Ind AS-115 summary

Applicable from April, 2018)

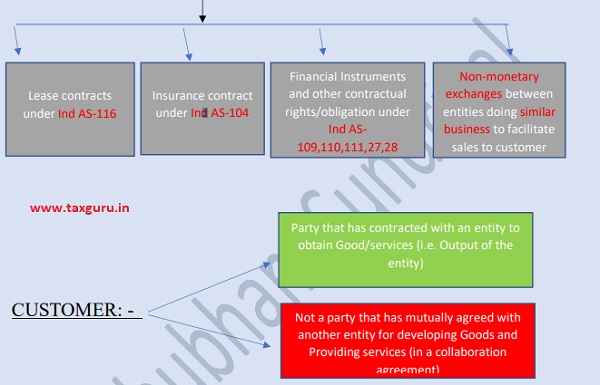

Scope- Applicable to all the contracts with CUSTOMER, except the followings-

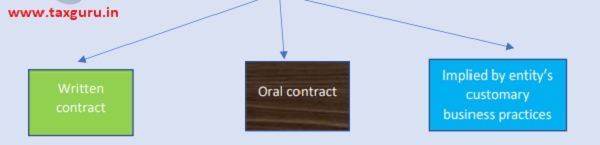

CONTRACT: – Agreement between 2 or more parties that creates enforceable rights and obligation.

–

–

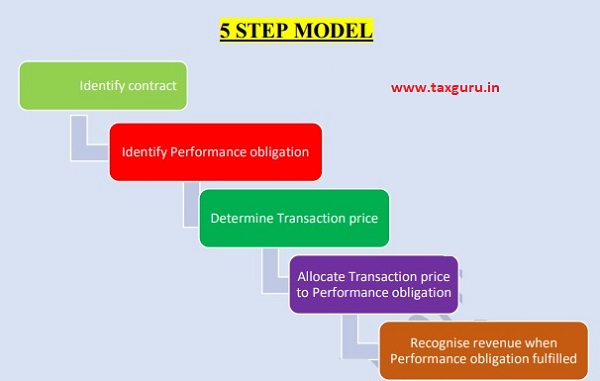

STEP-1 IDENTIFYING CONTRACT

Again 5 Key Steps- all should be satisfied

Key point- If step-1 not fulfilled and entity receive consideration from customer

↓

Recognize the REVENUE only if following 2 conditions are met

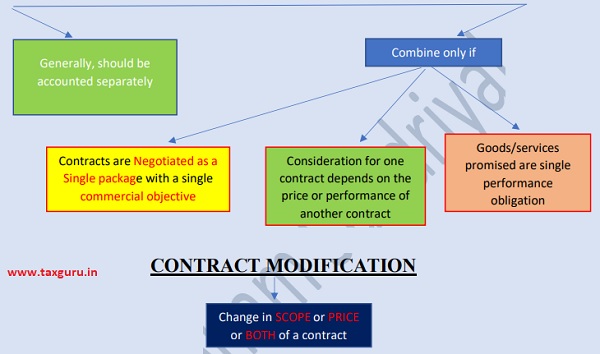

COMBINATION OF CONTRACT

CHECK WHETHER THESE 2 CONDITIONS ARE FULFILLED:-

STEP-2 PERFORMANCE OBLIGATION

PROMISE to transfer GOODS/SERVICES or SERIES of GOODS/SERVICES (same pattern of transfer to customer) that are DISTINCT

–

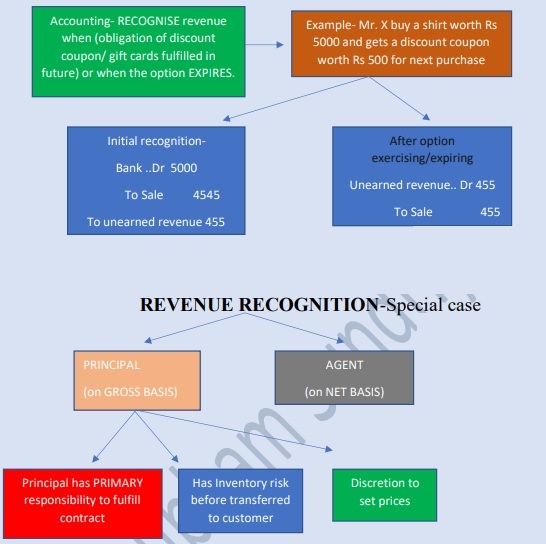

Non-Refundable Upfront Fee

STEP-3 TRANSACTION PRICE

–Consideration which an entity expects to be entitled for discharging performance obligation (excluding amount collected on behalf of 3rd party).

