INSURANCE REGULATORY AND

DEVELOPMENT AUTHORITY OF INDIA

IRDAI/ INT/ GDL/ 146/ 05/ 2021

24th May, 2021

GUIDELINES ON STANDARD PROFESSIONAL INDEMNITY POLICY FOR INSURANCE BROKERS/ CORPORATE AGENT/ WEB AGGREGATORS/ IMF

1. Preliminary

The insurance intermediaries engaged in solicitation and distribution of insurance products, viz., Insurance Brokers, Corporate Agents, Insurance Web Aggregators, Insurance Marketing Firms are required to take Professional Indemnity Insurance Policies in order to get themselves indemnified from the claims lodged against them, arising out of the contingencies mentioned in the regulations governing them. There have been numerous instances where the policy taken by the intermediary do not comply with the Regulatory provisions.

2. Objective

The objective of these guidelines is to specify the professional indemnity policy that meets the regulatory requirements.

3. General

These Guidelines for Professional Indemnity Policy for Insurance Brokers, Corporate Agents, Insurance Web Aggregators and Insurance Marketing Firms are issued in exercise of the powers conferred upon the Authority under clause (i) of sub section (2) of Section 14 of IRDA Act, 1999.

4. Guidelines on Standard Professional Indemnity Policy for Insurance brokers/ Corporate Agents/ Web Aggregators/ IMF

a. The standard professional indemnity policy shall have the mandatory covers as specified in these Guidelines which shall be uniform across the market.

b. The standard professional indemnity policy shall comply with all extant provisions as per guidelines Ref. IRDAI/NL/GDL/F&U/030/02/2016 dated 18th February, 2016 as amended from time to time.

c. Every General Insurer, who has been issued a Certificate of Registration to transact General Insurance Business, shall endeavour to offer this Standard Professional Indemnity for insurance brokers, corporate agents, web aggregators and insurance marketing firms.

5. Index

| S.No. | Item | Page No. |

| 1 | Section — I – General Rules and Regulations | 3 |

| 2 | Section — II – Standard Proposal Form | 5 |

| 3 | Section — III – Standard Policy Form | 11 |

Sd/-

(S.N. Rajeswari)

Member (Distn)

SECTTION I

PROFESSIONAL INDEMNITY

(INSURANCE BROKER/CORPORATE AGENT/WEB AGGREGATOR/IMF)

GENERAL RULES AND REGULATIONS

1. Applicability

The Professional Indemnity Policy (Insurance Brokers/ Corporate Agents/ Web Aggregators/ IMF) contained in these guidelines meets the regulatory requirements as specified in various insurance intermediaries regulations.

Any proposals beyond these may be considered by the insurance companies on merits. Premium, rates and other terms and conditions for such covers may be decided by the insurance companies as per their as per internal underwriting guidelines

2. Effective date

These Guidelines will come into force from 1st July, 2021.

3. Standard Proposal Form

The guideline specifies the proposal form that may be used by the insurers for underwriting the risk.

4. Standard Policy Form

All Policies, fresh and renewals, issued in the specified professional indemnity will meet the regulatory requirements of various insurance intermediary regulations.

5. Liabilities Covered

Policies issued shall cover all damages resulting from any claim for breach of duty of the insured, fraud and dishonesty of any employee which the Insured becomes legally liable to pay arising out of claims first made in writing against the Insured during the policy period including legal costs and expenses incurred with prior consent of Insurers, subject always to the limits of indemnity and other terms, conditions and exceptions of the policy. The ratio of limit of indemnity any one accident to any one year shall not exceed 1:1.

6. Policy Period

An insurer shall issue an annual policy to the insurance intermediary. The insurer shall endeavour to issue long term policy valid for the period of certificate of registration.

7. Premium Rates

The premium rates shall be determined by the insurers depending upon various risk factors and its Board approved underwriting policy.

The Business Turnover/ fees figure wherever required shall be accurately assessed and declared by the proposer at inception of the policy.

