The Securities and Exchange Board of India (SEBI) has released a consultation paper seeking public feedback on proposals to enhance the ease of doing business concerning the additional disclosure framework for Foreign Portfolio Investors (FPIs). The paper aims to gather comments on two key proposals focusing on exemptions for certain FPI categories. Let’s delve into the details.

SEBI’s move to seek public opinions on these proposals signifies a collaborative approach towards improving regulations for FPIs. Stakeholders in the financial markets, including university funds, endowments, and FPIs, are encouraged to participate in this consultation process. By actively engaging with SEBI, industry participants can contribute to shaping a regulatory framework that balances ease of doing business with necessary disclosures and safeguards.

Securities and Exchange Board of India

Consultation paper on proposals to improve ease of doing business with respect to the additional disclosure framework for FPIs

Click here to provide your comments

1. OBJECTIVE

1.1 . The objective of this consultation paper is to seek comments/ views/ suggestions from the public on two proposals to amend the additional disclosure framework for FPIs specified under the August 24, 2023 circular. The first proposal is to exempt Category I University Funds and University related Endowments FPI that meet certain objective criteria from the requirement of enhanced disclosures. The second proposal is to exempt enhanced reporting requirements for some funds with concentrated holdings in entities with no identified promoter group, where there is no risk of breach of Minimum Public Shareholding (MPS).

2. BACKGROUND AND EXTANT FRAMEWORK

2.1. To guard against the possible circumvention of Minimum Public Shareholding (“MPS”) norms, requirements under SEBI (Substantial Acquisition of Shares and Takeover) Regulations, 2011 (“SAST Regulations”), and Press Note 3, SEBI (Foreign Portfolio Investors) Regulations, 2019 (“FPI Regulations, 2019”) were amended in August 2023, and Regulations 22(6) and 22(7) were inserted in FPI Regulations, 2019. SEBI’s related circular dated August 24, 2023 (“August circular”) mandated disclosure of granular details of all entities holding any ownership, economic interest, or control in an FPI, on a full look through basis, without any threshold, by FPIs that fulfilled any of the following criteria:

a. holding more than 50% of their Indian equity Assets Under Management (AUM) in a single Indian corporate group; or

b. individually, or along with their investor group (in terms of Regulation 22(3) of the FPI Regulations, 2019), hold more than INR 25,000 crore of equity AUM in the Indian markets

2.2. Certain FPIs, including those having a broad based, pooled structure with widespread investor base or those having ownership interest by Government or Government related investors were exempted from such enhanced disclosure requirements, subject to certain conditions.

2.3. The August circular became effective from November 01, 2023 and the FPIs, which met the specified objective criteria were provided a time period of 90 days to realign their portfolios. Thereafter, the additional disclosure requirements would start to apply and FPIs whose investments continued to exceed the prescribed threshold post expiry of timelines for realignment would be required to make disclosures within 30 trading days. Accordingly, for such FPIs that met the objective criteria as on October 31, 2024 and were not exempted, adequate disclosures need to be made on or before March 11, 2024.

2.4. Further, while the broad principles were outlined in the August circular, the detailed mechanism for independently validating conformance of FPIs with the conditions and exemptions, was spelt out in the Standard Operating Procedure (SOP) framed by the pilot Custodians and DDPs Standard Setting Forum (CDSSF), in consultation with SEBI. The SOP for implementation of SEBI circular dated August, 2023, was accordingly adopted by the DDPs/Custodians on October 27, 2023 and was uploaded on their respective websites.

3. SUGGESTIONS ON THE GRANULAR DISCLOSURE FRAMEWORK RECEIVED DURING INTERACTIONS WITH INDUSTRY PARTICIPANTS

3.1. During the implementation of the granular disclosure framework, SEBI interacted with industry participants and received several suggestions and requests for clarifications. Accordingly, clarifications were provided to the DDPs/ Custodians and the SOP was accordingly modified.

3.2. During interactions with industry participants, the case for enhancing ease of doing business in respect of Category I University Funds and University related Endowment FPIs, and in respect of FPIs with concentrated holdings in listed entities without an identified promoter was made. Since these are technically new categories of exemptions that were not explicitly covered in the previous public consultation on the subject, they are being covered here.

4. PROPOSALS

4.1. The granular disclosure framework constituting the relevant provisions of the FPI Regulations, 2019, August circular and the SOP, provides the objective criteria, disclosure requirements, exemptions and independent validation norms, with respect to the FPIs coming under the purview of the framework. The framework was conceptualized on the principles of the fund being a pooled structure with broad-based, diversified investors with pari-passu interest of all investors in the fund with an independent validation of the holdings by the DDP.

