Case Law Details

In re Teachmint Technologies Pvt. Ltd. (CAAR Mumbai)

M/s. Tea referred to as ‘t Authority for A received in the s terms of Section applicant is seek Panel (IFP)- Au ACC, Sahar, Mzhmint Technologies Pvt. Ltd having IBC No. AAFICT91421 (hereinafter e applicant’), filed three applications for advance ruling before the Customs Authority Advance Rulings, Mumbai (CAAR, in short). The said applications were received in the secretariat of the CAAR, Mumbai on 30.09.2024, along with its enclosures in 2811 (1) of the Customs Act, 1962 (hereinafter referred to as the ‘Ace). The Applicant is seeking advance ruling on the classification of Teachmint Brand “Interactive Fiat Panel (IFP) -Automatic Data Processing Machine for import through .INCH, Nhava Sheva; ACC, Sehar and Mundra Port.

2. The applicant cant submitted as under:

2.1 The applicant is intending to import Teachmint 13rand “Interactive Flat Panel ([FP)-Automatic Data Processing Machine (Models – Teachmint X 65 Plus, Teachmint X 65 Pro, Teachmint X 7 Plus, Teachmint X 75 Pro, Teachmint X 75 Max, Teachmint X 85 Plus, Teachmint X 8 Pro, Teachmint X 86 Plus, Teachmint X 86 Pro, Teachmint X 86 Max, Teachmint X 98 Plus, Teachmint X 98 Pro, Teachmint X 110 Plus, Teachmint X 110 Pro)” (herein after ref referent as ‘subject goods’), from China. The subject good function as an all-inone (A10) comp iter system, akin to a large-sized tablet computer. It features a LCD Module with D-LED ba klit technology complemented by a user-friendly touchscreen interface. The subject item is n all-in-one (A10) computer system with touchscreen interface for input commands. The ardware specifications include an inbuilt Motherboard with a choice of either Quad Core or eta Core Micro Processor (CPU), Graphics Processing Unit, 4GB to 16GB RAM, 32GB to 768GB GB ROM and other essential characteristics for Automatic Data Processing Mac tries. The device incorporates an embedded Android system pre-loaded with Android Operati g Systems (OS).

2.2 The appllicant is of the bonafide belief that the subject goods are rightly classifiable under 8471 419 . Therefore. the present application is being filed to ascertain the correct classification fo the subject goods. under CTFI 84714190.

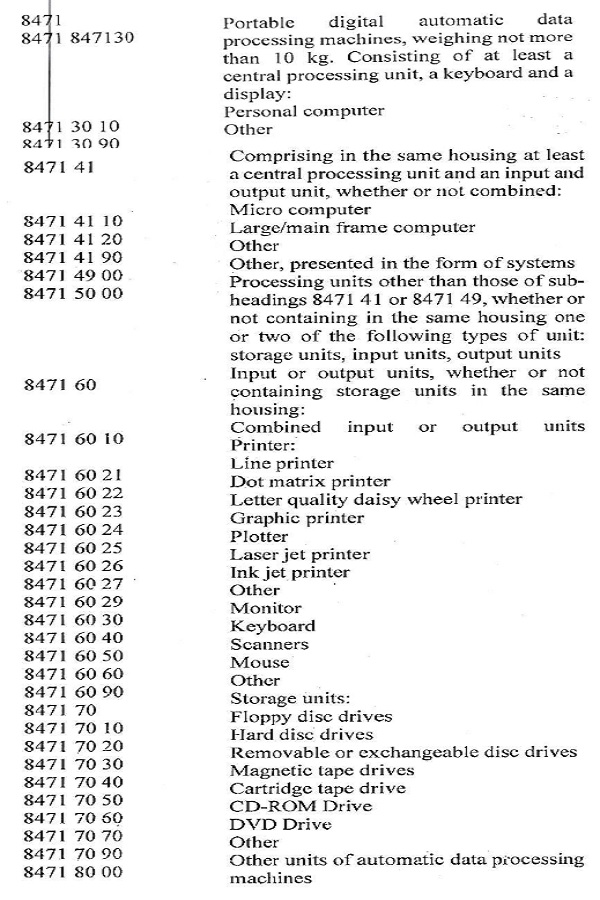

2.3 Chapter471 contains the following entries:

2.4 As per mandate under Note 6 (A) to Chapter 84 of C., Customs Tariff Act, 1975, the

ADP machine shall be capable of: –

(i) Storing the processing program necessary for the execution of the program;

