“Unlock the secrets of Dematerialisation for Private Companies. Explore the latest MCA amendment, demat benefits, and the process. Understand implications and consequences under the Companies Act. Ensure compliance with expert insights.”

Introduction: In a significant move, the Ministry of Corporate Affairs (MCA) has extended the requirement of dematerialisation of securities to private companies. This article explores the implications of the recent amendment, understanding dematerialisation, its benefits, the process involved, and the consequences of non-compliance under the Companies Act.

As per Companies Act, 2013, it was mandatory for all listed company to have its shares and other securities in demat form for their smooth trading in Stock exchanges. Though MCA, vide notification dated September 10, 2018 inserted Rule 9A in the Companies (Prospectus and Allotment of Securities) Rules, 2014 (‘PAS Rules’), mandating every unlisted public company to hold and issue securities only in demat form.

Recently, MCA vide Companies (Prospectus & Allotment of Securities) Second Amendment Rules, 2023 (‘Present Amendment’), has extended such requirement to private companies. The MCA has inserted Rule 9B in PAS Rules providing for mandatory dematerialisation of securities of private companies also. Now lets us understand this topic in thorough.

What is Dematerialisation?

Dematerialization is the process of converting your physical shares and securities into digital or electronic form. The basic agenda is to smoothen the process of buying, selling, transferring and holding shares and also about making it cost-effective and foolproof. All your securities are stored in an electronic form instead of physical certificate.

What are benefits of converting securities into demat form for a company?

Safe way to hold shares of a company – cannot be defaced or mutilated or stolen.

- Convenient – can be easily transferred electronically from one entity to another.

- Instant transfer of shares on authorization

- No stamp duty on transfer of shares.

- No risk of bad delivery of shares – fake share certificates, delays, bad delivery, missing certificate, etc.,

- Minimal paperwork.

- Reduction in transaction cost and legal cost.

- Even one share can be transferred.

- Easy maintenance of ownership information and changes to address of shareholder.

- Automatic credit to account on stock split or bonus.

- Single demat account of investor can hold multiple securities.

- Better transparency of securities

Which companies are required to demat securities?

Every Company is required to Dematerialisation its shares and securities:-

- All private company

- All public company

Except Small and Government companies. i.e. small and government companies are excepted from facilitate their securities into demat form.

Whether a private company which is a holding/ subsidiary company of another private company is also covered under dematerialisation?

If a private company is a subsidiary of another private company or is a holding company of another private company, then even if paid-up and turnover falls within the parameters indicated for a small company, it will not be considered as a small company and therefore, will be required to comply with the dematerialisation.

What kind of securities are covered for dematerialization?

The word “securities” is used and therefore, it is applicable to all kinds of securities i.e., equity shares, preference shares, debentures, warrants, etc.

Which section governs the dematerialization of securities within the regulatory landscape?

This falls under the purview of The Companies Act, 2013, specifically encompassing section 134, in conjunction with sections 92, 143, 149, 178, 186, 188, and The Companies (Accounts) Rules, 2014, subject to periodic amendments.

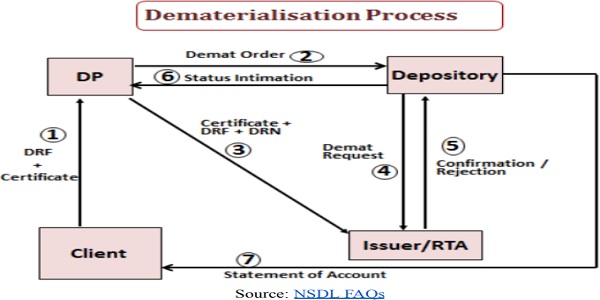

What is the process to demat securities?

The dematerialization process for securities in India involves several key steps within the framework of depositories. Here’s an overview:

- Depository Selection: Investors choose a depository to hold their securities in electronic form. In India, the two registered depositories are the National Securities Depository Limited (NSDL) and Central Depository Services (India) Limited (CDSL).

- Depository Participant (DP) Interaction: Investors cannot directly engage with depositories; instead, they must interact through a Depository Participant (DP). A DP acts as an intermediary between the investor and the depository, offering depository services.

- DP Registration: Various entities, such as public financial institutions, commercial banks, stock-brokers, clearing corporations/clearing houses, and NBFCs compliant with SEBI requirements, can register as DPs.

- Agreement Execution: To convert shares of a private limited company into demat form, both the company and its investors enter into an agreement with the depository participants.

- Electronic Holding: The depository holds the securities in electronic form on behalf of the investors. This eliminates the need for physical share certificates.

- Transaction Facilitation: DPs facilitate transactions on behalf of investors, allowing them to buy or sell securities in electronic form.

- Agreement with Investors: The company and its investors establish an agreement with the depository participants, outlining the terms and conditions for holding and transferring securities in demat form.

- Continuous Oversight: Regulatory bodies like the Securities and Exchange Board of India (SEBI) oversee the functioning of depositories and ensure compliance with regulations.

Whether the Company will be required to appoint a Registrar and Share Transfer Agent (‘RTA’)?

The role of RTA is to act as an intermediary between the issuer and the depository for facilitating dematerialisation and corporate actions undertaken by the issuer thereafter. It verifies the request received for dematerialisation from the depository participant and forwards to the Company.

However, it is not mandatory under the Act to appoint RTA if the company has an inhouse arrangement. Accordingly, where an RTA is not appointed, the Company will be required to perform the said activities to enable dematerialisation of securities held by the investors.

Whether the private companies covered under dematerialization section will be required to maintain a register of members?

No. In terms of Section 88 (3) of the Act, the register and index of beneficial owners maintained by a depository under section 11 of the Depositories Act, 1996 (22 of 1996), will be deemed to be the corresponding register and index for the purposes of the Act.

What is the last date for facilitating dematerialization of securities?

A private company, which as on last day of a financial year, ending on or after 31st March, 2023, shall, within eighteen months of closure of such financial year, comply with the provisions of this provision or

- Every private company making any offer for issue of any securities or buyback of securities or issue of bonus shares or rights offer, after the date when it is required to comply with dematerialization or

- Every holder of securities of the private company who intends to transfer such securities or who subscribes to any securities of the concerned private company whether by way of private placement or bonus shares or rights offer

What if dematerialization is not done?

There is no specific penalty specified under Section 29 of the Act and therefore, penalty as per

Section 450 of the Act will apply. As per Section 450 of the Act, company and every officer of the company who is in default will be liable to a penalty of Rs. 10,000. In case of continuing contravention, with a further penalty of Rs. 1,000 for each day after the first during which the contravention continues, subject to a maximum of Rs. 2,50,000 in case of a company and Rs. 50,000 in case of an officer who is in default or any other person.

Disclaimer: – The above article is prepared keeping in mind all the important and basic question as well as provision of the Companies Act, 2013 and Companies (Prospectus and Allotment of Securities) Rules, 2014. The author has tried to cover all the important and basic question. Under no circumstance, the author shall not liable for any direct, indirect, special or incidental damage resulting from, arising out of or in connection with the use of the information.

The Author is Corporate Consultant and provides varied array of services including Start-ups mentor, Secretarial, Legal, Trademark, taxation, Audit, GST, Book keeping and other ancillary advisory service in Delhi as well as The National Capital Region (NCR) and can be contacted through email id:- triptishakyacs2017@gmail.com and Contact Number: 91-7703890255

Author Bio

Madam,

Your above Article givres some basic information with regard to the dematerlised of shares. However my query is to you that what do you mean by Small Company. Either based on the Capital or based on the turnover. Which we have to choose.