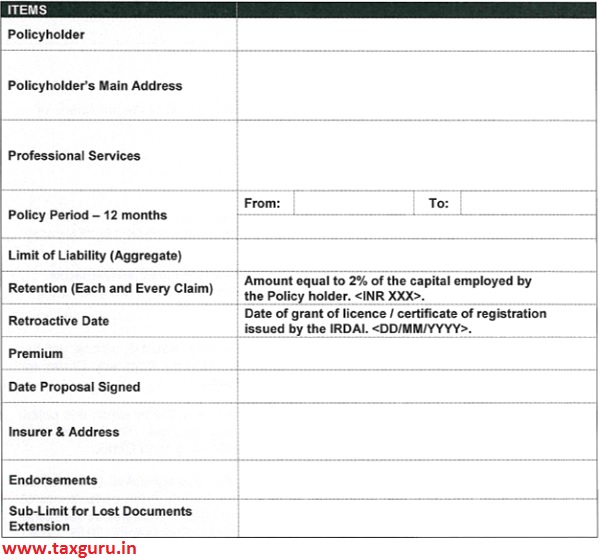

8. Retroactive Date

Retroactive Date is the date on which IRDAI has issued a license or certificate of registration to the intermediary. Should the limits under the policy be increased in the subsequent renewal, the date from which higher limits have been obtained shall be considered as the new retroactive date for the increased limits only.

9. Penalty Provision for Non-Purchase or Break in Policy

Since all insurance intermediaries for solicitation and distribution must mandatorily purchase a professional indemnity policy and the retroactive date is also from the date of granting certificate of registration by IRDAI, penal provisions shall become applicable in case the prospective insured has not purchased/ had a break in policy continuity.

During the gap period, subject to no known or reported losses/claims declaration a base rate + 5% over and above the repo rate on the premium due may be charged by the insurers for maintaining policy continuity.

SECTTION I

PROFESSIONAL INDEMNITY

(INSURANCE BROKER/CORPORATE AGENT/WEB AGGREGATOR/IMF)

PROPOSAL FORM

Insurance/ Re-Insurance Brokers/ Corporate Agent/ Web Aggregator/ Insurance Marketing Firm – Professional Indemnity Proposal Form

Notice

1. This is a proposal for a contract of Insurance. The proposal must be completed, signed and dated but completion does not bind you or the Insurer to enter into any contract of Insurance. If space is insufficient to answer any questions fully, please attach a signed continuation sheet.

2. All facts material to the proposed insurance must be disclosed, fully and truthfully to the best of your knowledge and belief. Failure to do so may make the contract of Insurance voidable or severely prejudice your rights in the event of a claim.

PROPOSER DETAILS

1. Name of company or entity (Insured):

2. Address of registered or principal office:

3. Type of Intermediary: (‘1)

| Direct Broker | |

| Re-Insurance Broker | |

| Composite Broker | |

| Corporate Agent | |

| Web Aggregator | |

| Insurance Marketing Firm (IMF) |

4. Website Address/Official e-mail ID:

5. Year & Date of Establishment:

6. IRDA Licence No. and Validity:

7. State the principal business activities for which insurance is desired:

8. State the capital employed in the entity as per last financial year audited balance sheet:

9. Has any change by way of merger, take-over or change of name occurred in the last 5 years?

If Yes, please provide details

10. Please provide details of Directors, partners or principals of the business

| Name | How long a Principal/Director/Partner? | Relevant Qualification and Year of Qualification |

11.a. Please provide details of offices or subsidiaries that are to be covered by this insurance:

b. Does the entity own any foreign subsidiary? If Yes, please give details:

12. Holding Pattern of the Entity

Private/Public (%):

FDI (%):

Institutional/Non-Institutional (%) :

13. Please detail the business’s gross Turnover/Fees for the last 3 Financial years and an estimate for the next financial year:

| Year | India | USA/Canada | Rest of World | TOTAL |

| Estimate for next Financial Year |

14. Please provide an estimate in percentage of total annual fees for the last complete Financial year from the following categories (whichever applicable)

| Type of Work | % |

| Personal Lines (incl. Motor) | |

| Commercial Motor | |

| Aviation (Small Aircraft) | |

| Aviation (Other) | |

| Marine (Small craft/Cargo) | |

| Marine (Other) | |

| Fire & Engg | |

| Other Property | |

| Liability | |

| Others (Pl. specify) | |

| Reinsurance | |

| TOTAL | 100%. |

15.1s this business split representative of the Firm’s business over the previous three years? Yes/No

If No, please provide details:

16. Are any substantial changes in the % amounts shown above likely during the next 12 months? Yes/No

If yes, please provide details:

17.1f the company places Commercial Property Insurance, provide details in respect of the three largest placements

| Client | Class of Insurance | Sum Insured |

18. If the company places Commercial Lines (excluding Fire & Perils), Marine or Aviation Insurance, provide details in respect of three largest placements

| Client | Class of Insurance | Sum Insured |

19. Does the company operate any Binding Authority (for RI brokers) arrangement whereby an Insurer or Underwriter has granted the company authority to either quote terms, set rates or handle claims without referral? Yes/No