(ii) Being freely programmed in accordance with the requirements of the user;

(iii) Performing arithmetical computations specified by the user; and

(iv) Executing without human intervention, a processing program which requires them to modify their execution, by logical decision during the processing run.

2.5 The s abject- goods are consisting the following character istics:

(i) An Integrated System with Central Processing Unit (CPU),

(ii) Mother Board,

(iii)Memory (RAM ± Storage),

(iv)Graphic Processing Unit,

(v) Touch Screen as Virtual Key Board as an Input Device, And

(vi) Video Display unit as an output device.

2.6. Theigital data processing machines have storage capability and also stored programs changed from job to job. Digital machines proceSs data is in’coded form. A code finite set of characters (binary cede, standard six-bit ISO code, etc.). The. data • ly automatic, by the use of data media such as magnetic tapes, or by direct reading euments, etc. There may also be arrangements for manual input by means of the input may be furnished directly by certain instruments (e.g., measuring The input data are converted by the input units into signals which can be used by and stored in the storage units. Part of the data and program or programs may be ored. in auxiliary storage units such as those using magnetic discs, magnetic tapes, machines must have a main storage capability which is directly accessible for of a particular program and which has a capacity at least sufficient to store those rocessing and translating programs and the data immcdiaLely necessary for the ssing run. Digital data processing. machines may comprise in the same housing, scessing unit, an input unit (e.g., a keyboard or a scanner) and an output unit (e.g., y unit), or may consist of a number of interconnected separate units. In the latter s form a “system” when it comprises at least the central processing unit; an input utput unit (see Subheading Note 1 to this Chapter). Since the subject goods i.e. are ADP Machine i.e. “Interactive Flat Panel (IFP) – Automatic Data Processing Machine” with all the c of the opinio Machine” ( Teachmint Teachmint Teachmint the CTHAIS Dntents as .stipulated under Note 6A of Chapter 84 of Customs Tariff, applicant is that the said goods, “Interactive Flat Panel (IFP) – Automatic Data Processing odels– Teachinint X 65 Plus,- Teachmint X 65 Pro, Teachmint X 75 Plus, 75 Pro, Teachrnint X 75 Max, Teachmint X 85 Plus, Teachmint X 85 Pro, 86 Plus, Teachmint X 86 Pro, Teachmint X 86 Max, Teachmint X 98 Plus, 98 Pro, Teachmint X 110 Pius, Teachmint X 110 Pro), merits classification under CTH/FISN 84714190.

2.7 It is Submitted that the subject goods a:c having all the essential features required for it d under the CTH 8471 4190 as an “Automatic Data Processing Unit comprising ousing at least a central processing unit and an input and output unit, whether or , other than a microcomputer and a Large or main frame computer”.

3. In terms of provisions of the Section 28-h (1) of the Customs Act, 1962 read with Sub‑ (7) of the Regulation no. 8 of the Customs Authority for Advance Rulings 2021, on the receipt of the said four applications, office of the CAAR, Mumbai pies of the said applications/suhinis:3ions tc the concerned Jurisdictional Commissionerate i.e. JNCH, Nhava Sheva; ACC, Sahar, Mumbai and Mundra as stated by the applicant at Sr. No. 13 of the CAAR-1 forms (Application form for advance rulings). Said copies were forwarded to the concerned Jurisdictional Commissioners of Customs calling upon them to furnish the re!evant records with comments, ii any, in respect of said, applications. However, office of the CAAR, Mumbai has received comments only from ACC, Sahar, Mumbai Commissionerate till date.

