is imposed on imports of a particular country. It is country specific. Dumping exists when a product is exported from one country to another at a price which is less than its normal value prevailing in the exporting country. The difference between the normal value and the export price is the dumping margin based on which anti dumping duty is imposed. No CVD, EC & SHEC are applicable.

Illustrations

Illustration 1 (computation of customs duty on import):

The following information is furnished by X on 8th June 2015 in respect of machinery imported from USA:

Assessable Value: Rs.11,00,000

Basic Customs duty: 7.5%

Excise duty chargeable on similar goods in India as per tariff rate: 12.5%

Additional duty of customs u/s 3(5) of CTA: 4%

Calculate the total customs duty payable by X.

Solution 1:

| Particulars | Amount in Rs. | Amount in Rs. | Remarks/Working |

| Assessable value | 11,00,000 | ||

| Add: BCD @7.5% | 82,500 | 82,500 | |

| Add: NCCD | – | Not applicable | |

| Subtotal | 11,82,500 | ||

| Add: CVD @12.5% | 1,47,813 | 1,47,813 | 11,82,500 x 12.5% |

| Add: EC & SHEC | – | Not applicable w.e.f 1/3/15 | |

| Subtotal | 13,30,313 | ||

| Add: EC & SHEC @3% | 6,909 | 6,909 | 2,30,413 x 3% |

| Subtotal | 13,37,222 | ||

| Add: Special CVD @4% | 53,489 | 53,489 | 13,37,222 x 4% |

| Value of imported goods | 13,90,711 | ||

| Value of total customs duty | 2,90,711 |

Illustration 2 (computation of anti-dumping duty):

A commodity is imported into India from a country covered by a notification issued by CG u/s 9A of CTA. Following particulars are given:

Assessable value: USD25,250

Quantity imported: 500 kg

Exchange rate applicable: Rs.64 = USD1

BCD: 12%, EC & SHEC as applicable

As per the notification, anti-dumping duty will be equal to the difference between the cost of commodity calculated @USD70 per kg and the landed value of the commodity imported. Calculate anti-dumping duty and total customs duty payable.

Solution 2:

| Particulars | Amount in Rs. | Amount in Rs. | Remarks/Working |

| Assessable value | 16,16,000 | 25250 x 64 | |

| Add: BCD @12% | 1,93,920 | 1,93,920 | |

| Add: NCCD | – | Not applicable | |

| Subtotal | 18,09,920 | ||

| Add: CVD @12.5% | – | Not applicable | |

| Add: EC & SHEC | – | Not applicable w.e.f 1/3/15 | |

| Subtotal | 18,09,920 | ||

| Add: EC & SHEC @3% | 5,818 | 5,818 | 1,93,920 x 3% |

| Subtotal | 18,15,738 | ||

| Add: Special CVD @4% | – | Not applicable | |

| Value of imported goods (Landed value) | 18,15,738 | ||

| Market value of imported goods | 22,40,000 | 500 kg x Rs.64 x USD70 | |

| Anti-dumping duty | 4,24,262 | 4,24,262 | 22,40,000 – 18,15,738 |

| Value of total customs duty | 6,24,000 |

A very good effort to explain Custom Duty details. Thanks .

Dear Madam,

whether CVD Refund is also available to a importer who availed area based excise exemption on manufacturing of final products from imported material?

Custom duty under S/3(3) is missing??

Dear Madam,

In your 1 exp.you have done mistake in remark 82500+147813=230313 and you written 230413 so pleas correct mistake. Thank you.

i want to know cess will be applicable on CVD (3)(1) or not?

I want to when goods imported from bangladesh basic duty is nil and CVD is 12.5% .whether edu cess and s.&h. educess wil have to pay?

@kamakshi: Since EC & SHEC on all excisable items are exempted from 1/3/15, I suppose it applies to all items on which cess was leviable earlier.

@M K Agrawal: I could only find a circular of 2004. dov.gov.in/newsite3/cir43.asp

@anil: Yeah right, 1% landing cost is added to CIF value to arrive at assessable value. But I couldn’t exactly understand what was yr query.

@sbv: Whats makes u think the calculation is wrong? Could u pls explain?

@Sagar Patel: U r right, though calculated amount is correct, amount shown in remarks is wrong. Thanks for correcting.

hi,

Actually I want to know whether Education cess and higher education cess on CVD is exempted for all the goods or only on goods mentioned in first schedule of custom act.

Madam

I want to know when imports are CIF any port whether Barges used at anchorage for discharge of vessel in midsea and payment for barges charges are to be included in Assessable value while calculating BCD.

Pl clarify with reference to latest judgements.

Thanks & Regards.

I think every time customs add 1% landing cost on CIF value. Thereafter it adds Basic Custom duty and other duties.

Nicely done @Poornima Madhava

I strongly feel that you are wrong in showing the proper calculation of anti dumping duty. please revise if wrong or comment back

In solution of Illustration 1, in calculation of EC & SHEC @3%, in Remark Column 2,30,413 x 3% is shown instead off 2,30,313*3% . Which is Wrong in nature.

Kindly Rectify the Same.

thank You.