4.2. The suggestions received from the industry participants have been weighed against the aforementioned principles and proposals in this regard have been formulated accordingly and are as follows:

Proposal 1: Exemption from making the additional disclosures to university funds and universities related endowments

4.2.1. University funds and endowments receive contributions from various donors and the returns from such investments accrue to the University, rather than to the donors. Further, such funds generally enjoy tax-exempt status in their home jurisdictions, and are therefore subject to disclosure requirements to ensure that the corpus of the fund is used for the purposes for which the fund was set up. Accordingly, University Funds and University related Endowments that meet certain size, vintage, stature, tax status, disclosure of holdings, and broad-based holdings criteria may be exempted from the additional disclosure requirements.

4.2.2. Further, in terms of Regulation 5(a)(iv)(III) of the FPI Regulations, 2019, university related endowments of such universities that have been in existence for more than five years and based in FATF member countries, are eligible for registration as Category I FPI.

4.2.3. In view of the above, it is proposed to exempt university funds and university related endowments, registered or eligible to be registered as Category I FPI, from the disclosure requirements prescribed under the August Circular, subject to the following additional conditions:

i. The university is listed in the Top 200 ranking as per the latest available QS World University Rankings issued by QS Quacquarelli Symonds Limited

ii. Its India equity AUM is less than 25% of its Global AUM

iii. Its global AUM is more than INR 10,000 crore

iv. It has filed appropriate return/ filing to the respective tax authorities in their home jurisdiction to evidence that the entity is in the nature of a non-profit organisation and is exempt from tax

4.2.4. The conditions mentioned above are proposed in order to ensure that the exemption is not misused through setting up of endowments for lesser known universities in jurisdictions where no or minimal disclosures are available. Further, the AUM criteria is being prescribed to ensure that only the well-funded and diversified funds are eligible for the exemption.

Questions for public comments

1. Do you agree that the proposal to exempt university funds and universities related endowments, registered or eligible to be registered as Category I FPI, from the disclosure requirements prescribed under the August Circular is in line with the principles outlined in para 2.2 above?

2. Do you agree that the additional conditions listed in para 4.2.3 above are sufficient to avoid misuse of the proposed exemption?

Proposal 2: Exemption in case of companies with no identified promoter and low FPI holdings

4.2.5. In respect of FPIs with concentrated holdings in a single corporate group, while describing the issue of potential circumvention of regulatory requirements such as maintenance of Minimum Public Shareholding (MPS) and adherence to Substantial Acquisition of Shares and takeovers (SAST) norms, para 3.1.1 of the Board Memorandum dated June 22, 2023 read as follows:

“3.1.1 Some FPIs have been observed to concentrate a substantial portion of their equity portfolio in a single investee company/ corporate group. In some cases, these concentrated holdings have also been near static and maintained for a long time. Such concentrated investments raise the concern and possibility that promoters of such corporate groups, or other investors acting in concert, could be using the FPI route for circumventing regulatory requirements such as that of disclosures under SAST Regulations or maintaining MPS in the listed company. Further, if this were the case, the apparent free float in a listed company may not be its true free float, increasing the risk of price manipulation in such scrips.”

4.2.6. In case of listed companies without any identified promoter, the entire shareholding is classified as “public” and there is no risk of circumvention of MPS requirements. To that extent, there is room for relaxing the additional disclosure requirements for FPIs holding concentrated positions in such companies. However, the concerns regarding circumvention of SAST Regulations would still persist.

4.2.7. Note that as per the extant SAST requirements, any investor along with persons acting in concert (PAC), acquiring more than 5% shares or voting rights in a listed company is required to make the disclosures prescribed therein. Disclosures are further to be made for increments/ decrements in holding of 2% thereafter. Holdings above 25% would require an open offer to be made.

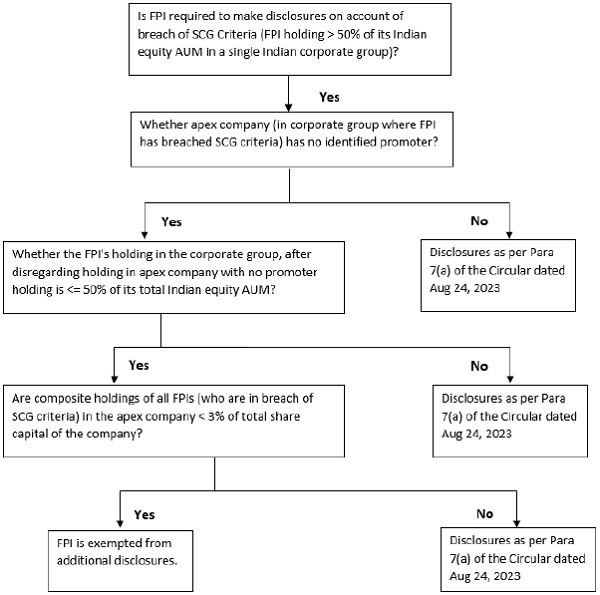

4.2.8. Consider a corporate group where the apex company, i.e., the eventual promoter/ associate to all other companies in the group, itself has no identified promoter.