CONSTRAINTS IN VARIABLE CONSIDERATION

↓

Significant reversal in already recognized revenue

SIGNIFICANT FINANCING COMPONENT

↓

If the time GAP between performance obligation & payment (advance or after delivery) is SIGNIFICANT (>12 months). It will be treated as hidden loan

↓

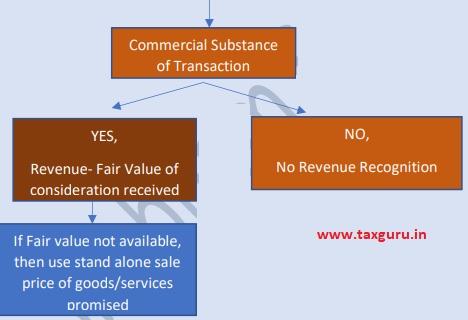

NON- CASH CONSIDERATION

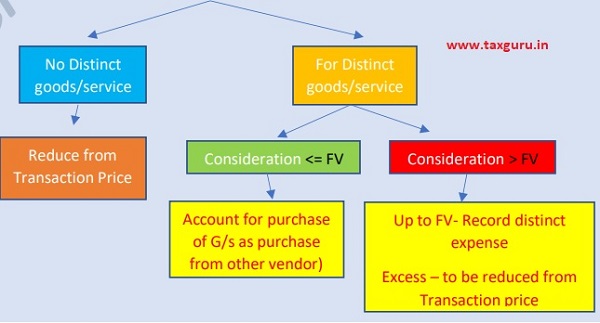

CONSIDERTAION PAYABLE TO CUSTOMER

STEP-4 ALLOCATION OF TRANSACTION PRICE TO PERFORMANCE OBLIGATION

↓

(Para 73)- Fairly depict consideration from each performance obligation on a relative standalone selling price basis except for allocating

–

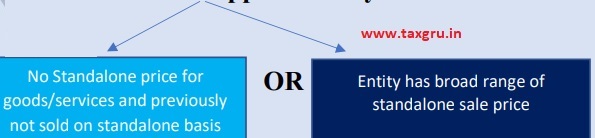

USE Residual approach only if

Key Point: – Allocate discount before applying RESIDUAL APPROACH

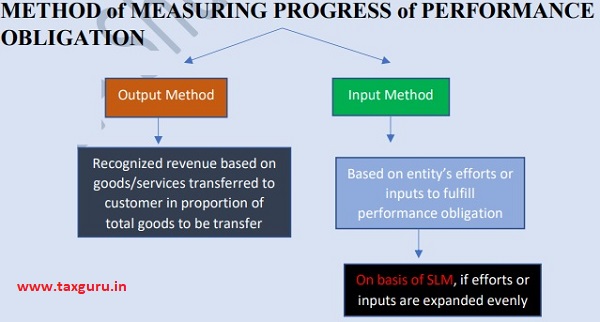

STEP-5 RECOGNIZING REVENUE WHEN PERFORMANCE OBLIGATION FULFILLED

↓

As and when CONTROL is transferred.

TRANSFER OF CONTROL

–

–

KEY NOTE- For OPTIONS, above treatment only if Option is likely to be exercised.

SERVICE CONCESSION ARRANGEMENTS

(Not a property plant and equipment)

(Ex- infra for public service such as Roads, Bridge, Tunnels etc.)

(also known as Build-operate-transfer, rehabilitate-operate-transfer, or public to private service concession agreement)

Key Point- If Operator performs >1 service such as Construction or upgradation and operation service) under a SINGLE contract, Consideration must be allocated to relative fair values of service delivered.

Author Bio

How do I become a member in Tax Guru ?

You can register at following link: https://taxguru.in/user/register.php