If Yes, please provide details:

20. In respect of the Binding Authorities referred above:

a. Are all the Binding Authorities in written form? Yes/No

b. Do all the Binding Authorities have a specified renewal date? Yes/No

c. Do all the Binding Authorities specify those individuals who have authority to bind risks under the Binding Authority? Yes/No

d. Do all the Binding Authorities restrict the territorial limits to those risks based within India? Yes/No

21. Is the business or any partner, principal, or director connected or associated (by way of shareholding, financial interest, contract of employment or otherwise) with any other company or organization? Yes/No

If Yes, please provide details

22.

a. Does the company always obtain written references from former employees while engaging employees? Yes/No

b. Are employees receiving cash and cheques in the course of their duties are required to pay in daily? Yes/No

c. All cheques drawn for more than I NR 50,000 require two signatories Yes/No

d. Cash in hand and petty cash are checked independently of the employees responsible at least monthly and additionally, without warning, at least every six months Yes/No

e. Bank statement, receipts, and supporting documents are checked at least monthly against the cash book entries independently of the employees making cash book entries or paying into the bank Yes/No

23. Does the company offer and promote continuing training? Yes/No

If Yes, please provide details

24. Claims History

a. Does any partner, director or principal, after enquiry, aware of any claims ever having been made against the company or their predecessors in business or any of the present or former partners, directors or principals? Yes/No

b. Does any partner, director or principal, after enquiry, aware of any circumstances or occurrences which may give rise to a claim against the company or their predecessors in business or any of the present or former partners, directors or principals? Yes/No

c. Does any partner, director or principal in receipt of any complaints, whether oral or in writing, regarding services performed, products or solutions sold or provided, or advice given by you Yes/No

If Yes to any of the above, please provide full details

d. Where claims have been notified to the Insurer/ Insurers, what actions have been taken to prevent occurrence of such claim scenario?

25. Previous Insurance

a. Please give details of existing Professional Indemnity Insurance for the company: Policy Period

Insurer

Limit of Indemnity

Policy Excess

Premium M

Territory/Jurisdiction

b. Has any proposal for Professional Indemnity Insurance made on behalf of the company or any predecessors in the business, or present partners/directors/principals ever been declined or has such insurance ever been cancelled, renewal refused or special terms imposed? Yes/No

If Yes, please provide details

c. Had there been any break in Continuous Policy coverage since registration of the Company? Yes/ No

If yes — Period to be specified and Reasons thereof to be given

26. Please provide Limit of Indemnity for which insurance is required. INR and ratio AOA : AOY = 1 : 1

27. For IMF, List of ISPs (Insurance Sales Person) and FSEs (only in the context of offering insurance services) to be given:

28. Do you have a Cyber policy? Please give details Would you like to cover Computer and Electronic crime under this policy?

29. Would you like to cover Computer and Electronic crime under this policy?

30. If yes, please give the Limit of Indemnity.

31. Total Premium:

Add – GST:

TOTAL:

I/We, hereby declare that the particulars contained herein are true and correct and that no material fact has been withheld, misstated or misrepresented and also that this proposal cum schedule forming part of the company’s standard policy shall be basis of contract between me/us and the insurance company.

PLACE

DATE

Signature of Authorized representative

PROHIBITION OF REBATES

The following is the copy of section 41 of the insurance Act,1938.

1. No person shall allow or offer to allow either directly or indirectly as on inducement to any person to take out or renew or continue an insurance in respect of any kind or risk relating to lives or property in India any rebate of the whole or part of commission payable or any rebate or the premium – shown on the policy nor shall any person taking out renewing continuing a policy except any rebate as may be allowed in accordance with the published prospectuses or tables of the insurer.

2. Any person making default in complying with the provisions of this section shall be punishable with fine which may extend to ten lakhs rupees.

Note: The Liability of the company does not commence until the proposal form has been accepted and full premium has been paid.

SECTION – III

PROFESSIONAL INDEMNITY

(INSURANCE BROKER/ CORPORATE AGENT/ WEB AGGREGATOR/ IMF)

POLICY FORM

Schedule Policy Number:

Issued at > this > day of > 200

Signed by______ for and on behalf of the Insurer.

……………………………………………………… Authorised Signatory

| Notice

This is a claims made insurance policy. This policy will only apply to Claims first made against the Insured by a Third Party and reported to the Insurer during the Policy Period. The limits of liability available to pay judgments or settlements shall be reduced by amounts incurred for legal defence. Further, please note that the amounts incurred for legal defence shall be applied against the Retention amount. |

In consideration of the payment of the Premium and subject to all of the provisions of this policy, the Insurer agrees as follows.