4. The applications were listed for hearing on 26.11.2024. The applicant was represented by Shri, Kuldeep Singh Nara (Advocate) and Shri Ashutosh Unhale, Associate Director, M/s Teachm int Technologies Pvt Ltd. They reiterated the contention submitted with the application. They contended that the subject import goods i.e. Interactive Flat Panel Display merit classification under CT1 34714190. They snhmitted that the device contains and hilids all the characteristics of an ADP Machine and comprises -input and output unit, a-central processing unit and equipped with RAM and ROM, Camera, Mic, connectivity with Wi-fi and Bluctooth and also connectable to–a computer system. They rely upoh the ORI f, Rule 3(a) Chapter note 6(A) of chapter 84 ancl–seion note of Section XVI. They also relied upon the rulings passed by this authority in previous – cases in the matter of CAAR/CUS/APPL/153/2023 and CAAR/CUS/APPL/30/2022 on similar issues. They also submitted a copy of BIS licence against most of the subject import goods (ref Licence No. R-41301507) in support of their

Shri Kumar B. Nandan, -Assistant Commissioner and Shri Dharam Singh- Appraising Officer from JNCH, Nhava Sheva appeared for hearing. They requested to allow a couple of days to file their written submission which was granted. However, no submission is submitted . by them till date. Nobody appeared from Mundra and ACC, Mumbai from department side for personal hearing.

5. Jurisdictional Commissionerate of ACC, Sahar,. Mumbai vide comments dated 26.11.2024 submitted that:

5.1 ADPMs are not a specific type of mac:;ine hut a category defined in Chapter 84, Note 6(A). For a mac{fine to qualify as an ADPM, it must meat certain criteria, including storing and processing data without human intervention.

5.2 Classification Guidelines:

General Rule I (GI? 11): Goods should be classified according to their specific function based on Chapter and Section Notes.

Chapter 84, Notes 6(D) & 6(E): AD?M classificatiob excludes certain items like monitors and projectors, even if they have ADPM features.

Section XVI, Note 3: For compeste machines (multi-functional), classification depends on the machine’s primary function. If the primary function is a display, the IFP cannot be classified asan ADPM, even if it includes ADPM features. –

5.3 Role display or p classified basf the Interactive Flat Panel (iFP): The IFP is primarily used as an interactive assentation tool, often in . educational or conference settings, and should be sd on its primary function (display), not its embedded ADPM features.

While connectivity) integrate AD. the IFP incorporates ADPM features (RAM, processor, Al, wireless its core function is display, similar to other devices like smart TVs, which also M features but are classified as televisions due to their primary display function.

5.4 Technological Evoloutionand Function: The IFP is part of the evolution from traditional s (chalkboards, whiteboards) to modern digital teaching aids, incorporating ichscreens and digital content sharing. However, its primary function remains ay, not a data processing machine. teaching too interactive to that of a displogical Evolution and Function: The IFP is part of the evolution from traditional s (chalkboards, whiteboards) to modern digital teaching aids, incorporating ichscreens and digital content sharing. However, its primary function remains ay, not a data processing machine.

The IFP’ is intended to replace projectors and traditional display systems, integrating ulti-touch, cloud connectivity, and hybrid learning capabilities, but it does not DPM or computer system.

5.5 Comparison with Similar Devices: Devices like smartphones, smart TVs, and smart grate ADPM features but are classified based on their primary function on for phones, entertainment for TVs, etc.). Similarly, the HT should be d on its primary function as a display.

Hence the product should be classified as a monitor or projector under subheading 8528 (Monitors, projectors, and similar devices) and not under CTH 8471 as an ADPM.

6. M/s Teachmint Technologies Pvt. Ltd , in their rebuttal letter dated 05.12.2024 Submitted:

6.1 That they disagree with ACC’s opinion that IFPs should be classified under CTH 8528 r projectors. They firmly maintain that IFPs are sophisticated Automatic Data achines (ADPMs) and, therefore, should he rightfully classified under CTH‑ 84714190.