4.2.8.1. Consider an FPI that has more than 50% of its India equity AUM in such a corporate group. It is proposed to relax the additional reporting requirement for such FPIs in the following manner.

4.2.8.2. If such FPI holds more than 50% of its India equity AUM in the corporate group, even after disregarding its holding in the apex company (with no identified promoter), it would come under the disclosure requirements of the August circular. The rationale for this is that even though the apex company in the group itself has no identified promoter, the FPI still holds a significant part of its portfolio in related companies that have an identified promoter.

4.2.8.3. If not, as long as the composite holdings of all such FPIs in the apex company in the group is less than 3% of the total equity share capital of the company, it would be exempted from the additional disclosure requirements.

Chart1: Flowchart illustrating exemption in case of companies with no identified promoter and low FPI holdings

4.2.8.4. The core principle behind the above formulation is that there is no risk of circumvention of MPS requirements in case of listed entities with no identifiable promoters. Further, the potential risk of circumvention of SAST Regulations through the FPI route is mitigated by adoption of an acceptable risk-threshold of 3% holding as against the extant SAST thresholds. On back-testing the formulation illustrated in Chart1 above, it is apparent that there will be no additional compliance burden on any FPI that will accrue on this account. On the contrary, the above formulation is expected to reduce the compliance burden on the industry without compromising the regulatory principles.

4.2.8.5. Custodians and depositories will track the utilisation of this 3% limit for companies without an identified promoter at the end of each day. When the 3% limit is met or breached, depositories and custodians will make this information public before start of trading the next day. Thereafter, prospective FPI positions in the company that breach the 50% concentration criteria in the corporate group will be required to either realign such positions below the 50% threshold within 10 trading days, or provide disclosures prescribed under Para 7 of the August circular; provided the aforementioned 3% cumulative FPI limit for the listed company continues to be in breach through the 10 trading days.

Questions for public comments

3. Do you agree with the proposal to keep the companies with no identified promoter and low holdings of identified FPIs, outside the scope of the granular disclosure framework?

4. Do you agree with the proposal to keep the threshold at 3% for holdings by identified FPIs in such companies?

5. PUBLIC COMMENTS

5.1. Considering the implications of the aforementioned matters on the market participants, public comments are invited on the above-detailed proposals. The comments/ suggestions should be submitted latest by March 08, 2024, through the following link:

https://www.sebi.gov.in/sebiweb/publiccommentv2/PublicCommentAction.do?doPublicComments=yes

5.2. The instructions to be followed for submitting comments on the consultation paper are as under:

INSTRUCTIONS FOR SUBMITTING COMMENTS

1. Before initiating the process, please read the instructions given on top left of the web form as “Instructions”.

2. Select the consultation paper you want to comment upon from the dropdown under the tab – “Consultation Paper” after entering the requisite information in the form.

3. Email Id and phone number cannot be used more than once for providing comments on the same consultation paper.

4. If you represent any organization other than the types mentioned under dropdown in “Organization Type”, please select “Others” and mention the type, which suits you best. Similarly, if you do not represent any organization, you may select “Others” and mention “Not Applicable” in the text box.

5. There will be a dropdown of Proposals in the form. Please select the proposals one-by-one and for each proposal please record your level of agreement with the selected proposal. Please note that submission of agreement level is mandatory.

6. If you do not want to react on any proposal, you may skip the same by selecting “Skip this proposal”;

7. If you want to provide your comments for the selected proposal, please select “Yes” from the dropdown under “Do you want to comment on the proposal” and use the text boxes provided for the same.

8. After recording your response to the proposal, click on “Submit” System will save your response to the selected proposal and prompt you to record your response for the next proposal. Please follow this procedure for all the proposals given in the dropdown.

9. Please download the pdf file, link of which is given at the bottom of the form, just before finally submitting the comments to last and final proposal. This pdf will help in case technical issue is faced while final submission of comments.

10. The final comments shall be submitted only after recording your response on all of the proposals in the consultation paper.

5.3. In case of any technical issue in submitting your comment through web based public comments form, you may contact the following through email with a subject: “Issue in submitting comments on consultation paper on proposals to improve ease of doing business with respect to the additional disclosure framework for FPIs”

a) afdconsultation@sebi.gov.in

b) Manish Kumar Jha, DGM (manishkj@sebi.gov.in)

c) Naveen Kumar, AGM (naveenkr@sebi.gov.in)

Issued on: February 27, 2024