Covers

| Professional Liability | The Insurer will pay on behalf of any Insured all Damages resulting from any Claim for any Breach of Duty of the Insured. |

| Fraud/Dishonesty | The Insurer will pay on behalf of any Insured, who is not the actual perpetrator, all Damages resulting from any Claim for Fraud/ Dishonesty of any Employee. |

| Defence | The Insurer has the right to defend any Claim which this policy may respond to under its Covers or Extensions. The Insurer shall pay Defence Costs incurred in defending such Claim. |

The Insurer is under no obligation to pay Loss, unless the Wrongful Act: (i) first takes place on or after the Retroactive Date; and (ii) is committed solely in the performance of or failure to perform Professional Services as per IRDAI (Insurance Brokers) Regulations, 2018, IRDAI (Registration of Corporate Agents) Regulations, 2015, IRDAI (Insurance Web Aggregator) Regulations, 2017 and IRDAI (Insurance Marketing Firm) Regulations, 2015 respectively.

Extensions

Court Attendance for any person described in (i) and (ii) below who actually attends court as a witness in connection with a Claim notified under and covered by this policy, Defence Costs will include the following rates per day for each day on which attendance in court has been required:

(i) for any principal, partner, or director Insured 25,000

(ii) for any Employee 12,500

No Retention shall apply to this Extension.

Extended Reporting Period If the Insurer cancels or does not renew this policy, other than for any breach of the terms of this policy by an Insured, the Policyholder shall have the right to a period of 60 days following the date of cancellation or expiry in which to give notice of any covered Claim first made against the Insured. That extended reporting period shall not apply if this policy or its cover has been replaced.

Lost Documents With respect to a Third Party’s Documents:

(i) for which an Insured is legally responsible, and

(ii) that, during the Policy Period, have been destroyed, damaged, lost, distorted, erased or mislaid solely in the performance or non-performance of Professional Services,

Damages shall also include costs and expenses reasonably incurred by the Insured in replacing or restoring such Documents provided that:

(a) such loss or damage is sustained while the Documents are either:

(i) in transit; or

(ii) in the custody of the Insured or of any person to whom the Insured has entrusted them;

(b) where the lost or mislaid Documents have been the subject of a diligent search by or on behalf of the Insured;

(c) the amount of any Claim for such costs and expenses shall be supported by evidence of expenditure that shall be subject to approval by a competent person to be nominated by the Insurer with the consent of the Insured; and

(d) the Insurer shall not be liable for any Claim arising out of wear, tear and/or gradual deterioration, moth and vermin, or other matters beyond the Insured’s

This Extension will be subject to a Sublimit of Liability of Rs. A separate retention of Rs. instead of the Retention will apply to each Claim covered under this Extension.

Definitions

| “Bodily Injury” | means physical injury, sickness, disease or death; and if arising out of the foregoing, nervous shock, emotional distress, mental anguish or mental injury. |

| “Breach of Duty” | means any actual or alleged negligent breach of duty, act, error, misstatements, misleading statements, breach of confidentiality or omission in the performance of or failure to perform Professional Services. |

| “Claim” | means any: (i) written demand or (ii) civil or administrative proceeding, that seeks Damages from Wrongful Acts. |

| “Damages” | means any amount that an Insured shall be legally liable to pay to a Third Party in respect of judgments rendered against an Insured, or for settlements negotiated by the Insurer with the consent of either the Insured or the Policyholder. |

| “Defence Costs” | means reasonable fees, costs and expenses incurred by or on behalf of the Insured in the investigation, defence, adjustment, settlement or appeal of any Claim. “Defence Costs” shall not mean any internal or overhead expenses of any Insured or the cost of any Insured’s time. |

| “Documents” | means all documents of any nature whatsoever including computer records and electronic or digitized data; but does not include any currency, negotiable instruments or records thereof. |

| “Employee” | any natural person who is or has been expressly engaged as an employee under a contract of employment with the Policyholder, including Insurance Sales Persons (ISP) and Financial Service Executives (FSE) and includes any persons sponsored/ authorised by the insured to handle insurance on its behalf. “Employee” shall not mean any: (i) principal, partner or director; (ii) temporary contract labour, self-employed person or labour-only sub-contractor; or (iii) an Intern |

| “Fraud/ Dishonesty” | means fraudulent or dishonest conduct of an Employee:

(i) not condoned, expressly or implicitly; and (ii) that results in liability to; the Policyholder. |

| “Infringement” | means an unintentional infringement of any intellectual property right of any Third Party, other than patents and Trade Secrets. |

| “Intern” | means a student or trainee who works, sometimes without pay, in order to gain work experience or satisfy requirements for a qualification. |

| “Insured” | means:

a. the Policyholder; b. any natural person, who is or has been a principal, partner or director of the Policyholder; c. any Employee; d. any temporary contract labour, self-employed persons, labour-only sub-contractors, solely under contract with, and under the direction and direct supervision of the Policyholder; and e. any estates or legal representatives of any Insured described in (b) and (c) of this definition; |

| “Insurer” | means the entity specified as such in the Schedule. |

| “Limit of Liability” | means the amount specified as such in the Schedule. |

| “Loss” | means Damages and Defence Costs. “Loss” shall not mean and this policy shall not cover anya. taxes;b. non-compensatory damages, including punitive, multiple, exemplary or liquidated damages;c. fines or penalties;d. the costs and expenses of complying with any order for, grant of or agreement to provide injunctive or other non-monetary relief;e. compensation, benefits or overhead of, or charges or expenses by any Insured; or f. any matters which may be deemed uninsurable under the law governing this policy or the jurisdiction in which a Claim is brought. |

| “Policy Period” | means the period of time specified in the Schedule unless the policy is cancelled in which event the Policy Period will end on the effective date of the cancellation. |

| “Policyholder” | means the entity or natural person specified as such in the Schedule. |

| “Pollutants” | means, but is not limited to, any solid, liquid, biological, radiological, gaseous or thermal irritant or contaminant whether occurring naturally or otherwise, including asbestos, smoke, vapour, soot, fibres, mould, spores, fungus, germs, fumes, acids, alkalis, nuclear or radioactive material of any sort, chemicals or waste. “Waste” includes, but is not limited to, material to be recycled, reconditioned or reclaimed. |

| “Premium” | means the amount specified as such in the Schedule and any premium adjustment reflected in an endorsement to this policy. |

| “Professional Services” | means services as specified as per IRDAI (Insurance Brokers) Regulations, 2018, IRDAI (Registration of Corporate Agents) Regulations, 2015, IRDAI (Insurance Web Aggregator) Regulations, 2017 and IRDAI (Insurance Marketing Firm) Regulations, 2015 respectively. |

| “Property Damage” | means damage to or loss of or destruction of tangible property or loss of use thereof. |

| “Retention” | means the amount specified as such in the Schedule. |

| “Retroactive Date” | means the date of grant of licence / certificate of registration issued by the Insurance Regulatory and Development Authority of India and which is specified as such in the Schedule. “Third Party” means any entity or natural person; provided, however, Third Party does not mean:

a. any Insured; or b. any other entity or natural person having a financial interest or executive role in the operation of the Policyholder. |

| “Trade Secret” | means information that derives independent economic value, actual or potential, from not being generally known and not being readily ascertainable through proper means by other persons who can obtain economic advantage from its disclosure or use. |

| “Wrongful Act” | means any Breach of Duty, Infringement, libel, slander, or Fraud/ Dishonesty. |

Exclusions

This policy shall not cover Loss in connection with any Claim:

| Antitrust | arising out of, based upon or attributable to any actual or alleged antitrust violation, restraint of trade or unfair competition; |

| Bodily Injury/ Property Damage | arising out of, based upon or attributable to Bodily Injury or Property Damage unless arising from an actual or alleged failure to achieve the legally required standard of care, diligence and expertise in performing Professional Services; |

| Contractual Liability/ Performance Guarantees | arising out of, based upon or attributable to any:

contractual liability or other obligation assumed, that goes beyond the duty to use such skill and care as is ordinarily applied to the professional services provided; (i) guarantee or warranty; or (ii) delay in performing, failing to perform or failing to complete any Professional Services, unless such delay or failure arises from a Breach of Duty by an Insured; Costs Assessment arising out of, based upon or attributable to any failure by any Insured or other party acting for the Insured to make an accurate pre-assessment of the cost of performing Professional Services; |

| Employment/ Discrimination | arising out of, based upon or attributable to any: (i) actual or alleged employment related: practices, harassment or discrimination; or (ii) intentional or systemic harassment or discrimination; |

| Insolvency | arising out of, based upon or attributable to the insolvency, administration or receivership of the Insured; |

| Infrastructure | arising out of, based upon or attributable to:

a. mechanical failure; b. electrical failure, including any electrical power interruption, surge, brown out or black out; or c. telecommunications or satellite systems failure; |

| Misdeeds | arising out of, based upon or attributable to any act which a judge, jury or other official tribunal or panel finds, or which an Insured admits, to be a criminal, dishonest or fraudulent act; and in such event, the Insurer shall be reimbursed for all Loss paid in connection with such Claim; provided, however, that this exclusion shall not apply to the Fraud/Dishonesty Cover. |

| Patent/Trade Secret | arising out of, based upon or attributable to the breach of licences concerning, infringement of or misappropriation of patents or Trade Secrets; |

| Pollution | arising out of, based upon or attributable to: (i) the actual, alleged or threatened presence, discharge, dispersal, release, migration or escape of pollutants, or (ii) any direction, request or effort to: (a) test for, monitor, clean up, remove, contain, treat, detoxify or neutralise Pollutants, or (b) respond to or assess the effects of Pollutants; |

| Prior Claims/ Circumstance | a. made prior to or pending at the inception of this policy; or

b. arising out of, based upon or attributable to any circumstance that, as of the inception of this policy, may reasonably have been expected by any Insured to give rise to a Claim; |

| Professional Services arising directly or indirectly from insured providing or failing to of FSEs | provide investment, financial advice or arrangement in relation to investments, loans or mortgages of any kind |

| Trade Debts | arising out of, based upon or attributable to any:

a. trading debt incurred by an Insured or b. guarantee given by an Insured for a debt; |

| U.S.A./Canada | claims made or pending within; or to enforce a judgment obtained in, the United States of America, Canada, or any of their territories or possessions; or |

| War/Terrorism | arising out of, based upon or attributable to any war (declared or otherwise), terrorism, warlike, military, terrorist or guerrilla activity, sabotage, force of arms, hostilities (declared or undeclared), rebellion, revolution, civil disorder, insurrection, usurped power, confiscation, nationalisation or destruction of or damage to property by or under the order of, any governmental, public or local authority or any other political or terrorist organisation. |

Claims

| Notification of Claims | The Insured shall, as a condition precedent to the obligations of the Insurer under this policy, give written notice to the Insurer of any Claim first made against the Insured as soon as practicable, during the Policy Period and in any event within 30 days of any Claim made against any Insured or any circumstances occurring during the Policy Period which might reasonably be expected to give rise to a Claim. All notifications must be in writing or by facsimile, and addressed as required in the Claims Notice Item on the Schedule. |

| Related Claims | If notice of a Claim against an Insured is given to the Insurer pursuant to the terms and conditions of this policy, then: (i) any subsequent Claim alleging, arising out of, based upon or attributable to the facts alleged in that previously noticed Claim; and (ii) any subsequent Claim alleging any Wrongful Act which is the same as or related to any Wrongful Act alleged in that previously noticed Claim, shall be considered made against the Insured and reported to the Insurer at the time notice was first given. Any Claim or Claims arising out of, based upon or attributable to (i) the same cause, or (ii) a single Wrongful Act, or (iii) a series of continuous, repeated or related Wrongful Acts, shall be considered a single Claim for the purposes of this policy. |

| Circumstances | During the Policy Period, an Insured may become aware of circumstances which may reasonably be expected to give rise to a Claim. In such event, an Insured may report the circumstances in writing to the Insurer. If in doing so, the Insured provides: (i) the reasons for anticipating the Claim, and (ii) full particulars as to dates, acts and persons involved; then any Claim which is subsequently made against an Insured and reported in writing to the Insurer alleging, arising out of, based upon or attributable to such circumstances, or alleging any Wrongful Act which is the same as or related to any Wrongful Act alleged or described in the previously notified circumstances, shall be considered first made against the Insured and reported to the Insurer at the time the facts or circumstances were first reported, if accepted by the Insurer. |

| Defence/Settlement | The Insurer does not assume any duty to defend, and the Insured shall defend and contest any Claim made against them unless the Insurer, in its sole and absolute discretion, elects in writing to take over and conduct the defence and settlement of any Claim. If the Insurer does not so elect, it shall be entitled, but not required, to participate fully in such defence and the negotiation of any settlement that involves or appears reasonably likely to involve the Insurer. The Insurer has the right at any time after notification of a Claim to make a payment to the Insured of the unpaid balance of the Limit of Liability, and upon making such payment, all obligations of the Insurer to the Insured under this policy, including, if any, those relating to defence, shall cease. |