6.2 That to ACC’s comments, while acknowledging the distinct nature of monitors and 1 short of definitively classifying IFPs as either. This ambiguity is particularly en that monitors and projectors fall under different tariff headings within CTH or, by definition, is an electronic visual display for computers, while a projector vice that projects images onto a surface. The ACC’s failure to specify the correct eading and their reliance on the broad category of CTH 8528 creates substantial uncertainty.

Furthermore, the ACC’s conclusion that IFPs are primarily display units seems solely based on theresence of a screen, neglecting the multifaceted functionalities of these devices.

This approach is overly simplistic and disregards the core nature of IFPs as sophisticated computing systems.

6.3 That IFPs ate far more than mere display units; they are fully functional, unrestricted All-in-One (A10) Automatic Data Pro;;essing (ADP). machines. They possess the following key characteristics:

- Integrated Hardware: IFPs incorporate a Central Processing Unit (CPU), motherboard, graphic card, mmory (RAM + Storage), Graphic Processing Unit (GPU), and a touch. screen that fe,noions as both an input and output device. These components are housed within the.display’s body, creating a compact and integrated computing system.

- Versatile SoftWare: IFPs typically ccm pre-loaded with an operating system, much like a tablet computer system. They can operate on Android or desktop operating systems such as Microsoft Windows, Apple Mac, and Chrome OS: This versatility allows’ for a wide range of applications and user customization.

- Extensive Functionality: IFPs offer a comprehensive suite offeatures, including:

- Plug-and-play compatibility with various operating systems.

- 0 Enhanced connectivity options for peripherals and devices.

- Built-in features like application marketplaces, cloud drives, and file managers.

- Soceenrecording and mirroring capabilities for collaboration..

These characteristics unequivocally demonstrate– that IFPs mee„ the conditions outlined in Chapter Note 6(A) of Chapter 84 of the Customs Tariff Act, 1975, defining ADPMs. They are capable of soaring and executing programs, performing arithmetic computations, making logical. decisions, and be: g freely. programed aceording,D user ru:airements.

Moreover, IF.Ps align with . the ‘Explanatory Notes to Heading 8471, which further clarifies the criteria for ADPMs. They possess the necessary hardware memory, free programmability, arithmetical computation capabilities, and logical decision-making abilities.

The classification of 1113s under CTII 84714190 is also strongly supported by the Harmonized System’s rules of interpretation,’ specifically Notes 3- and 4 to Section XVI and GRI 1. These rules emphasize the importance of classifying composite machines based on their principal function, in the case of IFPs, is data processing.

6.4 That their position is further strengthened by the precedent set in a similar matter before the principal bench of CE1STAT, New Delhi (FINAL ORDER NO. 50076-59077/2022). In this case, the court held that similar goods, namely Vie7.vSonic Interactive Display Systems, merle. classification under CTI 8471 41 90 as ADPMs. This ruling underscore the judicial recognition of the core functionality of such devices as data processing machines..

6.5 Based on the comprehensive arguments presental above, they urge. the Customs Authority. for Advance Rulings to classify IFPs t•nder CTI-1 84714190. This classification wets the inherent nature of il2Psos :Iophisticat’.;(1 data processing devices, aligning ionized•System Nomenciature; (,R1s, and established case law.

7. I have considered all the material’s placed before me in respect of the subject goods for. which advance ruling has been sought. I have gone through the written submissions, the wring personal hearing, comments from ACC, Sahar, Mumbai and as well as applicant. I proceed to pronounce ruling on the issue on the basis of information record. The subject goods for which advance’ ruling has been sought, its , functionality and utility etc. are broadly discussed in the aforementioned paras. The issue inolved is whether the impugned goods, namely, `Teachmint Brand “Interactive P)- can be considered as ADP machines.