| Insurer’s Consent | As a condition precedent to cover under this policy, no Insured shall admit or assume any liability, enter into any settlement agreement, consent to any judgment, or incur any Defence Costs without the prior written consent of the Insurer. Only those settlements, judgments and Defence Costs consented to by the Insurer, and judgments resulting from Claims defended in accordance with this policy, shall be recoverable as Loss under this policy. The Insurer’s consent shall not be unreasonably withheld, provided that the Insurer shall be entitled to exercise all of its rights under the policy. |

| Insured’s Consent | The Insurer may make any settlement of any Claim it deems expedient with respect to any Insured, subject to such Insured’s written consent. If any Insured withholds consent to such settlement, the Insurer’s liability for all Loss on account of such Claim shall not exceed the amount for which the Insurer could have settled such Claim, plus Defence Costs incurred as of the date such settlement was proposed in writing by the Insurer, less coinsurance (if any) and the applicable Retention. |

| Co-operation | The Insured will at their own cost: (i) render all reasonable assistance to the Insurer and co-operate in the defence of any Claim and the assertion of indemnification and contribution rights; (ii) use due diligence and do and concur in doing all things reasonably practicable to avoid or diminish any Loss under this policy; (iii) give such information and assistance to the Insurer as the Insurer may reasonably require to enable it to investigate any Loss or determine the Insurer’s liability under this policy. |

| Allocation | In the event that any Claim involves both covered matters and matters not covered under this policy, a fair and proper allocation of any cost of defence, damages, judgments and/or settlements shall be made between each Insured and the Insurer taking into account the relative legal and financial exposures attributable to covered matters and matters not covered under this policy. |

| Fraudulent Claims | If any Insured shall give any notice or claim cover for any Loss under this policy knowing such notice or claim to be false or fraudulent as regards amounts or otherwise, such Loss shall be excluded from cover under the policy, and the Insurer shall have the right, in its sole and absolute discretion, to avoid its obligations under or void this policy in its entirety, and in such case, all cover for Loss under the policy shall be forfeited and all Premium deemed fully earned and non-refundable. |

Purchase and Administration

| Policy Purchase | In granting cover to the Insured, the Insurer has relied upon the material statements and particulars in the proposal together with its attachments and other information supplied. These statements, attachments and information are the basis of cover and shall be considered incorporated and constituting part of this policy. If the Insurer becomes entitled to avoid this policy from inception or from the time of any variation in cover, the Insurer may at its discretion maintain this policy in full force but exclude the consequences of and any Claim relating to any matter which ought to have been disclosed before inception or any variation in cover. |

| Administration | )The Policyholder has acted and shall act on behalf of each and every Insured with respect to: (1) negotiating terms and conditions of, binding and amending cover; (2) exercising rights of Insureds; (3) notices; (4) Premiums; (5) endorsements; (6) dispute resolution; and (7) payments to any Insured. |

Limit and Retention

| Limit of Liability | The total amount payable by the Insurer under this policy shall not exceed the Limit of Liability. Sub-limits of Liability, Extensions and Defence Costs are part of that amount and are not payable in addition to the Limit of Liability. The Limit of Liability for the period provided in the Extended Reporting Period Extension is part of, and not in addition to, the Limit of Liability for the Policy Period. The inclusion of more than one Insured under this policy does not operate to increase the total amount payable by the Insurer under this policy. The Lost Documents Extension Sublimit of Liability shall be part of and not in addition to the Limit of Liability. |

| Retention | The Insurer shall only pay for the amount of any Loss which is in excess of the Retention. For the avoidance of doubt, the Retention also applies to Defence Costs. The Retention is to be borne by the Insured and shall remain uninsured. A single Retention shall apply to Loss arising from all Claims alleging the same Wrongful Act. Insurer may, in its sole and absolute discretion, advance all or part of the Retention, and, in that event, such amounts shall be reimbursed to the Insurer by the Insureds forthwith. |

| Other Insurance/ Indemnification | Unless otherwise required by law, Cover under this policy is provided only as excess over any self-insurance or other valid and applicable insurance, unless such other insurance is written only as specific excess insurance over the Limit of Liability. Nothing contained herein shall be construed to increase the Limit of Liability of this policy. To the extent that another insurance policy imposes upon an insurer a duty to defend a Claim, Defence Costs arising out of such Claim shall not be covered under this policy. |

General Provisions

| Assignment | This policy and any rights under or in respect of it cannot be assigned without the prior written consent of the Insurer. |

| Cancellation By Policyholder. | This policy may be cancelled by the Policyholder at any time only by mailing written prior notice to the Insurer. In such case, if no Claim has been made and no circumstance has been notified prior to such cancellation; Insurer shall retain the customary short rate proportion (unexpired portion of Premium less handling charges) of the Premium. Otherwise, Premium shall not be returnable and shall be deemed fully earned at cancellation. |

| By Insurer. | This policy may be cancelled by the Insurer delivering to the Policyholder by registered, certified, other first class mail or other reasonable delivery method, at the address of the Policyholder set forth in the Schedule, written notice stating when, not less than thirty (30) days thereafter, the cancellation shall be effective. Proof of mailing or delivery of such notice shall be sufficient proof of notice and this policy shall be deemed cancelled as to all Insureds at the date and hour specified in such notice. In such case, the Insurer shall be entitled to a pro-rata proportion of the Premium. Payment or tender of any unearned premium by the Insurer shall not be a condition precedent to the effectiveness of cancellation, but such payment shall be made as soon as practicable. |

| Arbitration | Any and all disputes or differences which may arise under, out of, in connection with or in relation to this policy, or to its existence, validity or termination, or to the determination of the amount or any amounts payable under this policy, shall be referred to a sole arbitrator to be appointed by the parties to the dispute within 30 days of any party giving notice of arbitration to the other(s).

In the event that the parties are unable to agree upon the identity of a sole arbitrator, the disputes or differences shall be referred to the decision of 3 arbitrators of whom one shall be appointed in writing by each of the parties within a period of 30 days after the failure to appoint a sole arbitrator and the third (who shall serve as Chairman) shall be appointed by the nominated arbitrators. In case either party shall refuse or fail to appoint an arbitrator within the aforesaid 30 days after receipt of notice in writing requiring an appointment, the other party shall be at liberty to appoint a sole arbitrator who shall thereafter be empowered to conduct the arbitration and determine the disputes or differences referred to him as if he had been appointed a sole arbitrator with the consent of both parties. The parties shall share the expenses of the arbitrator or arbitral tribunal equally and such expenses, along with the reasonable costs of the parties in the arbitration, shall be awarded by the arbitrator or arbitral tribunal in favour of the successful party in the arbitration or, where no party can be said to have been wholly successful, to the party who has substantially succeeded. The place of arbitration shall be India, the language of the arbitration shall be English, the law applicable to and in the arbitration shall be Indian law and the arbitration process will be in accordance with the provisions of the Arbitration & Conciliation Act 1996, as amended from time to time. It is a condition precedent to any right of action or suit upon this policy that the award by such arbitrator or arbitrators shall be first obtained. In the event that these arbitration provisions shall be held to be invalid then all such disputes shall be referred to the exclusive jurisdiction of the Indian courts. |

| Insolvency | Insolvency, receivership or bankruptcy of any Insured shall not relieve the Insurer of any of its obligations hereunder. |

| Plurals, Headings and Titles | The descriptions in the headings and titles of this policy are solely for reference and convenience and do not lend any meaning to this contract. Words and expressions in the singular shall include the plural and vice versa. In this policy, words in bold typeface have special meaning and are defined. Words that are not specifically defined in this policy have the meaning normally attributed to them. |

| Scope and Governing Law | Where legally permissible and subject to the U.S.A./Canada Exclusion, this policy shall apply to any Claim made against any Insured anywhere in the world. Any interpretation of this policy relating to its construction, validity or operation shall be made in accordance with the laws of India and in accordance with the English text as it appears in this policy. |

| Subrogation | If any payment is to be made under this policy in respect of a Claim, the Insurer shall be subrogated to all rights of recovery of the Insured whether or not payment has in fact been made and whether or not the Insured has been fully compensated for its actual loss. The Insurer shall be entitled to pursue and enforce such rights in the name of the Insured, who shall provide the Insurer with all reasonable assistance and co-operation in doing so, including the execution of any necessary instruments and papers. The Insured shall do nothing to prejudice these rights. Any amount recovered in excess of the Insurer’s total payment shall be restored to the Insured less the cost to the Insurer of such recovery. The Insurer agrees not to exercise any such rights of recovery against any Employee unless the Claim is brought about or contributed to by the dishonest, fraudulent, intentional criminal or malicious act or omission of the Employee. In its sole discretion, the Insurer may, in writing, waive any of its rights set forth in this Subrogation Clause. |

| Validity | This policy is not binding upon the Insurer unless it is countersigned on the Schedule by an authorised representative of the Insurer. |