7.1 The Impugned goods are basically described as an ADP machine, consisting integrated system with central Processing Unit., Mother Board, Graphic Processing Unit, Memory (RAM Lich Screen as Virtual Key Board as an input device and Video Display Unit as ice, all in one place, inside the display’s body. The subject goods typically come an operating system like a Tablet computer system, can operate on desktop terns Such as Microsoft Windows, Apple Mac, and Chrome OS, It has been the applicant that the subject goods merits classification under sub heading it satisfies all the requirements as mandated under Note 5(A) (later on referred as 6 (A) to Chapter 84 of Customs Tariff Act, 1975.

7.2 Rule of the General Rules of Interpretation (GR1) lays down that the titles of sections, sub-chapters are provided for ease of reference only; for legal purposes, shall be determined according to the terms of the headings and any relative Section or chapter Notes. The relevant CTHs and chapter notes are reproduced below:

Chapter 8471 of Customs Tariff Act, 1975 covers, “Automatic data processing machines and: magnetic or optical readers, machines for transcribing data onto data media in d machines for processing such data, not elsewhere specified or included’

6(A) states that:

“For the purpose of heading 8471, the expression “automatic data-processing machines” means, capable of

(1) storing the processing program or programs and at least the data immediately necessary for the execution of the Program;

(2) being freely programmed in accordance with the requirements of the user,

(3) performing arithmetical computations specified by the user; and

(4) executing, without human intervention, a processing program which requires o modify their execution, by logical decision during the processing run.”

In order to merit classification undo: heading 8471, it is clear that subject goods needs to satisfy the requirements of note 6(A) to Chapter 84. Therefore, there is a need to examine whether the features and specifications of the ;abject item tinder consideration meet the criteria as laid down in the relevant chapter note reproduced above.

7.3 It is understood from open available source that Automatic data processing (ADP) machines have storage capability and also stored programs which can be changed as per performance of tasks. Digital machines process data in coded form. A code consists of a finite set of characters (binary code, standard six-bit ISO code, etc.). The data input is usually automatic, by the use of data media such as magnetic tapes, or by direct reading of original documents, etc. There may also be arrangements for manual input by means of keyboards, touchscreen etc. The input ‘data are converted by the input units into signals which can be used by the machine, :1:41,-scred in the storage an.’§. Pant of the data and program or programs may be temporarily stored is auxiliary stowage. units such as those using magnetic discs, Magnetic tapes, etc. ‘But these machines must have” storage capability which is directly accessible for the execution of a particular program and which has a capacity at least sufficient to store those parts of the processing and trans–acting programs and the data immediately necessary for the current processing run. Digital aerate processing machines may comprise in the same housing, the central processing unit, an input unit (e.g., a keyboard or a scanner) and an output unit (e.g., a visual display unit), or may consist of a number of interconnected separate units. In the latter case, the units form a “system” when it comprises at least the central processing unit, an input unit, and an output unit (Subheading Note 2 to this Chapter): The goods under consideration termed as `Teachmint Brand “interactive Flat Panel (IFP)’ consists of an integrated system with Central Processing Unit, Memory Board, Graphi6 Processing Unit, Memory (RAM .-I- Storage), Touch Screen as Virtual Key Z3oard as an input device and Video Display Unit as an output device, all in One place, inside the display’s body. The subject item typically come loaded `:Ire a Tablet computer with Android Operating Systems (OS) It is observed that the subject item satisfies all the requirements as mandated under Note 6(A) to Chapter of Customs Tariff Act, 1975….

7.4 The impugned goods, as seen in para. 7.3 above, appears to be able to satisfy the requirements of as ADP machine. Note 6(9) to chapter 84 states Automatic data processing machines may be iii the form of systems eon E,,;.7 i; rig of a variable number of separate units. 6(C) to chapter 84 specifies the conditions for a unit to be classified as being part of an automatic data processing system. Note 6(d) to chapter 84 lists certain separately presented products that are to be excluded from heading 8471, even i,rthey can he classified as part of an ADP System. Note 6(E) to chapter 84 memory :hat a machine incorporating or working in .conjunction with an automatic data process iris machine and performing a specific function other than data processing are to be classified in the–headings appropriate to their respective function§ or failing that, ill residual headings. However, from the characteristics, working and features of the impugned item, it appears that these arc not units of ADP machines, but ADP machines themselves.

8. Based the comments from the Cornmissioncrate of Customs, ACC, Sahar, Mumbai, application for an advance ruling, it is observed that the classification of the lat-Panel (IFP) under [reading 8528 has been preferred over the claimed uncle; heading 8471. This preference is primarily based-on the fact that an IFP is t touchscreen display commonly used in meeting rooms and collaborative spaces. rt IF.PD functions as an interactive whiteboard (IWB). As per Note 6(D) to the Customs Tara heading 8471 does not cover monitors and projectors that orate television reception apparatus when presorted separately, even if they meet specified under Para (C) of the same Naze. Further, Para (E) of the Note clarifies or apparatus working in conjunction with an automatic data processing machine g functions beyond data processing must be classified according to their specific nder a residual heading if no specific classification applies.

Moreover, upon reviewing the comments fi•om’the Commissionerate, it is evident that been placed on display function of Interactive Flat-Panel (MP), which has led to n that the essential or -primary function of the product should be based on its ileitis. However, it appears that the significance of the word “Interactive” has not -plored. The term “Interactive” is crucial because it highlights the product’s multifunctionality, which extends beyond a mere display function. The interactivity of the IFP it meets the criteria set forth in Chapter Note 6(A) of Chapter .84; which outlines nets for an item to be classified as an “automatic data processing machine,” An built-in input, output, and processing units, is capable of performing various king it a multifunctional device rather than a simple display. The same view has this authority in similar cases referred in para 4 of this ruling. Similarly, Customs Advance Rulings, New Delhi In case of Mi./s Soperton Electronics Pvt. Ltd.: AR/Del/Soperton/31/2023 dated 04.12.2023 has taken the same view. I further „Junction by the competent court against rulings are brought to the notice of this emphasis ha• the conclusion display cape been fully e multifunction suggests that the require 1FP, with its functions, m been taken b Authority fo Ruling No. find that no authority.

9. Furth Ltd., the judgment of CESTAT, New Delhi in the case of Ingram Micro India Pvt.Ltd., offered [leading 847 India P. Ltd. no doubt the appellant, offered detailed explanation for classifying goods similar to the subject goods under 7 In the case of Customs Appeal No. 50708 and 50709 of 2021 (M/s Ingram Micro vs Principal Commissioner of Customs), the Hon’ble CESTAT held that there is goods in question should he classified under CTI 84714190, as claimed by the err than under CTI 85285200, as proposed by the Department.

10. From the facts on the record and forgoing discussion, it is observed that the conditions mandated under Note 6 (A) to Chapter 84 of Customs Tariff Act, 1975 are fulfilled by the consideration for which the advance ruling is sought. Technical literature available rays the subject goods as an A11-;n-ate (AIO) which is a fully functional ADP operates without restrictions. The AIO is equipped with hardware and software it to perform without artificial constraints general computing tasks, where users or allow are free to a remove applications of their choice.

11. In view of these facts, I find that “Interactive Fiat Panel (IFP) – Models- Teachrnint X 65 Plus, Teachmint X 65 Pro, “Feachiniiit X 75 Plus, Teachmint X 75 Pro, Teachmint X 75 Max, Teachmint X 85 Plus, Teachmint X 85 Pro, Teachmint X 86 Plus, Teachrnint X 86 Pro, Teachmint X 86 Max, Teachmint X 98 Plus, Teachmint X 98 Pro, Teachmint X 110 Plus, Teachmint X 110 Pro) merit classification under Heading 8471 and more specifically under CTI 8471 41 90 of the first schedule to the Customs Tariff Act, 1975.

12. rule accordingly.

(Prabhat K. Rameshwaram)

Customs Authority for Advance Rulings,

Mumbai